Executive summary:

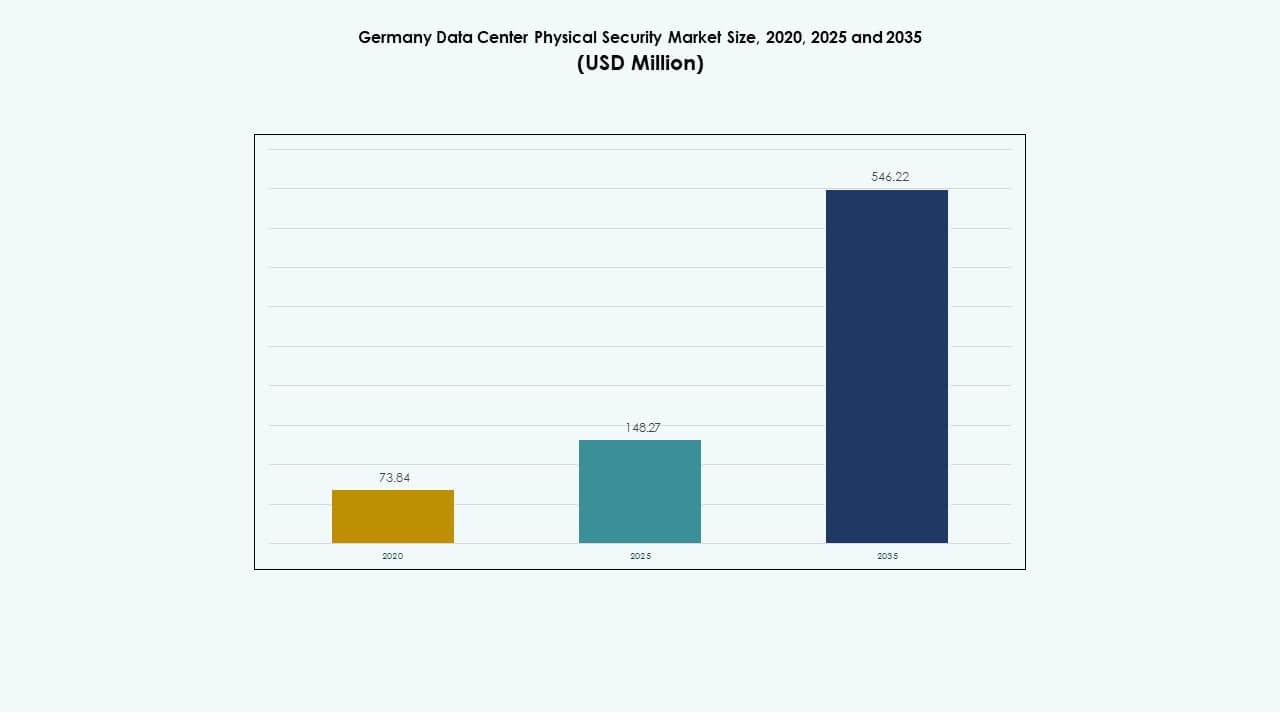

The Germany Data Center Physical Security Market size was valued at USD 73.84 million in 2020 to USD 148.27 million in 2025 and is anticipated to reach USD 546.22 million by 2035, at a CAGR of 13.84% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Germany Data Center Physical Security Market Size 2025 |

USD 148.27 Million |

| Germany Data Center Physical Security Market, CAGR |

546.22% |

| Germany Data Center Physical Security Market Size 2035 |

USD 546.22 Million |

Growing investment in hyperscale and colocation facilities drives steady security upgrades. Rising cloud adoption and stricter data protection regulations push operators to adopt AI-enabled video surveillance, access control, and intrusion detection systems. Integration of IoT sensors and automated management platforms supports faster response times and predictive maintenance. The market’s strategic importance lies in enabling secure digital infrastructure critical for enterprise continuity and investor confidence.

Western Germany leads the market due to its dense concentration of data centers and advanced connectivity. Southern and Northern regions follow with growing enterprise and colocation developments. Eastern Germany is emerging as a new growth corridor supported by government-led digital transformation projects. Increased public and private investments across regions enhance infrastructure security maturity and adoption of integrated monitoring systems.

Market Drivers

Market Drivers

Rising Deployment of Advanced Access Control and Surveillance Systems Across Critical Facilities

The Germany Data Center Physical Security Market expands with the adoption of advanced access control and surveillance systems that ensure real-time threat monitoring. Growing use of AI-powered facial recognition and biometric authentication strengthens entry-point protection in hyperscale and enterprise facilities. Operators prioritize integrated solutions combining video analytics and intrusion detection for seamless site coverage. Vendors enhance product accuracy through machine-learning upgrades. This progress drives consistent modernization across critical infrastructure. It builds investor confidence by improving operational continuity and resilience against physical intrusions.

- For instance, Bosch’s Intelligent Video Analytics detects, tracks, and classifies people and vehicles under varied lighting and weather conditions, reducing false alarms in perimeter security. Axis Communications’ Q-series cameras deliver up to 4K resolution with wide dynamic range and low-light performance for continuous surveillance accuracy.

Expansion of Hyperscale and Colocation Data Centers Enhancing Security Infrastructure Investments

Hyperscale and colocation providers upgrade physical security layers to meet client compliance demands. Growing investment in cloud and AI-driven infrastructure increases site vulnerability to targeted breaches. Companies focus on perimeter and cabinet-level security to maintain trust and uptime. Physical access data integration with cybersecurity protocols gains importance. It supports rapid response to multi-layer threats. Vendors develop modular systems that adapt to facility expansion without service disruption. This trend strengthens Germany’s leadership in secure digital infrastructure within Europe.

- For instance, Equinix’s Frankfurt data centers employ multi-factor biometric access controls and 24/7 on-site security monitoring across multiple facilities. Vantage Data Centers’ Berlin campus integrates AI-supported video analytics and advanced perimeter protection as part of its large-scale European hyperscale expansion.

Integration of IoT Sensors and AI Analytics to Enhance Threat Prediction and Response

Data centers deploy smart IoT-based systems that improve environmental and physical monitoring. AI analytics detect unusual movement patterns, reducing false alerts and manual interventions. Centralized dashboards offer predictive insights to facility managers for proactive security planning. Integration with network-based analytics enhances operational transparency. It allows quick assessment of risk zones during incidents. Advanced automation lowers response times and maintenance costs. This shift transforms physical security into a predictive defense model rather than a reactive function.

Government Regulations and Data Sovereignty Requirements Fueling Security Investments

Stricter EU and national regulations mandate robust security measures for data centers hosting sensitive information. Compliance frameworks like GDPR and ISO 27001 increase investment in access validation and surveillance systems. Operators prioritize certified solutions to safeguard client data integrity. The push for energy-efficient yet secure designs creates strong demand for automated security management tools. It aligns infrastructure safety with sustainability objectives. Regulatory pressure ensures continuous upgrades and market expansion for certified security providers.

Market Trends

Market Trends

Growing Convergence of Physical and Cybersecurity for Unified Risk Management

The Germany Data Center Physical Security Market witnesses convergence between physical and cybersecurity strategies to address complex hybrid threats. Organizations deploy unified platforms that link access control logs with network event data. This integration allows faster breach detection and improved compliance reporting. Managed service providers incorporate AI-driven analytics for automated policy enforcement. It improves incident resolution speed while minimizing downtime. Enterprises treat unified defense systems as a strategic differentiator in client trust and reliability.

Adoption of Cloud-Based Video Management and AI Surveillance Platforms

Cloud-based surveillance replaces legacy analog systems across new data centers. Remote access and analytics-driven management improve operational efficiency. AI platforms automate real-time monitoring and object detection across multiple facilities. Vendors introduce scalable subscription models that lower upfront costs. It benefits colocation operators seeking flexible, centrally controlled solutions. Growing partnerships between video technology firms and data center operators fuel platform innovation. These shifts redefine surveillance from passive recording to dynamic situational awareness.

Increased Emphasis on Green Security Solutions and Sustainable Infrastructure

Data center operators invest in eco-friendly security systems to align with sustainability goals. Low-energy cameras, smart lighting, and motion-triggered monitoring reduce power consumption. Vendors develop recyclable materials for enclosure and cabling infrastructure. It supports environmental targets without compromising safety. Sustainable solutions attract government incentives and corporate clients committed to carbon neutrality. Energy-efficient surveillance systems become a key investment metric in procurement decisions. This trend embeds sustainability into long-term operational strategies.

Rising Importance of Edge Security Architecture in Distributed Data Center Models

Decentralized computing environments create new security challenges across edge nodes. Companies implement compact access control and remote monitoring units for distributed facilities. AI-driven anomaly detection enhances local response capabilities. It secures small-scale centers operating near end users. Vendors design modular, ruggedized systems suitable for edge deployment. Integration with centralized command systems ensures policy consistency. This expansion supports real-time data processing while maintaining standardized protection layers.

Market Challenges

Market Challenges

High Capital Costs and Integration Complexities in Multi-Layer Security Infrastructure

The Germany Data Center Physical Security Market faces high implementation costs due to advanced technologies and system integration needs. Upgrading older sites with AI-enabled access systems demands major financial planning. Operators struggle to align new solutions with existing hardware and software protocols. Compatibility issues delay deployment timelines. Skilled workforce shortages compound integration hurdles. It pressures small and medium data centers to postpone security upgrades. Long procurement cycles further hinder technology refresh plans.

Data Privacy, Interoperability, and Maintenance Barriers in Evolving Security Ecosystems

Ensuring privacy compliance while using facial recognition or behavior analytics remains a complex challenge. Balancing GDPR obligations with monitoring efficiency requires careful policy design. Interoperability among devices from multiple vendors limits seamless data flow. Maintenance of IoT sensors and AI cameras adds operational burden. It increases downtime risk during upgrades. Vendors must support scalable, compliant, and user-friendly systems to retain competitiveness. Addressing these constraints remains critical for sustainable market growth.

Market Opportunities

Rising Investments in Smart and Autonomous Security Systems Across Next-Generation Data Centers

The Germany Data Center Physical Security Market benefits from rising adoption of autonomous drones, robotics, and AI-based analytics. Self-learning algorithms enable predictive maintenance and instant response. Global cloud firms expand partnerships with local integrators for secure deployments. It opens new opportunities for automation providers offering plug-and-play modules. Increasing R&D funding strengthens innovation in motion sensors and facial analytics.

Emergence of 5G and Edge Computing Creating Demand for Distributed Security Models

The growth of 5G networks and edge computing accelerates demand for micro-data centers requiring localized protection. Compact security solutions with remote management capabilities gain traction. Vendors offering adaptive, low-latency systems capture strong growth potential. It enables enterprises to protect distributed environments efficiently. Expansion of connected infrastructure boosts revenue prospects for scalable, network-aware security vendors.

Market Segmentation

By Data Center Size

Large data centers dominate due to higher infrastructure investment and advanced compliance requirements. These facilities deploy multi-layered systems integrating biometrics, video analytics, and perimeter defense. Medium centers focus on cost-efficient solutions that maintain reliability. Small sites adopt modular systems for scalability. The Germany Data Center Physical Security Market gains strength from large enterprise and hyperscale growth driven by digital expansion.

By Component

Solutions segment leads with extensive deployment of access control and surveillance systems. Service offerings grow steadily with consulting and integration support. Continuous maintenance ensures system uptime and compliance across regulated environments. The combination of hardware and managed services ensures holistic protection for operators. Demand for integrated solutions drives technological evolution in the market.

By Solution

Video surveillance remains the largest segment driven by adoption of AI-powered monitoring. Access control solutions advance through multi-factor authentication and smart card integration. Monitoring and detection technologies support incident response precision. Others, such as fire and environmental monitoring, enhance site safety. The Germany Data Center Physical Security Market reflects demand for intelligent, automated solutions across layers.

By Services

System integration dominates as operators prefer unified platforms linking multiple security layers. Consulting services support customized deployments for data-sensitive sectors. Maintenance and support remain essential for long-term reliability and regulatory compliance. Vendors expand managed service portfolios for smaller operators. Continuous upgrade contracts ensure steady recurring revenue streams.

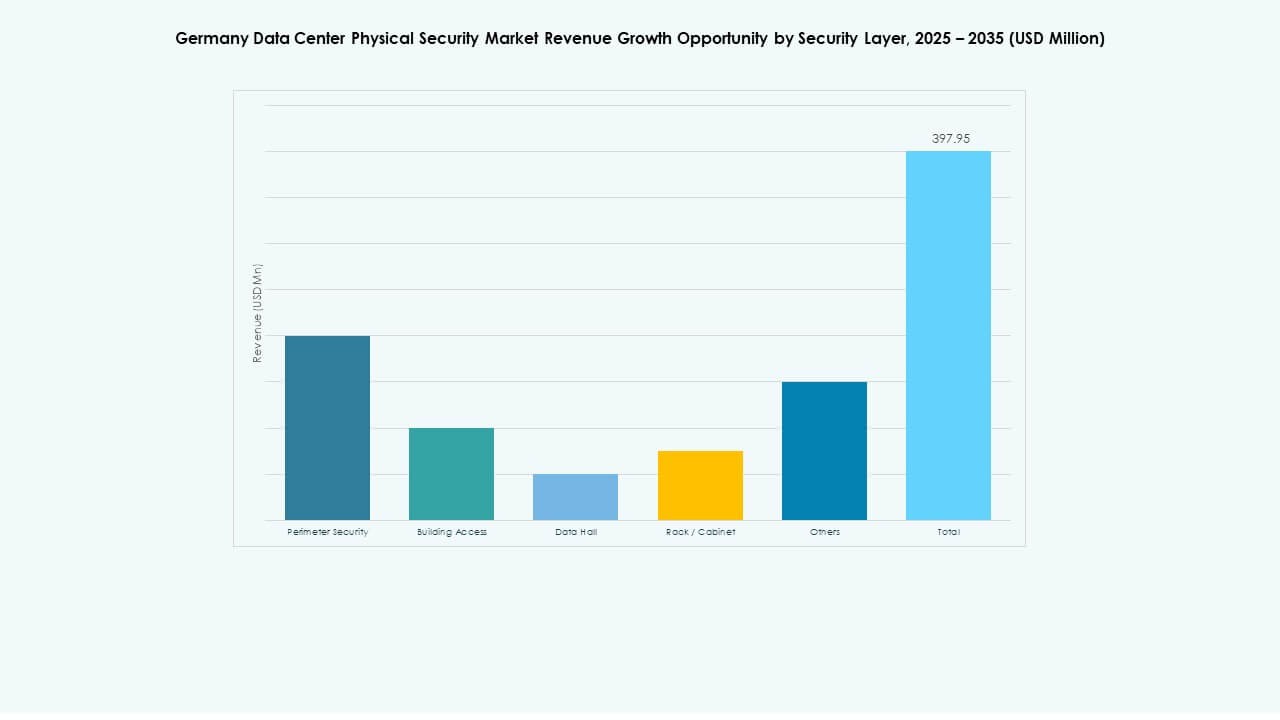

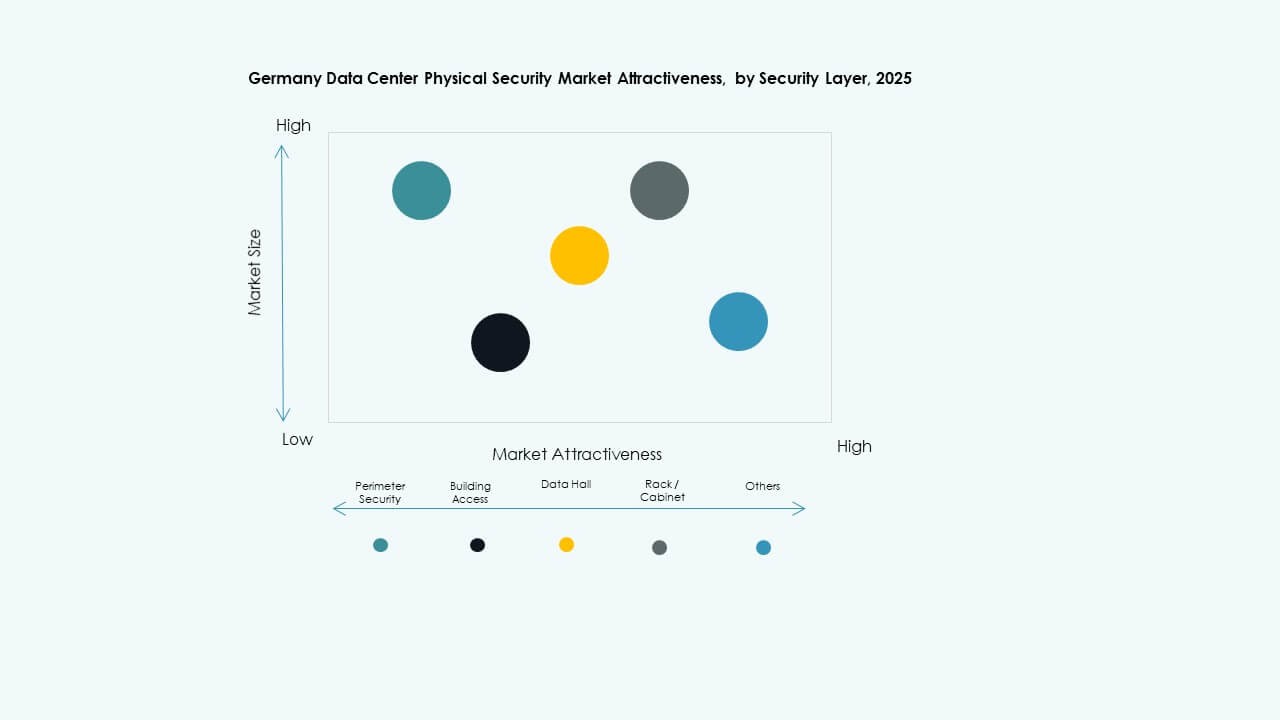

By Security Layer

Perimeter security holds major share due to its role in deterring unauthorized entry. Building access and data hall protection strengthen secondary layers. Rack and cabinet monitoring ensures micro-level asset protection. Others include fire suppression and environmental tracking systems. The Germany Data Center Physical Security Market emphasizes layered protection to enhance site resilience.

By Data Center Type

Hyperscale facilities lead due to massive infrastructure and client data concentration. Colocation centers follow with high service-level expectations from enterprise tenants. Edge and enterprise centers exhibit rising adoption of modular security kits. Others include regional facilities supporting specific workloads. Demand diversity drives innovation in adaptive security platforms.

By End-User

IT & Telecom sector dominates due to strong cloud and network growth. BFSI and government sectors prioritize compliance-driven protection. Healthcare centers adopt advanced biometric systems for sensitive patient data. Manufacturing and retail sectors expand secure storage needs for operational analytics. The Germany Data Center Physical Security Market benefits from rising sectoral digitization and compliance awareness.

Regional Insights

Regional Insights

Western Germany – Major Data Center Hub with Strong Security Infrastructure

Western Germany holds approximately 45% market share led by Frankfurt, Düsseldorf, and Cologne. The region hosts leading hyperscale and colocation facilities serving global cloud providers. Investment in AI-driven surveillance and smart access control remains high. It benefits from dense connectivity and proximity to financial institutions. Local regulations enforce strict compliance standards, fueling consistent technology upgrades.

- For instance, Citigroup’s Frankfurt Data Centre uses Siemens’ integrated building automation and security systems, combining fire protection, HVAC control, and power management under one platform. The facility implements Siemens’ Sinteso fire safety technology and centralized monitoring to ensure continuous reliability and operational safety.

Southern and Northern Germany – Expanding Mid-Tier Data Center Ecosystem

Southern and Northern regions together account for around 35% of market share. Cities like Munich and Hamburg attract new colocation and enterprise facilities. Rising e-commerce and industrial digitalization drive investment in scalable security platforms. Vendors introduce modular systems to match regional facility sizes. It supports balanced development across multiple infrastructure clusters.

Eastern Germany – Emerging Growth Corridor for Edge and Government Data Centers

Eastern Germany captures nearly 20% share, led by government-backed infrastructure projects. Edge and regional centers expand near Dresden and Leipzig to improve latency coverage. Growing public-sector digitization initiatives stimulate physical security adoption. It positions Eastern Germany as a rising market for cost-efficient, compliant systems. Integration of local providers strengthens competitiveness in the national ecosystem.

- For instance, the Fraunhofer Institute operates edge-computing research facilities near Dresden focused on low-latency data processing and secure infrastructure. The organization also develops advanced biometric recognition and intelligent energy management technologies through its applied research programs.

Competitive Insights:

- Bosch Sicherheitssysteme GmbH

- Axis Communications AB

- Honeywell International Inc.

- Johnson Controls

- Schneider Electric SE

- Siemens AG

- Securitas AB

- Cisco Systems, Inc.

- Genetec Inc.

- Dahua Technology Co. Ltd.

The Germany Data Center Physical Security Market features a strong mix of global technology leaders and regional specialists competing through innovation and integration. It is shaped by continuous product upgrades, mergers, and strategic alliances across surveillance, access control, and automation domains. Bosch, Honeywell, and Schneider Electric focus on end-to-end security ecosystems, while Axis and Genetec emphasize analytics-driven video solutions. Cisco and Siemens strengthen their position through network-centric and building management integration. Securitas expands through managed security services tailored to colocation and enterprise facilities. The market favors players offering scalable, AI-powered, and regulation-compliant solutions that address both operational efficiency and risk reduction.

Recent Developments:

- In September 2025, European cloud and hosting provider IONOS launched a new data center location in Germany, expanding its physical infrastructure and likely deploying enhanced security measures at the site to support its customers’ needs.

- In October 2025, ASSA ABLOY acquired Kentix GmbH, a German company specializing in monitoring and access control products designed for data centers, enhancing their capabilities in physical security for this sector.

- In December 2024, Bosch Sicherheitssysteme GmbH sold its security and communications technology product business to the European investment firm Triton. The transaction included three business units Video, Access and Intrusion, and Communication as Bosch aims to focus more on systems integration business.