Executive summary:

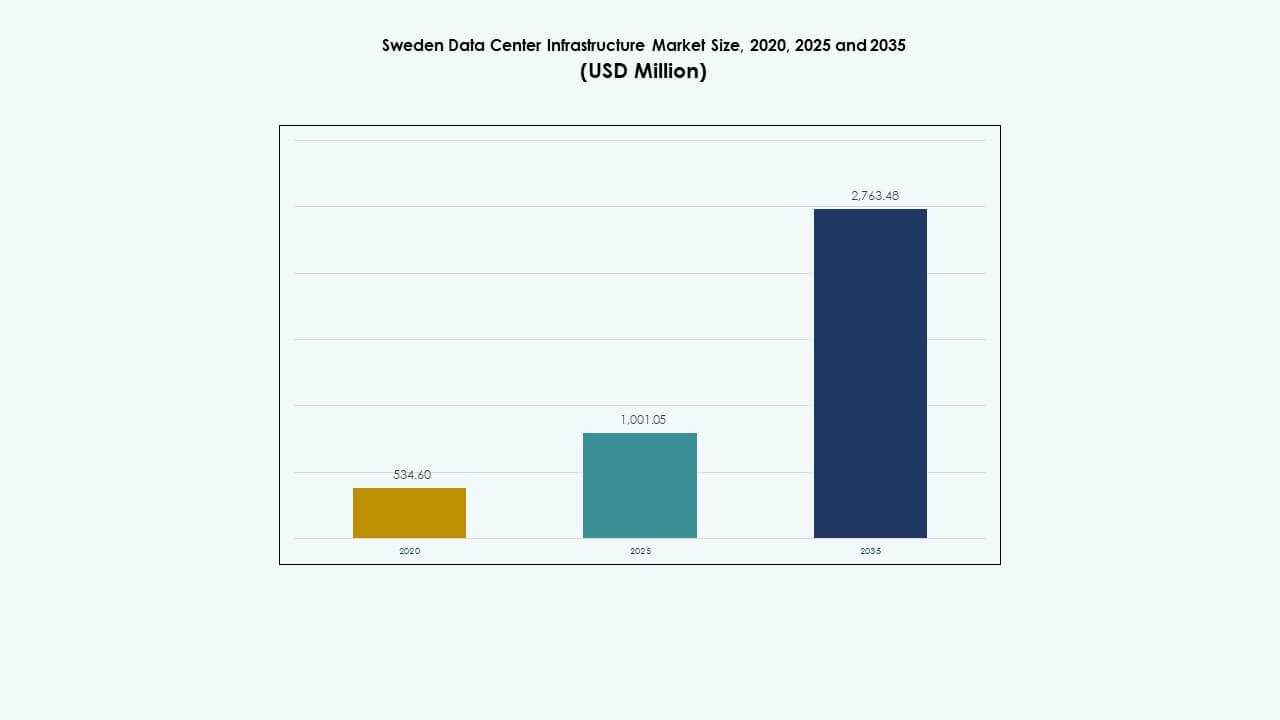

The Sweden Data Center Infrastructure Market size was valued at USD 534.60 million in 2020, reached USD 1,001.05 million in 2025, and is anticipated to attain USD 2,763.48 million by 2035, growing at a CAGR of 10.62% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Sweden Data Center Infrastructure Market Size 2025 |

USD 1,001.05 Million |

| Sweden Data Center Infrastructure Market, CAGR |

10.62% |

| Sweden Data Center Infrastructure Market Size 2035 |

USD 2,763.48 Million |

Strong adoption of AI workloads, edge computing, and renewable-powered data centers drives market momentum. Companies invest in energy-efficient designs and modular architectures to cut operational costs. Government support for sustainable infrastructure and cross-border connectivity enhances Sweden’s global data center competitiveness. Its reliability, policy stability, and innovation-friendly ecosystem make it a strategic investment destination for international hyperscalers.

Southern and Central Sweden lead with dense connectivity, advanced power grids, and proximity to major enterprises. Northern Sweden is emerging rapidly due to abundant hydropower, low temperatures, and availability of large land parcels for green data centers. Western and Eastern Sweden show moderate growth, driven by rising edge deployments and expanding regional cloud demand.

Market Drivers

Market Drivers

Rising Integration of Renewable Energy and Sustainable Data Center Designs

The Sweden Data Center Infrastructure Market grows through strong sustainability mandates and green power integration. Operators rely on hydro, wind, and biomass energy to cut carbon emissions. The cold Nordic climate supports natural cooling systems that reduce power use. Major players invest in liquid cooling and heat recovery technologies. These efforts align with Sweden’s zero-emission targets. Sustainable design lowers operational costs while attracting ESG-focused investors. Data center developers gain policy incentives for renewable-based projects. The government’s grid reliability enhances investor trust and long-term energy security.

- For instance, Google launched its Europe-north2 cloud region outside Stockholm in March 2025, backed by long-term wind energy agreements exceeding 700 MW capacity. EcoDataCenter in Falun integrates renewable energy with heat recovery to supply district heating for local pellet production, achieving climate-positive operations.

Expansion of Cloud Computing, AI, and IoT Infrastructure Needs

Rapid adoption of cloud computing and AI workloads drives infrastructure upgrades across Sweden. Enterprises seek scalable, high-density data centers to support automation and analytics. The rise in connected devices fuels greater need for storage and low-latency networks. Global providers like AWS and Microsoft expand local cloud zones to meet compliance demands. It supports digital transformation across industries such as healthcare and finance. Businesses depend on advanced infrastructure for AI-driven decision systems. These trends elevate investment inflows and innovation. The demand for faster data exchange reinforces Sweden’s position as a Nordic technology hub.

Government Policies Encouraging Digital Transformation and Connectivity

National digitalization strategies push extensive investments in connectivity and IT systems. The government supports data-driven industries through tax incentives and simplified licensing. Fiber optic networks and 5G deployment strengthen Sweden’s data center ecosystem. Local authorities promote sustainable buildouts with land zoning support and renewable-energy partnerships. Businesses leverage these frameworks to accelerate modernization and cloud adoption. It supports new edge and colocation facility developments. Enhanced bandwidth and cross-border connectivity attract hyperscale and enterprise tenants. Regulatory clarity fosters confidence among international investors and cloud operators.

Innovation in Power Efficiency and Smart Cooling Technologies

Continuous innovation in power and cooling efficiency shapes infrastructure competitiveness. Operators use AI-based energy optimization systems to balance workload efficiency. Advanced modular designs improve scalability and installation time. Hybrid systems combining air and liquid cooling enhance reliability and power usage effectiveness (PUE). The Sweden Data Center Infrastructure Market benefits from such technological efficiency. Renewable-powered battery systems ensure backup reliability. Digital twins and automation enhance asset monitoring and lifecycle management. These innovations secure consistent uptime and sustainable expansion.

- For instance, EcoDataCenter operates a large-scale data center campus in Borlänge, designed with modular architecture and powered entirely by renewable energy. The company focuses on low-carbon operations and partners with RISE to advance liquid cooling and AI-based energy optimization technologies for sustainable performance validation.

Market Trends

Growing Deployment of Modular and Prefabricated Data Center Solutions

The industry moves toward modular construction to meet time-sensitive deployment needs. Prefabricated systems allow faster delivery with reduced on-site labor. Flexible scalability makes them suitable for enterprise and edge environments. The Sweden Data Center Infrastructure Market leverages these systems for rural and urban setups. Energy-efficient prefabricated modules cut waste during assembly. Construction firms adopt design-build and EPC models for precision control. Modular systems lower capital risks for operators entering new regions. Adoption rates rise due to consistent quality and speed of execution.

Adoption of AI, Automation, and Digital Twin Technology for Facility Management

Artificial intelligence and automation tools now drive efficient data center management. Predictive maintenance through sensors minimizes downtime and resource loss. Operators employ digital twins for monitoring airflow, thermal loads, and energy usage. AI enhances security systems and dynamic workload allocation. It helps balance power and cooling operations automatically. The Sweden Data Center Infrastructure Market adopts these tools to improve uptime and reliability. Automation reduces manual intervention in complex data center environments. Efficiency improvements directly lower operational expenditure across large campuses.

Increasing Edge Data Center Investments for Low-Latency Applications

The surge in IoT and real-time services encourages edge facility expansion. Businesses require local processing power to minimize latency in critical workloads. Edge infrastructure supports smart city frameworks, telemedicine, and autonomous transport. Telecom firms collaborate with cloud providers to deploy micro data hubs. It strengthens service coverage in remote areas. The Sweden Data Center Infrastructure Market experiences rising deployments near urban centers. Edge models complement hyperscale facilities by offloading regional traffic. Demand for 5G-connected edge centers continues accelerating infrastructure diversification.

Focus on Heat Reuse and Energy Recovery Systems in Cold Climates

Operators in Sweden integrate district heating systems into data centers. These systems redirect waste heat to residential and industrial networks. Energy reuse improves sustainability ratings and attracts corporate clients with green goals. Municipal partnerships streamline connection frameworks for heat-sharing infrastructure. The Sweden Data Center Infrastructure Market sees growing heat reuse projects in Stockholm and Luleå. These models reduce carbon output and maximize total energy efficiency. Operators gain recognition for supporting circular economy models. Sustainable design becomes a differentiating factor in competitive tendering.

Market Challenges

Rising Energy Costs and Power Availability Constraints

The Sweden Data Center Infrastructure Market faces constraints from fluctuating power costs. While renewable resources are abundant, seasonal variations impact electricity supply. Operators must plan for grid stability amid high-capacity expansion. Power-intensive AI and HPC workloads increase demand on local utilities. High energy pricing pressures profitability for colocation and hyperscale providers. Limited substation availability near industrial zones delays project approvals. Developers invest in energy storage and grid optimization to mitigate risks. Balancing sustainability and capacity remains a core industry challenge.

Supply Chain Delays and Regulatory Complexity in Infrastructure Projects

Data center developers encounter supply delays in equipment procurement. Import dependency for critical hardware extends project timelines. Environmental review processes and land-use approvals slow construction cycles. The Sweden Data Center Infrastructure Market contends with complex permitting for large builds. Skilled labor shortages in mechanical and electrical trades increase project costs. Logistics hurdles affect transport of heavy cooling and power units to remote areas. Businesses manage these challenges through local sourcing and advanced planning. Regulatory reforms could streamline deployment for future facilities.

Market Opportunities

Rising Foreign Direct Investment and Expansion of Hyperscale Campuses

Foreign investors target Sweden for its sustainable energy framework and reliable grid. Global hyperscalers expand regional campuses to serve Europe’s cloud demand. The Sweden Data Center Infrastructure Market benefits from international partnerships and capital inflows. Strong political stability attracts long-term infrastructure commitments. Growing enterprise digitalization opens opportunities for managed hosting and colocation services. Emerging regions near Stockholm and Malmö attract new developments. Demand for multi-megawatt campuses continues to rise across the Nordics.

Emergence of Green Data Center Certifications and Advanced Cooling Solutions

New sustainability benchmarks create scope for advanced green-certified facilities. Operators use AI-controlled cooling and liquid immersion systems to cut PUE ratios. The Sweden Data Center Infrastructure Market gains from environmental certifications that appeal to global clients. Manufacturers design energy-saving hardware for local climate adaptation. District heating integration further enhances facility value. Investors favor developers meeting ISO 14001 and EN 50600 standards. This shift strengthens Sweden’s leadership in climate-smart digital infrastructure.

Market Segmentation

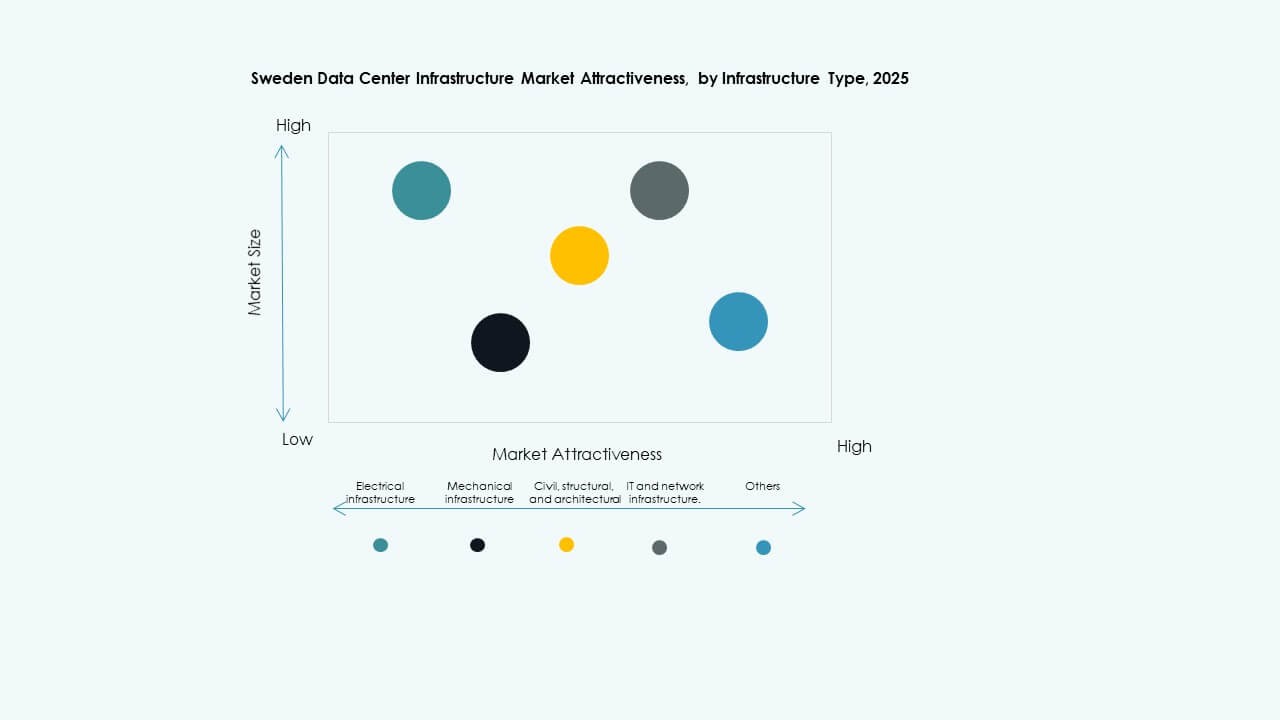

By Infrastructure Type

Electrical infrastructure dominates due to strong focus on energy reliability and redundancy. Operators deploy advanced grid interconnections and UPS systems for 24/7 continuity. Mechanical systems gain importance in cold-region data centers emphasizing efficient cooling. IT and network infrastructure evolve with AI-ready servers and high-speed interconnects. Civil and structural frameworks support modular scalability. The Sweden Data Center Infrastructure Market shows balanced growth across all types, though power systems hold the largest share.

By Electrical Infrastructure

Uninterruptible Power Supply (UPS) systems form the backbone of mission-critical operations. Battery Energy Storage Systems (BESS) grow with renewable integration. PDUs and switchgears enhance distribution safety and load management. Utility grid connections ensure sustainable performance during peak loads. The Sweden Data Center Infrastructure Market advances toward hybrid power topologies. Emerging AI-based monitoring improves energy efficiency. Electrical reliability remains the key purchase criterion for large operators.

By Mechanical Infrastructure

Cooling infrastructure sees major innovation across Sweden’s data centers. Air-cooled chillers and CRAC/CRAH units dominate due to the favorable Nordic climate. Containment systems improve temperature control, reducing power usage. Pumps and piping enable efficient liquid cooling in high-density environments. The Sweden Data Center Infrastructure Market emphasizes low-PUE mechanical solutions. AI-based cooling management tools gain adoption. Reliability and modular scalability remain design priorities.

By Civil / Structural & Architectural

Structural systems adopt prefabricated modules and sustainable materials. Raised flooring enhances airflow, while advanced insulation supports thermal stability. Modern buildings integrate steel superstructures and composite envelopes for durability. The Sweden Data Center Infrastructure Market focuses on modular construction for speed and flexibility. Design optimization improves seismic safety and energy performance. Sustainable architecture reinforces Sweden’s carbon neutrality ambitions.

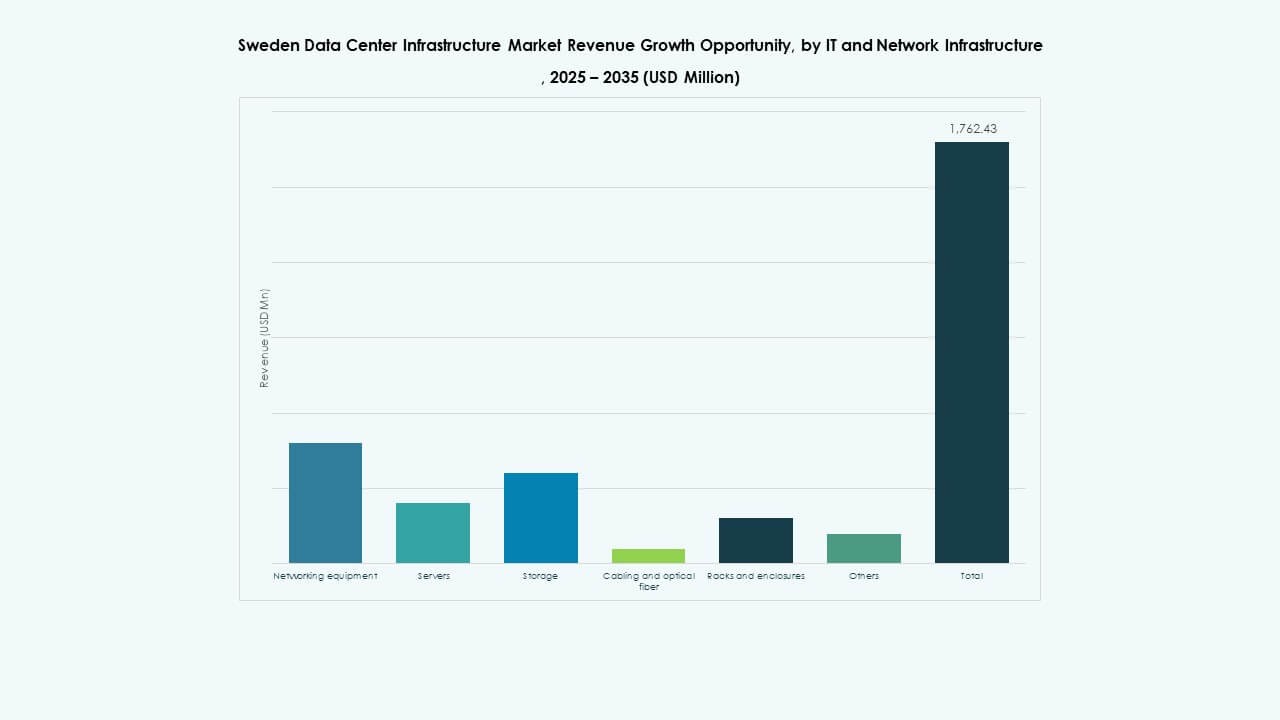

By IT & Network Infrastructure

Servers, storage, and high-speed networking equipment anchor the IT backbone. Demand rises for fiber cabling and scalable rack enclosures. AI workloads drive stronger investments in GPU-based computing clusters. The Sweden Data Center Infrastructure Market integrates automated network management for efficiency. Modern hardware supports latency-sensitive applications. Cloud interconnects link national and regional facilities seamlessly. IT infrastructure remains the innovation center of the ecosystem.

By Data Center Type

Hyperscale data centers hold the largest market share with rapid cloud expansion. Colocation facilities serve SMEs seeking cost-efficient scalability. Enterprise and edge centers emerge to support regional workloads. The Sweden Data Center Infrastructure Market evolves with hybrid setups linking cloud and edge nodes. Hyperscale growth aligns with renewable power proximity. Compact modular builds cater to localized applications.

By Delivery Model

Design-build and EPC models dominate due to predictable cost and faster execution. Modular factory-built solutions gain traction for small deployments. Turnkey construction appeals to hyperscalers demanding complete project integration. Retrofit and upgrade projects increase to modernize aging assets. The Sweden Data Center Infrastructure Market leverages hybrid delivery frameworks for flexibility. Streamlined construction management ensures scalability and compliance.

By Tier Type

Tier 3 data centers dominate due to high uptime and redundancy. Tier 4 facilities attract critical industries like finance and government. Tier 1 and Tier 2 centers continue supporting small enterprise needs. The Sweden Data Center Infrastructure Market trends toward higher-tier adoption. Reliability and certification standards remain key decision factors. Growth in Tier 3+ designs aligns with rising demand for secure colocation.

Regional Insights

Southern and Central Sweden – Leading Hubs for Hyperscale Expansion (Market Share: ~52%)

Southern and Central regions, including Stockholm, dominate due to superior connectivity and energy availability. Major hyperscale campuses cluster near grid substations and fiber corridors. The Sweden Data Center Infrastructure Market thrives in this zone due to abundant renewable integration. Stockholm serves as the national digital backbone. The region benefits from strategic logistics and cooling advantages. Continuous government support reinforces infrastructure scalability.

Northern Sweden – Emerging Green Energy Data Center Corridor (Market Share: ~32%)

Northern areas, including Luleå and Boden, lead in renewable-powered data centers. Abundant hydropower and cold climate enhance energy efficiency. The Sweden Data Center Infrastructure Market grows through green initiatives backed by EU funding. The region attracts international operators building sustainable campuses. Low energy costs and access to Arctic cooling strengthen its appeal. High-voltage grid investments expand future capacity across this corridor.

- For instance, atNorth’s data center in Boden delivers a PUE of 1.07 using 100% renewable hydropower and free Arctic air cooling. The Sweden Data Center Infrastructure Market grows through green initiatives supported by EU funding and strong sustainability policies.

Western and Eastern Sweden – Secondary Growth Clusters (Market Share: ~16%)

Western and Eastern subregions experience rising colocation and edge deployments. Göteborg and Uppsala attract regional enterprises expanding digital operations. The Sweden Data Center Infrastructure Market sees small to medium-scale projects here. Enhanced fiber routes link these cities with national hubs. Emerging players adopt modular centers to serve niche sectors. Continued urbanization and digital adoption sustain steady growth across these zones.

- For instance, Microsoft’s Gävle campus near Uppsala includes facilities such as GVX01, GVX02, and GVX21, designed to support regional edge computing through integrated power and connectivity infrastructure.

Competitive Insights:

- Schneider Electric SE

- ABB Ltd.

- Vertiv Group Corp.

- Dell, Inc.

- Cisco Systems, Inc.

- Equinix, Inc.

- Digital Realty Trust, Inc.

- Huawei Technologies Co., Ltd.

- Fujitsu

- Eaton Corporation plc

The competitive landscape in the Sweden Data Center Infrastructure Market features a mix of global infrastructure providers and major data-center operators. Schneider Electric, ABB, and Vertiv compete on power, cooling and energy-management solutions. Dell and Cisco supply servers, networking gear, and IT infrastructure. Operators such as Equinix and Digital Realty offer colocation and hyperscale facility services. Huawei and Fujitsu add alternative IT hardware and network solutions, while Eaton delivers complementary power infrastructure. Firms compete over reliability, energy efficiency, sustainable design, and modular builds. Pressure to support high-density workloads and cloud services drives innovation. Investors select players with proven track records in uptime, green credentials, and scalable infrastructure.

Recent Developments:

- In August 2025, Edgemode and Vertical Data announced a strategic collaboration to develop a 20 MW AI-optimized data center in Sweden, combining renewable energy capabilities with AI hardware expertise.

- In June 2025, Brookfield Asset Management announced plans to invest up to $10 billion in building a major AI data center in Sweden, targeting hyperscale infrastructure growth

- In March 2025, Google Cloud launched its 42nd cloud region in Sweden, enhancing digital infrastructure for local businesses and organizations with advanced cloud technologies.