Executive summary:

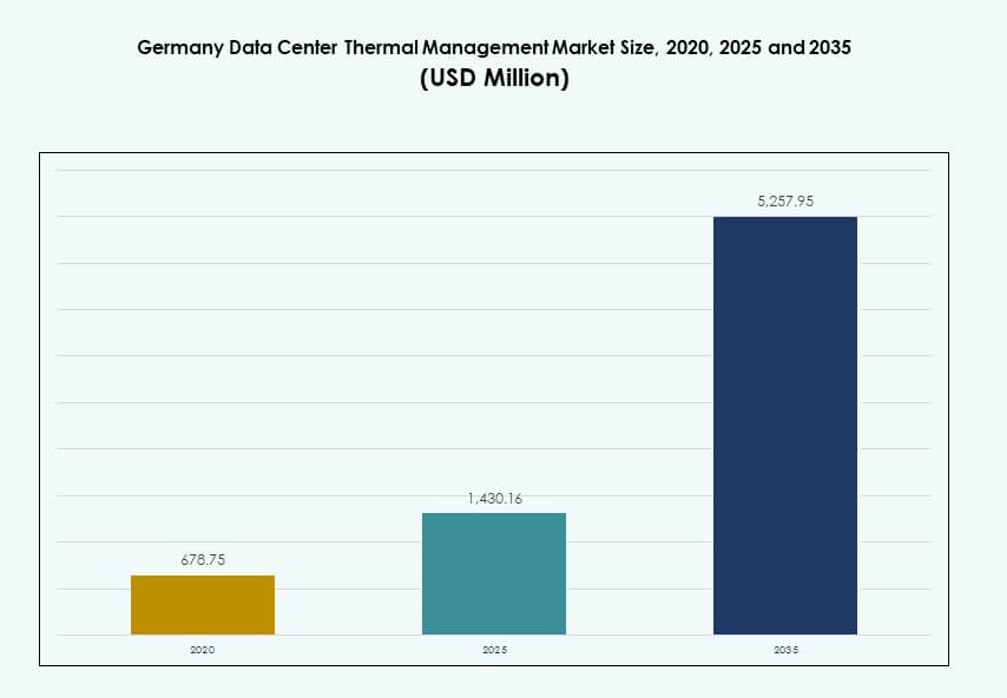

The Germany Data Center Thermal Management Market size was valued at USD 678.75 million in 2020, rising to USD 1,430.16 million in 2025, and is anticipated to reach USD 5,257.95 million by 2035, at a CAGR of 13.81% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Germany Data Center Thermal Management Market Size 2025 |

USD 1,430.16 Million |

| Germany Data Center Thermal Management Market, CAGR |

13.81% |

| Germany Data Center Thermal Management Market Size 2035 |

USD 5,257.95 Million |

The market is driven by rising rack power density, growth in hyperscale data centers, and national energy-efficiency mandates. Liquid-based and hybrid cooling technologies are replacing legacy air systems to support AI, HPC, and real-time analytics. Operators are adopting AI-enabled thermal automation tools and integrating waste heat reuse into green building designs. These shifts make the market strategic for data center operators, infrastructure vendors, and institutional investors focused on sustainable, high-performance infrastructure.

Frankfurt leads the market due to its dense hyperscale ecosystem and interconnection capacity. Berlin and Munich are emerging with strong colocation and enterprise investments. Regions such as North Rhine-Westphalia and Saxony are gaining relevance with modular edge deployments and access to green energy. This regional diversity encourages the adoption of flexible and localized cooling technologies across facility types.

Market Dynamics:

Market Drivers

Rising Rack Density in Hyperscale and AI-Driven Data Centers Demands Advanced Thermal Systems

Hyperscale facilities in Germany are integrating AI workloads and high-performance computing, pushing rack densities beyond 20–30 kW. This shift requires advanced thermal management systems that go beyond traditional air-based methods. Direct-to-chip liquid cooling and rear door heat exchangers are being adopted to maintain optimal performance. These systems ensure lower PUE, improving operational efficiency across large data halls. The Germany Data Center Thermal Management Market benefits from this demand for high-efficiency cooling. Operators aim to minimize downtime and energy costs while supporting expanding workloads. Infrastructure upgrades focus on scalable, high-capacity cooling systems. This trend drives investment across both new builds and retrofits.

- For instance, Hetzner Online’s Nuremberg Data Center Park uses direct free cooling and holds a TÜV SÜD‑certified PUE of 1.1242. The facility is designed for high efficiency and supports large-scale server deployments of up to 32,000 units.

Government Energy Regulations and Climate Goals Push Operators Toward Greener Cooling Infrastructure

Germany’s strict energy efficiency mandates and climate goals require data centers to reduce carbon footprints. Thermal management systems play a key role in achieving these sustainability targets. Operators must shift to liquid cooling, hybrid systems, or AI-optimized air circulation to comply. Subsidies and carbon taxes create financial incentives for low-emission infrastructure upgrades. The Germany Data Center Thermal Management Market aligns closely with national decarbonization policies. Investors view this compliance as a pathway to long-term stability. Green-certified data centers attract clients focused on ESG benchmarks. Operators also pursue LEED and ISO certifications to strengthen market position.

- For example, GISA’s data center in Halle near Leipzig captures waste heat from its cooling water and uses it to preheat office spaces. This measure cut energy consumption by around 22,000 kWh in January 2025, demonstrating practical reuse of residual data center heat in real‑world operations.

Technological Innovation in Thermal Management Hardware and Software Drives Performance Gains

Rapid innovation in both hardware and software is shaping cooling strategies. New-generation chillers, fans, and heat exchangers offer better performance with lower energy use. AI and machine learning enhance airflow management and dynamic cooling responses. DCIM dashboards and CFD simulations help operators visualize and adjust real-time temperature patterns. These tools reduce human error and optimize power consumption. The Germany Data Center Thermal Management Market benefits from these technologies through improved reliability. Integrators and OEMs collaborate to embed smart cooling into modular systems. Customization options cater to different data center sizes and structures. This modularity improves upgrade timelines and cost control.

Shift Toward Edge and Modular Data Centers Fuels Demand for Compact, Scalable Cooling Systems

The rise of edge computing and modular data centers across urban and remote zones creates demand for compact cooling. These smaller sites face space and power constraints, requiring highly efficient thermal units. Passive liquid cooling and sealed systems are preferred in edge deployments. The Germany Data Center Thermal Management Market supports this shift through flexible system designs. Vendors offer pre-integrated rack-based cooling tailored to limited environments. Investors target edge sites in healthcare, manufacturing, and telecom for their low-latency benefits. Thermal resilience in edge setups becomes a key differentiator. Scalable solutions enable phased expansion with minimal disruption.

Market Trends

Adoption of AI-Based Cooling Optimization Tools for Dynamic Energy and Airflow Management

Operators in Germany are adopting AI-based tools to manage airflow and energy use in real time. These tools analyze data from sensors and adjust cooling patterns instantly. They help reduce hotspots and balance temperature across racks and aisles. AI models also forecast load behavior, allowing predictive thermal adjustments. The Germany Data Center Thermal Management Market is seeing rapid growth in smart software deployments. These tools integrate with BMS and DCIM platforms for centralized control. Companies reduce overcooling, saving electricity and extending equipment life. Predictive optimization lowers operational risk while boosting sustainability metrics.

Growth in Demand for Liquid Cooling Across Colocation and High-Density Workloads

Liquid cooling solutions are gaining traction across colocation and enterprise environments. Direct-to-chip and immersion cooling are no longer limited to hyperscale setups. Medium-sized data centers also adopt liquid systems to manage rising rack density. These solutions support GPU-intensive workloads like AI training and 3D modeling. The Germany Data Center Thermal Management Market sees strong demand from engineering, fintech, and research institutions. Liquid cooling supports better temperature uniformity and lower PUE. Vendors offer retrofitting kits for older racks. This shift expands liquid-based infrastructure beyond early adopters.

Data Center Renovation Projects Include Thermal Retrofits as Key Upgrade Priority

Operators are upgrading aging data centers to support new efficiency standards. Thermal systems are often the first focus during retrofits due to their impact on energy use. Air containment strategies, heat recovery, and hybrid cooling integration top the list. The Germany Data Center Thermal Management Market supports these projects with scalable, modular retrofit kits. Operators aim to meet updated building codes and ESG goals without full rebuilds. Smart cooling retrofits offer fast ROI and improve resilience. These projects unlock capacity in urban data center clusters. Local utilities also support upgrades through grid incentive programs.

Software-Defined Thermal Management Emerges in Integration with Edge Infrastructure

Software-defined cooling is expanding into edge and micro data center deployments. These systems rely on minimal staff and demand autonomous thermal control. Embedded software monitors temperature changes and adjusts fans or liquid flow. This trend is crucial for industries deploying hundreds of edge nodes across Germany. The Germany Data Center Thermal Management Market adapts to these needs through embedded control firmware. Vendors bundle cooling units with onboard diagnostics and cloud-based dashboards. These features reduce maintenance and unplanned downtime. It creates new revenue channels for cooling-as-a-service models.

Market Challenges

High Upfront Investment in Advanced Cooling Technologies Limits Adoption Across Mid-Sized Operators

Implementing liquid cooling or hybrid systems involves significant capital outlays. Mid-sized enterprises and colocation providers often delay upgrades due to budget limits. Equipment, installation, and skilled labor costs raise the total deployment burden. The Germany Data Center Thermal Management Market faces resistance among operators lacking economies of scale. ROI timelines for thermal upgrades can stretch beyond investor expectations. Vendors must offer financing or retrofit-friendly designs to increase adoption. Cost barriers slow progress on national energy efficiency goals. This creates a gap between leading hyperscale firms and small players.

Regulatory Complexity and Regional Grid Constraints Impact Sustainable Cooling Deployment

Germany’s diverse state-level regulations create uncertainty in thermal system deployment. Environmental permits, emissions limits, and power usage requirements differ by region. Grid availability also affects thermal strategy, especially in edge or rural sites. Operators face delays when aligning with local codes and utility guidelines. The Germany Data Center Thermal Management Market must adapt cooling designs to these fragmented rules. Compliance costs increase project complexity and timelines. Power-intensive cooling systems may not align with regional carbon reduction targets. These constraints limit flexibility in thermal innovation and planning.

Market Opportunities

Rising Preference for District Heating Integration and Waste Heat Recovery Opens New Revenue Models

Data centers are beginning to integrate thermal output with local district heating networks. Waste heat from cooling systems can support residential and industrial heating. This trend aligns with Germany’s energy circularity goals. The Germany Data Center Thermal Management Market finds new revenue streams through heat reuse agreements. Operators position themselves as heat suppliers while meeting emission targets. Government support strengthens this dual-use strategy.

Growing 5G, IoT, and AI Deployment Drives Demand for High-Efficiency Cooling in Edge and Modular Sites

Germany’s 5G and IoT expansion increases data demand at the network edge. Edge and modular data centers must operate reliably in diverse environments. The Germany Data Center Thermal Management Market sees strong growth in sealed cooling systems and passive liquid loops. Telecom and manufacturing sectors invest in these setups for real-time data processing. This creates opportunities for compact, resilient thermal products.

Market Segmentation

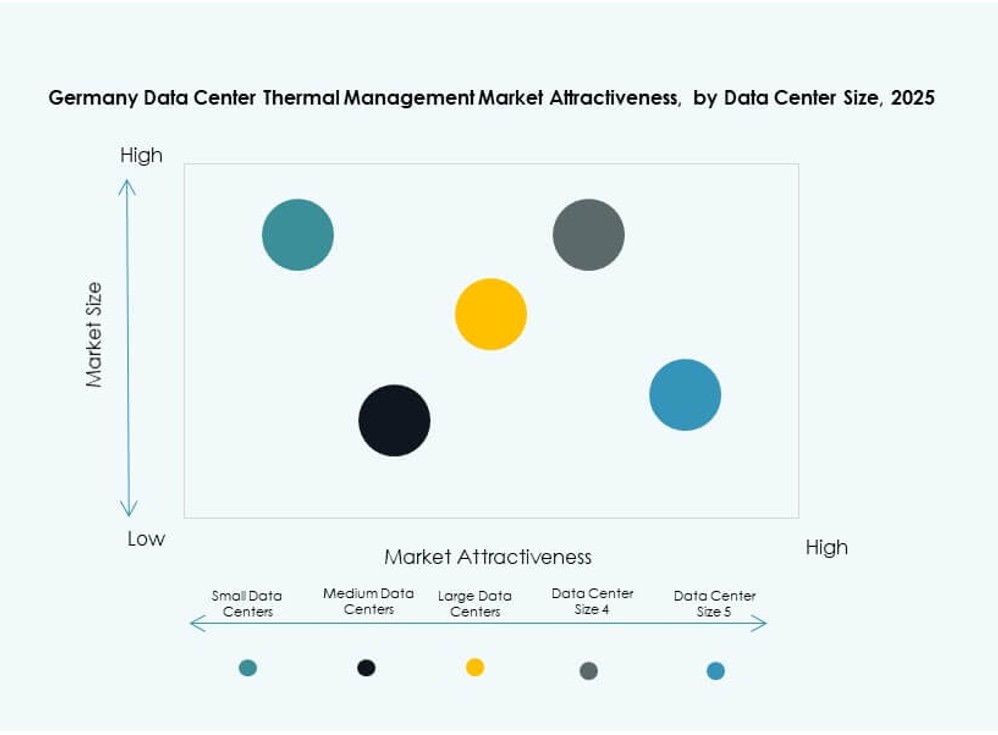

By Data Center Size

Large data centers dominate the Germany Data Center Thermal Management Market, accounting for over 50% of the total share. These facilities demand advanced cooling systems to handle high-density workloads. Small and medium data centers are growing steadily, driven by edge computing and colocation expansion. Mid-sized sites adopt scalable hybrid systems, while small sites use rack-level cooling. Large data centers continue to be primary adopters of liquid cooling.

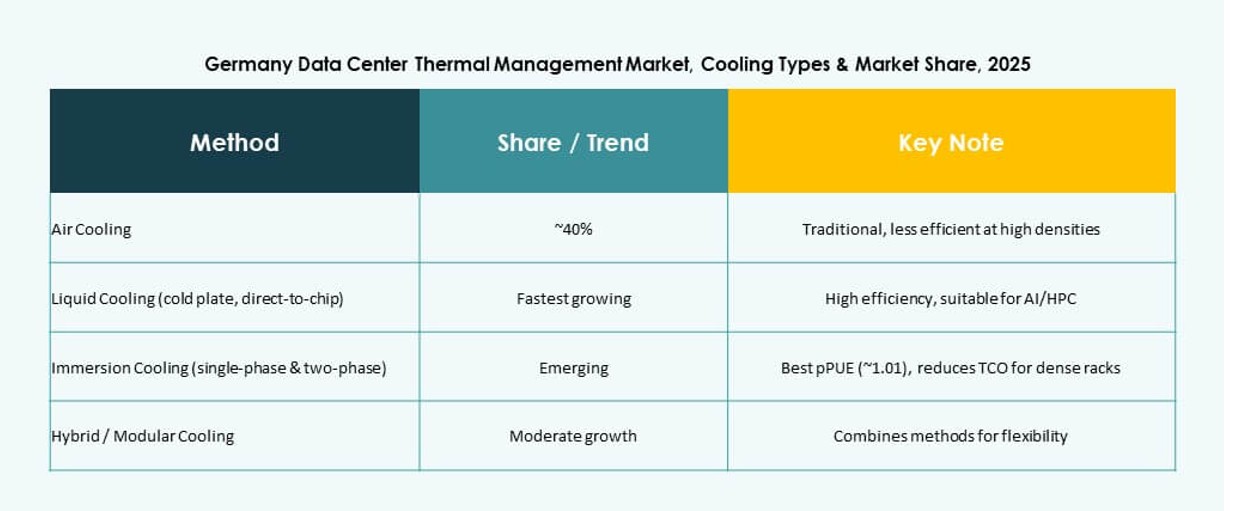

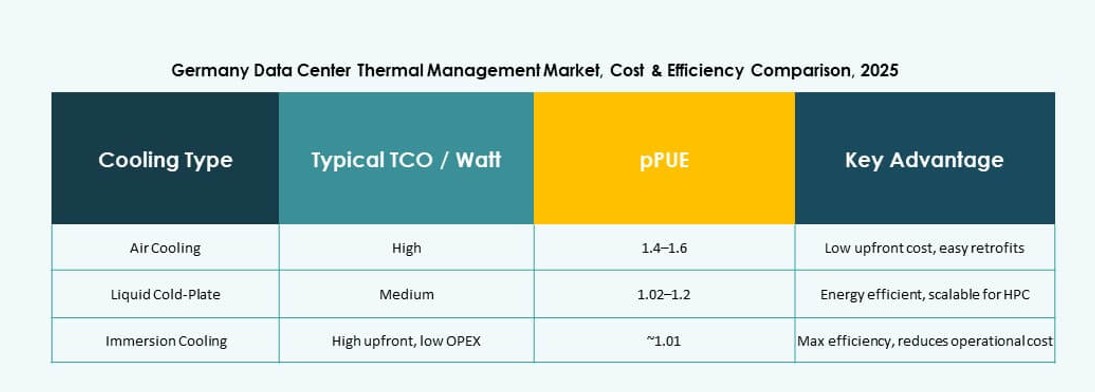

By Cooling Technology

Air-based cooling remains the most widely used across facilities, but liquid-based solutions are growing fast. Direct-to-chip and immersion cooling are expanding due to better heat transfer performance. Rear door heat exchangers are popular for retrofits. Hybrid systems combine air and liquid for energy savings. Thermoelectric and phase-change cooling remain niche but attract innovation. The Germany Data Center Thermal Management Market shows a strong shift toward liquid technologies in high-density zones.

By Component

Hardware holds the largest share due to the dominance of physical cooling systems like chillers and fans. Software is gaining momentum with AI-based optimization tools and DCIM dashboards. Services contribute significantly through retrofitting, installation, and remote monitoring. The Germany Data Center Thermal Management Market sees hardware investment driven by hyperscale builds. Software and services grow fastest in enterprise and colocation segments.

By Hardware

Cooling units and chillers form the bulk of hardware demand. Heat exchangers and airflow devices are essential for maintaining consistent temperature control. Fans and distribution components support air-based and hybrid setups. The Germany Data Center Thermal Management Market adopts advanced chillers for PUE reduction. Innovations in liquid distribution and heat reuse systems gain traction in large and modular data centers.

By Software

AI optimization tools lead the software segment with demand for real-time thermal management. DCIM platforms and BMS modules allow integrated cooling control. CFD simulation tools support planning and airflow design. The Germany Data Center Thermal Management Market favors software that enhances cooling efficiency and lowers energy consumption. Vendors integrate thermal modules into broader energy dashboards.

By Services

Installation and commissioning hold the largest share among services. Preventive maintenance and thermal monitoring services ensure long-term reliability. Retrofits and upgrades address changing density needs. Monitoring-as-a-service is rising with remote facility growth. The Germany Data Center Thermal Management Market benefits from bundled service packages across lifecycle stages.

By Data Center Type

Hyperscale data centers dominate due to high-density workloads and large cooling footprints. Colocation/cloud centers follow, driven by enterprise outsourcing and digital transformation. Edge and micro data centers are growing fast with 5G rollout. Enterprise data centers modernize thermal systems to meet ESG goals. The Germany Data Center Thermal Management Market reflects strong demand across all types, with hyperscale leading in volume and innovation.

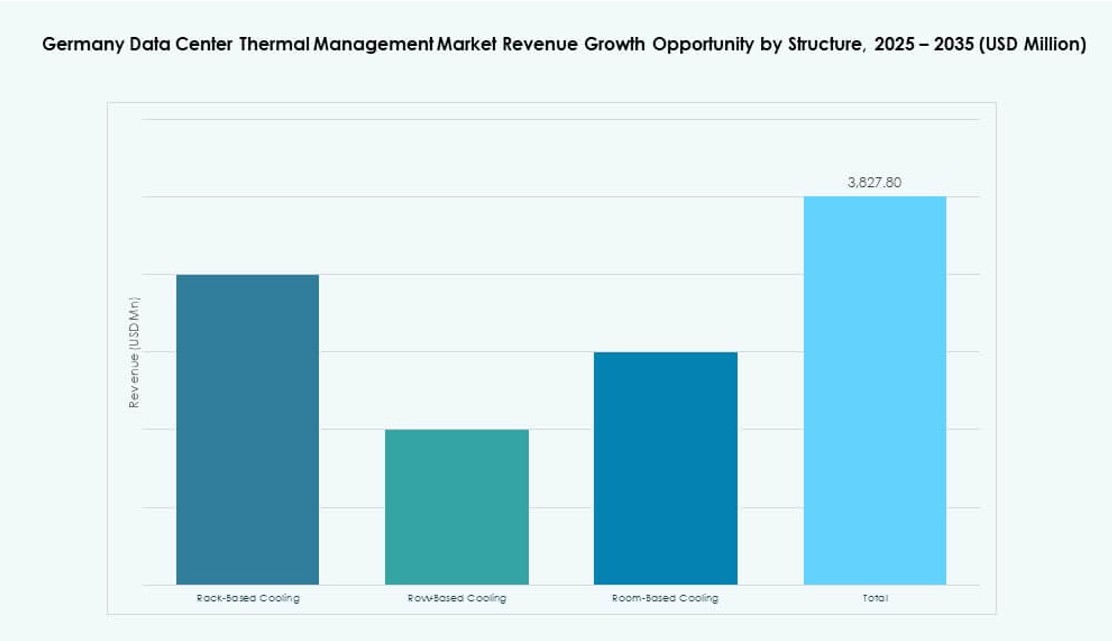

By Structure

Room-based cooling remains common in legacy setups, but row-based and rack-based solutions are gaining preference. Rack-based systems support liquid cooling and high-density workloads. The Germany Data Center Thermal Management Market shifts toward modular cooling with rack and row adoption. These setups offer better efficiency and control compared to traditional room-wide air handling.

Regional Insights

Frankfurt Leads with Over 45% Share Driven by Hyperscale Cluster and Interconnection Density

Frankfurt dominates the Germany Data Center Thermal Management Market with its concentration of hyperscale and colocation facilities. The city offers high interconnection density, favorable fiber infrastructure, and direct access to DE-CIX. Thermal systems in Frankfurt facilities focus on low-PUE and green energy integration. The region sees rapid adoption of liquid and hybrid cooling due to workload intensity. Investors prioritize Frankfurt due to demand certainty and infrastructure readiness.

- For instance, Equinix FR5 in Frankfurt provides N+1 cooling redundancy with approximately 3 MW cooling capacity. The facility uses advanced air containment to support efficient airflow and high-density deployments.

Berlin and Munich Account for 30% Combined Share with Strong Growth in AI, Research, and Cloud Hubs

Berlin and Munich are emerging growth centers, together holding around 30% market share. These cities attract enterprise and research workloads, particularly in AI and biotechnology. Their data centers adopt modular designs and compact cooling systems for retrofits. The Germany Data Center Thermal Management Market supports expansion in these zones through tailored cooling technologies. Urban zoning and limited space encourage row-based and sealed cooling formats.

- For example, Virtus Data Centres broke ground on its Berlin Marienpark campus in 2025, which will include four buildings totaling 57.6 MW of IT load across 19,000 sqm. The project is designed with a PUE target below 1.2 through efficient cooling systems and supports sustainable waste heat reuse into the local district network.

Rural and Border Regions Hold the Remaining 25% Share with Rise in Edge and Green Data Infrastructure

Smaller towns and rural zones near borders are adopting edge data centers for telecom and logistics needs. These areas represent 25% of the Germany Data Center Thermal Management Market. Operators choose these regions for renewable energy access and lower real estate costs. Cooling strategies focus on passive or free cooling using favorable climate conditions. Waste heat reuse and district heating integration are more feasible in these locations. These zones support distributed computing models across industries.

Competitive Insights:

- Vertiv Group Corp.

- Schneider Electric

- Stulz GmbH

- Rittal GmbH & Co. KG

- Airedale International Air Conditioning Ltd.

- Daikin Industries Ltd.

- Delta Electronics, Inc.

- Siemens AG

- Johnson Controls International plc

- Mitsubishi Electric Corporation

The Germany Data Center Thermal Management Market features strong competition between global infrastructure giants and regional specialists. Vertiv, Schneider Electric, and Stulz dominate with comprehensive thermal portfolios and tailored modular solutions. Rittal and Siemens drive local adoption through integrated systems and energy-efficient products. Air-based cooling systems remain a staple, but rapid growth in liquid and hybrid cooling technologies is reshaping vendor strategies. Companies focus on AI-based optimization software, compact liquid modules, and edge-ready designs to align with changing data center demands. It shows growing investment in service innovation, retrofit capability, and green certifications to meet Germany’s sustainability targets. Partnerships and product innovation define long-term positioning.

Recent Developments:

- In November 2025, Delta Electronics, Inc. formed a global strategic partnership with Siemens to deliver prefabricated modular power solutions, including advanced UPS, batteries, and cooling systems tailored for hyperscale AI data centers, with potential applicability in Germany.

- In November 2025, Eaton Corporation signed a definitive agreement to acquire Boyd Thermal for $9.5 billion, enhancing its liquid cooling portfolio to address escalating thermal challenges in high-density data centers.