Executive summary:

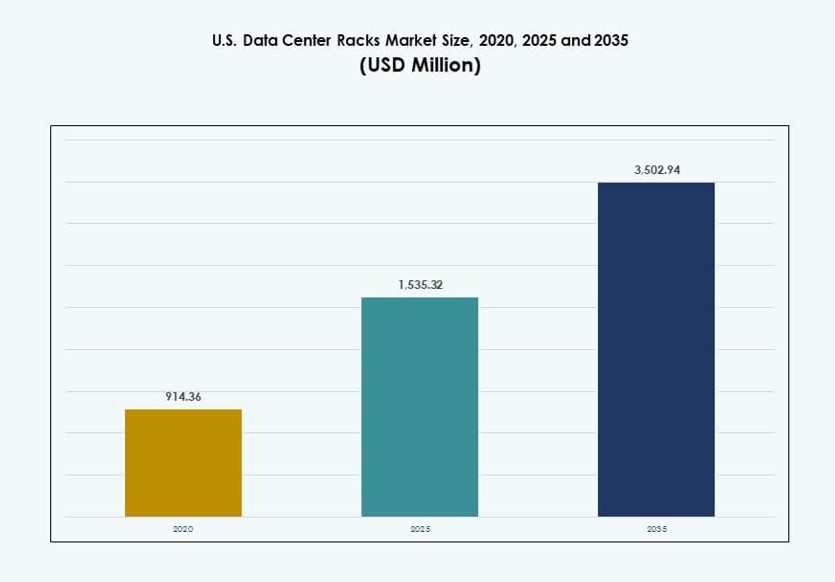

The U.S. Data Center Racks Market size was valued at USD 914.36 million in 2020 to USD 1,535.32 million in 2025 and is anticipated to reach USD 3,502.94 million by 2035, at a CAGR of 8.55% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| U.S. Data Center Racks Market Size 2025 |

USD 1,535.32 Million |

| U.S. Data Center Racks Market, CAGR |

6.74% |

| U.S. Data Center Racks Market Size 2035 |

USD 3,502.94 Million |

The market is being shaped by AI adoption, high-density compute clusters, and liquid-cooled infrastructure. Enterprises are shifting toward racks supporting 40–80 kW to handle GPU-powered workloads. Innovations in modular racks, smart PDUs, and pre-integrated thermal systems are accelerating deployments across core and edge environments. It plays a strategic role in enabling scalability, operational efficiency, and sustainability for cloud and enterprise players. Investors are prioritizing this space due to rising demand from AI factories and hyperscale facilities.

Northern Virginia leads the U.S. market with strong hyperscale concentration and robust fiber infrastructure. Texas, Arizona, and Ohio are emerging due to power availability, land access, and tax incentives. The West Coast remains vital, driven by AI hubs, cloud providers, and semiconductor infrastructure. Central states are also gaining traction as colocation firms expand into underserved but well-connected regions. This distribution supports diverse digital workloads and low-latency coverage.

Market Dynamics:

Market Drivers

Rising Adoption of AI Workloads and High-Density GPU Clusters in Core U.S. Data Centers

Enterprises and hyperscalers are deploying high-performance computing clusters for AI and ML workloads. This shift requires data center racks with advanced thermal management and power distribution. Liquid-cooled and hybrid racks now support up to 80 kW per rack in some facilities. The U.S. Data Center Racks Market is benefitting from GPU-hungry applications like LLM training and inferencing. Rack designs have evolved to support rear-door heat exchangers and sidecar cooling. These innovations make racks critical infrastructure in AI-native architectures. U.S. firms investing in AI are pushing demand for scalable rack platforms. Businesses see rack upgrades as foundational to futureproofing AI readiness. Investors target this market for its alignment with exponential compute growth.

- For instance, CoreWeave’s U.S. data centers deployed NVIDIA DGX GB200 SuperPOD racks, each supporting 132 kW per rack and housing 72 Blackwell GPUs per system to accelerate AI training workloads at scale. This setup reflects the growing demand for ultra-high-density rack infrastructure across AI-focused facilities.

Increased Modularization and Standardization to Accelerate Deployment Timelines for Hyperscale and Edge Facilities

Rack-level standardization is reshaping how new data centers are rolled out across the U.S. Pre-integrated modular rack systems reduce deployment time and optimize supply chains. OEMs are shipping rack-ready solutions that align with Open Compute Project (OCP) and Open19 standards. These efforts are reducing customization needs and enabling rack-level orchestration. The U.S. Data Center Racks Market supports this trend with pre-engineered enclosures tailored for scale. Colocation and hyperscale players are adopting repeatable rack designs for faster regional replication. Modular racks now ship with integrated PDUs, cabling, and containment. It ensures that deployment is predictable and serviceable at scale. The approach benefits service providers pursuing edge-to-core infrastructure models.

- For instance, Microsoft actively deploys Open Compute Project (OCP) V3 rack designs across its U.S. data centers, including in Chicago, to streamline modular infrastructure rollouts. These racks integrate standardized PDUs and cable management systems, supporting faster deployment and greater operational efficiency.

Stringent Energy Efficiency and Heat Dissipation Standards Are Redefining Rack Design and Cooling Integration

New efficiency regulations and rising operational costs drive innovation in rack cooling strategies. Traditional air-cooled racks face performance limits beyond 20–25 kW. Operators now turn to liquid cooling integrations with compatible rack formats. The U.S. Data Center Racks Market has responded with liquid-ready and hybrid-cooled rack configurations. These designs accommodate heat-intensive chipsets used in AI, blockchain, and 5G applications. Efficient cooling ensures rack density doesn’t compromise uptime or component lifespan. Vendors integrate sensors and environmental monitors directly into rack infrastructure. This trend enhances sustainability and meets ESG goals for enterprise operators. Energy-efficient rack setups help achieve long-term TCO optimization.

Enterprise Cloud Migration and Edge Data Center Expansion Reinforce Rack-Level Infrastructure as a Strategic Asset

Hybrid cloud adoption drives new infrastructure across both metro and edge zones in the U.S. Cloud-native businesses demand flexible rack infrastructure that supports rapid capacity scaling. The U.S. Data Center Racks Market is central to this transformation, powering Tier III and IV compliant rollouts. Enterprises are deploying micro data centers with 19-inch and 23-inch rack formats in distributed zones. These include telecom base stations, smart city nodes, and industrial automation sites. Rack deployments at the edge enable proximity computing and reduce latency. Federal and state governments also invest in localized IT resilience, creating more rack-based deployments. Rack infrastructure has moved beyond the backroom to the frontlines of digital transformation.

Market Trends

Rising Demand for AI-Optimized Racks with Integrated Liquid Cooling, Power, and Thermal Management

Purpose-built racks designed for AI hardware are becoming standard in new facilities. These racks include hot-swappable liquid cooling blocks, high-power PDUs, and telemetry systems. Integrated sensors allow real-time thermal control across rack-mounted GPUs. The U.S. Data Center Racks Market supports AI-native deployments with customizable high-wattage enclosures. Nvidia and AMD GPU clusters often require racks supporting 40–80 kW thermal loads. New facilities integrate these racks at design phase rather than retrofitting later. Rack manufacturers co-develop with cloud and AI firms to meet thermal and electrical requirements. Edge deployments are also seeing compact liquid-cooled rack units. This evolution signals a shift toward smarter, workload-aware rack formats.

Rapid Shift Toward Pre-Assembled Rack Systems That Support Faster Deployment and Scalability

Vendors now deliver pre-configured rack systems with integrated cable management, PDUs, and containment kits. These all-in-one racks reduce on-site integration time and staffing requirements. Operators deploy them across edge zones and colocation sites with speed and consistency. The U.S. Data Center Racks Market includes major OEMs focused on factory-integrated rack builds. This model fits enterprise hybrid strategies that blend core and edge computing. It also aligns with just-in-time facility expansions in high-demand regions. Rack integrators are forming partnerships with software vendors for plug-and-play orchestration. These turnkey units streamline data center build cycles. Pre-built racks support the shift toward infrastructure-as-a-service models.

Higher Rack Power Densities Prompt Evolution of Monitoring Tools and Environmental Controls

Rising rack wattages require advanced monitoring systems to maintain uptime and prevent thermal overloads. Vendors integrate smart sensors, airflow controls, and automated power alerts in rack enclosures. Operators use AI-driven dashboards to monitor rack health at a granular level. The U.S. Data Center Racks Market now offers racks embedded with thermal cameras and humidity detectors. These features enable predictive maintenance and real-time optimization. Facilities handling workloads above 30 kW per rack demand such precision tools. Smart racks help reduce energy waste and improve resource utilization. These systems are critical for colocation providers offering uptime SLAs. Environmental analytics become a competitive differentiator.

Wider Adoption of Open Frame and Custom Width Racks for Edge and High-Speed Interconnect Use Cases

Telecom and 5G rollout strategies drive demand for open frame racks in confined or distributed environments. These racks offer easier cable access and airflow in limited spaces. Network racks with 23-inch and custom widths are being deployed in cell sites, smart hubs, and urban shelters. The U.S. Data Center Racks Market supports this with robust SKUs tailored to edge deployment. Vendors are providing corrosion-resistant and ruggedized options for outdoor use. Edge AI and content delivery networks also use narrow racks to optimize vertical space. Custom depth and flexible rail mounting make these racks more versatile. These designs cater to low-footprint, high-connectivity deployments.

Market Challenges

Integration Complexities in AI-Driven Facilities with Multi-Vendor Rack Ecosystems and Cooling Technologies

Data centers deploying AI clusters face complex infrastructure integration issues at the rack level. Multiple vendors offer racks with proprietary thermal designs, making standardization difficult. Aligning GPU server specs, cooling systems, and PDUs creates configuration challenges. The U.S. Data Center Racks Market encounters fragmentation due to lack of cross-vendor compatibility. Operators struggle to unify power distribution across diverse rack types. Deploying liquid-cooled GPU racks next to air-cooled servers creates airflow conflicts. Inconsistencies in sensor protocols slow down centralized rack monitoring. These issues increase deployment time and raise the risk of thermal bottlenecks. Facilities need rack standards that streamline AI-native integrations.

Escalating Costs of High-Density Rack Components and Supply Chain Bottlenecks Impacting Deployment Timelines

High-performance racks with advanced cooling and power modules often carry significant cost premiums. Enterprises face budget constraints when scaling GPU-ready infrastructure. Custom-built racks also require longer lead times due to specialized manufacturing. The U.S. Data Center Racks Market deals with fluctuating steel and copper prices, which impact overall costs. Semiconductor shortages delay delivery of smart PDUs and rack-based sensors. Logistics disruptions further complicate multi-site rack deployments. Small and mid-sized data centers lack resources to absorb these delays. These challenges hinder regional deployment agility and delay service launches. Pricing volatility continues to influence rack procurement strategies.

Market Opportunities

AI Infrastructure Buildouts Create Demand for Ultra-High-Density Racks and Liquid-Cooling Ecosystems

AI training centers and LLM deployment zones are scaling across major metro areas. The U.S. Data Center Racks Market can serve these zones with 50–100 kW capable rack units. Rack vendors can co-innovate with GPU manufacturers and cloud firms to capture this demand. Opportunities also exist in hybrid racks integrating air and liquid cooling. Companies that offer full-stack rack systems with orchestration APIs will gain strategic value. Growth in AI infrastructure opens recurring revenue from managed rack systems.

Edge Expansion Enables Rack Penetration Across Non-Traditional Sectors and Smart Infrastructure Projects

Demand for edge computing pushes rack deployment in retail, logistics, and government locations. The U.S. Data Center Racks Market can expand in Tier II and III cities through modular micro racks. Vendors offering ruggedized, narrow-width racks gain access to telecom and smart city contracts. Growth in surveillance, industrial IoT, and mobile compute boosts edge rack demand. Strategic partnerships with telecom firms will unlock regional rack market segments.

Market Segmentation

By Rack Type

Cabinet racks dominate the U.S. Data Center Racks Market, holding the highest share due to their flexibility, security, and ability to support high-density configurations. They are widely used in hyperscale and enterprise environments requiring structured cable management and airflow control. Open frame racks are gaining popularity in test environments and edge deployments due to their accessibility. The “Others” segment includes wall-mount and custom enclosures serving niche use cases.

By Rack Height

42U racks are the most widely adopted in the U.S. Data Center Racks Market, balancing capacity with compatibility. They support efficient vertical space use and simplify standardization across facilities. Above 42U racks are growing in large-scale deployments, particularly for AI and GPU-heavy workloads. Below 42U racks serve edge, retail, and smaller setups needing space-constrained solutions.

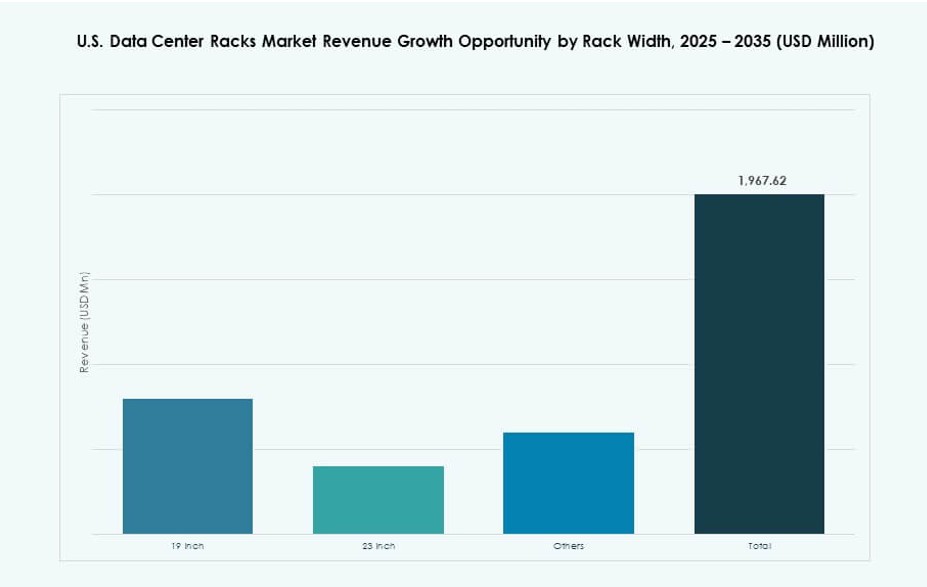

By Width

The 19-inch width remains the industry standard and leads the U.S. Data Center Racks Market due to its broad compatibility with IT equipment. It suits most server, network, and storage devices. The 23-inch width segment is gaining relevance in telecom and carrier-grade installations. Custom and “Others” width racks address specialized configurations across military and healthcare verticals.

By Application

Server racks dominate the U.S. Data Center Racks Market due to the large volume of compute resources deployed in colocation and enterprise facilities. Network racks play a supporting role, used for structured cabling and network interconnection gear. The server rack segment continues to expand as enterprises transition to cloud-ready and AI-based workloads.

By End-user

Large data centers are the key consumers in the U.S. Data Center Racks Market, contributing the highest revenue share. Hyperscale operators, cloud providers, and major colocation firms drive most of the demand. Small and mid-sized data centers represent an emerging segment, especially in edge computing zones and regional service areas.

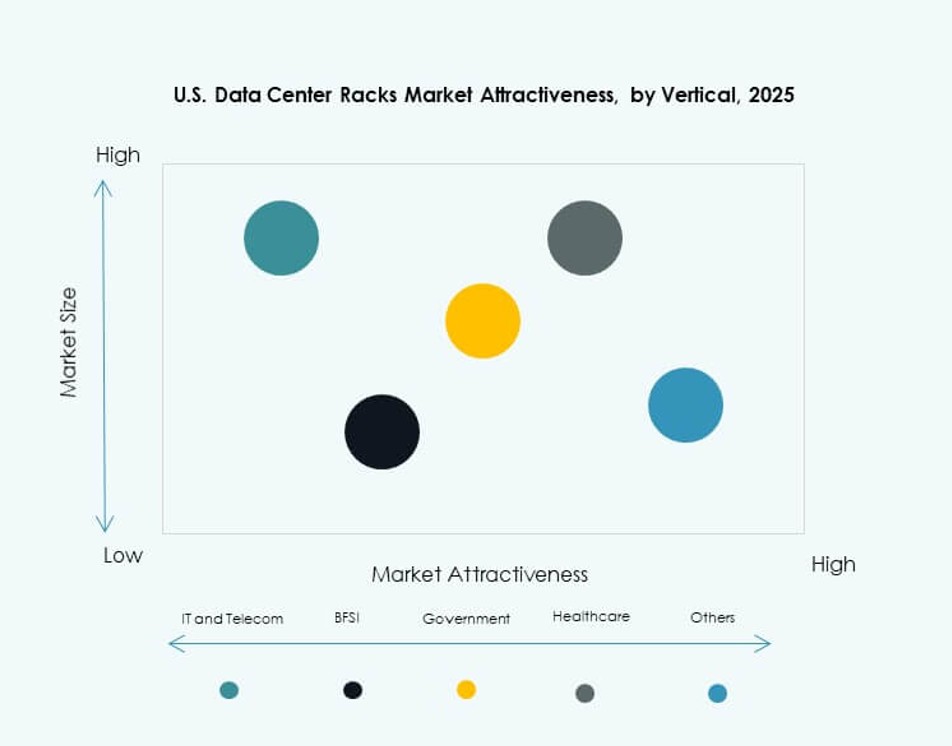

By Vertical

IT & Telecom is the largest vertical in the U.S. Data Center Racks Market, driven by cloud expansion and 5G infrastructure needs. Government & Defense and BFSI sectors are also major users due to security and compliance needs. Healthcare and Energy segments are growing as they modernize digital infrastructure. Retail and Others represent emerging verticals adopting edge-based rack deployments.

Regional Insights

Northern Virginia and the East Coast Maintain Over 40% Market Share Due to Hyperscale and Federal Demand

Northern Virginia, home to Ashburn’s data center alley, leads the U.S. Data Center Racks Market with over 40% share. This region hosts major hyperscale operations and federal cloud initiatives. Dense fiber infrastructure, favorable policies, and power availability support continuous rack deployment. States like Maryland and North Carolina complement this growth with enterprise and colocation facilities. The East Coast is also home to emerging edge nodes supporting AI and content delivery. It remains a critical investment zone for both domestic and global players.

Texas, Arizona, and the Midwest Hold Nearly 30% Market Share Due to Power Availability and Tax Incentives

Southern and central U.S. states such as Texas and Arizona contribute nearly 30% of the U.S. Data Center Racks Market. These states attract rack-heavy deployments due to ample power, real estate, and tax incentives. Dallas, Phoenix, and Columbus are seeing increased hyperscale builds. The Midwest is gaining traction with states like Iowa and Ohio offering low-latency access to the East and West coasts. Rack vendors find opportunity here through OEM integration at the hyperscale and regional level.

- For instance, Meta is developing a large-scale data center campus in Temple, Texas, with planned investments exceeding $800 million to support AI and cloud infrastructure. The region continues to attract hyperscale operators due to its power availability and expansion-ready land.

West Coast States Contribute Around 20% Market Share Due to Cloud Hubs and AI Innovation Zones

California, Oregon, and Washington account for approximately 20% of the U.S. Data Center Racks Market. These states are central to AI innovation, public cloud expansion, and semiconductor development. Silicon Valley continues to drive rack upgrades for AI inferencing and training clusters. Oregon offers energy-efficient hosting with green power incentives. The West Coast remains vital for high-density rack deployments, especially in AI, biotech, and high-frequency trading environments. Rack vendors collaborate with AI firms on advanced enclosures in these zones.

- For instance, Microsoft launched its first Azure region in Austria in 2025 with three availability zones to support regional cloud demand. In the U.S., EdgeCore’s Prince William County campus in Virginia is publicly planned to scale up to 1.1 GW, making it one of the largest hyperscale developments aimed at high-density deployments.

Competitive Insights:

- Schneider Electric

- Vertiv Group

- Rittal

- Eaton

- AMCO Enclosures

- Belden Inc.

- Chatsworth Products

- Cisco Systems, Inc.

- Dell Inc.

- Hewlett Packard Enterprise (HPE)

The U.S. Data Center Racks Market is highly competitive, with global and domestic players actively innovating to meet rising rack density, thermal load, and edge deployment needs. Schneider Electric and Vertiv lead with advanced modular designs and integrated cooling systems. Rittal and Eaton offer scalable cabinet solutions aligned with OCP standards. Dell, Cisco, and HPE bundle racks with compute infrastructure, giving them strategic advantage in enterprise contracts. AMCO Enclosures and Chatsworth focus on customized enclosures and telecom-specific designs. Vendors are forming partnerships to co-develop liquid-ready racks for AI workloads. It continues to attract players offering integrated power, cable, and airflow control features. Competitors are expanding production and local support to serve hyperscale and colocation growth across U.S. regions.

Recent Developments:

- In July 2025, Vertiv acquired Great Lakes Data Racks & Cabinets for approximately USD 200 million, expanding its portfolio of high-density, AI-ready rack solutions to meet surging demand in hyperscale data centers.

- In June 2025, Schneider Electric launched EcoStruxure Pod Data Center and EcoStruxure Rack Solutions featuring integrated rack configurations for high-density AI clusters exceeding 1MW power demands.

- In May 2025, Vertiv launched an 800 VDC power architecture tailored for AI factories, featuring centralized rectifiers and rack-level converters that reduce copper usage and enhance energy efficiency.

- In March 2025, Schneider Electric collaborated with ETAP and NVIDIA on digital twin technology using NVIDIA Omniverse to enhance real-time data center operations, supporting rack power densities up to 132kW for AI factories.