Executive summary:

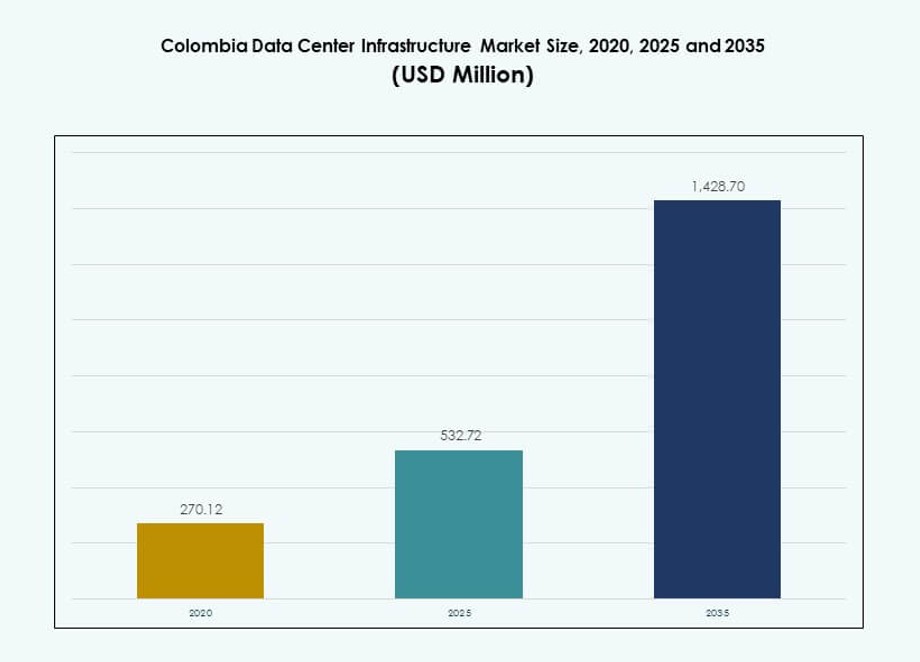

The Colombia Data Center Infrastructure Market size was valued at USD 270.12 million in 2020 to USD 532.72 million in 2025 and is anticipated to reach USD 1,428.70 million by 2035, at a CAGR of 10.30% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Colombia Data Center Infrastructure Market Size 2025 |

USD 532.72 Million |

| Colombia Data Center Infrastructure Market, CAGR |

10.30% |

| Colombia Data Center Infrastructure Market Size 2035 |

USD 1,428.70 Million |

Strong demand for cloud computing, enterprise digitalization, and secure colocation services is driving infrastructure investments across Colombia. Businesses seek low-latency, carrier-neutral, and energy-efficient facilities to support critical workloads. Innovation in power, cooling, and modular construction is reducing deployment time and costs. Strategic focus on sovereign data hosting, coupled with regulatory clarity and investor interest, makes the market attractive for global and regional players aiming to scale operations in Latin America.

Bogotá remains the dominant hub due to strong fiber networks, enterprise density, and government digital initiatives. Medellín is emerging as a technology and smart-city cluster, attracting investments in edge and modular data centers. Coastal cities such as Barranquilla are gaining traction due to submarine cable access, expanding digital reach. These regional developments strengthen geographic resilience and support national data infrastructure goals.

Market Dynamics:

Market Drivers

Expansion Of Cloud Computing And Enterprise Digital Transformation Demand

The Colombia Data Center Infrastructure Market benefits from rapid cloud service adoption. Enterprises migrate workloads from on‑premise systems to scalable environments. Financial institutions require secure and compliant hosting platforms. Retail and e‑commerce firms depend on reliable uptime for digital channels. Telecom operators expand backend capacity to support data traffic growth. Public sector digitization programs increase national data processing needs. Businesses value proximity hosting to reduce latency. Investors view stable demand visibility as a long‑term advantage.

- For instance, Equinix BG2 in Bogotá spans about 32,000 sq ft (2,900 m²) and its initial phase supports around 550 cabinets, with room to expand to approximately 1,100 cabinets in later phases. This facility strengthens Colombia’s data infrastructure and supports enterprise and cloud deployment needs.

Rising Adoption Of Energy Efficient And Resilient Infrastructure Systems

Energy efficiency drives infrastructure investment decisions across Colombia. Operators deploy advanced power management and cooling technologies. High electricity costs encourage optimization of power usage effectiveness. Backup power systems gain priority to ensure business continuity. Renewable energy integration supports sustainability targets. Equipment vendors focus on modular and scalable designs. These upgrades reduce operating risk for operators. Investors favor assets with lower long‑term operating costs.

- For instance, GTD El Poblado in Medellín is a Tier III‑certified data center with 1,200 m² total building size and 271 m² of fully built‑out white space to host critical IT equipment. The facility uses N+1 redundancy across power and cooling infrastructure to support reliable operations and high availability for enterprise and cloud workloads.

Growth In Colocation And Carrier Neutral Facility Deployment

Colocation demand grows among mid‑size and large enterprises. Companies prefer shared infrastructure to limit capital exposure. Carrier neutral facilities support multi‑network connectivity. This model improves redundancy and service flexibility. International cloud providers partner with local operators. The Colombia Data Center Infrastructure Market gains depth from this ecosystem. It strengthens service availability for regional customers. Investors value recurring revenue models from colocation contracts.

Government Policy Support And Data Sovereignty Requirements

National regulations encourage local data hosting. Public institutions prioritize domestic infrastructure for sensitive data. Compliance needs drive demand for certified facilities. Policy stability supports private infrastructure investment. Local permitting frameworks show gradual improvement. Infrastructure developers gain clearer project visibility. These factors reduce entry risk for new players. Long‑term policy alignment supports capital inflows.

Market Trends

Shift Toward Modular And Prefabricated Data Center Construction Models

Operators adopt modular construction to shorten deployment timelines. Prefabricated components improve build quality control. This approach limits onsite labor dependency. Expansion becomes faster and more predictable. Modular facilities support phased capacity additions. Cost visibility improves for developers. The Colombia Data Center Infrastructure Market reflects this structural shift. Investors favor scalable build strategies.

Increased Focus On Edge Data Centers Near Demand Centers

Edge facilities gain relevance for latency sensitive applications. Content delivery and fintech services drive this trend. Regional cities require localized data processing. Operators deploy smaller facilities closer to users. This model supports smart city and IoT use cases. Network resilience improves through distributed architecture. Market participants adjust location strategies. Capital allocation shifts toward decentralized assets.

Rising Use Of Automation And Remote Infrastructure Management Tools

Automation improves operational efficiency across facilities. Operators deploy intelligent monitoring systems. Remote management reduces staffing intensity. Predictive maintenance lowers unplanned downtime risk. These tools support consistent service levels. Technology vendors expand software driven solutions. Operational transparency increases for investors. Asset performance becomes easier to benchmark.

Growing Emphasis On Sustainability Reporting And Green Certifications

Sustainability reporting gains importance among operators. Clients request transparent energy and carbon metrics. Certification standards influence facility design choices. Renewable sourcing discussions increase among developers. Efficient cooling systems receive higher investment priority. The Colombia Data Center Infrastructure Market aligns with global ESG expectations. Compliance improves brand credibility. Investors value sustainability aligned portfolios.

Market Challenges

Power Infrastructure Constraints And Grid Reliability Concerns

Power availability remains a key operational challenge. Grid reliability varies across regions. Operators depend heavily on backup generation systems. Fuel logistics add operational complexity. Power cost volatility impacts margins. Infrastructure upgrades require high upfront investment. The Colombia Data Center Infrastructure Market must balance growth with power risk. These factors influence site selection decisions.

High Capital Intensity And Skilled Workforce Availability Gaps

Data center projects demand large capital commitments. Financing access varies by developer profile. Skilled engineering talent remains limited locally. Training requirements increase project timelines. Equipment imports face logistical delays. Cost overruns affect return expectations. It challenges smaller operators entering the market. Risk management becomes critical for investors.

Market Opportunities

Expansion Of Regional Cloud Zones And Hyperscale Partnerships

Cloud providers explore regional expansion opportunities. Local partnerships reduce market entry barriers. Demand from enterprises supports new capacity rollout. Hyperscale projects create anchor tenancy benefits. Infrastructure ecosystems grow around large campuses. The Colombia Data Center Infrastructure Market gains global visibility. These developments attract institutional investors. Long‑term contracts support revenue stability.

Development Of Secondary City Data Center Hubs

Secondary cities present untapped infrastructure potential. Land availability supports cost‑efficient development. Proximity to users improves service quality. Local governments promote digital infrastructure investment. Edge computing use cases expand steadily. Network diversification improves national resilience. This opportunity lowers concentration risk. Investors gain portfolio diversification options.

Market Segmentation

By Infrastructure Type

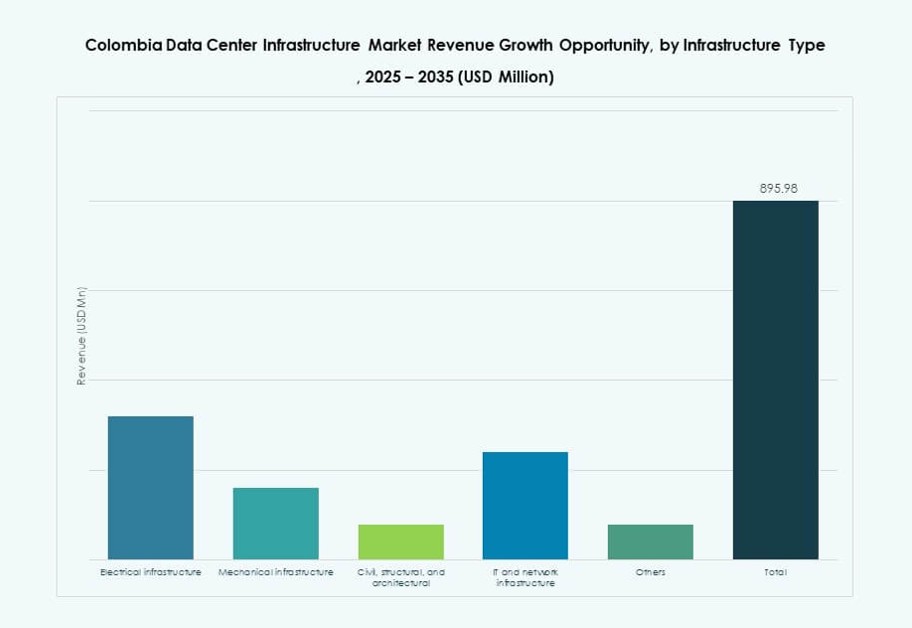

Electrical and mechanical infrastructure dominate total investment share. Power and cooling systems receive priority spending. IT and network infrastructure follows with steady growth. Civil and structural works support expansion projects. The Colombia Data Center Infrastructure Market benefits from balanced infrastructure demand. Electrical systems lead due to reliability needs. Mechanical solutions grow with efficiency focus. These segments attract continuous capital allocation.

By Electrical Infrastructure

UPS systems and power distribution units hold major share. Grid connection upgrades support capacity expansion. Battery energy storage adoption shows strong growth. Switchgears ensure operational safety and redundancy. The Colombia Data Center Infrastructure Market prioritizes power stability. Electrical resilience drives procurement decisions. Vendors focus on scalable configurations. Growth aligns with uptime requirements.

By Mechanical Infrastructure

Cooling units and chillers dominate mechanical spending. Hot and cold aisle containment gains adoption. Efficient airflow management reduces energy use. Pumps and piping support system reliability. The Colombia Data Center Infrastructure Market values thermal efficiency. Mechanical upgrades lower operating costs. Demand aligns with sustainability goals. This segment supports long‑term performance.

By Civil / Structural & Architectural

Site preparation and superstructure works lead investment. Building envelopes improve environmental control. Raised floors support cabling flexibility. Modular building systems gain market share. The Colombia Data Center Infrastructure Market benefits from standardized designs. Civil works ensure compliance and resilience. Growth supports phased expansions. Investors value construction predictability.

By IT & Network Infrastructure

Servers and networking equipment command dominant share. Storage systems grow with data volumes. High density racks support cloud workloads. Optical fiber demand rises with connectivity needs. The Colombia Data Center Infrastructure Market reflects digital workload growth. IT refresh cycles remain consistent. Vendors focus on energy efficient hardware. Capital flow remains steady.

By Data Center Type

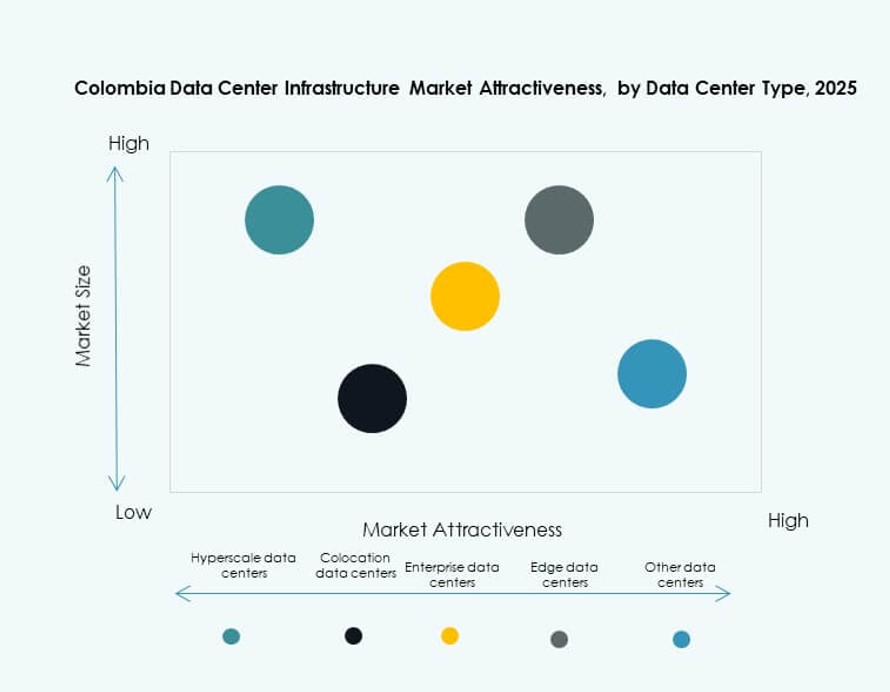

Colocation data centers lead market share. Hyperscale facilities show fastest growth. Enterprise data centers maintain steady demand. Edge facilities expand in secondary locations. The Colombia Data Center Infrastructure Market benefits from diversified models. Each type serves distinct user needs. Revenue streams remain balanced. Investors gain exposure flexibility.

By Delivery Model

Turnkey and design‑build models dominate projects. EPC approaches reduce execution risk. Retrofit and upgrade demand grows steadily. Modular factory‑built delivery gains traction. The Colombia Data Center Infrastructure Market values speed and certainty. Delivery efficiency improves timelines. Developers prefer integrated solutions. Risk mitigation supports investment confidence.

By Tier Type

Tier III facilities hold the largest share. Enterprises prioritize high availability standards. Tier IV demand remains niche but strategic. Tier I and II serve limited workloads. The Colombia Data Center Infrastructure Market aligns with uptime requirements. Certification influences client trust. Higher tiers attract premium clients. Revenue stability improves.

Regional Insights

Central Region Including Bogotá And Surrounding Areas

Bogotá accounts for nearly 45% market share. Enterprise concentration drives infrastructure demand. Financial and government institutions anchor capacity needs. Strong fiber connectivity supports operations. Skilled workforce availability favors this region. The Colombia Data Center Infrastructure Market relies heavily on this hub. Investment activity remains consistent.

- For instance, Equinix operates the BG1 data center in Bogotá with about 21,570 ft² of raised floor colocation space. The facility features N+1 UPS redundancy and supports cabinet power density in the range of 4–6 kVA, ensuring reliable enterprise‑grade operations.

Antioquia Region Including Medellín

Medellín contributes around 25% market share. Innovation driven enterprises support growth. Smart city initiatives increase data processing needs. Lower land costs attract developers. Connectivity improvements strengthen competitiveness. It emerges as a secondary hub. Investor interest continues to rise.

Caribbean And Other Emerging Regions

Caribbean regions hold nearly 30% combined share. Proximity to submarine cables supports edge deployments. Latency sensitive services benefit from coastal access. Infrastructure remains in early development stages. Regional demand grows steadily. The Colombia Data Center Infrastructure Market gains geographic balance. Future expansion potential remains strong.

- For instance, Ascenty is building two data centers in Colombia, each with about 9,000 m² of total area in Bogotá. These facilities are designed with robust poweru, redundancy, and carrier‑neutral infrastructure to support enterprise and cloud workloads in strategic locations.

Competitive Insights:

- Scala Data Centers

- MDC Data Centers

- ABB

- Ascenty

- Cisco Systems, Inc.

- Dell Inc.

- Equinix, Inc.

- IBM

- Schneider Electric

- Vertiv Group Corp.

The Colombia Data Center Infrastructure Market features a mix of global vendors and regional operators competing across power systems, cooling, IT hardware, and colocation services. It sees strong activity from hyperscale-focused firms like Scala and Equinix, which invest in large-scale, carrier-neutral campuses. Infrastructure giants like ABB, Vertiv, and Schneider Electric dominate the electrical and mechanical components segment with modular and energy-efficient solutions. Cisco, Dell, Lenovo, and IBM compete on networking and server-side hardware, offering integrated systems to local enterprises and cloud providers. Colocation players such as Ascenty and MDC cater to mid-size clients needing scalable, secure hosting environments. Product innovation, sustainability credentials, and service reliability remain key competitive levers. Market consolidation trends emerge through strategic partnerships and mergers, shaping the long-term positioning of key players.

Recent Developments:

- In December 2025, Ilkari reinforced its role in Colombia’s data center market by securing ICREA Level IV certification for sovereign high-density infrastructure, amid projections of market growth from $81 million in 2024 to over $300 million by 2030

- In October 2024, ODATA (an Aligned Data Centers company) announced a $1.3 billion expansion in Colombia’s data center infrastructure market, unveiling two new facilities DC BG02 and DC BG03 in Cundinamarca, Bogotá, with a combined IT capacity of 144 MW expected to complete initial phases by late 2026.