Executive summary:

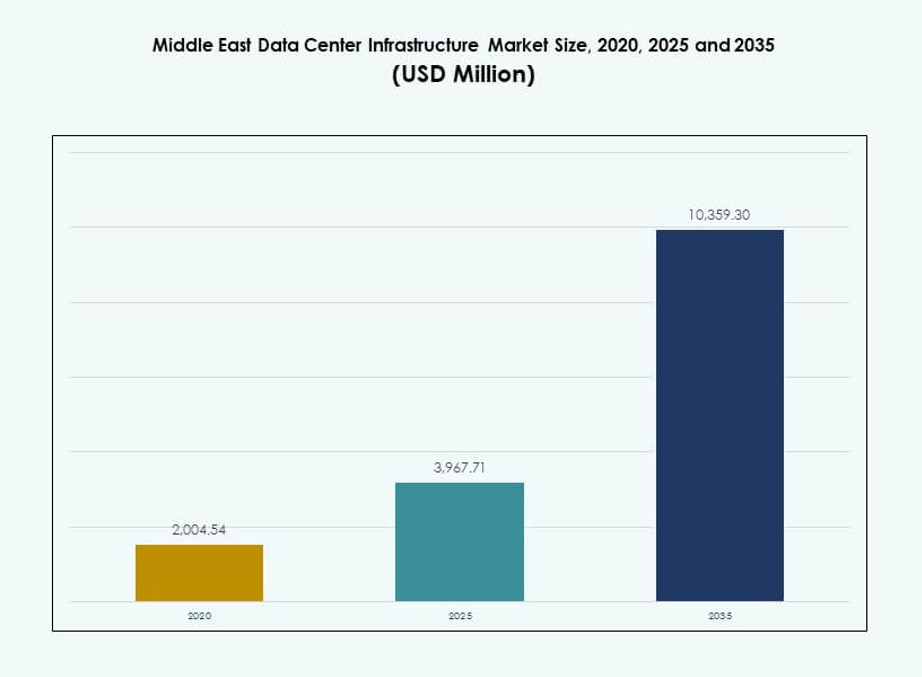

The Middle East Data Center Infrastructure Market size was valued at USD 2,004.54 million in 2020 to USD 3,967.71 million in 2025 and is anticipated to reach USD 10,359.30 million by 2035, at a CAGR of 10.00% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Middle East Data Center Infrastructure Market Size 2025 |

USD 3,967.71 Million |

| Middle East Data Center Infrastructure Market, CAGR |

10.00% |

| Middle East Data Center Infrastructure Market Size 2035 |

USD 10,359.30 Million |

The market is advancing due to rapid cloud adoption, edge computing growth, and rising AI and IoT integration. Businesses are shifting toward energy-efficient and modular infrastructure to support high-density computing. Innovations in liquid cooling, AI-ready systems, and smart power distribution are transforming facility design and operations. The region’s strategic location connecting Asia, Europe, and Africa enhances its appeal as a digital hub. Investors see strong potential in supporting hyperscale, colocation, and edge deployments to meet growing regional demand.

The UAE and Saudi Arabia lead infrastructure growth due to large-scale cloud investments and strong government support. These nations host major hyperscale and colocation developments supported by sovereign wealth and enterprise demand. Qatar, Kuwait, and Oman are emerging markets with national digital agendas and increasing foreign investment. Broader regional connectivity and enterprise digitalization continue to drive expansion across both leading and rising economies.

Market Dynamics:

Market Drivers

Accelerated Cloud Expansion and Hyperscale Investments Across Core Middle East Economies

Cloud service providers and hyperscale players are scaling infrastructure across the Middle East to meet enterprise demand. Countries like the UAE and Saudi Arabia continue to attract major data center investments due to pro-digital policies. Amazon Web Services, Microsoft, Google, and Oracle have all announced hyperscale developments. This has led to growing demand for power, cooling, and connectivity infrastructure. The Middle East Data Center Infrastructure Market benefits from this cloud-led momentum. Investments are shifting toward scalable, modular, and energy-efficient systems. Rising consumption of AI, IoT, and big data across industries intensifies the need for computing power. Government-supported economic diversification strategies position the region as a digital hub.

- For instance, AWS committed $5.3 billion for three availability zones in Saudi Arabia by 2026. This has led to growing demand for power, cooling, and connectivity infrastructure.

Growing AI, IoT, and Edge Computing Demands Are Reshaping Infrastructure Priorities

AI training workloads, machine learning models, and IoT networks are creating data growth at the edge. Real-time data analytics and latency-sensitive applications require distributed infrastructure and advanced hardware. Organizations across oil & gas, healthcare, and financial services adopt edge data centers to reduce latency. This shift is reshaping procurement in power distribution, rack designs, and liquid cooling. The Middle East Data Center Infrastructure Market aligns with this evolution, supporting next-gen computing capabilities. Data security, low-latency connectivity, and AI-ready systems are now core infrastructure priorities. Edge deployment models complement core and hyperscale setups. This infrastructure diversification presents new revenue streams for OEMs and engineering firms.

Public Sector Digitization and Smart Government Programs Driving Infrastructure Modernization

Public sector cloud-first strategies and smart city initiatives boost demand for secure and scalable data infrastructure. Governments in the Middle East invest heavily in e-governance, national AI plans, and connected services. These programs require high-availability facilities with robust power and thermal management systems. Saudi Arabia’s Vision 2030 and the UAE’s Digital Government Strategy lead infrastructure upgrades across ministries and public entities. The Middle East Data Center Infrastructure Market gains from this consistent public sector investment. Procurement focuses on Tier III and Tier IV reliability standards. Public-private partnerships foster infrastructure innovation, driving broader industry adoption. Government digital mandates act as long-term growth stabilizers for the market.

- For instance, Microsoft completed construction of three Azure availability zones in Saudi Arabia’s Eastern Province in December 2024. These zones are expected to become operational by 2026, supporting sovereign cloud and AI infrastructure.

Energy Efficiency and Sustainability Regulations Transforming Data Center Designs

New regional regulations on energy use, carbon emissions, and water consumption are changing data center engineering. Cooling systems are shifting to liquid-based and indirect evaporative technologies. Power architecture now includes smart UPS, high-efficiency PDUs, and renewable integration. Energy consumption metrics have become critical to win large public or private contracts. The Middle East Data Center Infrastructure Market responds with greener infrastructure designs. Operators aim to reduce power usage effectiveness (PUE) and carbon footprint. Companies adopt solar power and onsite energy storage for energy resilience. Data centers evolve into more sustainable, smart-grid-compatible facilities across major cities in the region.

Market Trends

Modular, Scalable, and Prefabricated Infrastructure Is Gaining Traction for Speed and Efficiency

Data center developers are shifting toward modular and prefabricated construction to reduce lead times and control project risks. These systems offer factory-built components that are deployed rapidly with minimal onsite work. Standardization improves quality and enables easy scalability. Design-build and turnkey EPC models increasingly integrate modular power and cooling blocks. The Middle East Data Center Infrastructure Market supports this trend as regional operators seek faster commissioning. High land costs and tight timelines for hyperscale projects drive modular adoption. Prefabricated systems also simplify compliance with Tier standards. Their flexibility fits colocation and enterprise requirements in urban and remote locations alike.

Rise of Liquid Cooling Systems in High-Density Data Centers Across the Region

With rising power densities and AI workloads, traditional air-based cooling is reaching its limits. Liquid cooling systems, including direct-to-chip and immersion cooling, are gaining adoption. Hyperscale and AI-focused facilities require thermal systems that reduce energy use and space footprint. Liquid systems provide better efficiency at scale. The Middle East Data Center Infrastructure Market supports this shift with rising procurement of advanced chillers and pumps. Data center operators target PUE improvements and reduced water consumption. Vendors now offer integrated solutions for hybrid cooling models. The move toward liquid-cooled racks is growing across new builds and retrofits in the Gulf region.

Fiber Connectivity Expansion and Carrier-Neutral Facilities Reshaping Network Infrastructure

The demand for high-speed, low-latency connectivity drives investment in fiber optic networks and IXPs across the Middle East. Carrier-neutral data centers offer enterprises flexibility and multi-cloud routing. Global and regional telecoms are expanding fiber backbones connecting Gulf cities to Africa, Europe, and Asia. This boosts demand for networking equipment, cabling, and optical fiber infrastructure. The Middle East Data Center Infrastructure Market benefits from these connectivity upgrades. Data centers are designed with high fiber port densities and scalable routing architectures. Network resilience and diverse paths are now key selection criteria. Improved interconnectivity supports hybrid and multi-cloud adoption across industries.

Increased Localization of Digital Infrastructure by Regional Sovereign Wealth and Private Equity Funds

Investment funds across the Middle East are actively building or acquiring data center assets to localize digital infrastructure. These entities aim to reduce reliance on foreign-hosted cloud while ensuring data sovereignty. Their investment supports end-to-end infrastructure deployment, including civil, mechanical, and electrical systems. Governments encourage domestic control over critical digital infrastructure. The Middle East Data Center Infrastructure Market grows as sovereign-backed operators scale their presence. Local manufacturing and EPC firms benefit from infrastructure localization mandates. Build-operate-transfer models are emerging in partnership with global cloud providers. These shifts make data centers a strategic investment class in regional capital markets.

Market Challenges

Power and Water Resource Constraints Impacting Scalability of Infrastructure Deployment

Data centers require consistent access to electricity and cooling water, yet utilities in some regions remain constrained. High temperatures and water scarcity in parts of the Middle East limit cooling options. Grid capacity shortages delay hyperscale site development. These factors challenge infrastructure scalability in emerging zones. The Middle East Data Center Infrastructure Market must innovate around these constraints. Liquid and hybrid cooling, battery energy storage, and onsite renewables become critical. Developers face higher OPEX due to resource inefficiencies. Energy cost volatility also affects long-term profitability for colocation and cloud providers in underdeveloped power zones.

Skilled Labor Gaps and Regulatory Complexities Slowing Project Timelines

Specialized talent is needed to design, engineer, and operate advanced data center infrastructure. The regional shortage of certified personnel delays integration of IT, power, and thermal systems. Local codes vary across countries, creating compliance complexity. Licensing, approvals, and land acquisition involve bureaucratic hurdles. These delays impact modular and greenfield project execution. The Middle East Data Center Infrastructure Market faces higher time-to-market for new capacity. Companies must invest in training, partnerships, and regulatory navigation. Talent development and streamlined regulations are essential to sustain infrastructure growth across the region.

Market Opportunities

Strategic Role of the Region as a Digital Hub Linking Europe, Asia, and Africa

The Middle East’s location positions it as a vital data transit and hosting hub. Global cloud providers and submarine cable operators view it as a bridge for east-west digital traffic. The Middle East Data Center Infrastructure Market can capitalize on this through network-focused investments. IXPs, carrier hotels, and landing stations drive infrastructure upgrades. Interconnection and hosting services gain traction, supported by strategic partnerships and sovereign funds.

Emerging Government Projects and Industrial Zones Driving Regional Data Center Demand

Smart cities, industrial zones, and special economic areas across the GCC and Levant regions plan large-scale data needs. Government and enterprise workloads require secure local hosting. The Middle East Data Center Infrastructure Market sees demand for modular, prefabricated systems in these developments. This opens opportunities for OEMs, EPC firms, and cloud integrators. Growth accelerates in second-tier cities with public sector funding.

Market Segmentation

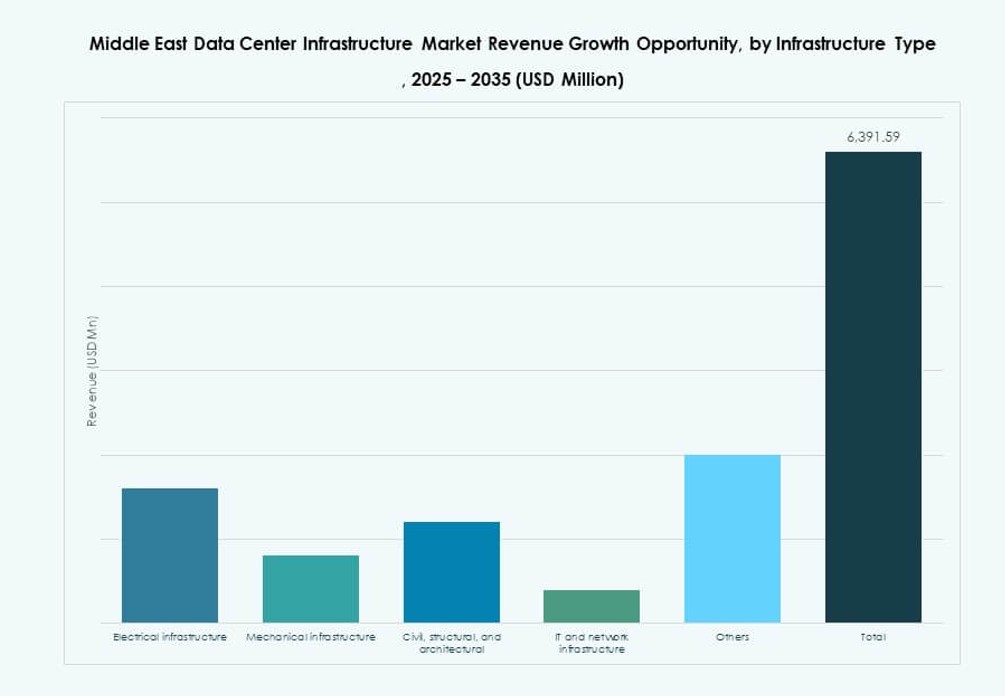

By Infrastructure Type

Electrical infrastructure dominates the Middle East Data Center Infrastructure Market due to the region’s high focus on power reliability and uptime. Advanced UPS systems, PDUs, and switchgears form the backbone of uninterrupted operations. Mechanical infrastructure is expanding, especially in facilities designed for AI and HPC workloads needing efficient thermal management. IT & network infrastructure continues to grow due to rising demand for servers, optical cabling, and high-speed networking. Civil and architectural elements are evolving with prefabricated building systems and modular rooms gaining share. Each infrastructure segment plays a vital role in regional capacity expansion.

By Electrical Infrastructure

UPS systems and battery energy storage solutions represent a major share of electrical infrastructure spending. Frequent grid fluctuations and rising rack densities increase reliance on scalable backup systems. PDUs and smart switchgears enable real-time power monitoring and redundancy. The Middle East Data Center Infrastructure Market also sees growing utility investments in grid connections near hyperscale zones. Lithium-ion battery systems are replacing legacy lead-acid units. Operators integrate AI-enabled energy management platforms with electrical systems. Power quality, redundancy, and sustainability are central procurement factors across this segment.

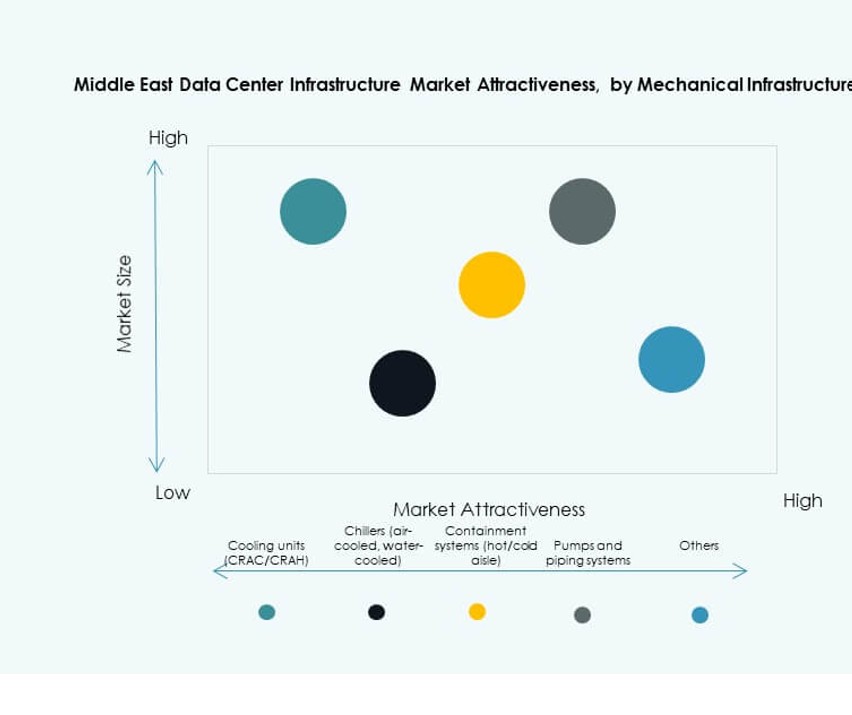

By Mechanical Infrastructure

Cooling units, including CRAH and CRAC systems, remain critical components, especially in the Gulf’s extreme climate. Advanced containment solutions and chilled water systems dominate new builds. Indirect evaporative systems gain traction due to water efficiency. Pumps, piping, and modular cooling plants are now designed for AI-ready facilities. The Middle East Data Center Infrastructure Market aligns with global cooling innovation trends. Data centers seek to balance PUE reduction with long-term OPEX savings. Mechanical systems are evolving for scalability and energy optimization.

By Civil / Structural & Architectural

Site preparation and modular superstructure components are gaining traction for speed and standardization. Raised floors, steel-frame systems, and suspended ceilings allow for flexible layouts. Energy-efficient cladding and roof designs improve thermal control. The Middle East Data Center Infrastructure Market sees strong demand for modular construction systems due to tight project timelines. Civil infrastructure planning now includes seismic, flood, and fire resilience features. EPC firms integrate smart building management into architectural components.

By IT & Network Infrastructure

Networking equipment, fiber optic cabling, and server racks dominate IT infrastructure demand. The growth of multi-cloud environments drives advanced routing and switching deployments. Optical cabling enables high-speed data transmission across floors and zones. The Middle East Data Center Infrastructure Market expands with hyperscale and enterprise server deployments. Server and storage configurations evolve to support AI and real-time workloads. IT infrastructure purchasing is now aligned with workload types and software architecture. Network resilience and low-latency routing remain core priorities.

By Data Center Type

Hyperscale data centers lead the market share, backed by global cloud giants building regional hubs. Colocation facilities also see strong growth due to rising enterprise outsourcing. Edge data centers gain relevance in remote zones with latency-sensitive applications. The Middle East Data Center Infrastructure Market benefits from this mix of deployment models. Enterprise-owned data centers decline as managed services grow. AI and IoT use cases further drive edge data center construction.

By Delivery Model

Turnkey and design-build EPC models dominate project delivery in the region. Modular factory-built systems are rising in share due to fast deployment and scalability. Retrofit and upgrade models are common in older facilities undergoing AI and cloud transitions. The Middle East Data Center Infrastructure Market increasingly favors EPC models that integrate electrical, mechanical, and IT scopes. Delivery model choice depends on operator size, workload requirements, and location.

By Tier Type

Tier III and Tier IV facilities hold the majority share due to enterprise and public sector demand for uptime. Tier I and II are limited to non-critical or edge deployments. The Middle East Data Center Infrastructure Market aligns with global uptime expectations, especially from BFSI and government customers. Tier-certified designs support risk mitigation and business continuity. Redundancy and fault tolerance drive investments in advanced tier architecture.

Regional Insights

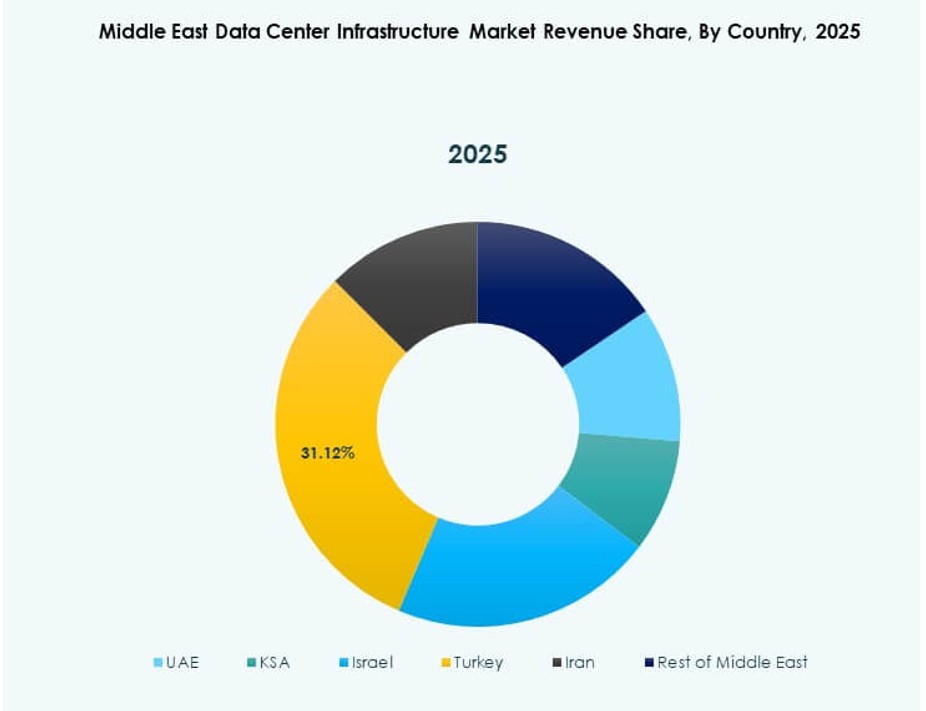

Gulf Cooperation Council (GCC) Dominates with Over 75% Share Backed by Saudi Arabia and UAE

Saudi Arabia and the UAE are leading the region’s data center infrastructure growth due to massive government investments and hyperscale developments. These countries account for over 75% of the Middle East Data Center Infrastructure Market. The UAE remains an innovation leader, while Saudi Arabia focuses on large-scale Vision 2030 projects. Dubai, Riyadh, and Abu Dhabi host major colocation and cloud campuses. Government mandates, smart city programs, and enterprise cloud adoption drive GCC expansion.

Emerging Growth in Qatar, Kuwait, and Bahrain Supported by Telecom and Cloud Projects

Qatar and Kuwait are investing in digital transformation and cloud localization, creating strong demand for data center infrastructure. Bahrain is positioning itself as a fintech and digital services hub. These countries represent the next wave of infrastructure expansion in the Middle East Data Center Infrastructure Market. Telecom companies and sovereign funds play active roles in building local capacity. Project pipelines include new colocation sites, modular deployments, and government data hubs.

- For instance, STC Bahrain and center3 announced major progress on a $320 million ICT project including Bahrain Data Center Park in November 2025.

Levant and Other Non-GCC Countries Showing Early Stage Development Momentum

Countries such as Jordan, Egypt, and Iraq are witnessing early investments in digital infrastructure. These markets remain small but show strong long-term potential. Education, healthcare, and banking sectors lead demand for secure hosting. Government digitalization and improved power access support infrastructure development. The Middle East Data Center Infrastructure Market sees emerging opportunities in these areas, especially for modular and edge data center models.

- For instance, Equinix launched DX3 data center in Dubai with initial capacity for 900 racks across 135,000 square feet, part of over $60 million investment, though serving broader MENA access.

Competitive Insights:

- Khazna Data Centers

- Gulf Data Hub

- Moro Hub

- Center3 (stc)

- Equinix, Inc.

- Huawei Technologies Co., Ltd.

- Schneider Electric

- Vertiv Group Corp.

- Dell Inc.

- Cisco Systems, Inc.

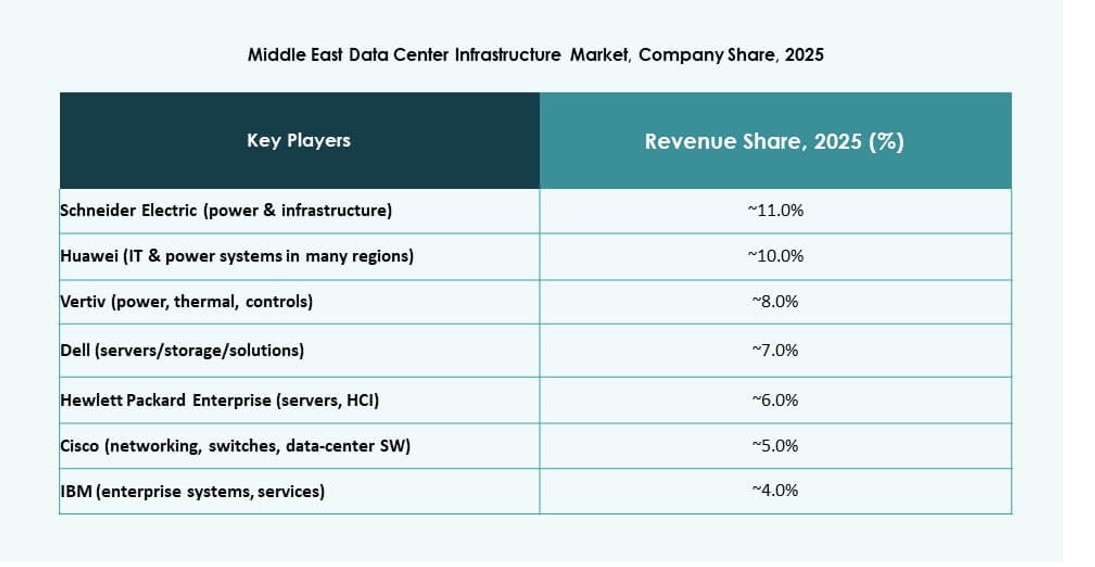

The Middle East Data Center Infrastructure Market features a mix of global OEMs, regional colocation operators, and vertically integrated cloud infrastructure players. Local firms like Khazna, Center3, and Gulf Data Hub lead hyperscale and colocation expansion with government and enterprise backing. Global leaders such as Schneider Electric, Huawei, and Vertiv provide advanced power and cooling systems to support high-density deployments. IT infrastructure vendors like Dell and Cisco support compute, storage, and networking layers. Market competition intensifies due to sovereign digital transformation programs and foreign direct investment. Players focus on energy efficiency, modular construction, and Tier III–IV certified builds. Strategic partnerships, EPC alliances, and AI-ready infrastructure offerings shape differentiation across segments. The market favors firms offering end-to-end capabilities from design to operation.

Recent Developments:

- In December 2025, Khazna Data Centers acquired a 225,000-square-metre land parcel in Dammam, Saudi Arabia, to develop up to 200 MW of AI-ready data centre capacity, marking its first facility in the Kingdom.

- In November 2025, KKR partnered with Gulf Data Hub for a $5 billion investment to expand data infrastructure across the Gulf, including acquiring a significant stake pending approvals.