Executive summary:

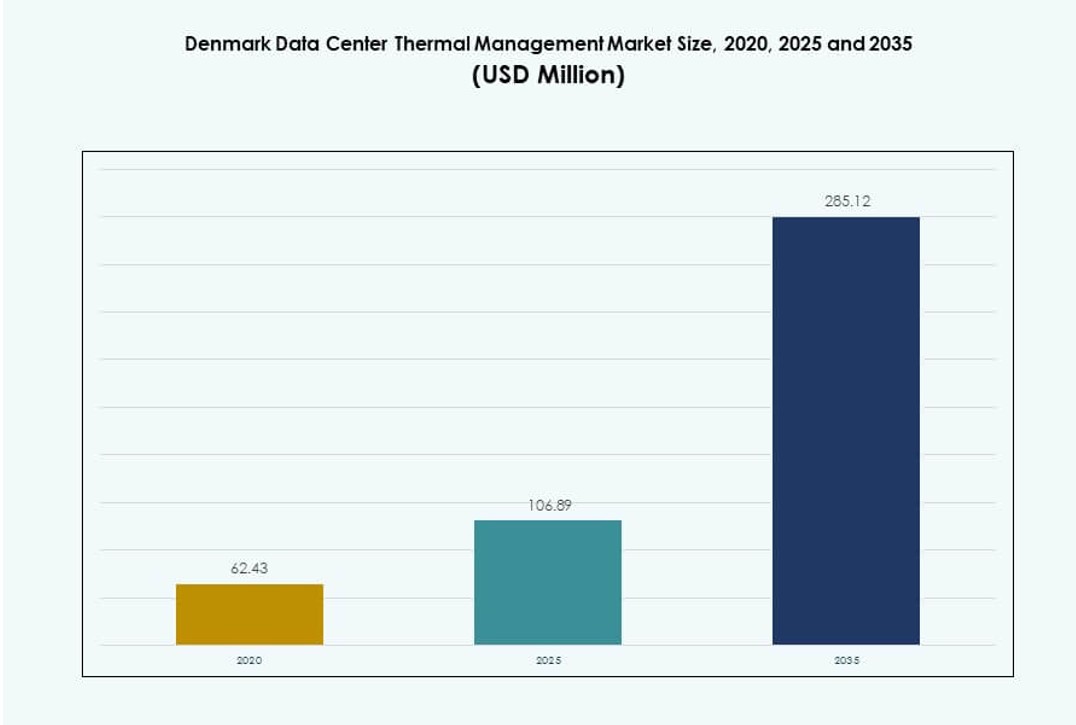

The Denmark Data Center Thermal Management Market size was valued at USD 62.43 million in 2020, increased to USD 106.89 million in 2025, and is anticipated to reach USD 285.12 million by 2035, at a CAGR of 10.25% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Denmark Data Center Thermal Management Market Size 2025 |

USD 106.89 Million |

| Denmark Data Center Thermal Management Market, CAGR |

10.25% |

| Denmark Data Center Thermal Management Market Size 2035 |

USD 285.12 Million |

The market is driven by rising demand for energy-efficient cooling systems amid growing hyperscale and AI-focused data centers. Companies are adopting liquid-based and hybrid cooling solutions to support high-density computing with reduced energy consumption. Smart thermal monitoring, AI-based optimization, and modular designs are reshaping operations. These shifts enable better resource utilization, uptime, and environmental compliance. For businesses and investors, the market offers long-term growth potential aligned with Denmark’s national green goals and strong digital infrastructure momentum.

Greater Copenhagen leads the market due to hyperscale deployments and international connectivity. Its mature infrastructure attracts major colocation and cloud service providers. Eastern Denmark is emerging with public sector initiatives, R&D investments, and sustainability-focused upgrades. Western Denmark supports edge and localized facilities for industrial and rural applications. These subregional dynamics reinforce Denmark’s strategic role in Northern Europe’s sustainable data center landscape.

Market Dynamics:

Market Drivers

High-Density Computing Workloads Driving Advanced Thermal Solutions Demand

Enterprise IT infrastructure in Denmark is shifting toward high-density racks that exceed 20 kW per rack. This intensifies the demand for next-generation thermal systems such as direct-to-chip liquid cooling and rear door heat exchangers. Operators prioritize performance efficiency and heat management in smaller footprints. The Denmark Data Center Thermal Management Market benefits from this transition, supporting precision control over thermal loads. New deployments focus on reducing energy consumption while maintaining uptime. Equipment manufacturers respond by developing systems tailored for AI and HPC loads. It reinforces the need for tailored cooling in compact hyperscale environments. Thermal systems are no longer support functions but mission-critical layers. This elevates the strategic role of thermal innovation in infrastructure planning.

Policy-Backed Decarbonization Driving Sustainable Thermal Management Adoption

Denmark’s climate policies create incentives for data centers to reduce carbon output. Thermal systems play a critical role in energy efficiency, heat reuse, and water-free cooling. The national strategy encourages renewable integration across power and cooling operations. The Denmark Data Center Thermal Management Market reflects this shift, with operators investing in technologies that align with green metrics. Liquid cooling, ambient air systems, and dry coolers are prioritized for their sustainability profile. It supports investor confidence in long-term operational savings and environmental compliance. ESG-focused funds target assets that reduce scope 1 and 2 emissions. Government support boosts retrofits of legacy sites to align with newer thermal benchmarks. Operators deploy smart cooling to meet future emissions targets.

AI and Machine Learning Applications Reinforcing Thermal Infrastructure Upgrades

AI and machine learning workloads require stable thermal conditions for optimal performance. Denmark’s digital economy invests in platforms handling model training, simulation, and automation. These systems generate high heat density, challenging conventional cooling methods. The Denmark Data Center Thermal Management Market gains from AI infrastructure expansion. AI-ready systems adopt hybrid cooling, combining liquid and air for performance and resilience. It ensures minimal thermal fluctuations and greater workload efficiency. Intelligent cooling platforms also use AI to optimize energy use in real time. This integration reduces OPEX and supports scalability. Thermal management has become a foundational layer in AI infrastructure design.

- For instance, Bulk Infrastructure’s N01 data center campus in Norway added a 12 MW facility in 2023, fully contracted to meet demand for high-density AI and HPC workloads. The campus operates on 100% renewable energy and supports scalable GPU and CPU infrastructure.

Growing Colocation and Edge Deployment Accelerating Scalable Thermal Strategies

Colocation providers expand facilities to meet rising enterprise demand for cloud and hybrid services. These facilities must support diverse workloads and tiered cooling strategies. Modular thermal systems enable quick scaling across phases. The Denmark Data Center Thermal Management Market reflects this flexibility with rising demand for row-based and rack-based solutions. Edge data centers emerge across urban and industrial zones, requiring localized cooling. It drives innovation in compact, energy-efficient cooling systems. Colocation firms adopt predictive thermal management for uptime assurance. Standardized cooling helps reduce installation timelines and ensures design uniformity. Infrastructure providers invest in flexible platforms to meet future thermal needs.

- For instance, Aalborg Forsyning is deploying four MAN Energy Solutions heat pumps with a total capacity of 177 MW, using seawater as the heat source for district heating. This system is expected to cut up to 210,000 tons of CO₂ annually, supporting Denmark’s green energy transition.

Market Trends

Adoption of Heat Reuse and District Heating Integration in Data Center Sites

Denmark’s commitment to sustainability includes leveraging waste heat from data centers for public heating. Operators integrate heat reuse systems with municipal grids for residential or industrial use. This model reduces carbon emissions while monetizing excess thermal energy. The Denmark Data Center Thermal Management

Market reflects this integration across both hyperscale and enterprise facilities. It builds cross-sector partnerships between utility providers and colocation players. Cooling infrastructure now includes heat exchangers and smart transfer modules. Heat reuse aligns thermal strategies with circular economy goals. It supports permit approvals and enhances public support. Operators gain a long-term asset value through energy circularity.

Expansion of Immersion Cooling in AI and High-Performance Compute Facilities

Immersion cooling enters mainstream deployment across AI and blockchain processing environments. The technology submerges hardware in dielectric liquid to manage extreme thermal output. Its efficiency surpasses conventional systems in compact rack environments. The Denmark Data Center Thermal Management Market includes strong growth in immersion-based setups. Operators value reduced space, minimal mechanical parts, and better heat removal. It enables quiet operation and lower maintenance overhead. Vendors provide prefabricated immersion modules to simplify deployment. It enhances rack densities in space-constrained sites. AI-heavy data centers adopt immersion cooling to support 200–300 kW rack loads.

Use of AI-Based Thermal Management for Real-Time Optimization and Fault Prediction

Operators now use AI-powered tools to monitor and control thermal loads across facilities. These platforms track temperature, airflow, and energy consumption across racks in real time. AI predicts system anomalies and initiates preemptive adjustments to avoid faults. The Denmark Data Center Thermal Management Market supports adoption of DCIM-integrated thermal controls. Software platforms recommend cooling profiles based on usage patterns and weather data. It improves energy efficiency by avoiding overcooling. This trend reduces staff workload and improves uptime metrics. Predictive systems offer insights that drive better planning. Data centers view AI-based cooling as a strategic cost and performance enabler.

Shift Toward Modular and Scalable Thermal Management Solutions in New Builds

Prefabricated and modular cooling systems gain favor for fast deployment and easy scaling. Operators demand thermal units that can expand with IT loads across growth phases. Modular cooling reduces build timelines while maintaining system integrity. The Denmark Data Center Thermal Management Market reflects this shift toward containerized and plug-and-play designs. It supports colocation providers who build in phases. Modular systems integrate with both liquid and air systems. Vendors offer compatibility with hot/cold aisle setups and hybrid cooling methods. It helps operators avoid over-provisioning while remaining expansion-ready. Modular thermal infrastructure accelerates time-to-market and cost control.

Market Challenges

Balancing High-Density Rack Cooling with National Energy Efficiency Goals

High-density servers generate extreme thermal loads that strain traditional cooling infrastructure. While operators adopt liquid cooling, integrating it with legacy air systems remains complex. Many facilities lack the layout to support direct-to-chip or immersion cooling. The Denmark Data Center Thermal Management Market faces pressure to reconcile high-performance workloads with sustainability mandates. Operators must stay within power usage limits even when demand surges. Failure to optimize cooling leads to system instability and higher OPEX. Utility regulations tighten around energy use per square meter. It forces providers to balance performance with compliance. Legacy infrastructure requires expensive retrofitting to meet modern cooling demands.

Limited Skilled Workforce and Integration Delays in Advanced Cooling Projects

Deployment of smart or hybrid cooling systems often needs specialist knowledge. Local talent gaps in CFD modeling, AI thermal controls, and fluid system management delay rollout. Projects stall due to integration complexity across software and hardware interfaces. The Denmark Data Center Thermal Management Market must overcome limited technical expertise in regional hubs. Vendor dependency increases when in-house capabilities are low. It slows commissioning and increases deployment risks. Continuous training and skill building become essential. Delays raise CAPEX and frustrate colocation clients waiting for access. High-level integration between IT and OT layers remains a persistent barrier.

Market Opportunities

Growing Preference for Smart, Sustainable Cooling Among Hyperscale Operators

Hyperscale companies continue investing in smart cooling to meet ESG goals and efficiency targets. Denmark’s renewable energy profile enhances appeal for green facility expansion. The Denmark Data Center Thermal Management Market offers strong potential for scalable, low-emission cooling systems. It supports investment in liquid-air hybrids and AI-driven monitoring platforms. Operators seek suppliers with proven efficiency metrics and compatibility with carbon offset strategies.

Rising Edge Deployment Driving Compact and Remote Cooling Innovation

Edge computing requires thermal solutions tailored for micro facilities in remote or urban sites. Denmark’s smart city initiatives and IoT rollouts push demand for localized infrastructure. The Denmark Data Center Thermal Management Market creates opportunities in compact, self-regulating cooling units. Vendors gain from edge-specific products with rapid deployment features. Market growth links directly to sensor-driven thermal automation at edge nodes.

Market Segmentation

By Data Center Size

Large data centers dominate the Denmark Data Center Thermal Management Market due to hyperscale expansions. These facilities account for the highest share driven by large IT loads and energy efficiency mandates. Medium-sized centers follow closely, serving enterprise and public workloads. Small data centers remain relevant for edge computing and disaster recovery. Large facilities invest more in liquid and hybrid cooling to manage dense server environments.

By Cooling Technology

Air-based cooling remains the most widely deployed segment due to legacy systems and cost efficiency. Direct air and hot/cold aisle configurations dominate in small to medium setups. Liquid-based cooling is growing fast, driven by AI and HPC infrastructure, with direct-to-chip emerging as a key technology. Hybrid systems combining both liquid and air serve high-density, scalable environments. Thermoelectric and phase-change systems stay niche but support innovation.

By Component

Hardware contributes the largest revenue share in the Denmark Data Center Thermal Management Market. Demand stems from physical cooling units, fans, heat exchangers, and liquid distribution systems. Software is growing due to DCIM, CFD tools, and AI-based control systems. Services gain importance in retrofits, preventive maintenance, and real-time monitoring, especially for colocation and multi-tenant facilities.

By Hardware

Cooling units and chillers lead the hardware segment, followed by fans and heat exchangers. Advanced setups use rear door units and direct liquid modules. Piping and fluid distribution systems are essential for liquid cooling. Other components like leak detection systems and airflow controllers add to the reliability. Hardware performance directly influences uptime and PUE benchmarks.

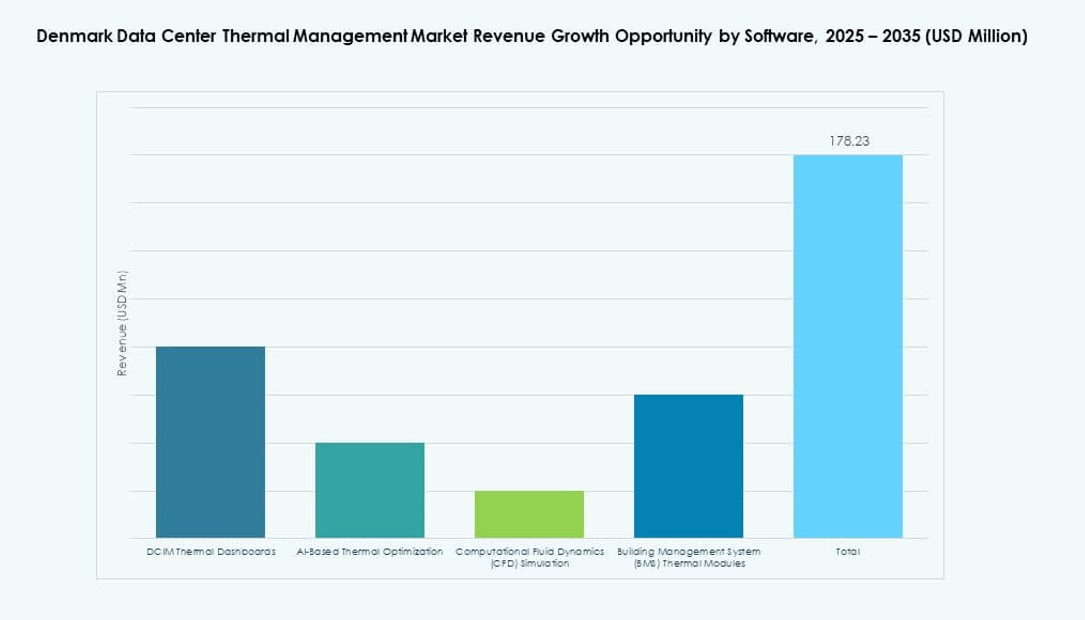

By Software

DCIM dashboards lead in adoption, enabling centralized visibility and thermal control. AI optimization platforms follow, offering real-time analytics and system learning. CFD simulation tools support airflow planning in both greenfield and retrofit projects. BMS modules integrate cooling with broader facility controls. These tools help reduce manual intervention and boost automation in complex thermal environments.

By Services

Installation and commissioning dominate, especially for new builds and capacity expansions. Preventive maintenance ensures long-term system reliability and avoids downtime. Monitoring-as-a-Service gains from operators outsourcing temperature tracking and fault detection. Retrofit and upgrade services rise with aging infrastructure modernization. Others include training, consultation, and performance audits to enhance system output.

By Data Center Type

Hyperscale centers hold the largest share with ongoing expansion by global tech firms. Colocation/cloud providers also invest in scalable thermal platforms. Enterprise centers use standardized systems but seek energy savings. Edge and micro centers emerge with compact, integrated cooling. Other data centers include government and university setups, focusing on reliability and green metrics.

By Structure

Room-based cooling still dominates in legacy setups but loses share to modular systems. Rack-based cooling gains in edge and AI data centers due to compactness. Row-based systems strike a balance between scalability and performance. Vendors focus on integrated offerings that support fast deployment and energy control. Rack and row systems align with high-density and hybrid environments.

Regional Insights

Greater Copenhagen Leading in Hyperscale and Colocation Investments

Greater Copenhagen holds over 60% of the Denmark Data Center Thermal Management Market due to hyperscale campuses and network hubs. Its access to international fiber, stable power grid, and clean energy makes it ideal for large deployments. Major colocation providers expand facilities to serve growing enterprise workloads. It remains the epicenter for AI-ready and high-density installations. Public-private partnerships accelerate smart grid integration for efficient thermal operations.

- For instance, STACK Infrastructure opened a data center campus outside Copenhagen in Høje-Taastrup, securing initial power capacity for multiple water-cooled halls to support high-density AI workloads.

Eastern Denmark Emerging with Renewable Integration and Green Data Center Projects

Eastern Denmark contributes around 25% of market share, driven by renewable power availability and public sector IT needs. Cities like Odense and Køge attract attention with land availability and heat reuse infrastructure. Operators leverage district heating networks to monetize excess heat. It pushes adoption of heat exchangers and thermal recovery modules. The region supports medium-sized data centers for research, healthcare, and e-government.

Western Denmark Supporting Edge and Regional Infrastructure Growth

Western Denmark accounts for nearly 15% of market share, supported by edge deployments and secondary hubs. Local governments promote digital access in rural and industrial zones. Smaller facilities use modular cooling systems and containerized designs. It enables rapid setup and low environmental impact. Regional providers target energy-efficient solutions for disaster recovery and latency-sensitive applications. Market activity grows with expansion of 5G and IoT ecosystems.

- For instance, Thylander plans a 100 MW hyperscale data center in Esbjerg with initial 10-20 MW phase in 2026, integrating seawater cooling from a former power plant and excess heat into local district heating.

Competitive Insights:

- Vertiv Group Corp.

- Johnson Controls International plc

- Mitsubishi Electric Corporation

- Daikin Industries Ltd.

- Delta Electronics, Inc.

- Asetek, Inc.

- Trane Technologies plc

- Airedale International Air Conditioning Ltd.

- Danfoss

- Grundfos

Competitors in the Denmark Data Center Thermal Management Market focus on product differentiation and customization for high-performance environments. Leading firms leverage strong service networks and brand recognition to secure large contracts with hyperscale and colocation providers. It pushes vendors to enhance system efficiency, modular design, and real-time monitoring tools. Partnerships between thermal hardware makers and software developers bolster predictive maintenance and optimization features. Mid‑tier players emphasize niche solutions like immersion cooling or compact systems for edge facilities. Price competition influences purchasing decisions for smaller data centers. Established vendors drive innovation through R&D and frequent product upgrades. Market share shifts toward firms that deliver scalable solutions with lower total cost of ownership and reliable performance.

Recent Developments:

- In December 2025, Trane Technologies entered a deal to acquire Stellar Energy Digital, integrating modular cooling into its Americas HVAC unit for data center growth. The move targets agile, sustainable solutions for high-growth thermal management.

- In November 2025, Daikin Applied acquired Chilldyne for negative pressure direct-to-chip liquid cooling, complementing prior buys for hyperscale efficiency.