Executive summary:

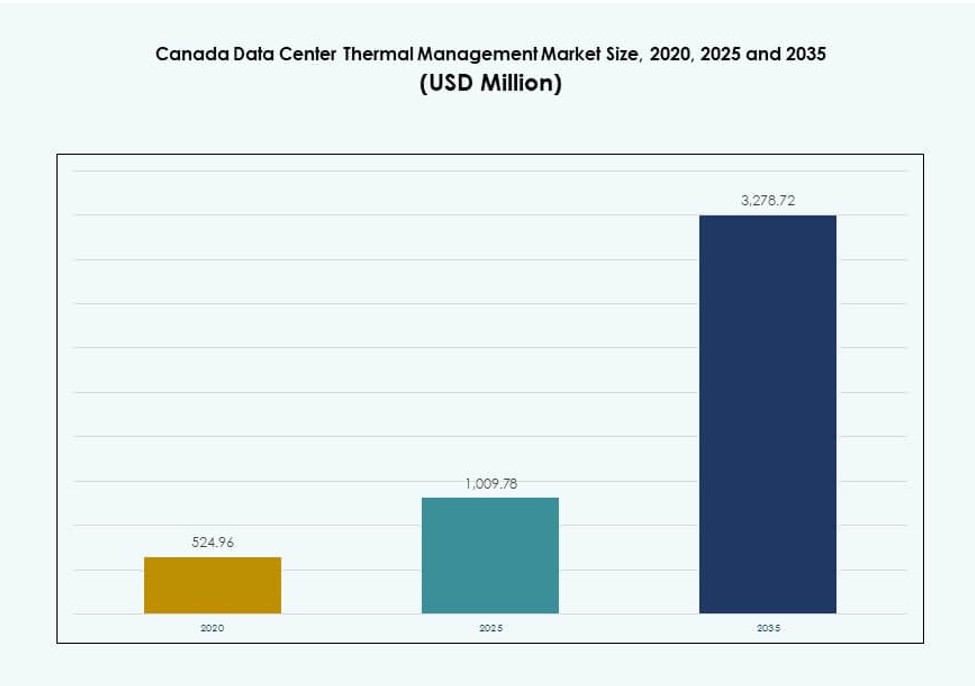

The Canada Data Center Thermal Management Market size was valued at USD 524.96 million in 2020, increased to USD 1,009.78 million in 2025, and is anticipated to reach USD 3,278.72 million by 2035, at a CAGR of 12.43% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Canada Data Center Thermal Management Market Size 2025 |

USD 1,009.78 Million |

| Canada Data Center Thermal Management Market, CAGR |

12.43% |

| Canada Data Center Thermal Management Market Size 2035 |

USD 3,278.72 Million |

The market benefits from rapid adoption of liquid cooling, AI-powered airflow management, and modular thermal infrastructure. Hyperscale and colocation operators are scaling high-density racks that demand efficient thermal designs. Innovations in direct-to-chip and immersion cooling support AI and HPC growth. Businesses prioritize low PUE and long-term energy savings, aligning with green building standards. For investors, this sector offers strong ROI through energy-efficient infrastructure upgrades and regulatory-backed initiatives.

Ontario leads the national market, driven by hyperscale expansion in Toronto and strong grid access. Québec is emerging rapidly due to low-cost hydroelectric energy and favorable climate for free cooling. Western provinces like Alberta and British Columbia are gaining momentum with edge data center deployments supporting telecom and industrial workloads. Growth in these zones is supported by modular thermal solutions and rising demand for decentralized computing.

Market Dynamics:

Market Drivers

Growing Adoption of AI, HPC, and Cloud Driving Demand for Thermal Infrastructure

The Canada Data Center Thermal Management Market is witnessing strong demand from the growing deployment of AI workloads and high-performance computing (HPC). These systems produce dense heat loads, which demand advanced cooling solutions. Liquid cooling, including direct-to-chip and immersion technologies, is gaining preference over legacy air-based systems. Cloud providers and colocation players are prioritizing thermal efficiency to meet service-level uptime. The need to manage power usage effectiveness (PUE) is a strategic factor for investment planning. Green building compliance is another factor encouraging thermal innovation. Enterprises are also expanding in edge locations, further pushing efficient localized cooling. Investors view thermal infrastructure as vital for operational continuity and ESG reporting.

Strategic Importance of Modular Cooling Systems in a Decentralized Data Center Landscape

Modular thermal management is gaining traction with operators deploying row- and rack-based cooling systems. This shift reflects the rising importance of scalable deployments in smaller edge and regional sites. Modular systems offer faster deployment, easier retrofits, and reduced downtime during upgrades. Prefabricated solutions improve installation flexibility in both hyperscale and micro data centers. The Canada Data Center Thermal Management Market benefits from this shift by enabling phased capacity additions. Operators use modular units to support load variability and redundancy without overprovisioning. These solutions align with real estate limitations in urban centers. Strategic planning increasingly incorporates thermal modularity in new builds and retrofits.

Sustainability Targets Driving Shift to Eco-Friendly Cooling Technologies

Operators are investing in sustainable thermal solutions to meet federal and provincial energy targets. Free cooling, liquid cooling with low-GWP fluids, and AI-optimized airflow are becoming essential tools. Enterprises in Canada face mounting pressure to align with carbon-neutral targets by 2030 and beyond. Cooling upgrades offer a direct path to reducing energy usage intensity (EUI). The Canada Data Center Thermal Management Market sees this shift as a competitive factor. Green certifications like LEED and BOMA BEST are influencing procurement of cooling systems. Data center firms partner with utilities and cleantech firms to explore energy reuse and heat recovery. Strategic buyers prefer vendors offering eco-friendly and future-ready technologies.

- For instance, QScale’s QO1 campus in Québec achieves PUE below 1.2 through up to 80% free cooling enabled by winter temperatures and 100% renewable hydroelectricity.

Government Incentives and Local Grid Policies Accelerating Energy-Efficient Thermal Deployments

Utility rebate programs and tax credits are incentivizing high-efficiency cooling retrofits. Provinces like Ontario and Québec promote investment in advanced cooling through targeted incentives. Power availability limitations in key metros push operators toward low-energy cooling models. Policies regulating maximum energy consumption per rack influence thermal planning from the design stage. The Canada Data Center Thermal Management Market aligns closely with national energy efficiency goals. Government-backed pilot programs support innovation in thermal designs. Data center zoning guidelines now include thermal performance benchmarks. Strategic funding access accelerates faster adoption of next-generation cooling units in Tier II and Tier III cities.

- For example, TELUS converted its Rimouski facility in Québec into Canada’s first sovereign AI factory, incorporating natural cooling systems that reduce water usage by over 75% compared with traditional data centers. The site leverages renewable energy and advanced infrastructure, reinforcing sustainable, high‑performance compute capacity within Canadian borders.

Market Trends

Wider Use of Liquid Cooling in High-Density Environments Across Enterprise and Hyperscale Sites

Liquid cooling is transitioning from niche to mainstream in Canada’s hyperscale and enterprise deployments. Direct-to-chip and immersion cooling are preferred for AI, ML, and blockchain applications. These workloads generate heat levels exceeding air-cooled system thresholds. Operators favor these technologies for their efficiency at rack densities above 20 kW. The Canada Data Center Thermal Management Market shows increased vendor activity in modular liquid cooling systems. Hardware partners now co-develop liquid cooling-ready servers. High thermal performance and improved TCO attract enterprise buyers. Regulatory support for low-emission systems further boosts the trend.

Emergence of AI-Driven Thermal Management Systems for Real-Time Optimization

AI-powered DCIM and BMS software modules are enabling predictive and automated cooling adjustments. These platforms use real-time temperature, humidity, and workload data to optimize airflow and chiller performance. Canadian operators use AI for controlling CRACs, fan speeds, and containment systems. The Canada Data Center Thermal Management Market shows rising demand for software-led cooling optimization. Vendors bundle AI dashboards with CFD simulations and digital twins. Smart control reduces OPEX and prevents thermal hotspots. It enables compliance with efficiency benchmarks. Operators rely on this trend to meet demanding uptime SLAs.

Regional Colocation Growth Driving Investments in Distributed Thermal Systems

Colocation providers in Toronto, Montréal, and Calgary are expanding their footprints rapidly. These expansions often involve multi-tenant environments with varying thermal needs. Operators deploy row-based and rack-based systems to support diverse client workloads. The Canada Data Center Thermal Management Market sees thermal scalability as critical in this segment. Colocation firms differentiate based on PUE and heat management metrics. Smart airflow control and isolated hot/cold zones are in demand. Flexible cooling configurations help reduce operational disputes and ensure tenant satisfaction. New sites prioritize modular thermal layouts to improve ROI.

Integration of Renewable Cooling Technologies to Reduce Environmental Impact

Operators in Canada are deploying adiabatic cooling, river-based systems, and geothermal-assisted chillers. These solutions reduce reliance on refrigerants and power-hungry compressors. Québec and British Columbia lead in implementing renewable thermal strategies. The Canada Data Center Thermal Management Market is exploring closed-loop cooling using hydro or waste-heat recovery. Facilities also experiment with snow-cooled reservoirs and seasonal thermal storage. Renewable integration aligns with ESG mandates and helps secure green financing. Thermal suppliers now offer tailored renewable cooling solutions. This trend strengthens regional green tech ecosystems.

Market Challenges

Complexity in Retrofitting Existing Sites with Next-Generation Cooling Systems

Retrofitting legacy facilities remains difficult due to existing design limitations. Operators face structural and spatial challenges in fitting liquid or hybrid cooling. Older buildings lack containment pathways, redundant piping, and elevated floors. The Canada Data Center Thermal Management Market must address these technical hurdles to enable widespread upgrades. CAPEX requirements and operational disruption deter swift retrofits. Coordination between MEP teams, OEMs, and IT managers slows down progress. Vendors often need to custom-engineer solutions for each retrofit. This limits speed and scalability. Smaller players lack resources for full cooling modernization.

Limited Talent and Training for Advanced Cooling Systems Across Canadian Data Center Operations

Operators struggle to find technicians trained in liquid cooling, modular deployments, and AI-managed systems. Most current staff are familiar with traditional air-cooled infrastructure. This creates delays during system configuration, fault diagnostics, and upgrades. The Canada Data Center Thermal Management Market depends on workforce skill development to scale. Training programs for cooling optimization are scarce across provinces. AI-based thermal platforms also require knowledge of machine learning and controls. Inexperienced teams may operate systems inefficiently, reducing expected ROI. Vendors are building support programs, but demand still exceeds supply.

Market Opportunities

Strategic Scope for Edge and Micro Data Center Cooling Across Remote and Industrial Zones

Canada’s vast geography and remote enterprise locations create demand for edge cooling systems. Mining, oil & gas, and telecom deployments need rugged thermal units for smaller IT nodes. The Canada Data Center Thermal Management Market sees strong opportunity in compact, weatherproof, and modular cooling solutions. These systems operate in extreme climates and limited access areas. Vendors offering low-maintenance, pre-configured systems can gain market share in these zones.

Emerging Opportunity in Heat Reuse Systems for Urban District Heating and Sustainability Goals

Heat reuse from data centers can support district heating in urban zones. Montréal, Toronto, and Vancouver are exploring heat-sharing with nearby buildings. The Canada Data Center Thermal Management Market can grow by aligning with city decarbonization efforts. Technologies that transfer waste heat from racks to heating grids open new revenue models. Public-private partnerships and utility support strengthen the case for investment.

Market Segmentation

By Data Center Size

Large data centers dominate the Canada Data Center Thermal Management Market due to hyperscale deployments and rising AI demand. These facilities require robust thermal designs and advanced control systems. Medium-sized data centers also grow steadily, serving colocation and enterprise clients. Small facilities remain relevant in edge locations, though with smaller revenue contributions.

By Cooling Technology

Air-based cooling holds a substantial share, particularly through hot/cold aisle setups and rear door exchangers. However, liquid-based cooling is growing faster, with direct-to-chip and immersion systems gaining adoption. Hybrid systems combining both approaches attract operators seeking flexibility. Phase-change and thermoelectric remain niche but show promise in edge applications.

By Component

Hardware contributes the largest revenue share in the Canada Data Center Thermal Management Market. Key growth comes from next-gen chillers and airflow systems. Software components like AI optimization and DCIM platforms are rising rapidly in value. Services such as retrofits, maintenance, and commissioning see strong demand due to system complexity.

By Hardware

Cooling units and chillers dominate, driven by large deployments. Fans, heat exchangers, and piping components follow, supporting airflow control and liquid circulation. Emerging hardware includes modular CDU systems and smart sensors. Distribution components gain value through ease of integration in retrofits.

By Software

DCIM dashboards and AI-based optimization tools lead software demand. These tools help manage energy use and prevent thermal failures. CFD simulations support planning and modeling efforts. BMS modules integrate thermal performance with building energy systems, offering a holistic view.

By Services

Installation and commissioning services lead the segment due to constant new builds. Monitoring as a service and preventive maintenance follow closely. Retrofits and upgrades are critical for legacy sites. Vendors offering bundled service contracts hold competitive advantage in the market.

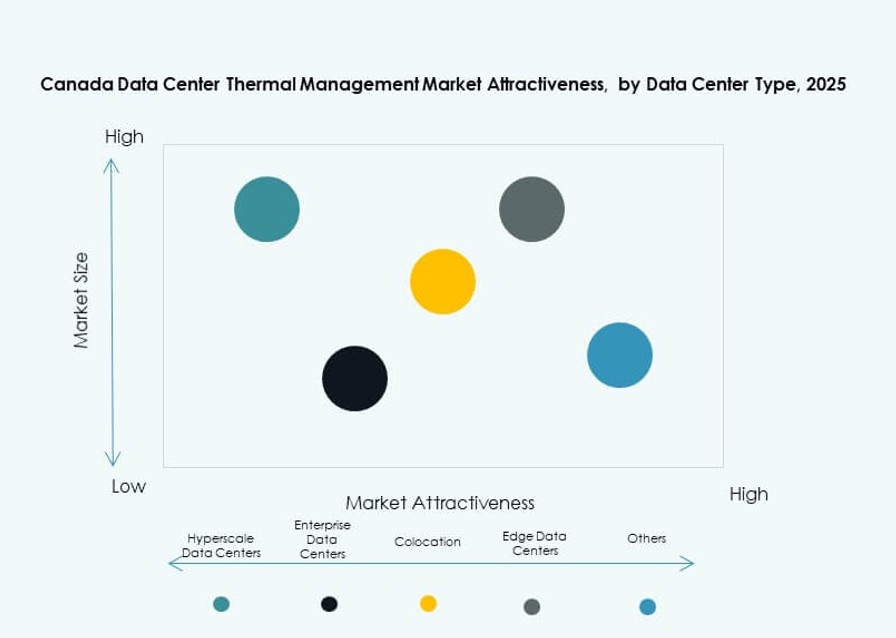

By Data Center Type

Hyperscale data centers lead due to high-density rack environments and large-scale deployments. Colocation and cloud facilities follow, driven by multi-tenant cooling needs. Enterprise and edge/micro data centers grow steadily, supporting regional and sector-specific demand. Specialized data centers like financial or telecom sites remain niche.

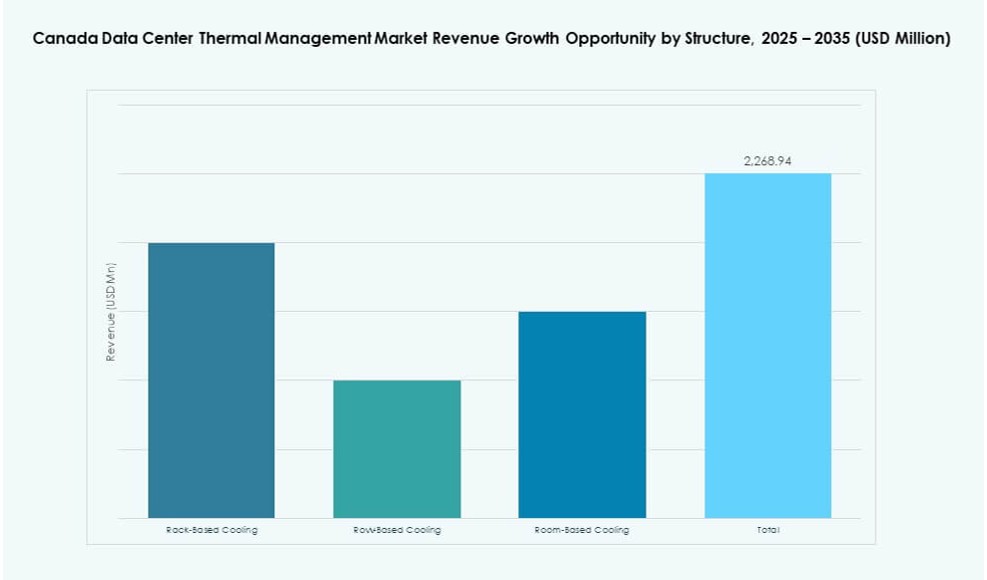

By Structure

Row-based and rack-based cooling systems are preferred for modularity and high-density zones. Room-based cooling still holds a share in legacy and large enterprise environments. The market trends toward decentralized, rack-level cooling to enhance efficiency and enable phased deployments.

Regional Insights

Ontario Dominates the Market Due to Toronto’s Position as a Hyperscale and Colocation Hub

Ontario holds the largest share of the Canada Data Center Thermal Management Market, accounting for nearly 43%. Toronto leads hyperscale activity, hosting major players like Google, AWS, and Microsoft. Power constraints in the region drive focus on thermal optimization. Incentives from provincial authorities support advanced cooling deployments. The region also benefits from a strong network of infrastructure vendors and consultants.

Québec Emerges as a Green Energy Leader with Favorable Cooling Conditions

Québec contributes about 28% market share, supported by low-cost hydroelectric power and cooler climate conditions. Montréal is a fast-growing data center location with a green footprint. Operators here use renewable energy and advanced thermal systems to meet ESG targets. Policies promoting sustainable infrastructure attract international investors. River-based and adiabatic cooling gain attention due to water access and energy cost savings.

- For instance, QScale’s Q01 campus in Québec operates on nearly 100% renewable hydroelectric power supplied by Hydro‑Québec. The facility is designed for high energy efficiency and sustainable cooling, and Hewlett Packard Enterprise serves as an anchor tenant supporting green data center infrastructure.

Western Provinces Show Rising Demand for Edge and Modular Data Centers

Western Canada, including Alberta and British Columbia, holds around 17% of the market share. These regions support edge deployments in oil, gas, mining, and telecom sectors. Modular, rack-based cooling systems see strong uptake. Urban areas like Vancouver are witnessing retail colocation growth. Harsh weather conditions push for ruggedized thermal systems that ensure uptime in remote or industrial environments.

- For instance, hyperscale players like AWS are adopting direct-to-chip liquid cooling globally to support high-density AI racks, a trend that aligns with modular edge data center deployments emerging across Western Canada.

Competitive Insights:

- Vertiv Group Corp.

- Schneider Electric

- Stulz GmbH

- Trane Technologies plc

- Delta Electronics, Inc.

- Johnson Controls International plc

- Daikin Industries Ltd.

- Airedale International Air Conditioning Ltd.

- Huawei Technologies Co., Ltd.

- Eaton Corporation

The Canada Data Center Thermal Management Market features a highly competitive landscape led by global infrastructure providers and regional HVAC specialists. Vertiv, Schneider Electric, and Stulz dominate due to strong portfolios across liquid, air, and hybrid cooling systems. Delta Electronics and Daikin drive innovation in energy-efficient thermal products. Johnson Controls and Trane lead in integrating smart building systems with cooling platforms. Huawei and Eaton focus on scalable hardware for hyperscale and edge facilities. It benefits from players offering full-stack solutions spanning hardware, software, and services. Competitive advantage depends on localized support, modularity, energy efficiency, and sustainability alignment. Strategic partnerships and AI-driven software adoption are key differentiators among leading firms.

Recent Developments:

- In November 2025, Eaton Corporation announced it had signed a definitive agreement to acquire Boyd Thermal, the thermal management business of Boyd Corporation, for $9.5 billion.

- In September 2025, Johnson Controls International plc expanded its thermal management portfolio with the Silent-Aire Coolant Distribution Unit (CDU) platform for high-density data center racks. This scalable liquid cooling solution supports AI workloads and builds on existing products like York and M&M Carnot.