Executive summary:

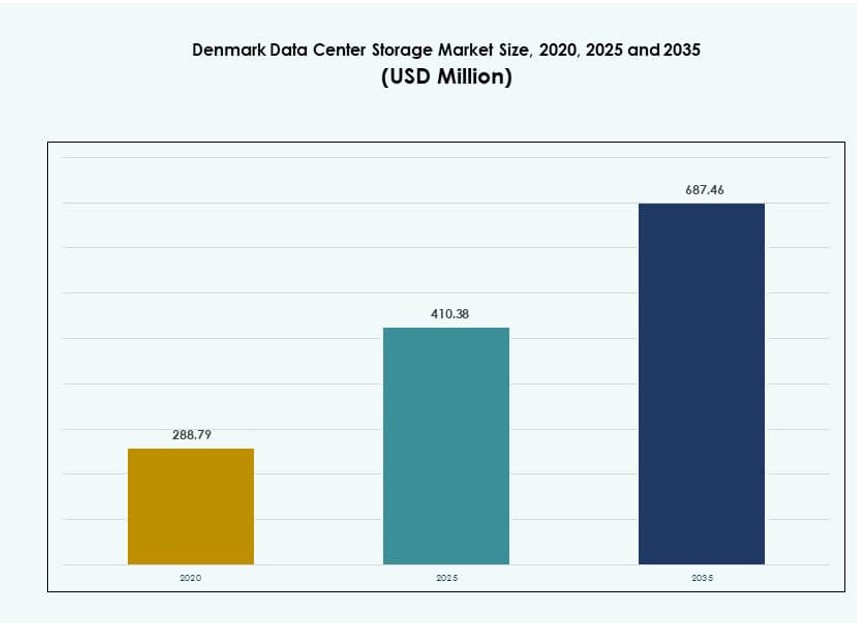

The Denmark Data Center Storage Market size was valued at USD 288.79 million in 2020 to USD 410.38 million in 2025 and is anticipated to reach USD 687.46 million by 2035, at a CAGR of 5.24% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Denmark Data Center Storage Market Size 2025 |

USD 410.38 Million |

| Denmark Data Center Storage Market, CAGR |

5.24% |

| Denmark Data Center Storage Market Size 2035 |

USD 687.46 Million |

Digital transformation across sectors is accelerating demand for advanced storage systems in Denmark. Enterprises are shifting toward software-defined, hybrid, and flash-based architectures to support data-intensive workloads. The market benefits from public cloud adoption, smart city projects, and regulatory focus on data sovereignty. Storage solutions that offer scalability, compliance, and energy efficiency are seeing high uptake. Businesses prioritize solutions that align with Denmark’s green goals and enable fast, secure access to critical data.

The Capital Region leads the Denmark Data Center Storage Market due to its dense network infrastructure and large data center footprint. Central and Southern Denmark are emerging with growing deployments in sustainable energy and edge computing. Regions like Aarhus and Odense support enterprise workloads with cost-effective, renewable-powered facilities. These areas benefit from strong local initiatives and high-speed fiber connectivity.

Market Dynamics:

Market Drivers

Rising Enterprise Demand for High-Performance Storage to Support Digital Transformation

Large-scale digital transformation across public and private sectors fuels demand for advanced storage systems. Enterprises seek scalable, high-throughput storage to support AI, analytics, and IoT platforms. These use cases drive interest in hybrid setups with low-latency access and backup reliability. Businesses in Denmark are also modernizing legacy infrastructure to remain agile and competitive. The Denmark Data Center Storage Market benefits from this ongoing shift toward software-defined and flash-optimized systems. Cloud migration initiatives among telecom, banking, and healthcare sectors amplify storage infrastructure demand. Storage vendors tailor offerings to meet compliance and sustainability goals. Investors consider this market vital for enabling Denmark’s data-driven economy. Its maturity aligns with the broader EU digital strategy.

Technology Shift Toward Flash and Software-Defined Architectures Fuels Infrastructure Modernization

The increasing adoption of all-flash arrays and software-defined storage shapes procurement decisions across Danish enterprises. Traditional storage is being replaced with dynamic and energy-efficient solutions that offer better IOPS and real-time processing. Organizations prioritize hardware-agnostic software layers that simplify management and reduce costs. This modernization aligns with carbon-neutral data strategies promoted by Danish authorities. Enterprises prefer modular systems with lower total cost of ownership and high availability. The Denmark Data Center Storage Market aligns well with Europe’s push toward digital sovereignty. AI readiness is another factor influencing design and scale of new storage deployments. Edge storage is gaining traction across smart city and utility sectors. Innovation, scalability, and compliance form the backbone of buyer expectations.

Data-Intensive Applications and Regulatory Pressures Push Demand for Scalable Storage Solutions

Growth in AI, 5G, video analytics, and cloud-native applications strains conventional storage systems. Enterprises require robust, scalable architectures to support rising throughput and secure data sovereignty. The Denmark Data Center Storage Market reflects growing pressure from EU compliance frameworks such as GDPR and NIS2. These rules elevate the need for on-premise and hybrid storage with strict access controls and backup policies. Healthcare and public sector workloads increasingly demand secure, high-availability storage infrastructure. IT teams opt for systems with seamless backup, disaster recovery, and multi-region support. Denmark’s innovation-friendly environment encourages tech providers to test pilot deployments for next-gen solutions. Efficient rack density and sustainability in storage procurement remain top buyer criteria.

- For instance, Digital Realty operates nearly 70 MW of combined capacity across its Copenhagen data centers, offering scalable hybrid storage solutions that support GDPR and NIS2 compliance for public sector and healthcare workloads. These facilities enable high-availability, regulation-aligned data management in Denmark.

Strategic Role of Denmark as a Low-Carbon, High-Connectivity Hub for Data Infrastructure

Denmark’s position as a low-latency gateway to Northern Europe supports its expanding data infrastructure. Subsea cable routes, renewable energy resources, and a pro-digital government create an ideal environment for storage growth. Hyperscale and edge data center deployments contribute significantly to overall storage expansion. The Denmark Data Center Storage Market supports workloads from regional financial hubs, government projects, and cross-border services. Demand is rising for systems with high availability, encryption, and modular growth capabilities. Enterprises view the country’s connectivity and green credentials as a strategic advantage. Storage vendors leverage this positioning to serve both local and export markets. Public-private digital infrastructure partnerships are fostering future-ready deployments.

- For instance, Microsoft plans to launch a full data center region in Denmark by 2026, spanning Esbjerg and Varde, with modular storage infrastructure powered entirely by renewable energy. The sites will support secure government and cross-border workloads with scalable cloud storage capabilities.

Market Trends

Surge in Hyperscale Projects with In-Built Storage Ecosystems Transforming Procurement Models

Denmark is attracting hyperscale cloud and AI infrastructure projects that integrate advanced storage systems. Global cloud firms prioritize the country for regional replication, fault tolerance, and low-latency availability. Procurement shifts toward colocation models where storage is bundled with compute and bandwidth. The Denmark Data Center Storage Market sees higher integration of cloud-native storage layers like object storage and NVMe over Fabrics. This helps reduce data bottlenecks and boost performance. Distributed applications across edge nodes also influence central storage design. Modular deployments allow phased upgrades without disrupting uptime. Vendors compete by offering SLA-driven storage ecosystems rather than discrete hardware sales. This reshapes the traditional storage value chain.

Increased Demand for Edge Storage Systems in Renewable Energy and Public Infrastructure Projects

Denmark’s focus on digitized public infrastructure and smart grid systems drives edge storage demand. Applications in traffic management, renewable monitoring, and emergency systems require local storage with low latency. Edge nodes complement centralized storage by processing and retaining critical data at the source. The Denmark Data Center Storage Market reflects growth in high-speed SSDs and rugged storage appliances for these setups. Local governments prioritize systems with remote access, autonomous recovery, and real-time analytics support. Vendors offer edge-to-core management interfaces to unify operations. Edge demand supports storage diversity, with SSDs gaining significant ground over legacy HDD. These use cases enhance regional resilience and operational efficiency.

Focus on Sustainability Drives Shift to Green Storage Technologies in Facility Design

Enterprises are aligning storage procurement with Denmark’s strong climate commitments and green building codes. Solutions with lower power consumption, longer lifecycle, and efficient cooling dominate RFPs. The Denmark Data Center Storage Market benefits from adoption of circular design principles and hardware recycling initiatives. Liquid-cooled racks, flash-based storage arrays, and energy-aware firmware features are now standard in newer facilities. Vendors partner with clean power utilities to market their offerings as zero-carbon ready. Buyers assess sustainability metrics including heat reuse, power utilization effectiveness, and lifecycle emissions. Public sector procurement also includes sustainability clauses. Energy-efficient storage has become a default requirement, not a premium option.

High-Availability and Zero-Downtime Expectations Increase Demand for Advanced Backup Solutions

With critical data workloads running on digital platforms, Danish enterprises seek robust backup and recovery systems. Cyber-resilience and zero-downtime operations drive demand for integrated disaster recovery solutions. The Denmark Data Center Storage Market records strong interest in replication, mirroring, and snapshot-based backup. Enterprises demand faster recovery point and time objectives. Storage vendors bundle backup features with enterprise-grade arrays. Integration with cyber incident response and business continuity platforms becomes a purchase criterion. Demand rises for immutable storage and air-gapped systems. Financial services, telecom, and healthcare sectors especially prioritize always-on availability. This shifts the focus from storage capacity to resilience and assurance.

Market Challenges

High Operating Costs and Electricity Pricing Risks Impact Storage System ROI

Though Denmark offers abundant renewable energy, its high electricity prices remain a challenge for data center operations. Storage systems, especially in high-density environments, contribute to energy load and cooling demand. Enterprises must balance performance with energy efficiency to control operational costs. The Denmark Data Center Storage Market faces ROI pressures for deploying high-end flash systems or high-availability clusters. Rising inflation and capex constraints can delay planned upgrades. SMEs in particular face affordability gaps in adopting software-defined storage or hyperconverged infrastructure. The cost of training and migration also affects mid-market deployments. Pricing volatility and uncertain energy tariffs impact long-term TCO planning.

Data Sovereignty and Integration Complexity Constrain Cross-Border Storage Architectures

Enterprises with multinational footprints face regulatory challenges in cross-border data access and storage replication. The Denmark Data Center Storage Market must comply with both EU-wide laws and localized mandates. Integrating global storage frameworks with local privacy requirements increases technical and legal complexity. Businesses are cautious about vendor lock-in and compliance penalties. Hybrid and multi-cloud architectures must ensure strict data governance, creating integration hurdles. The lack of skilled workforce in niche storage integration and security areas adds pressure. Solutions must meet NIS2 and GDPR mandates, while offering seamless orchestration. These constraints make large-scale implementations time-consuming and resource-intensive.

Market Opportunities

Digital Sovereignty Push and Government Initiatives Open New Avenues for Compliant Storage Solutions

Denmark’s support for digital autonomy and secure infrastructure opens strong opportunities for compliant storage systems. Enterprises and public agencies invest in in-country solutions aligned with EU digital goals. The Denmark Data Center Storage Market can benefit from vendor-neutral platforms offering local control, backup, and transparency. Vendors that combine compliance, performance, and sustainability stand to win long-term contracts across multiple verticals.

Growth in AI Workloads and Analytics Adoption Spurs Demand for Specialized Storage Architectures

Enterprises across sectors deploy AI and data analytics platforms that require high-performance and low-latency storage. The Denmark Data Center Storage Market sees growing demand for GPU-optimized arrays and NVMe-based systems. Solutions that support real-time data ingestion and processing gain traction. Providers offering AI-integrated storage orchestration can tap emerging edge AI deployments and public sector innovation labs.

Market Segmentation

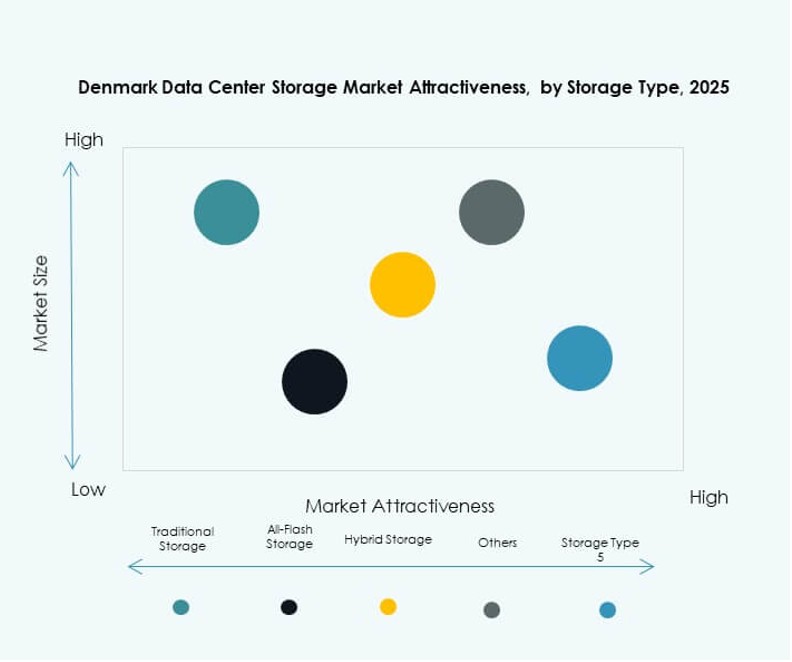

By Storage Type

The Denmark Data Center Storage Market is segmented into Traditional Storage, All-Flash Storage, Hybrid Storage, and Others. All-Flash Storage leads the market with growing demand for faster processing and reduced latency. Hybrid models follow due to their flexibility and cost efficiency. Traditional storage systems are declining but still relevant for archival needs. Flash dominance is driven by performance-sensitive sectors like BFSI and telecom.

By Storage Deployment

The key storage deployments include Storage Area Network (SAN), Network-Attached Storage (NAS), Direct-Attached Storage (DAS), and Others. SAN systems dominate the Denmark Data Center Storage Market due to their scalability and high performance. NAS systems are popular in mid-sized enterprises for shared access. DAS is preferred in edge environments for cost-effective deployment. SAN’s role expands in enterprise and colocation segments.

By Component

The market is segmented by Hardware and Software components. Hardware holds the larger share due to the physical infrastructure required in every facility. However, the software segment is growing faster due to rising adoption of software-defined storage (SDS). SDS provides flexibility, better scalability, and cloud compatibility. Vendors focus on automation-driven software layers to enhance management efficiency and reduce human intervention.

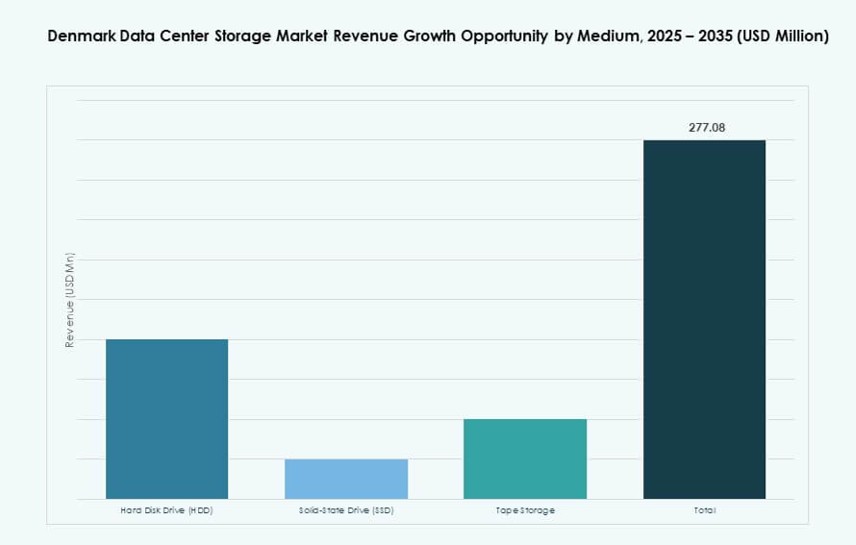

By Medium

The storage medium segmentation includes Hard Disk Drives (HDD), Solid-State Drives (SSD), and Tape Storage. SSD dominates the Denmark Data Center Storage Market due to its speed and durability. HDDs still support archival storage in cost-sensitive deployments. Tape storage is niche, used mainly for backup and cold storage. SSD adoption is favored for mission-critical and latency-sensitive applications.

By Deployment Model

Deployment models include On-premises, Cloud-based, and Hybrid. Hybrid storage leads due to its balance of control and flexibility. It supports compliance and scalability across sectors. On-premises solutions are still strong in government and BFSI due to data sovereignty concerns. Cloud-based deployments grow in SMEs and startups focused on agility and cost. Hybrid remains the preferred model in multicloud strategies.

By Application

Key applications include IT and Telecommunications, BFSI, Government, Healthcare, and Others. IT and Telecommunications account for the highest market share due to the volume of data and need for high uptime. BFSI follows closely, driven by regulatory compliance and real-time transaction needs. Government projects demand secure, in-country storage. Healthcare focuses on patient data protection and rapid access.

Regional Insights

Capital Region of Denmark (Hovedstaden) Leads with Over 55% Market Share Due to Dense Data Center Footprint

The Capital Region dominates the Denmark Data Center Storage Market with over 55% share, led by Copenhagen’s dense concentration of enterprise data centers and hyperscale facilities. Its strong international connectivity, power availability, and enterprise IT demand make it a preferred location for storage-intensive applications. The region supports both government and private cloud infrastructure with high service-level agreements.

- For instance, Digital Realty’s CPH3 facility in Ballerup provides 75,000 square feet (6,968 m²) of colocation space powered by 100% renewable energy.

Central and Southern Denmark Regions Emergent with Sustainable and Edge-Focused Storage Deployments

The Central Denmark Region, including Aarhus, holds around 25% of the market, driven by expanding digital infrastructure projects and mid-tier data center activity. Southern Denmark, with cities like Odense, contributes nearly 12%, supported by renewable energy projects and smart grid investments. These areas attract storage deployments focused on sustainability, edge readiness, and cost optimization for secondary urban centers.

Northern Denmark and Zealand Regions Hold Niche but Growing Market Share in Strategic Sectors

Northern Denmark and Zealand together account for roughly 8% of the market. These regions see growing interest from specialized industries like energy, public infrastructure, and academic research. Storage deployments here often support edge and private cloud setups with high availability needs. Their growth depends on local digitalization plans, land availability, and expanding regional fiber networks.

- For instance, atNorth’s data center campus in Varde, Denmark, is designed for up to 250 MW capacity and supports direct liquid cooling to enable high-density, energy-efficient computing. The site leverages Denmark’s renewable energy infrastructure for sustainable operations.

Competitive Insights:

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- IBM Corporation

- NetApp

- Huawei Technologies Co., Ltd.

- Cisco Systems, Inc.

- Fujitsu Limited

- Lenovo Group

- Hitachi Vantara

- Cohesity, Inc.

The Denmark Data Center Storage Market is competitive, with global tech leaders and domestic IT firms shaping its landscape. Dell Technologies and HPE dominate enterprise deployments with broad portfolios in all-flash, hybrid, and software-defined storage. IBM and NetApp remain strong in high-availability systems and backup solutions. Huawei and Cisco offer integrated storage-network platforms, while Fujitsu and Lenovo focus on sustainability and efficiency. Domestic players like Netcompany and KMD support localized deployments, especially for public sector IT. Competition centers on hybrid readiness, energy efficiency, and compliance features. Companies aim to differentiate through modularity, SLA-backed services, and partnerships. It reflects strong vendor alignment with Denmark’s digital and green goals.

Recent Developments:

- In May 2025, NNIT secured a major contract with Energinet to develop an IT platform handling vast energy data volumes, investing three-digit DKK millions to support Denmark’s green energy transition through advanced DevOps services.

- In April 2025, KMD, a key Danish IT firm, announced its migration of the KMD Opus ERP platform to SAP S/4HANA Cloud via Microsoft Azure, enhancing public sector solutions with AI integration and long-term cloud stability.