Executive summary:

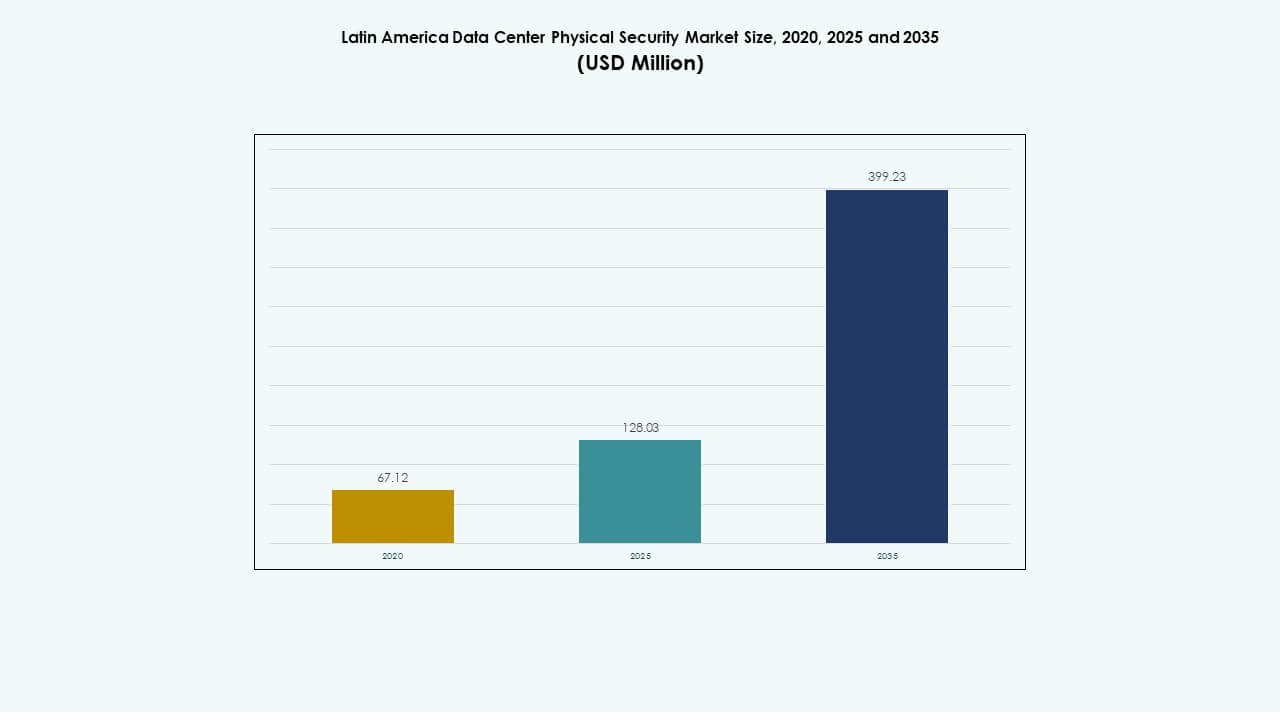

The Latin America Data Center Physical Security Market size was valued at USD 67.12 million in 2020 to USD 128.03 million in 2025 and is anticipated to reach USD 399.23 million by 2035, at a CAGR of 11.99% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Latin America Data Center Physical Security Market Size 2025 |

USD 128.03 Million |

| Latin America Data Center Physical Security Market, CAGR |

11.99% |

| Latin America Data Center Physical Security Market Size 2035 |

USD 399.23 Million |

Market expansion is driven by the rapid development of hyperscale and colocation data centers, increased demand for AI-integrated surveillance systems, and stricter data compliance frameworks. Businesses are prioritizing investments in smart monitoring, biometric access, and automated threat detection systems to ensure resilience. For investors, the market holds strong strategic importance as digital infrastructure and cloud adoption continue to grow across Latin America.

Brazil leads the Latin America Data Center Physical Security Market with extensive hyperscale investments and digital transformation projects. Chile and Mexico are emerging as secondary hubs supported by reliable energy networks and favorable regulations. Colombia and Argentina are attracting new developments with government-backed digital initiatives and growing colocation activity.

Market Drivers

Market Drivers

Expansion of Hyperscale and Colocation Facilities

The Latin America Data Center Physical Security Market benefits from rapid expansion in hyperscale and colocation facilities. Growing cloud adoption and increased enterprise data traffic are driving construction across major cities. Companies such as Equinix, Ascenty, and Scala Data Centers are investing heavily in infrastructure. The need for higher resilience against physical threats has led to advanced access control and AI-driven monitoring adoption. Integration of biometric authentication and perimeter intrusion detection has become standard. Governments emphasize digital sovereignty, increasing investment in secure facilities. The growing reliance on cloud and colocation services fuels the demand for robust protection. Investors see this trend as a sign of long-term regional growth stability.

- For instance, Ascenty recently announced construction of five new data center facilities across Brazil, Chile and Mexico under a major USD 925 million credit facility.

Adoption of AI and IoT-Enabled Security Systems

AI and IoT integration play a major role in strengthening physical protection. Modern data centers now deploy interconnected sensors, cameras, and smart devices to monitor movement and predict security breaches. Machine learning algorithms identify abnormal activities faster than human intervention. In the Latin America Data Center Physical Security Market, such technologies reduce operational risks while enhancing compliance. IoT-based perimeter systems improve detection accuracy and lower false alarms. Vendors like Honeywell and Bosch expand their regional offerings with predictive security analytics. Cloud-based management tools give operators real-time insights into system performance. These developments help businesses maintain 24/7 uptime and secure critical assets. Investors value this transition for its operational efficiency and lower total cost of ownership.

Regulatory Push for Data Sovereignty and Compliance

Regional governments enforce data sovereignty regulations that demand higher protection levels. Laws in Brazil, Mexico, and Chile promote local data processing with strict privacy and physical safety standards. Data center operators respond by upgrading facility access and surveillance infrastructure. In the Latin America Data Center Physical Security Market, compliance is both a necessity and a competitive advantage. Certification under ISO 27001 and Tier IV standards has become vital for credibility. This regulatory push attracts global cloud providers aiming to meet governance benchmarks. National cybersecurity frameworks are strengthening, supporting regional digital transformation. For investors, compliant infrastructure signals maturity and risk mitigation, enhancing market attractiveness.

Shift Toward Energy-Efficient and Integrated Security Designs

Operators are integrating sustainability with security, aligning energy-efficient designs and smart systems. Physical protection now complements low-power surveillance and intelligent lighting networks. In the Latin America Data Center Physical Security Market, integration of renewable-powered monitoring systems supports green infrastructure targets. Data centers deploy modular architecture that simplifies sensor management. Combining automation and security ensures minimal downtime and optimized resource use. Green-certified facilities with smart monitoring gain preference among enterprises. Advanced building management systems (BMS) link physical access with energy use tracking. This shift creates long-term benefits for both operational safety and environmental goals, drawing new capital investments.

- For instance, in Buenos Aires, major operators are implementing modular security solutions that include multi-point video surveillance and perimeter intrusion detection compliant with local regulations.

Market Trends

Market Trends

Integration of Smart Video Analytics and Facial Recognition

The adoption of smart video analytics marks a key transformation. Data centers employ AI-powered systems for real-time threat assessment and facial verification. In the Latin America Data Center Physical Security Market, the shift reduces manual oversight and improves response accuracy. Facial recognition supports faster employee identification while preventing unauthorized entry. Continuous monitoring through cloud-based analytics enhances transparency and audit capabilities. Real-time alerts integrate with mobile control applications, empowering remote facility management. Vendors are introducing adaptive software that learns from recurring incidents. This trend increases system intelligence and improves threat anticipation across large campuses.

Rise of Cloud-Native Security Infrastructure

Cloud-native management platforms are redefining how physical systems are maintained. Operators now control multi-site access, video, and alarm systems through centralized dashboards. In the Latin America Data Center Physical Security Market, cloud-managed platforms ensure scalability and simplified operations. They allow predictive maintenance by analyzing equipment performance data. Subscription-based services reduce upfront hardware costs and improve flexibility. Companies embrace hybrid models combining on-premises sensors with cloud analytics. These innovations enable faster incident detection and unified policy enforcement. The rise of service-based security models aligns with digital transformation goals.

Growing Focus on Edge Data Centers and Micro-Security Solutions

Edge computing drives a new trend toward distributed facility protection. Smaller, localized data centers require compact, automated, and energy-efficient security systems. In the Latin America Data Center Physical Security Market, edge facilities deploy modular camera networks and biometric locks. The trend reflects the growing demand for low-latency applications like AI and IoT analytics. Vendors design scalable products adaptable to diverse climates and infrastructures. Micro-data centers integrate smart lighting, motion sensors, and intrusion alarms in compact form. Businesses prefer remote management tools that link multiple edge nodes securely. This focus enhances operational continuity in underserved or remote regions.

Partnerships Between Tech Vendors and Local Integrators

Collaborations between international vendors and local security providers shape the competitive landscape. Global firms supply advanced technologies while regional integrators handle compliance and installation. In the Latin America Data Center Physical Security Market, these partnerships ensure localization and faster deployment. Joint ventures enhance market access in regulated sectors like finance and healthcare. Training programs upskill local technicians in advanced security systems. Vendors adapt to local climate and power conditions to improve reliability. These alliances strengthen customer trust and enable tailored service models. The trend supports knowledge transfer and creates long-term economic value.

Market Challenges

High Installation Costs and Infrastructure Limitations

High upfront costs remain a significant barrier across Latin America. Deploying advanced biometric and surveillance systems requires expensive equipment and integration expertise. The Latin America Data Center Physical Security Market faces limitations due to outdated infrastructure in several regions. Power instability and limited fiber connectivity raise operational risks. Smaller operators hesitate to invest in top-tier protection due to cost constraints. Import taxes and complex logistics raise equipment pricing, delaying deployments. Many facilities still depend on legacy analog systems with minimal automation. Vendors must balance affordability with technological innovation to achieve broader adoption.

Skilled Workforce Shortage and Regulatory Gaps

Lack of trained personnel in security technology slows progress. The Latin America Data Center Physical Security Market requires expertise in AI analytics, sensor integration, and compliance management. However, skilled engineers and certified technicians remain limited. Rapid policy changes create uncertainty for investors and slow project execution. Differences in safety standards across countries complicate regional alignment. Smaller nations lack clear frameworks for critical infrastructure protection. This regulatory inconsistency creates uneven adoption across markets. Continuous training and harmonized standards are essential to ensure sustainable market growth.

Market Opportunities

Rising Cloud and AI Infrastructure Investments

The region experiences strong investment from global cloud and telecom operators. Companies such as AWS, Microsoft, and Google expand their footprints across major economies. The Latin America Data Center Physical Security Market benefits from parallel investments in physical protection. AI-enabled surveillance and biometric access technologies are gaining traction. These projects open opportunities for local manufacturers and integrators. Vendors offering smart and scalable systems can achieve significant contract growth. Governments promoting digital infrastructure modernization further amplify demand.

Emerging Green Data Centers and Smart Campus Development

Growing environmental consciousness supports new opportunities in sustainable facility design. The Latin America Data Center Physical Security Market aligns security with energy-efficient operations. Green campuses adopt solar-powered surveillance, low-emission materials, and intelligent air systems. Integration of smart sensors enhances both environmental and physical performance. Investors target eco-certified facilities for long-term returns. Partnerships between global OEMs and regional builders foster innovation. These developments will define the future investment focus of the region’s data center ecosystem.

Market Segmentation

By Data Center Size

Large data centers dominate the Latin America Data Center Physical Security Market due to the presence of hyperscale facilities from global cloud providers. These centers require multi-layered access systems, real-time surveillance, and redundant monitoring structures. Medium-sized data centers grow steadily with regional colocation and enterprise demand. Small facilities serve localized applications but face investment challenges. The increasing presence of modular facilities will boost mid-tier market participation.

By Component

Solutions hold a larger share of the market than services, driven by growing adoption of surveillance, biometric, and intrusion systems. In the Latin America Data Center Physical Security Market, service segments like integration and consulting support ongoing system optimization. Demand for long-term maintenance contracts continues to rise. Solution vendors dominate initial capital deployment, while managed service providers ensure sustained uptime and reliability.

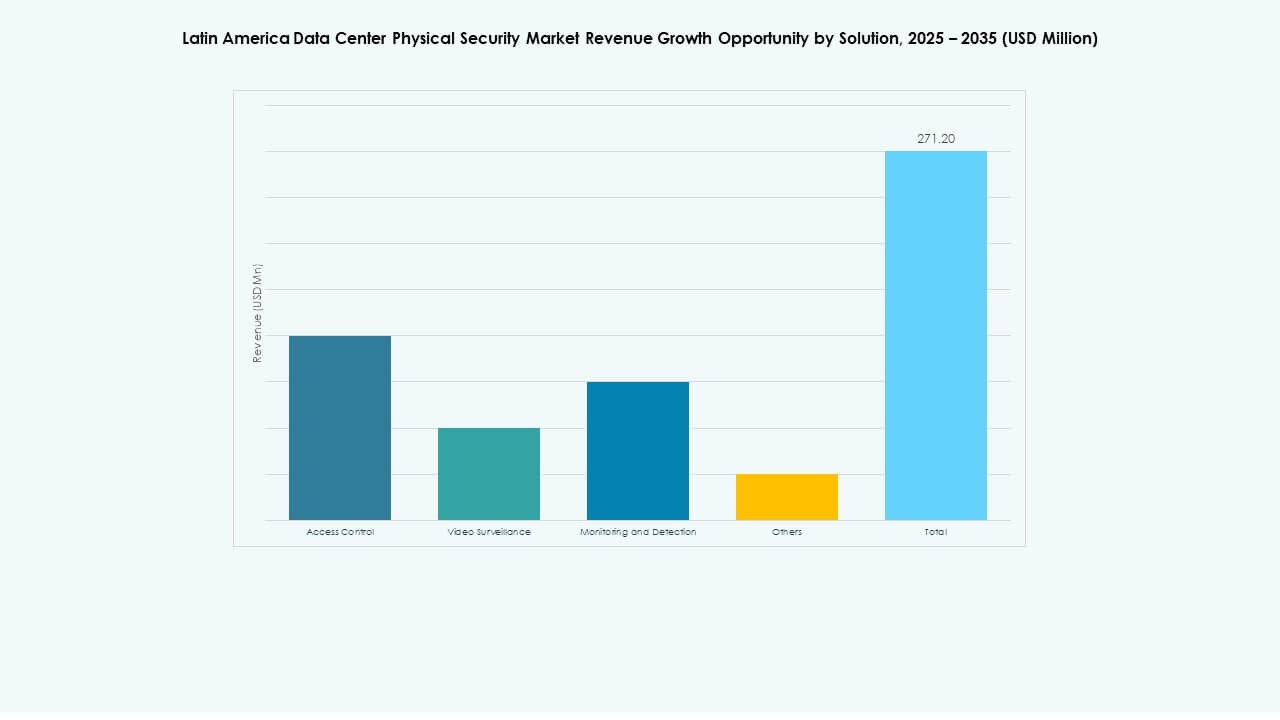

By Solution

Access control and video surveillance lead this segment, accounting for most deployments. These solutions protect sensitive zones and verify personnel identity. Monitoring and detection systems are expanding rapidly through AI-based analytics. The Latin America Data Center Physical Security Market also sees growth in integrated dashboards linking these tools. Emerging technologies like infrared and LiDAR enhance detection range and accuracy.

By Services

System integration remains the key service segment, ensuring smooth deployment of security systems. Consulting services guide operators on compliance with evolving data protection standards. The Latin America Data Center Physical Security Market emphasizes maintenance to prevent downtime and improve resilience. Outsourced service models gain traction among mid-tier data centers seeking efficiency. Preventive maintenance contracts improve cost control and risk management.

By Security Layer

Perimeter and building access layers dominate this segmentation, forming the first line of defense. Data hall and rack-level protection grow with rising adoption of AI servers and sensitive assets. The Latin America Data Center Physical Security Market expands across multiple zones using smart locks and advanced video analytics. Layered security ensures redundancy and resilience against intrusion attempts.

By Data Center Type

Hyperscale data centers lead with significant investment from multinational cloud providers. Colocation facilities follow due to rising enterprise outsourcing needs. The Latin America Data Center Physical Security Market also benefits from enterprise and edge data center expansion. Edge data centers require compact and autonomous security tools for remote sites. The “others” category includes modular facilities supporting 5G and AI workloads.

By End-user

IT & Telecom and BFSI sectors hold the largest shares due to their dependence on secure digital infrastructure. Government & defense projects are expanding with public cloud initiatives. Healthcare and retail segments show strong demand for protected data environments. The Latin America Data Center Physical Security Market grows through industry-wide digital transformation. Manufacturing and e-commerce facilities strengthen their data protection measures to ensure business continuity.

Regional Insights

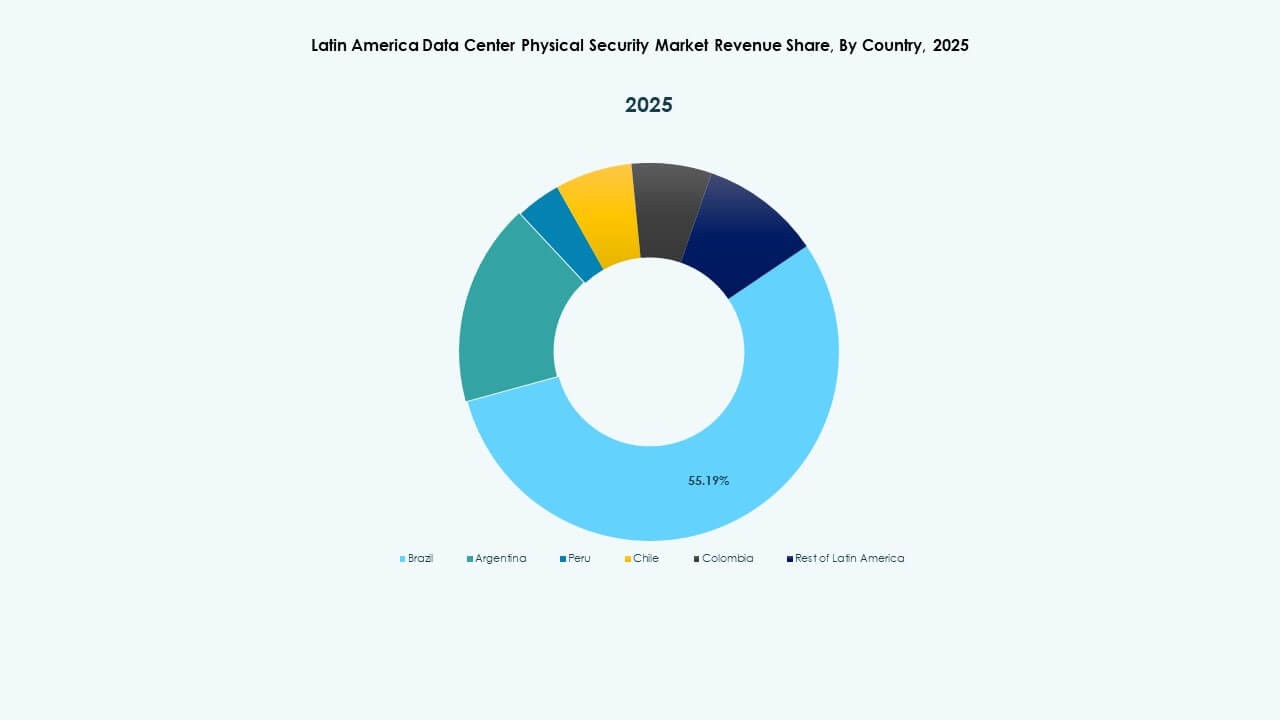

South America – Brazil and Chile Lead Regional Deployment

South America accounts for about 60% of the total market share, led by Brazil and Chile. The Latin America Data Center Physical Security Market benefits from hyperscale data center expansion in São Paulo, Rio de Janeiro, and Santiago. Brazil hosts global providers like Equinix and ODATA, driving infrastructure modernization. Chile’s stable energy policies and international connectivity attract new investments. Security demand focuses on advanced access control and energy-efficient surveillance systems. These countries serve as innovation centers for regional data resilience and compliance.

- For instance, Equinix is expanding in Brazil and has a new data-center campus under development in São Paulo and Rio de Janeiro to meet surging demand.

North Latin America – Mexico and Colombia Emerging Strongly

Mexico captures nearly 25% of the regional share due to robust industrial growth and data localization policies. The Latin America Data Center Physical Security Market in this area evolves through investments by carriers and cloud providers. Mexico City and Querétaro lead facility development, while Colombia strengthens its ecosystem through regulatory reforms. Demand grows for integrated access control and high-resolution video monitoring systems. These nations benefit from strong connectivity with the U.S. market and expanding cloud zones.

Rest of Latin America – Argentina and Peru Showing Potential

Smaller economies including Argentina and Peru hold around 15% market share but show steady improvement. The Latin America Data Center Physical Security Market here benefits from new colocation projects and government-driven digital strategies. Local integrators introduce modular security systems for mid-sized facilities. Challenges remain in regulatory standardization and high infrastructure cost. Yet, steady investments in telecom networks and industrial parks are expanding security demand. Growth in these regions will accelerate as digital transformation programs mature.

- For instance, recent analyses list Argentina and Peru among the 17 Latin American countries with both existing and upcoming colocation data centers.

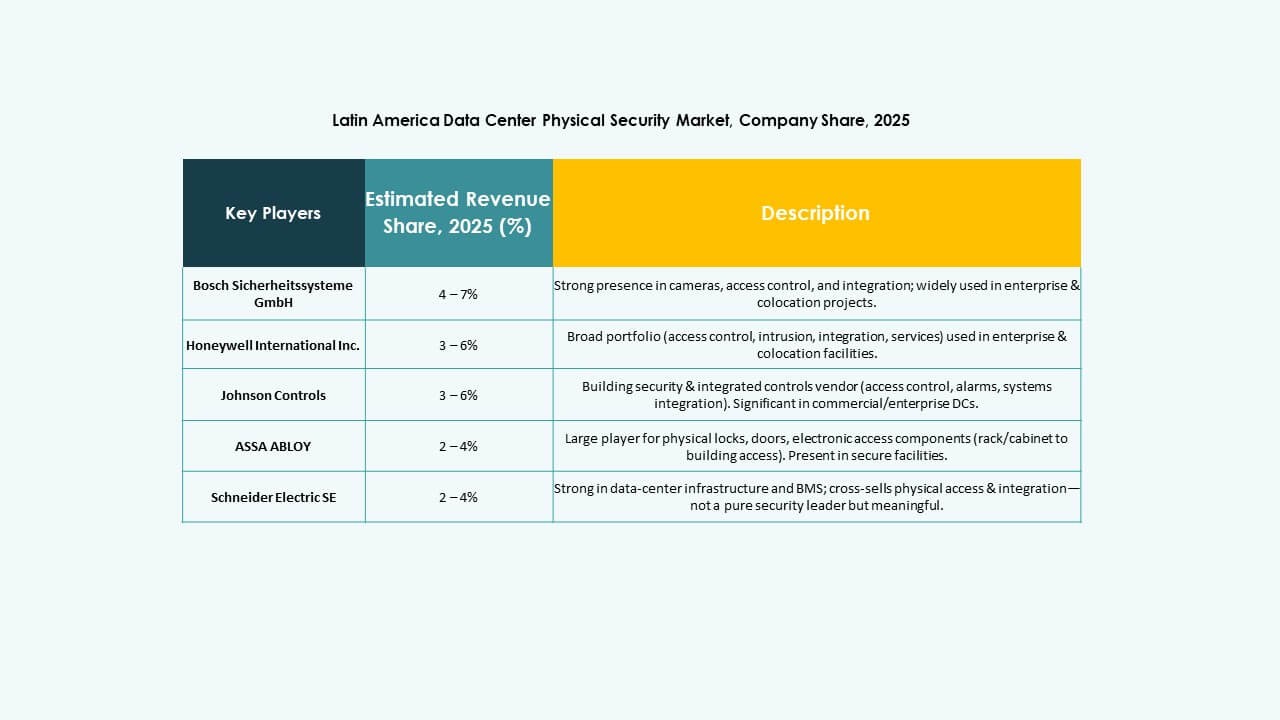

Competitive Insights:

Competitive Insights:

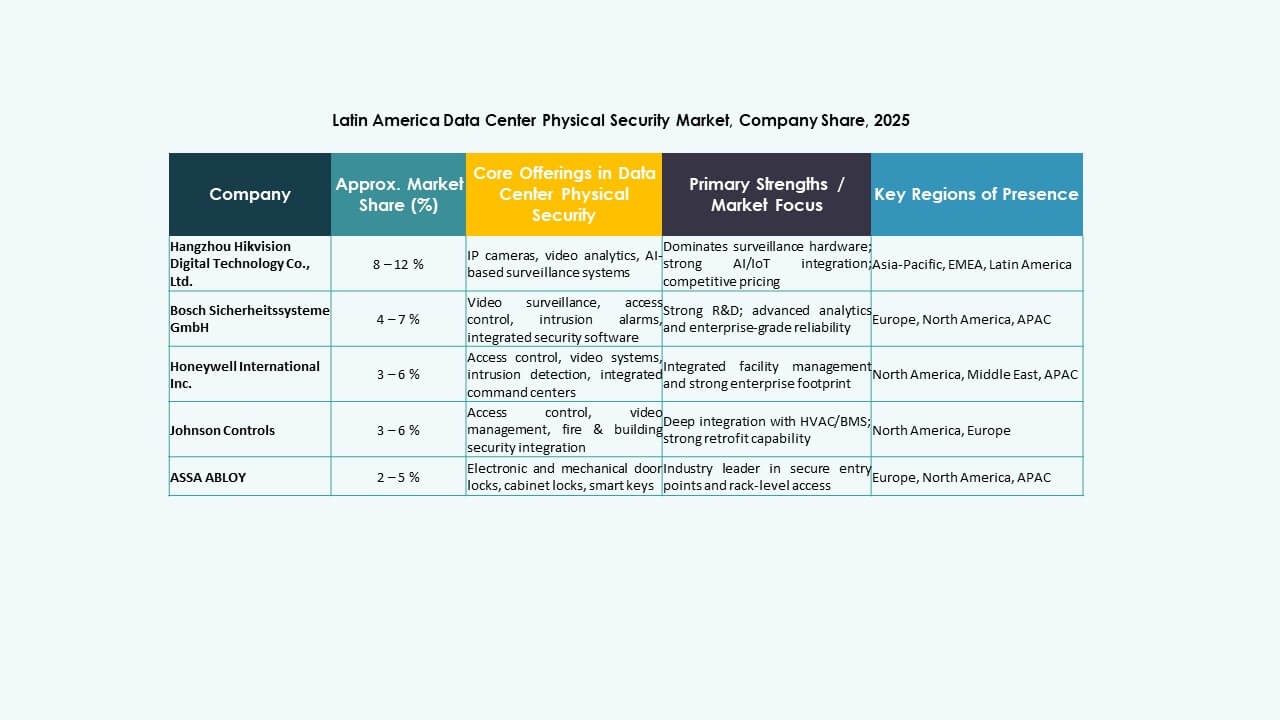

- Bosch Sicherheitssysteme GmbH

- Johnson Controls International plc

- Honeywell International Inc.

- Axis Communications AB

- Schneider Electric SE

- ABB Ltd

- Siemens AG

- Cisco Systems, Inc.

- Genetec Inc.

- Dahua Technology Co., Ltd.

The competitive landscape shows a mix of established global security firms and specialized surveillance providers battling for data-center contracts. Bosch and Johnson Controls leverage broad portfolios to offer integrated access control, intrusion detection, and monitoring systems. Honeywell and Schneider Electric focus on enterprise-grade solutions combining physical security with building management. Axis and Dahua emphasize high-end video surveillance and analytics modules. ABB, Siemens, Cisco and Genetec supply infrastructure that scales across large hyperscale and colocation centers. The presence of diverse offerings pushes innovation and cost competition. In this environment, building trust through compliance, reliability, and service capability gives firms a major edge in winning contracts.

Recent Developments:

- In April 2025, Allied Universal expanded its footprint in Latin America by acquiring Celar Security and Soltes Technology in Colombia, adding $490 million in annual revenue across the South American region. This acquisition signifies Allied Universal’s commitment to strengthening its presence and service offerings within the physical security market in Latin America.

- In June 2025, Bosch Sicherheitssysteme GmbH completed the sale of its security and communication technology products business to the European investment firm Triton. This business unit, renamed Keenfinity Group, now operates autonomously within Triton’s portfolio and includes brands in video systems, access control, intrusion alarms, and communications.