Executive summary:

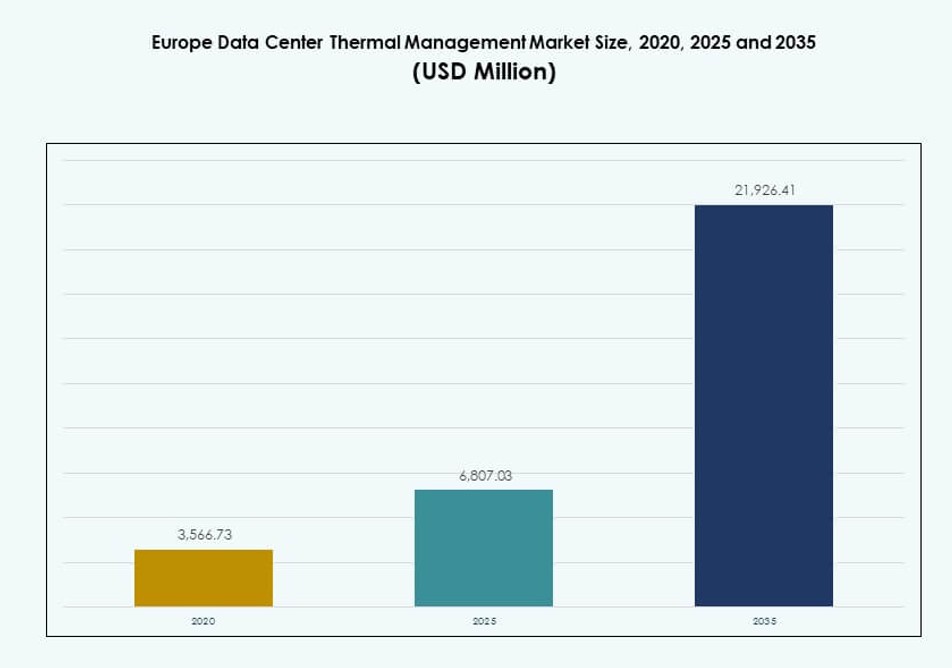

The Europe Data Center Thermal Management Market size was valued at USD 3,566.73 million in 2020 to USD 6,807.03 million in 2025 and is anticipated to reach USD 21,926.41 million by 2035, at a CAGR of 12.34% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Europe Data Center Thermal Management Market Size 2025 |

USD 6,807.03 Million |

| Europe Data Center Thermal Management Market, CAGR |

12.34% |

| Europe Data Center Thermal Management Market Size 2035 |

USD 21,926.41 Million |

Rising rack power densities, AI-driven workloads, and growing energy efficiency mandates are driving strong demand for advanced cooling systems. Businesses adopt liquid-based and AI-optimized thermal solutions to ensure uptime, cut operational costs, and meet sustainability goals. Innovation in direct-to-chip cooling, modular units, and predictive controls plays a critical role in supporting workload scalability. The market is strategically important for investors targeting long-term value in digital infrastructure, as thermal systems influence total cost of ownership and regulatory compliance across facilities.

Western Europe leads the market, with Germany, the UK, and the Netherlands at the forefront due to hyperscale presence, robust digital infrastructure, and regulatory pressure. Nordic countries are emerging as key regions by leveraging natural climate benefits and renewable energy for sustainable cooling. Southern and Eastern Europe are seeing growing demand, driven by expanding edge deployments, affordable land, and improved connectivity. This regional mix reflects evolving demand across centralized and distributed data environments.

Market Dynamics:

Market Drivers

Rapid Increase in Rack Power Density and AI Workloads Demanding Efficient Thermal Control

The Europe Data Center Thermal Management Market is driven by rising rack power densities in hyperscale and enterprise data centers. New workloads such as AI and machine learning require dense compute clusters, which generate significant heat. Operators deploy advanced cooling systems to maintain equipment reliability. Air-based solutions struggle at higher heat loads, pushing adoption of direct-to-chip and immersion cooling. Efficient thermal design now directly impacts data center uptime and performance. Infrastructure teams integrate thermal planning into early-stage development. Cooling investments are now strategic business decisions. The growing role of sustainability policies further reinforces energy-conscious cooling choices. Long-term value lies in lifecycle cost savings and operational resilience.

- For instance, AI-optimized deployments in Europe reached average rack densities of 36 kW by 2023, while general colocation facilities maintained averages between 8–12 kW. High-performance zones supporting HPC and liquid-cooled environments now deploy racks exceeding 40 kW.

Sustainability Mandates and Energy Efficiency Standards Accelerating Thermal Innovations

Across Europe, strict energy policies and carbon reduction targets drive demand for sustainable cooling technologies. Data centers face rising scrutiny for power use and environmental impact. Operators adopt energy-efficient thermal solutions to comply with EU-wide standards and country-specific regulations. PUE and WUE benchmarks guide investment in advanced cooling infrastructure. Technologies such as free cooling, liquid loops, and AI-based optimization enable compliance. Renewable energy integration supports low-impact thermal performance. ESG frameworks make thermal management critical for attracting green investors. Energy audits often start with assessing thermal efficiency metrics. The Europe Data Center Thermal Management Market gains strategic value from aligning with clean energy agendas.

- For instance, data centers in England have achieved water usage effectiveness (WUE) as low as 0.36 liters per kWh by using optimized indirect and hybrid cooling systems. These WUE benchmarks support investment decisions in sustainable thermal infrastructure.

High Adoption of Liquid Cooling in New Build and Retrofit Projects

The shift toward liquid-based cooling systems has gained momentum across new and legacy data centers. Operators upgrade traditional air systems with direct-to-chip or immersion cooling to manage rising heat loads. This change improves cooling efficiency and reduces floor space use. Retrofit projects include row-level cooling modules and sealed cabinets. Developers prioritize scalable, modular liquid systems to future-proof operations. Liquid cooling supports high compute densities for AI, blockchain, and analytics use cases. Data centers in colder climates combine liquid systems with ambient air to extend efficiency. Manufacturers offer integrated cooling products to ease deployment. It strengthens competitiveness and ROI for owners and investors.

Digital Transformation and Edge Computing Driving Distributed Cooling Demands

The market sees growth in distributed data center networks requiring flexible thermal solutions. Edge deployments often operate in space-constrained or remote areas with limited infrastructure. These setups need localized, low-maintenance cooling strategies. Compact liquid systems and self-contained modules enable thermal control without traditional HVAC. AI-based automation helps maintain optimal performance with minimal intervention. Retail, telecom, and industrial firms adopt edge setups for low-latency services. Thermal systems are now part of digital infrastructure strategy. Localized cooling reduces dependency on central utility supply. The Europe Data Center Thermal Management Market grows as digital transformation deepens across industries.

Market Trends

Growing Integration of AI-Driven Cooling Algorithms to Optimize Thermal Performance

Data centers across Europe are integrating AI software to dynamically control cooling loads. These platforms analyze sensor data to adjust airflow, coolant flow rate, and power distribution in real time. AI-based thermal management improves uptime and lowers energy use. Operators reduce overcooling and identify hotspots early. The approach supports predictive maintenance and reduces human intervention. AI tools scale across large and distributed data center portfolios. Optimization becomes continuous, not reactive. Operators combine AI with CFD modeling for deep thermal insights. The Europe Data Center Thermal Management Market benefits from embedding AI into thermal strategies.

Rise of Modular and Prefabricated Cooling Systems for Speed and Scalability

Operators deploy modular cooling systems to accelerate construction and support rapid scaling. These prefabricated systems include integrated cooling units that reduce onsite labor. Modular design helps meet timelines for hyperscale and colocation clients. Liquid cooling modules are now built with standard dimensions for fast installation. Operators can scale thermal capacity without major redesigns. Cooling-as-a-module is gaining popularity in distributed and edge facilities. Manufacturers offer rack, row, and room-based modules tailored to different load profiles. The Europe Data Center Thermal Management Market adopts modular strategies to improve speed-to-market and minimize disruptions during upgrades.

Increased Focus on Water Usage Effectiveness and Zero-Liquid Discharge Systems

Operators now evaluate thermal systems using both PUE and WUE metrics. Water-saving measures are becoming as critical as energy use. Cooling towers and adiabatic systems face pressure due to water scarcity concerns. Operators shift to closed-loop systems or use air-liquid hybrid solutions to reduce evaporative losses. In urban or regulation-heavy locations, zero-liquid discharge cooling designs are becoming standard. Facilities monitor water consumption through automated metering and cloud dashboards. WUE benchmarks are becoming key parameters in ESG assessments. The Europe Data Center Thermal Management Market aligns with circular water principles to reduce environmental footprint.

Cross-Integration of DCIM and Thermal Management Platforms for Operational Synergy

Operators merge DCIM tools with thermal controls for a unified view of data center performance. These integrated platforms provide real-time analytics, asset mapping, and cooling system control. Operators monitor rack-level temperatures and correlate with workload patterns. Automated triggers adjust CRAC/CRAH units, pumps, and containment zones. It improves responsiveness and reduces manual tuning. System-wide thermal transparency supports SLA compliance and energy audits. Modular software packages are preferred for multivendor sites. The Europe Data Center Thermal Management Market adopts unified control to streamline data center operations and improve thermal outcomes.

Market Challenges

High Capital Investment and Retrofit Complexity Limit Rapid Adoption of Advanced Systems

Deploying new thermal systems involves significant capital investment, which deters small and mid-size operators. Advanced systems like immersion cooling or rear-door heat exchangers require specialized infrastructure. Retrofitting existing facilities presents compatibility issues with legacy racks and power systems. Space limitations often prevent the full implementation of newer cooling modules. Downtime risks during upgrades also delay retrofitting decisions. Some operators delay investment until equipment reaches end-of-life. Uncertainty around technology standardization makes long-term planning difficult. The Europe Data Center Thermal Management Market faces barriers due to upgrade cost, design complexity, and operational disruption risks.

Talent Shortage and Limited Expertise in Emerging Cooling Technologies Slow Deployment

The region faces a skills gap in designing, implementing, and maintaining advanced thermal management systems. Workforce trained in legacy air systems struggles to manage liquid-based setups. Operators require engineers who understand fluid dynamics, automation, and energy modeling. Talent shortages increase project lead times and consulting costs. Mismanagement risks rise in high-density deployments. Vendor support becomes essential for system stability. Training programs lag behind rapid tech shifts in thermal design. The Europe Data Center Thermal Management Market must address this skill gap to support reliable and timely adoption of emerging cooling innovations.

Market Opportunities

Growing Investments in Hyperscale and Edge Facilities Creating Need for Scalable Cooling

Europe’s digital expansion brings strong investment in hyperscale and edge infrastructure. Operators look for modular, energy-efficient cooling systems that scale with load growth. These systems improve deployment speed and support sustainability goals. Compact thermal units meet edge needs while centralized liquid cooling supports hyperscale. The Europe Data Center Thermal Management Market benefits from this dual growth, enabling tailored solutions for different scales and use cases.

Government Incentives and Sustainability Mandates Accelerate Adoption of Green Cooling

Policymakers across the EU support low-carbon data centers through incentives and tax benefits. This drives demand for eco-friendly cooling systems using renewable energy, heat reuse, and water recovery. Compliant systems gain fast-tracked permits and utility approvals. The Europe Data Center Thermal Management Market grows as policy alignment reduces risk and improves investor confidence in green infrastructure projects.

Market Segmentation

By Data Center Size

Large data centers hold the dominant share due to heavy deployment in hyperscale and colocation projects. These facilities require high-capacity cooling systems with modular scalability. Medium-sized centers are also growing, especially in enterprise and regional edge hubs. Small centers hold a niche presence but adopt flexible, low-footprint thermal systems. The Europe Data Center Thermal Management Market sees strong volume in large builds due to concentrated workload demands.

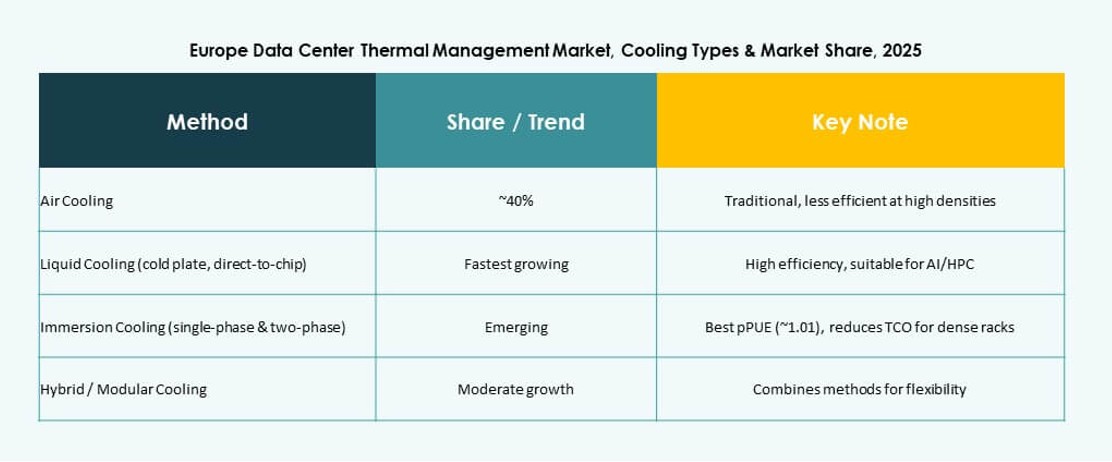

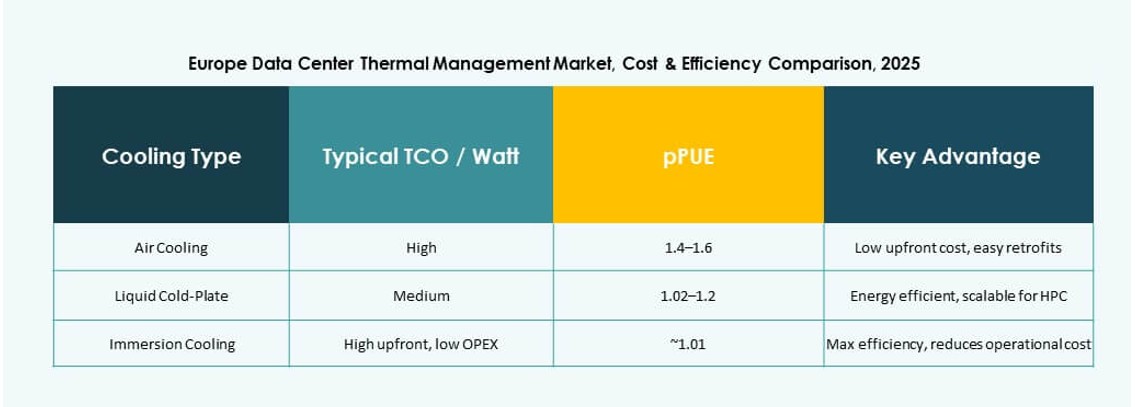

By Cooling Technology

Air-based cooling remains widely used, especially with direct air and hot/cold aisle containment. Liquid-based cooling is rising, led by direct-to-chip and immersion solutions for AI-heavy environments. Hybrid setups mix air and liquid for staged cooling. Emerging options like thermoelectric and phase-change show innovation but limited scale. The Europe Data Center Thermal Management Market sees air-liquid combinations dominate future builds for balanced efficiency.

By Component

Hardware leads the market with demand for chillers, airflow units, and heat exchangers. Software adoption grows due to AI optimization and simulation tools that improve thermal efficiency. Services play a key role in installations, retrofits, and monitoring. The Europe Data Center Thermal Management Market is shaped by integrated offerings that combine all three components to deliver reliable cooling outcomes.

By Hardware

Cooling units and heat exchangers hold strong demand in large-scale facilities. Rear-door and airflow devices suit high-density configurations. Piping systems evolve to support modular, leak-proof deployment. The Europe Data Center Thermal Management Market benefits from product innovations in high-efficiency chillers and compact cooling loops.

By Software

AI optimization platforms gain traction for energy-aware cooling. DCIM dashboards offer centralized visibility and control. CFD simulations help with proactive thermal planning. BMS modules integrate with power and cooling for unified facility management. The Europe Data Center Thermal Management Market grows with software-led cooling intelligence.

By Services

Preventive maintenance and retrofits see rising demand as facilities modernize. Monitoring-as-a-service is gaining in edge environments. Installation and commissioning remain essential for greenfield projects. Service providers focus on uptime and regulatory compliance. The Europe Data Center Thermal Management Market relies on expert services to support thermal infrastructure throughout the asset lifecycle.

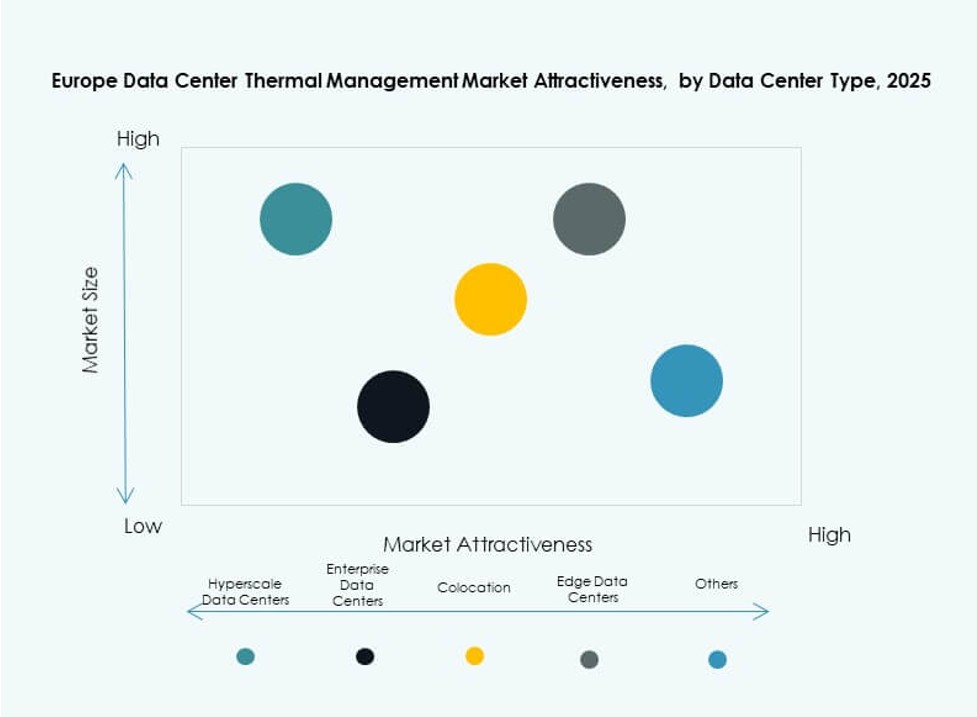

By Data Center Type

Hyperscale facilities dominate due to their large footprint and high thermal loads. Colocation/cloud sites show strong growth with shared cooling models. Edge/micro centers need compact, adaptive thermal systems. Enterprise data centers adopt hybrid approaches. The Europe Data Center Thermal Management Market thrives across multiple data center types with tailored cooling strategies.

By Structure

Rack-based cooling gains share in dense computing environments. Row-based systems balance efficiency and scalability in modular builds. Room-based approaches remain common in legacy or large-scale deployments. The Europe Data Center Thermal Management Market aligns cooling structure with workload profiles and space availability.

Regional Insights

Western Europe Dominates the Market with Over 40% Share

Western Europe leads the Europe Data Center Thermal Management Market due to strong data infrastructure in Germany, the UK, France, and the Netherlands. These countries support large hyperscale deployments and cloud zones. Strict energy policies push adoption of sustainable cooling. Operators invest heavily in advanced systems to meet green targets. The region’s share stands above 40%, driven by mature data ecosystems and robust demand.

- For instance, CyrusOne’s Frankfurt FRA5 facility uses N+1 free cooling air-cooled chillers with a closed-loop chilled water system across its 54 MW IT capacity.

Nordic Countries Emerging with 25% Share Backed by Climate Advantage and Green Power

Nordic nations including Sweden, Norway, Finland, and Denmark hold around 25% market share. These countries use natural cooling and renewable energy to minimize operational costs and environmental impact. The cold climate allows free cooling throughout the year. Data center growth in this region is driven by hyperscale interest in green hosting. Local governments support digital infrastructure with low taxes and clean energy access.

- For instance, Daikin supplies energy-efficient chiller systems to Green Mountain’s DC1-Stavanger facility in Norway, which operates with up to 30 MW IT load. The site leverages advanced cooling and 100% renewable hydropower for sustainable operations.

Southern and Eastern Europe Gaining Traction with 20% Market Share

Southern and Eastern Europe together account for roughly 20% of the market, led by Spain, Italy, Poland, and Czech Republic. These regions attract colocation and edge deployments due to lower real estate costs and expanding connectivity. Governments offer incentives for digital infrastructure growth. Operators target second-tier cities for regional data hubs. The Europe Data Center Thermal Management Market expands here as demand for decentralized computing increases.

Competitive Insights:

- Vertiv Group Corp.

- Schneider Electric

- Stulz GmbH

- Airedale International Air Conditioning Ltd.

- Munters Group AB

- Rittal GmbH & Co. KG

- Daikin Industries Ltd.

- Delta Electronics, Inc.

- Huawei Technologies Co., Ltd.

- Trane Technologies plc

The Europe Data Center Thermal Management Market features a competitive landscape led by global and regional powerhouses. Vertiv, Schneider Electric, and Stulz dominate with scalable thermal solutions tailored for hyperscale, colocation, and edge deployments. These players focus on liquid cooling innovations and AI-driven thermal optimization. Companies like Airedale, Munters, and Rittal offer modular systems adapted for European climate zones and regulatory compliance. Market leadership depends on system energy efficiency, retrofit capabilities, and ease of integration with power infrastructure. Firms compete on service quality, system uptime, and software-enabled control. It is driven by sustainability targets and investor demand for low-impact, future-ready infrastructure.

Recent Developments:

- In November 2025, Eaton Corporation signed a definitive agreement to acquire Boyd Thermal for $9.5 billion, expanding its liquid cooling technology for data centers to address surging AI-driven power demands

- In March 2025, Delta Electronics, Inc. unveiled next-generation power and liquid cooling solutions, including 1.5MW liquid-to-liquid Coolant Distribution Units (CDUs), at NVIDIA GTC 2025 designed for AI and HPC data centers.

- In October 2024, Wieland acquired Onda S.p.A., an Italian producer of advanced heat exchangers, to bolster its data center cooling and thermal solutions in Europe.