Executive summary:

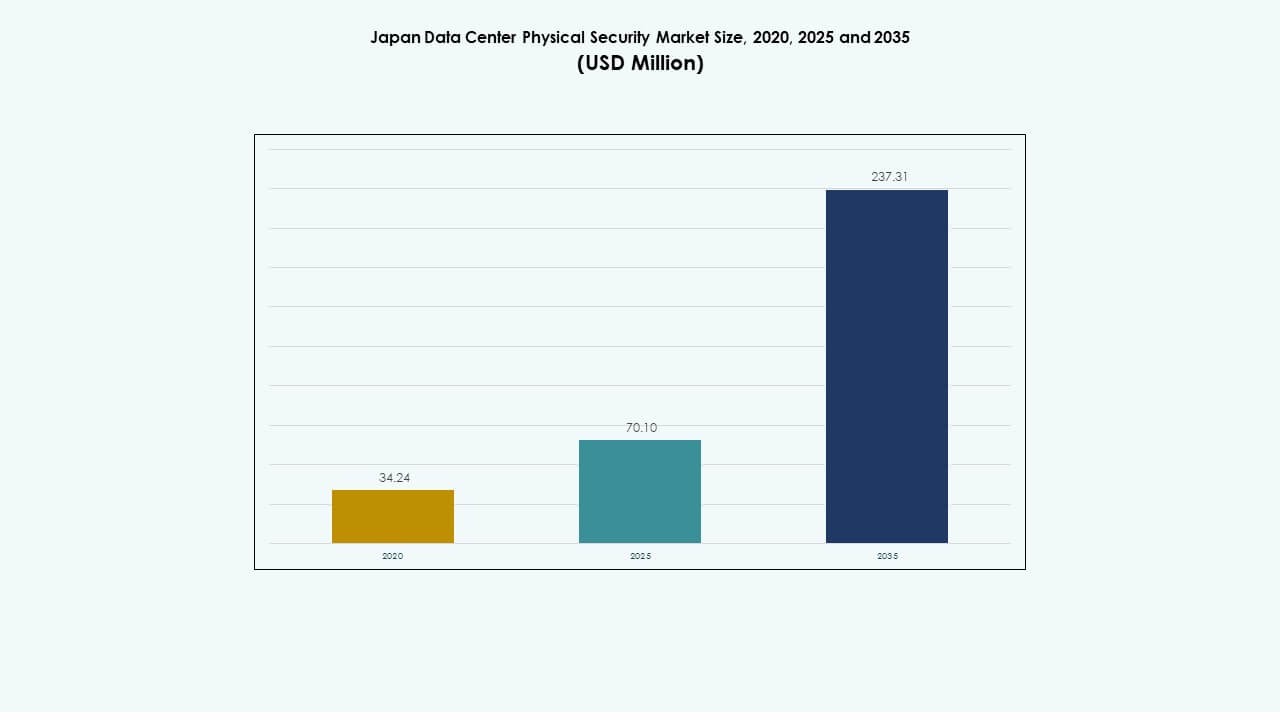

The Japan Data Center Physical Security Market size was valued at USD 34.24 million in 2020 to USD 70.10 million in 2025 and is anticipated to reach USD 237.31 million by 2035, at a CAGR of 12.89% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Japan Data Center Physical Security Market Size 2025 |

USD 70.10 Million |

| Japan Data Center Physical Security Market, CAGR |

12.89% |

| Japan Data Center Physical Security Market Size 2035 |

USD 237.31 Million |

Growing emphasis on digital infrastructure expansion and AI-driven surveillance technologies fuels market growth. The sector benefits from increasing deployment of hyperscale and colocation facilities that require multi-layered defense mechanisms. Rising investments in biometric access control, intrusion detection, and integrated monitoring systems strengthen the market. It holds strategic importance for investors due to strong compliance standards, technological innovation, and high capital reliability within Japan’s data center ecosystem.

Tokyo and the Kanto region dominate due to dense enterprise clusters and hyperscale facilities supporting major cloud providers. The Kansai region, led by Osaka, emerges as a key secondary hub driven by new colocation projects. Northern regions like Hokkaido gain traction for their cooler climates and renewable energy potential, attracting green data center investments. Expanding edge infrastructure in regional zones supports balanced national market growth.

Market Drivers

Expanding Digital Infrastructure and Rising Data Center Construction

The Japan Data Center Physical Security Market benefits from rapid digital transformation across industries. Growing deployment of hyperscale and edge data centers drives strong demand for advanced security solutions. Operators prioritize physical resilience to safeguard equipment from theft and sabotage. New projects in Tokyo, Osaka, and Fukuoka emphasize redundant surveillance and biometric access systems. It gains traction as investors seek reliable long-term infrastructure returns. Rising workloads from cloud, AI, and IoT create additional data capacity requirements. This growth fosters modernization of existing facilities. The surge in private and public cloud services enhances spending on site-level protection.

- For instance, by 2025, Tokyo is set to contribute over 1 GW of new data center power capacity, while Osaka is adding around 440 MW, supporting Japan’s total data center capacity growth to approximately 2.3 GW. These figures come from a comprehensive database cataloguing 115 active facilities and 46 upcoming projects across Japan, including major hubs like Tokyo, Osaka, and Fukuoka.

Adoption of AI-Driven Surveillance and Automation Technologies

Artificial intelligence adoption transforms surveillance and monitoring processes. Smart cameras integrated with analytics tools deliver real-time threat identification. Automated incident alerts reduce human error and improve response accuracy. In the Japan Data Center Physical Security Market, this innovation ensures proactive defense for mission-critical environments. Automation supports centralized monitoring of multiple sites across regions. AI systems analyze behavioral patterns to prevent unauthorized entry attempts. Companies investing in such tools improve operational continuity. AI-integrated solutions also comply with national safety and privacy mandates. Advanced automation builds confidence among investors and clients managing sensitive data.

- For example, SoftBank is developing major AI data centers in Japan, including a 300 MW facility in Hokkaido’s Tomakomai and a 150 MW expandable site in Osaka’s Sakai district. These projects aim to strengthen Japan’s AI computing capacity and support national digital infrastructure expansion.

Rising Emphasis on Compliance and Cyber-Physical Integration

Stringent regulations by the Ministry of Internal Affairs and Communications drive compliance-based investments. Operators integrate physical and cyber defenses to achieve unified protection frameworks. It pushes vendors to design systems that detect both hardware intrusion and network breaches. The Japan Data Center Physical Security Market experiences stronger spending from BFSI and government sectors. Biometric authentication, audit trails, and encryption hardware form a standard security stack. Global certifications such as ISO 27001 and ISMS certification become crucial for credibility. Compliance strengthens investor trust and ensures uninterrupted operations. The growing importance of regulatory alignment creates sustained growth potential.

Increased Private Investment and Strategic Partnerships

Private equity firms and real estate funds expand portfolios by investing in data center campuses. Rising valuations encourage security system upgrades for asset protection. It demonstrates that investors see security as a key operational differentiator. Partnerships between Japanese firms and global vendors accelerate technology adoption. Domestic manufacturers collaborate with software providers to offer integrated security ecosystems. Increased competition pushes suppliers to enhance analytics and access control features. Demand for sustainability-compliant security systems also rises. These investment trends highlight the strategic value of the market in supporting Japan’s digital economy.

Market Trends

Shift Toward Biometric and Touchless Access Solutions

Touchless systems gain traction due to pandemic-driven safety norms and convenience. The Japan Data Center Physical Security Market sees wide adoption of facial and iris recognition devices. Contactless entry lowers contamination risks while improving access control speed. Organizations prefer multimodal biometric systems for higher verification accuracy. These tools integrate with cloud management software to track entry logs securely. Facility managers favor solutions with fast integration into legacy systems. AI-enhanced biometrics streamline both workforce and visitor management. The rise of non-contact security fosters a more efficient and hygienic environment.

Growing Use of IoT Sensors and Smart Monitoring Networks

IoT-based surveillance brings precision to threat detection and environmental control. Real-time sensor data helps operators track temperature, motion, and entry points. The Japan Data Center Physical Security Market benefits from systems connecting through secure IoT gateways. Predictive maintenance alerts improve equipment reliability and reduce downtime. Cloud platforms allow remote oversight of multiple facilities. Integrated IoT frameworks enhance situational awareness in large-scale campuses. These advancements attract enterprises seeking unified operational dashboards. Adoption continues to rise as firms balance efficiency with high-level protection.

Integration of Cloud-Based Video Surveillance Systems

Cloud-managed video analytics enable scalable and flexible control. Data center managers prefer remote-access solutions with automatic data backup. It strengthens resilience during emergency situations. The Japan Data Center Physical Security Market expands through vendors offering hybrid cloud platforms. Video surveillance-as-a-service (VSaaS) models reduce upfront hardware costs. AI-enhanced footage analysis enables faster decision-making. Cloud storage secures recordings while allowing compliance with retention laws. This shift transforms security management into a data-driven discipline. Cloud-based infrastructure becomes central to future-ready protection strategies.

Sustainability and Green Data Center Security Initiatives

Operators implement eco-efficient designs for energy and resource optimization. Security vendors align products with green compliance standards. It drives installation of low-power cameras and smart lighting systems. The Japan Data Center Physical Security Market adopts sustainability-driven procurement policies. Facilities utilize modular systems that minimize waste during upgrades. Green-certified components help reduce total operational emissions. Integrating sustainability with security boosts brand reputation. Eco-conscious buyers favor solutions that merge efficiency with resilience.

Market Challenges

High Capital Expenditure and Integration Complexities

Upgrading traditional systems requires substantial investment in hardware and software integration. The Japan Data Center Physical Security Market faces cost barriers for small and medium data centers. Implementing biometrics, sensors, and AI-based analytics increases setup costs. Compatibility between new and legacy equipment complicates rollout schedules. Vendors must provide scalable options to reduce total ownership cost. Delays in component availability hinder continuous operations. Supply chain disruptions caused by global semiconductor shortages raise procurement risks. Firms that fail to modernize face higher vulnerability levels. Cost optimization remains a central challenge for many operators.

Shortage of Skilled Workforce and Evolving Threat Landscape

Japan experiences a shortage of trained professionals managing hybrid physical-cyber systems. The Japan Data Center Physical Security Market requires multidisciplinary expertise in AI, automation, and infrastructure. Recruiting and retaining specialists becomes difficult amid rising industry competition. New threat types demand continuous skill upgrading. Cyber-physical convergence increases the need for adaptive training. Lack of workforce readiness delays system response and maintenance efficiency. Changing compliance frameworks further add to training complexity. Security lapses from human errors continue to challenge operators’ resilience strategies.

Market Opportunities

Expansion of Edge and Regional Data Centers Across Japan

Emerging data centers in Hokkaido, Kyushu, and Okinawa present new demand zones. The Japan Data Center Physical Security Market benefits from expansion beyond Tokyo and Osaka. Edge computing sites need localized surveillance and automated access systems. It opens prospects for regional system integrators and local technology providers. Vendors offering modular security architectures gain traction. Rising investments in regional connectivity increase equipment orders. Government incentives supporting digital infrastructure further strengthen growth prospects. Regional expansion ensures broader adoption of standardized protection frameworks.

Innovation in AI Analytics and Unified Security Platforms

AI-powered monitoring platforms enable intelligent event correlation and predictive alerts. Integration of physical and logical security layers creates seamless oversight. The Japan Data Center Physical Security Market gains new opportunities from AI-based threat modeling. Firms offering unified dashboards enhance visibility and control across facilities. These tools improve compliance management and reduce downtime. Strategic collaborations between hardware makers and software providers spur innovation. AI analytics create competitive advantages for early adopters. Unified security management becomes a key differentiator in long-term contracts.

Market Segmentation

By Data Center Size

Large data centers dominate due to hyperscale deployments by global cloud providers. These facilities require multi-layered access systems and continuous monitoring networks. The Japan Data Center Physical Security Market sees medium centers gaining traction from enterprise digital transformation. Small centers remain focused on cost-efficient yet compliant systems. Growth in AI workloads drives higher adoption of scalable security architectures. Large centers capture nearly 55% of total demand. Their role in serving cloud and content delivery platforms sustains long-term investment.

By Component

Solutions lead the component segment with advanced integration capabilities. The Japan Data Center Physical Security Market observes strong growth in analytics-enabled solutions like surveillance and access control. Services such as maintenance and consulting ensure lifecycle performance. Integration and support services expand alongside new construction projects. Vendors offering end-to-end coverage secure large contracts. Services represent around 40% of total spending. The combination of both elements ensures reliable and compliant protection across facilities.

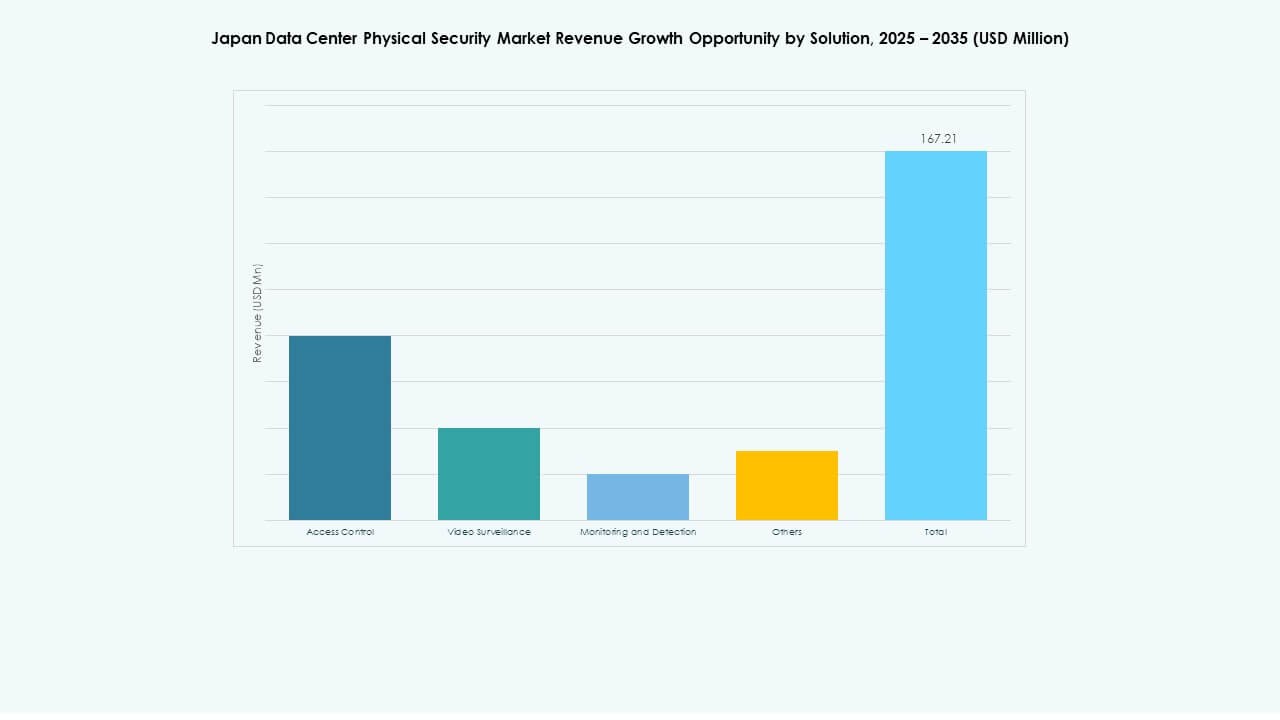

By Solution

Access control and video surveillance dominate the segment. These systems provide real-time verification and incident recording. The Japan Data Center Physical Security Market experiences rising demand for integrated detection platforms. Monitoring and detection tools help maintain operational continuity. Multi-factor authentication and smart ID management improve compliance. The “Others” category includes fire suppression and environmental safety modules. Access control holds the largest share due to regulatory reliance on identity verification.

By Services

System integration services lead this category. They ensure compatibility between hardware, analytics software, and cloud infrastructure. Consulting services help clients design compliance-ready frameworks. The Japan Data Center Physical Security Market gains value from predictive maintenance programs. Support services sustain uptime and equipment reliability. Service providers focusing on continuous upgrades retain strong customer bases. The expansion of co-location facilities further drives integration demand.

By Security Layer

Perimeter and building access layers dominate due to facility size and visitor flow. Data halls and racks also gain focus for protecting equipment from insider threats. The Japan Data Center Physical Security Market invests heavily in layered defense structures. Combining physical and digital verification ensures holistic safety. Perimeter security holds nearly 40% market share. Growing use of smart barriers and motion sensors reinforces protection at entry points.

By Data Center Type

Hyperscale data centers lead adoption due to heavy automation requirements. Colocation facilities follow with demand for flexible, shared infrastructure protection. The Japan Data Center Physical Security Market shows rising enterprise data center upgrades. Edge facilities expand rapidly to support low-latency applications. Hyperscale centers account for the majority of investments in advanced surveillance. Their strategic role in global network operations ensures consistent spending.

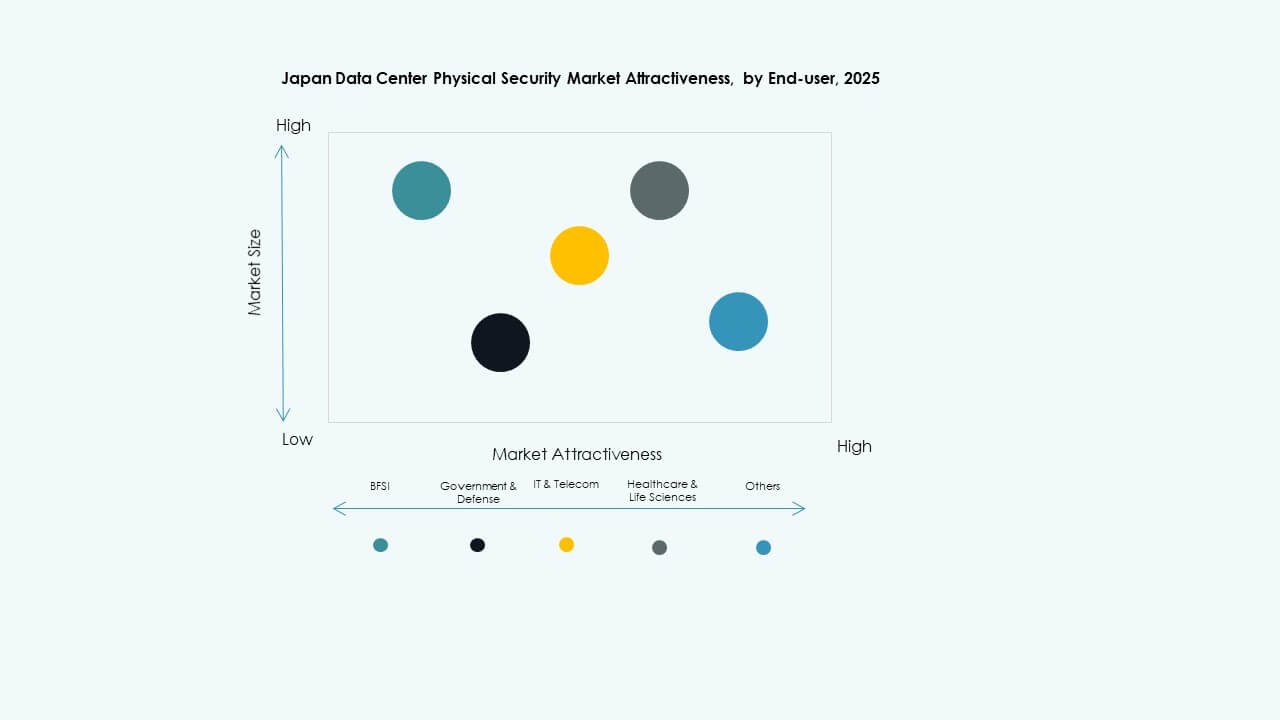

By End-user

IT and Telecom dominate end-user demand followed by BFSI and Government. These sectors require secure operations for data integrity and regulatory compliance. The Japan Data Center Physical Security Market gains momentum from cloud service expansion. Healthcare and manufacturing sectors invest in privacy-driven physical protection. Retail and e-commerce players strengthen warehouse and data logistics security. IT and Telecom hold nearly 35% share due to continuous cloud adoption.

Regional Insights

Tokyo and Kanto Region – The Core Hub

Tokyo and surrounding prefectures dominate with nearly 60% market share. The Japan Data Center Physical Security Market sees highest infrastructure density here. Demand stems from major cloud and telecom players operating hyperscale sites. Tokyo’s robust energy grid and connectivity attract continuous investment. It maintains strict security compliance frameworks and advanced infrastructure standards. Ongoing expansion of urban campuses reinforces dominance through high redundancy and automation levels.

- For example, NTT has demonstrated its All-Photonics Network (APN) technology under the IOWN initiative, achieving sub-millisecond data transmission between remote data centers. This innovation enables ultra-low latency and high-capacity communication, supporting next-generation data center connectivity in Japan.

Kansai Region – Expanding Secondary Cluster

Osaka and nearby cities hold around 25% market share. The Japan Data Center Physical Security Market grows rapidly due to data traffic redistribution. Kansai’s lower seismic risk and energy efficiency policies attract global investors. New colocation centers install high-resolution surveillance and multi-tier access control. Regional logistics networks enable fast response and system integration. The cluster strengthens its role as Japan’s second major digital hub.

Emerging Regions – Rising Edge and Green Zones

Hokkaido, Kyushu, and Okinawa regions represent about 15% share. The Japan Data Center Physical Security Market benefits from cool climates reducing energy costs. Operators build redundant facilities for disaster recovery and latency optimization. Local governments encourage expansion through land and tax incentives. These regions attract data-driven manufacturing and renewable energy projects. Edge computing developments and green initiatives make them attractive future markets.

- For example, the ESR and STACK consortium’s Keihanna Data Center campus in the Kansai area is an authentic example of emerging green data center zones. It is designed with a total capacity of 72 megawatts, and has received LEED Gold certification for sustainability and energy efficiency.

Competitive Insights:

- Bosch Sicherheitssysteme GmbH

- Honeywell International Inc.

- Johnson Controls

- Schneider Electric SE

- Siemens AG

- Cisco Systems, Inc.

- Axis Communications AB

- Dahua Technology Co. Ltd.

- Hanwha Vision Co. Ltd.

- Secom Co. Ltd.

The Japan Data Center Physical Security Market features intense competition led by multinational and domestic players offering integrated surveillance, access control, and automation systems. It shows strong vendor activity in AI analytics, biometric authentication, and IoT-enabled monitoring. Bosch, Honeywell, and Johnson Controls dominate enterprise-grade deployments, while Secom and Axis strengthen regional coverage. Schneider Electric and Siemens leverage infrastructure portfolios to deliver unified facility management solutions. Local partnerships and service customization define competitive differentiation. Global entrants expand through alliances with Japanese system integrators, focusing on compliance and low-latency support. Continuous product innovation and adherence to national security standards remain key to sustaining leadership.

Recent Developments:

- In October 2025, SAKURA Internet launched its “Manual Diagnosis Series” to enhance high-precision cybersecurity services for businesses in Japan and globally. This initiative aims to strengthen cybersecurity measures by providing manual diagnosis capabilities designed to detect vulnerabilities with greater accuracy.

- In October 2025, ASSA ABLOY acquired Kentix GmbH, a German company specializing in monitoring and access control products designed for data centers, enhancing their capabilities in physical security for this sector.

- In January 2025, ASSA ABLOY also acquired InVue, a Charlotte-based provider of asset protection and access control solutions, aligning with their strategy to expand globally in access control and asset protection.

- In June 2024, Honeywell International Inc. completed the acquisition of Carrier Global Corporation’s Global Access Solutions business for $4.95 billion, enhancing its building automation portfolio with advanced access control solutions like LenelS2, Onity, and Supra, which support security needs in data centers including those in Spain.

- In December 2024, Bosch Sicherheitssysteme GmbH sold its security and communications technology product business to the European investment firm Triton. The transaction included three business units Video, Access and Intrusion, and Communication as Bosch aims to focus more on systems integration business.