Executive summary:

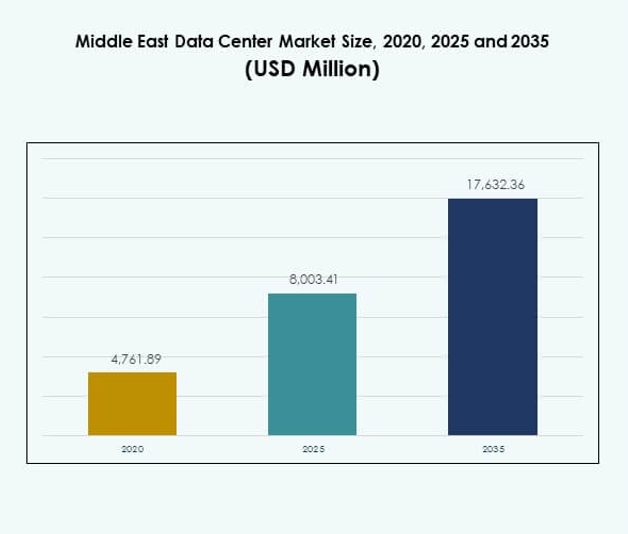

The Middle East Data Center Market size was valued at USD 4,761.89 million in 2020 to USD 8,003.41 million in 2025 and is anticipated to reach USD 17,632.36 million by 2035, at a CAGR of 8.17% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Middle East Data Center Market Size 2025 |

USD 8,003.41 Million |

| Middle East Data Center Market, CAGR |

8.17% |

| Middle East Data Center Market Size 2035 |

USD 17,632.36 Million |

Growth is fueled by increasing cloud adoption, rising demand for digital infrastructure, and strong investment in hyperscale facilities. Enterprises and governments integrate AI, IoT, and big data platforms that require scalable, secure, and energy-efficient data centers. Innovation in automation, modular solutions, and renewable integration strengthens competitiveness. The market is strategically important for global providers and investors seeking to build digital ecosystems that support economic diversification and long-term technological resilience.

The UAE and Saudi Arabia lead the market due to large-scale digital transformation programs and smart city initiatives. Qatar and Israel emerge as growing hubs with strong investment in connectivity and financial services infrastructure. Turkey strengthens its role as a regional bridge between Europe and Asia, while smaller economies expand modular and edge deployments to improve competitiveness. These dynamics highlight the diverse regional landscape shaping the Middle East Data Center Market.

Market Drivers

Adoption Of Cloud Platforms And Growth Of Digital Transformation

The Middle East Data Center Market benefits from rapid cloud adoption and strong digital transformation programs. Governments across the region are investing in smart cities, digital economies, and e-government services. Businesses seek scalable infrastructure that supports real-time applications, data analytics, and cross-border services. Enterprises use hybrid and multi-cloud strategies to ensure flexibility and resilience. It supports AI and IoT platforms that demand high storage and compute capacity. Telecom operators expand networks to strengthen connectivity. Investors view data centers as critical to enabling innovation. Strategic importance continues to rise with expanding workloads.

Innovation In Energy Efficiency And Focus On Green Infrastructure

Sustainability drives investment decisions with operators focusing on renewable integration and efficient cooling systems. The Middle East Data Center Market prioritizes energy-saving technologies like liquid cooling, modular UPS, and AI-based power management. Green certifications enhance operator reputation and attract global clients. Solar energy deployment increases in the UAE and Saudi Arabia, reducing dependence on traditional energy. It ensures cost optimization while aligning with national decarbonization targets. Operators see sustainable practices as differentiators in a competitive market. Energy efficiency becomes a core factor for long-term competitiveness. Businesses adopt these practices to strengthen ESG positioning.

- For instance, in October 2022, Khazna Data Centers partnered with Emerge, a joint venture between Masdar and EDF, to develop a ground-mounted solar PV plant with an installed capacity of 7 megawatts peak (MWp) to power the Khazna AUH6 facility in Masdar City, Abu Dhabi, supporting sustainable operations and contributing to the UAE’s renewable energy goals.

Rise Of Hyperscale Facilities And Investment By Global Players

Global hyperscale providers expand aggressively to serve rising regional demand. The Middle East Data Center Market attracts Amazon Web Services, Microsoft Azure, Google Cloud, and Oracle, each building cloud regions. Local telecom operators collaborate with international firms to establish joint ventures. Hyperscale facilities support growing AI workloads, blockchain, and edge computing. It enables businesses to reduce latency and improve data sovereignty. Governments encourage foreign direct investment in digital infrastructure. This creates opportunities for technology transfer and local job creation. Investors benefit from stable long-term returns through expanding hyperscale deployments.

- For instance, as of September 2025, Amazon Web Services (AWS) has expanded its global infrastructure to 120 Availability Zones within 38 geographic regions including major new zones in the Middle East allowing customers to run latency-sensitive workloads close to end users and support high-availability enterprise cloud deployments across the region.

Strategic Role In Regional Connectivity And Global Trade Routes

Geographic location strengthens the market’s strategic value as the Middle East links Asia, Europe, and Africa. Submarine cable projects, such as 2Africa and PEACE, improve international connectivity. The Middle East Data Center Market benefits from low-latency access that supports financial services and digital commerce. Regional hubs like UAE and Qatar become gateways for global data traffic. It provides a secure backbone for multinational firms expanding in the region. Strong investment in 5G accelerates demand for edge facilities. Enterprises gain efficiency by hosting data closer to users. The market plays a pivotal role in global digital trade.

Market Trends

Shift Toward Modular And Edge Data Center Deployments

The Middle East Data Center Market witnesses growing demand for modular and edge deployments. Enterprises and telecom providers build edge facilities to support 5G, IoT, and smart city use cases. Modular solutions allow faster installation and scalability, which attracts small enterprises and regional operators. It ensures agility in meeting fluctuating demands. Edge centers reduce latency for streaming, gaming, and industrial automation. Global firms collaborate with local partners to roll out modular technologies. The trend aligns with government-backed digital infrastructure projects. This accelerates adoption across both developed and emerging subregions.

Integration Of Artificial Intelligence And Advanced Automation

Automation is transforming operations with AI-powered monitoring, predictive maintenance, and autonomous management systems. The Middle East Data Center Market sees providers deploying AI for power optimization, cooling management, and workload balancing. Enterprises use automation tools to ensure compliance and improve efficiency. It reduces downtime and operational risks while enhancing scalability. Vendors offer AI-driven orchestration platforms to simplify multi-cloud environments. This strengthens the role of advanced technologies in improving competitiveness. Innovation in robotic automation also supports routine maintenance. The integration trend builds a pathway toward next-generation smart facilities.

Expansion Of Regional Colocation And Interconnection Services

Demand for colocation rises sharply as enterprises prefer flexible models over large capital expenditure. The Middle East Data Center Market records strong uptake from SMEs, fintechs, and digital-native firms. Colocation providers expand interconnection hubs that connect enterprises with telecom, cloud, and content providers. It improves service delivery and enhances ecosystem efficiency. Neutral colocation centers become attractive for global firms seeking secure and scalable infrastructure. Growth of managed services also supports colocation expansion. Regional governments back colocation to encourage SME participation in digital ecosystems. This trend sustains long-term infrastructure growth.

Adoption Of High-Density Racks And Next-Generation Networking

High-density infrastructure is gaining prominence to meet demand for AI, big data, and GPU-driven workloads. The Middle East Data Center Market invests in racks supporting more than 15 kW, strengthening capacity utilization. Next-generation networking solutions like 400G and optical interconnects are widely adopted. It supports faster traffic flow and enhanced reliability for mission-critical applications. Enterprises adopt SDN and NFV technologies for flexible networking. Vendors promote products that reduce latency and improve security. Operators integrate automation with networking to simplify large deployments. High-density systems become essential in sustaining competitive advantages.

Market Challenges

High Energy Consumption And Cooling Limitations In Harsh Climates

The Middle East Data Center Market faces major hurdles from high power use and cooling constraints. Harsh desert conditions increase costs for HVAC and liquid cooling systems. It puts pressure on operators to balance energy efficiency and operational reliability. Dependence on water-based cooling raises sustainability issues in arid regions. Limited availability of renewable power in some subregions restricts adoption of green practices. Rising demand for capacity increases overall energy strain. Governments enforce stricter efficiency regulations, adding compliance costs. Operators face difficulty in aligning profit targets with energy efficiency goals.

Data Sovereignty, Cybersecurity, And Skilled Workforce Gaps

Another challenge involves compliance with complex data sovereignty and cybersecurity frameworks. The Middle East Data Center Market must adhere to strict local hosting rules in UAE, Saudi Arabia, and Qatar. It requires continuous investment in advanced security tools and threat monitoring. Regional operators face increasing cyberattack risks, which threaten trust and resilience. Limited availability of skilled professionals delays large-scale digital projects. Talent gaps in AI, cloud management, and cybersecurity affect scalability. Geopolitical risks further complicate data governance. Businesses invest in training but shortages continue to slow sector-wide growth.

Market Opportunities

Rising Government Support And Strategic Investments In Digital Infrastructure

The Middle East Data Center Market gains opportunities from government-backed digital strategies and foreign direct investment. Smart city projects, fintech expansion, and healthcare digitization create strong demand. It benefits from rising partnerships between global cloud providers and local telecom operators. AI-driven applications and IoT platforms strengthen growth prospects. Enterprises look for regional hosting to comply with data sovereignty laws. Investments in submarine cables further enhance global connectivity. The ecosystem presents attractive opportunities for private equity and infrastructure investors.

Growth Potential In Edge Computing And Sector-Specific Deployments

Emerging industries such as e-commerce, media, and manufacturing accelerate demand for edge facilities. The Middle East Data Center Market expands opportunities in modular deployments serving specific industry clusters. It enables low-latency services for fintech, healthcare, and retail applications. Edge nodes improve operational efficiency and customer experience. Telecom operators gain new revenue streams through hosting edge workloads. Enterprises explore hybrid strategies combining colocation, cloud, and edge. Future growth lies in expanding use cases that integrate 5G, AI, and IoT.

Market Segmentation

By Component

Hardware dominates the Middle East Data Center Market due to demand for servers, storage, and networking systems. Operators invest in advanced power and cooling technologies to ensure uptime in extreme conditions. Security systems gain traction as cyber risks increase. Software, particularly DCIM and virtualization, supports automation and efficient management. Services such as integration and managed support expand as enterprises outsource operations. The combined demand strengthens the ecosystem with hardware holding the largest revenue share.

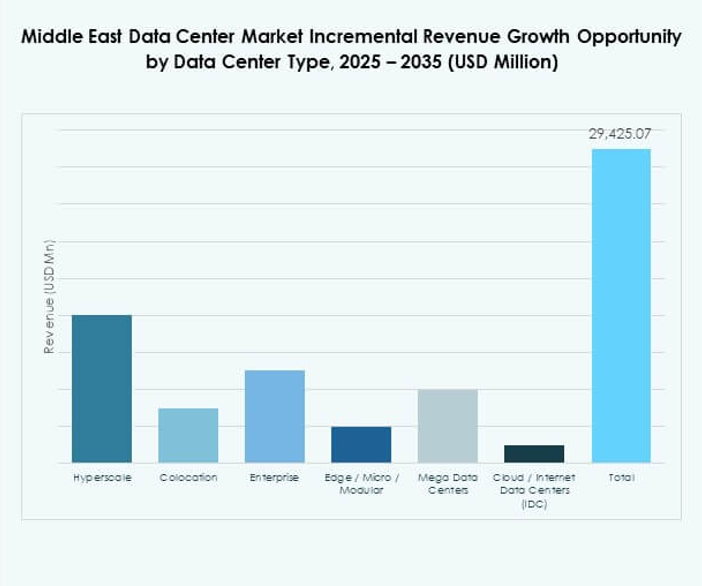

By Data Center Type

Hyperscale facilities lead the Middle East Data Center Market with strong investments from global cloud providers. These centers handle large AI and big data workloads. Colocation grows rapidly as SMEs seek cost-effective solutions. Edge and modular centers expand with the rollout of 5G and smart cities. Enterprise data centers maintain relevance in banking and defense sectors. Mega facilities emerge in Saudi Arabia and UAE, backed by sovereign wealth funds. Cloud-based internet data centers grow with rising regional e-commerce.

By Deployment Model

Cloud-based models dominate the Middle East Data Center Market as enterprises migrate critical workloads. On-premises deployments remain important for sensitive government and defense applications. Hybrid models gain traction as firms balance security with flexibility. It provides resilience while meeting compliance requirements. Enterprises deploy cloud-native apps that demand scalable resources. Cloud-first strategies gain support from policymakers. Hybrid deployments create long-term value by supporting multi-cloud strategies. Growth is concentrated in telecom, BFSI, and healthcare sectors.

By Enterprise Size

Large enterprises hold the leading share in the Middle East Data Center Market. They require high-capacity infrastructure to handle complex applications across BFSI, telecom, and manufacturing. SMEs increase adoption through colocation and cloud-based services. It ensures cost savings and reduces capital expenditure. Governments encourage SME participation through digital transformation programs. Hybrid and modular solutions allow SMEs to expand as needed. Large enterprises drive overall market demand, while SMEs sustain growth through flexible models.

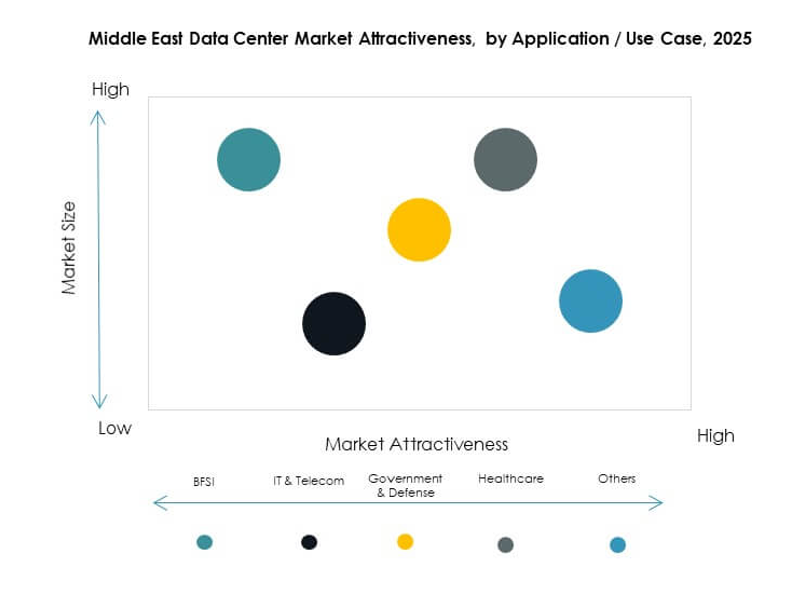

By Application / Use Case

BFSI leads the Middle East Data Center Market due to heavy reliance on secure and compliant infrastructure. IT and telecom follow with large-scale investments in 5G, IoT, and AI platforms. Healthcare accelerates demand for real-time data and patient record management. Retail and e-commerce grow with rising online shopping activity. Media and entertainment require low-latency streaming and gaming solutions. Manufacturing and energy sectors adopt smart systems needing high data throughput. Government and defense maintain sensitive applications with strong demand for local hosting.

By End User Industry

Cloud service providers dominate the Middle East Data Center Market, supported by hyperscale investments. Enterprises expand adoption for hybrid and multi-cloud strategies. Colocation providers strengthen regional interconnection hubs. Government agencies demand localized hosting for compliance and security. It ensures diversified growth across industries. The balance between global providers and local enterprises creates a dynamic ecosystem. Cloud and colocation lead expansion, while government projects strengthen domestic demand.

Regional Insights

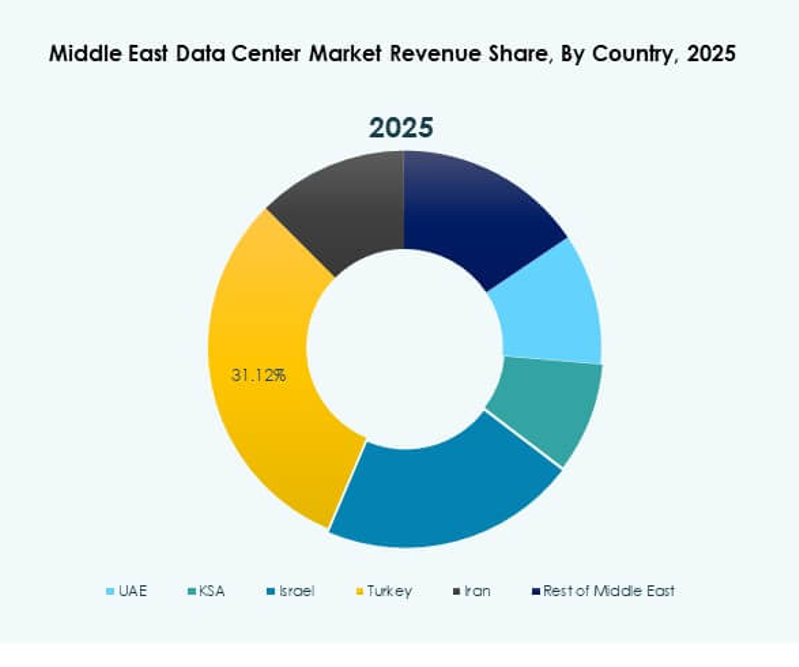

Gulf Cooperation Council (GCC) Leading Regional Market

The GCC holds 58% share of the Middle East Data Center Market, led by UAE and Saudi Arabia. Both nations invest heavily in hyperscale facilities and digital transformation programs. It supports smart cities, e-government projects, and financial services. Strong submarine cable networks enhance their role as connectivity hubs. Sovereign wealth funds provide capital for mega projects. Businesses gain access to advanced infrastructure, strengthening competitiveness and regional leadership.

- For instance, in February 2024, Khazna Data Centers launched the AUH6 data center in Abu Dhabi with a verified IT power capacity of 31.8 MW and modular design architecture. Khazna further secured $2.62 billion in financing in September 2025 from ADCB and First Abu Dhabi Bank to expand hyperscale digital infrastructure across the UAE, maintaining a 73% market share in the country.

Levant Region Developing With Growing Investment In Telecom And Cloud

The Levant region accounts for 24% share of the Middle East Data Center Market. Countries like Jordan and Lebanon expand telecom infrastructure and promote cloud adoption. It supports startups and financial services seeking digital resilience. Investments flow into modular and colocation centers. Regional governments introduce policies to attract private investors. Growth is steady but limited by geopolitical instability. The Levant continues to evolve into a growing contributor.

North Africa Emerging With Rising Demand For Localized Hosting

North Africa secures 18% share of the Middle East Data Center Market. Egypt leads the subregion with strong government-backed IT programs. It attracts hyperscale and colocation providers serving both domestic and cross-border markets. Morocco and Tunisia expand data centers to support e-commerce and fintech. It gains strategic importance due to its proximity to Europe and sub-Saharan Africa. Regional players focus on localized hosting and energy-efficient facilities. North Africa emerges as a growth-oriented subregion with strong potential.

- For instance, in September 2025, Telecom Egypt approved the sale of its Cairo Regional Data Hub (RDH) data center campus to Helios Investment for $230 million. The RDH campus provides a designed IT load of 2.5 MW in its first phase and can host up to 4,000 racks, delivering major connectivity to international submarine cables and serving as a strategic regional hub.

Competitive Insights:

- Etisalat

- Equinix Middle East

- MedOne

- Equinix, Inc.

- Digital Realty Trust, Inc.

- NTT Communications Corporation

- Microsoft Corporation

- Amazon Web Services, Inc.

- Google LLC (Alphabet Inc.)

The Middle East Data Center Market features intense competition driven by global hyperscale providers and strong regional operators. It benefits from substantial investments by Microsoft, Amazon Web Services, and Google, which expand cloud regions and enhance digital capacity. Equinix and Digital Realty strengthen their colocation presence, while NTT focuses on managed services and international connectivity. Regional firms such as Etisalat and MedOne play a crucial role in addressing local hosting needs and compliance requirements. The competitive environment is shaped by partnerships, green initiatives, and advanced technologies like liquid cooling and AI-driven automation. It supports enterprises and governments seeking secure, scalable, and sustainable infrastructure, creating opportunities for both global leaders and local players to reinforce their market position.

Recent Developments:

- In July 2025, Ooredoo Qatar unveiled a new AI cloud platform, powered by Nvidia Hopper GPUs and hosted by its data center division, Syntys. This move is designed to accelerate scalable and secure AI infrastructure deployment in Qatar, providing businesses with access to Nvidia’s AI Enterprise suite and supporting the country’s innovation and digital transformation goals.

- In Q1 2025, G42 Holdings acquired the 40% stake held by e& in Khazna Data Center for $2.2 billion. This acquisition made G42 the majority shareholder and expanded its data center footprint in the United Arab Emirates, signaling a major investment in the region’s digital infrastructure. The transaction aligns with the UAE’s government-backed visions for economic diversification and technology leadership.

- In May 2025, Qualcomm partnered with HUMAIN, a Saudi company backed by the country’s Public Investment Fund (PIF), through a memorandum of understanding aiming to deliver advanced AI data centers and develop the local semiconductor ecosystem. The collaboration will foster cloud and edge deployments and nurture engineering talent within the Kingdom.

- In April 2025, Digital Realty Trust, Inc. unveiled its first data center in Crete, Greece, enhancing connectivity throughout the Eastern Mediterranean and supporting Middle East data flows.