Executive summary:

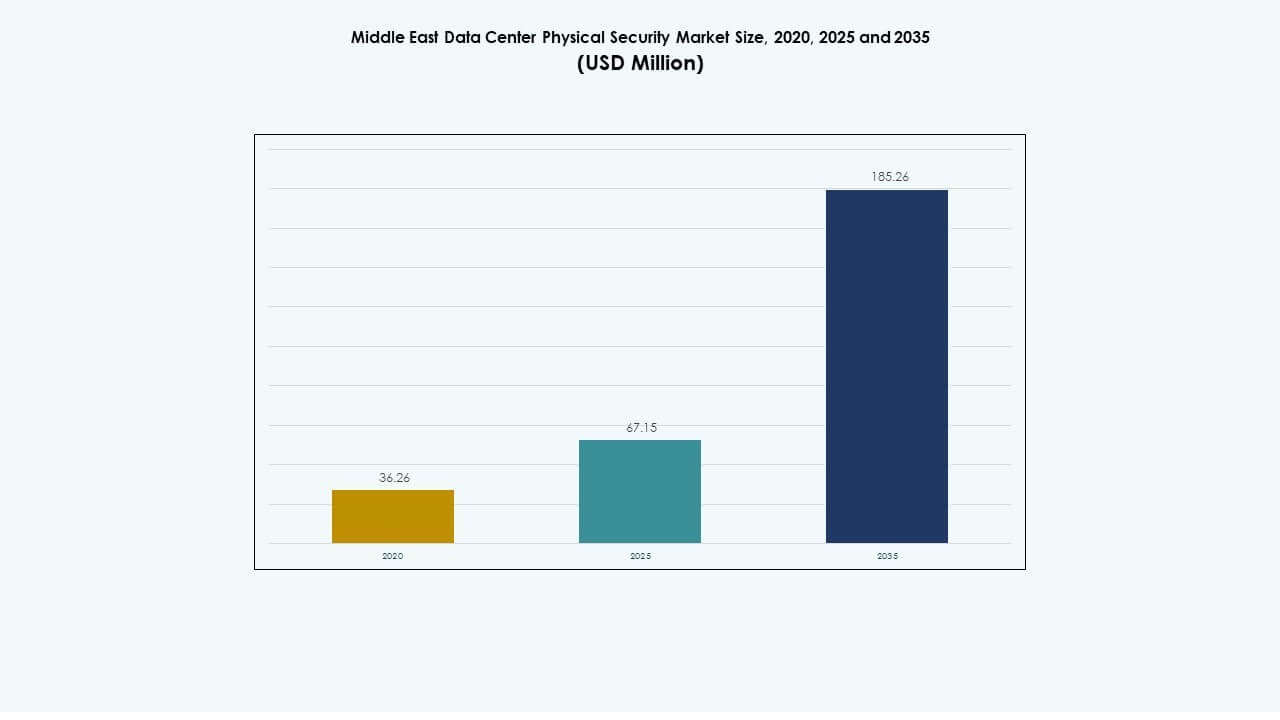

The Middle East Data Center Physical Security Market size was valued at USD 36.26 million in 2020 to USD 67.15 million in 2025 and is anticipated to reach USD 185.26 million by 2035, at a CAGR of 10.57% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Middle East Data Center Physical Security Market Size 2025 |

USD 67.15 Million |

| Middle East Data Center Physical Security Market, CAGR |

10.57% |

| Middle East Data Center Physical Security Market Size 2035 |

USD 185.26 Million |

Strong demand for secure digital infrastructure drives market expansion across the region. Rising investments in hyperscale and colocation facilities accelerate the need for integrated surveillance and biometric access systems. Enterprises focus on AI-based monitoring tools that improve threat detection and operational efficiency. Growing alignment with international security standards strengthens investor confidence. The Middle East Data Center Physical Security Market serves as a strategic segment for both technology vendors and regional infrastructure developers seeking scalable protection systems.

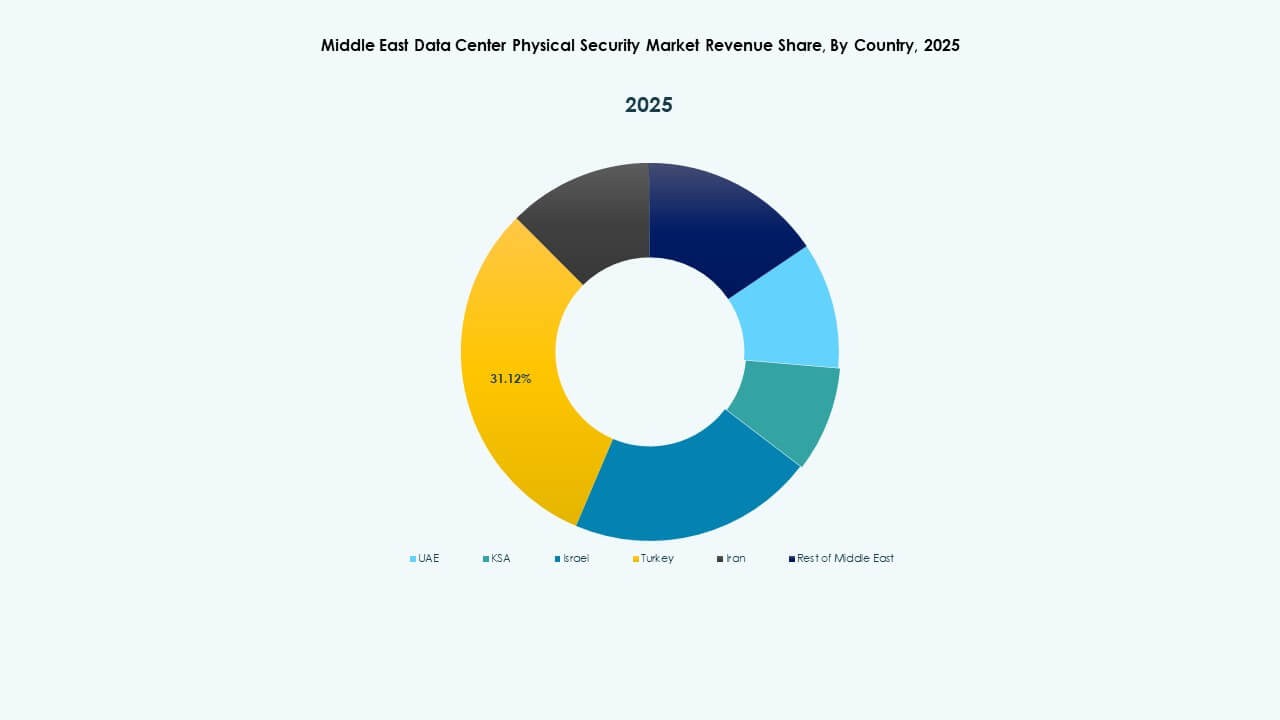

The United Arab Emirates and Saudi Arabia dominate the market, supported by government-backed digital transformation and large-scale data center investments. Qatar and Bahrain show increasing deployment in colocation and enterprise facilities. Israel contributes through advanced R&D in biometric and AI-driven surveillance. Turkey and other emerging economies demonstrate steady growth due to expanding internet penetration and cloud adoption. Regional leadership stems from policy stability, energy availability, and strategic geographic connectivity.

Market Drivers

Market Drivers

Rising Adoption of Advanced Physical Security Technologies

The Middle East Data Center Physical Security Market gains momentum from the rapid integration of AI-enabled surveillance, biometric authentication, and sensor-driven access systems. Governments enforce data protection laws that mandate strong physical and digital safeguards. Data centers adopt machine learning analytics to identify intrusions in real time. Edge computing and cloud expansion raise the need for scalable protection. Organizations deploy intelligent video monitoring to reduce security breaches. Vendors introduce integrated security management platforms supporting centralized control. AI-based recognition systems enhance operational safety across multi-tenant facilities. Growing smart city projects amplify security investments in critical infrastructure.

- For instance, G42’s Khazna Data Centers in the UAE implement security frameworks aligned with NIST SP 800-53 standards, covering more than 100 security and privacy controls. The facilities follow U.S. commercial-grade protection benchmarks to ensure high compliance and operational resilience across their infrastructure.

Expansion of Hyperscale and Colocation Facilities

Large-scale hyperscale projects in Saudi Arabia, the UAE, and Qatar create higher demand for multi-layered physical security solutions. Operators prioritize advanced entry systems, perimeter barriers, and fire protection infrastructure. Colocation providers expand footprints to serve global clients with compliance-driven operations. Investors target greenfield developments with pre-integrated security automation frameworks. The market benefits from rising collaboration between cloud providers and security system integrators. Facility growth drives demand for modular protection systems that align with international certifications. Continuous construction of new campuses strengthens the need for AI-integrated safety technologies. Businesses view security resilience as a key differentiator in competitive markets.

- For instance, Microsoft and G42 partnered in 2024 to expand cloud and AI infrastructure across the UAE, including new data centers designed to meet TIA-942 certified standards. The collaboration emphasizes secure, high-reliability facilities supporting national digital transformation goals.

Integration of Cyber and Physical Security Frameworks

The convergence of cybersecurity and physical protection defines a major shift in regional operations. Data centers adopt unified control systems linking access, surveillance, and digital security under single dashboards. Security orchestration platforms support cross-functional monitoring across facilities. This integration minimizes response time during unauthorized entry or network threats. Enterprises establish redundancy zones with controlled physical access to critical areas. The Middle East Data Center Physical Security Market benefits from partnerships among cybersecurity vendors and physical security providers. Combined systems help ensure compliance with ISO 27001 and local regulatory standards. Hybrid solutions foster resilience across hyperscale and enterprise environments.

Government Initiatives and Regulatory Compliance

National transformation programs such as Saudi Vision 2030 and UAE Digital Strategy reinforce secure data center development. Authorities impose physical protection measures in new infrastructure projects. Compliance with frameworks like ISO 27001 and TIA-942 drives large-scale adoption of certified access and surveillance systems. Governments fund digital sovereignty initiatives supporting national data centers. Public-private partnerships encourage secure colocation development. Regulatory clarity ensures data localization and access management across industries. This approach improves investor confidence in facility security standards. Businesses prioritize regulatory alignment to maintain service reliability and trust in regional operations.

Market Trends

Market Trends

Growing Implementation of AI and Video Analytics in Security Systems

AI-driven video surveillance emerges as a key trend across the Middle East. Facilities install smart cameras that detect movement patterns and anomalies in restricted zones. AI-based analytics deliver predictive maintenance and threat detection insights. The Middle East Data Center Physical Security Market adopts machine learning algorithms to manage traffic flow and prevent unauthorized entry. Real-time alerts enable faster response to operational risks. Integrators design scalable platforms to handle multi-site management. Automation reduces dependency on manual supervision while improving accuracy. Video analytics also enhance energy efficiency by optimizing surveillance schedules.

Rising Popularity of Modular and Scalable Security Infrastructure

Data centers favor modular security systems supporting phased expansion. Providers deploy flexible access control and monitoring frameworks that integrate with existing IT setups. Modular deployment shortens installation timelines and lowers operational disruption. Facilities in emerging economies prioritize cost-effective scalable designs. The trend supports faster adaptation to capacity growth and regulatory changes. Security vendors introduce plug-and-play solutions with remote management capability. The Middle East Data Center Physical Security Market benefits from this adaptability across colocation and hyperscale projects. Scalable modules ensure sustained security efficiency during continuous infrastructure upgrades.

Increased Focus on Energy-Efficient and Sustainable Security Operations

Sustainability becomes a strategic priority for regional operators. Facilities integrate energy-efficient lighting, power-optimized surveillance, and sensor-based access controls. The shift toward green data centers promotes resource-conscious security solutions. Vendors innovate with low-power camera systems and recyclable hardware. Operators deploy smart facility systems that align with LEED and ISO 50001 standards. Sustainable security aligns with environmental goals and reduces long-term operational costs. The Middle East Data Center Physical Security Market embraces eco-efficient systems that combine reliability and sustainability. Energy monitoring tools track power consumption across critical security equipment.

Growing Investments in Edge Data Centers and Remote Security Management

Edge data center expansion across secondary cities drives need for remote security solutions. Providers implement cloud-based monitoring tools for distributed sites. These systems centralize control across multiple regions. Mobile authentication and IoT-enabled access sensors reduce the need for on-site staff. Edge centers use automated fire detection and AI-driven threat analytics to manage smaller footprints. The Middle East Data Center Physical Security Market gains traction through investment in scalable regional networks. Cloud-managed platforms simplify deployment and lower latency. Remote visibility ensures operational consistency across expanding digital ecosystems.

Market Challenges

Market Challenges

High Capital Costs and Integration Complexity

The integration of advanced physical security systems requires large upfront investment. Many regional operators face challenges aligning new technologies with legacy infrastructure. Multi-layered systems like AI analytics and biometric control demand complex integration. Smaller enterprises struggle with procurement and maintenance costs. Skilled workforce shortages delay deployment and increase project risks. The Middle East Data Center Physical Security Market experiences uneven adoption due to financing constraints. Interoperability issues between vendors limit flexibility in upgrades. Businesses seek modular solutions to minimize financial strain and technical bottlenecks.

Evolving Threat Landscape and Regulatory Pressure

Rapid digital transformation introduces new vulnerabilities in facility protection. Constantly evolving threats require frequent security system upgrades. Regional governments impose strict data sovereignty laws that raise compliance costs. Operators must meet both international and local certification standards. This regulatory duality complicates procurement strategies for global players. The Middle East Data Center Physical Security Market navigates growing scrutiny around cross-border data handling. Maintaining alignment between physical and cybersecurity standards remains difficult. Frequent audits and certification renewals increase administrative workloads and operational delays.

Market Opportunities

Growing Government and Private Sector Investment in Data Infrastructure

Expanding smart city projects and sovereign cloud initiatives generate new investment avenues. Governments fund large-scale data center programs focusing on national resilience. Private players partner with global hyperscalers to build secure campuses. The Middle East Data Center Physical Security Market benefits from these long-term commitments. Investors prioritize certified infrastructure with enhanced perimeter and building access systems. Market expansion aligns with the region’s ambition to become a digital hub. Demand for integrated safety frameworks encourages foreign collaboration and technology transfer.

Innovation in Biometric and AI-Based Access Control Solutions

AI-powered biometrics open fresh opportunities for security enhancement. Facial recognition, fingerprint sensors, and behavioral analytics redefine perimeter protection. Vendors develop AI-based access verification systems to reduce manual supervision. Integration of analytics improves incident response and facility control. Regional operators adopt cloud-hosted authentication for scalable operations. The Middle East Data Center Physical Security Market evolves through continuous R&D and pilot deployments. Technology upgrades support predictive security management and regulatory compliance. Innovation fosters market differentiation and builds trust among enterprises and governments.

Market Segmentation

Market Segmentation

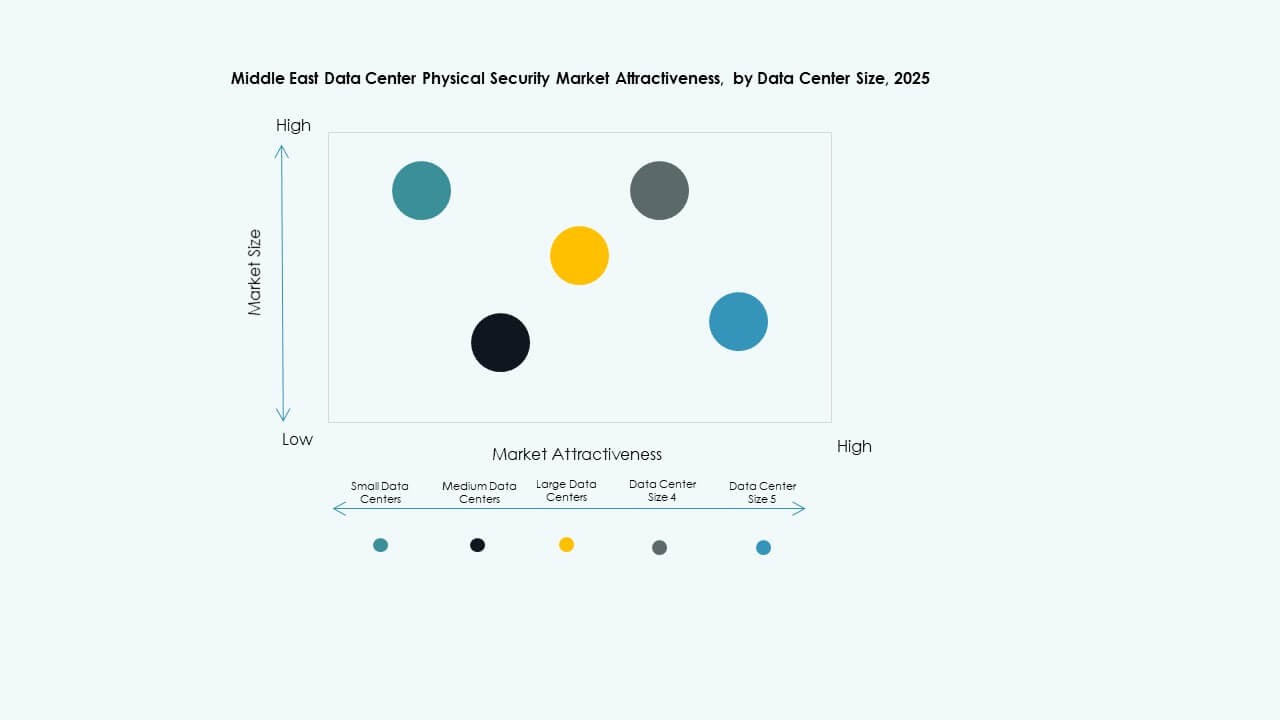

By Data Center Size

Large data centers dominate due to widespread hyperscale developments across Saudi Arabia and the UAE. These facilities demand advanced surveillance, multi-level access systems, and fire safety integration. Medium data centers expand steadily, driven by cloud service providers. Small centers serve niche enterprise needs with cost-efficient monitoring systems. The Middle East Data Center Physical Security Market benefits from scaling infrastructure supporting different business models. Large-scale operations secure major revenue share due to continuous investment in next-generation infrastructure.

By Component

Solutions hold the dominant share, powered by the demand for integrated surveillance, biometric, and detection platforms. Services, including integration and maintenance, follow closely as organizations seek continuous support. Vendors focus on offering end-to-end solutions combining software and hardware reliability. Growing complexity of multi-site operations encourages outsourcing of maintenance tasks. The Middle East Data Center Physical Security Market values service consistency for high uptime and compliance. Service partnerships ensure smoother lifecycle management across regional installations.

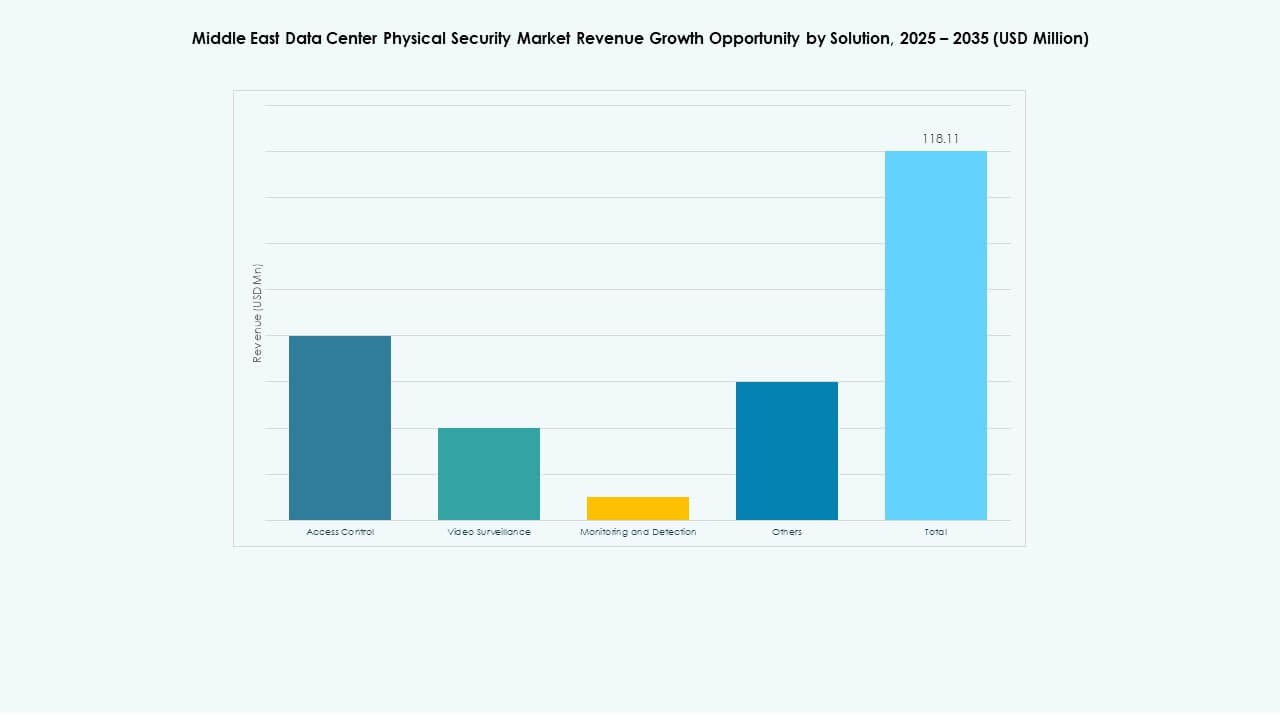

By Solution

Access control remains the leading solution category with strong demand from colocation and government facilities. Video surveillance systems gain traction through AI analytics and smart monitoring tools. Monitoring and detection technologies enhance real-time incident response. Other solutions include fire and intrusion alarms used across mid-sized centers. The Middle East Data Center Physical Security Market sees consistent growth in integrated solutions combining these components. Investment in hybrid surveillance drives modernization of critical environments.

By Services

System integration leads due to complex requirements in large-scale facilities. Consulting services help design secure architectures for compliance. Maintenance and support hold steady importance to ensure continuous monitoring performance. Operators rely on specialized vendors for software updates and component upgrades. The Middle East Data Center Physical Security Market gains stability through strong after-sales support frameworks. Long-term maintenance contracts provide predictable cost structures and reduce downtime.

By Security Layer

Perimeter and building access layers dominate due to their vital role in preventing unauthorized entry. Data hall and rack-level security solutions grow in importance with increasing colocation density. Operators deploy layered protection frameworks to minimize internal threats. Integrated multi-zone monitoring ensures rapid incident response. The Middle East Data Center Physical Security Market thrives on this structured defense approach. Rising hyperscale facilities amplify demand for advanced rack security sensors and smart locks.

By Data Center Type

Hyperscale facilities account for the highest market share with robust infrastructure investments. Colocation centers expand rapidly to meet regional enterprise needs. Enterprise and edge data centers grow due to rising local hosting demand. Edge facilities in remote zones rely on cloud-managed surveillance. The Middle East Data Center Physical Security Market balances growth across these segments. Investment in hyperscale and colocation types drives technology innovation and deployment pace.

By End-User

IT and telecom sectors lead due to expanding cloud adoption and connectivity services. Government and defense segments invest in sovereign data centers to secure national infrastructure. BFSI emphasizes compliance and identity verification systems. Healthcare and retail accelerate modernization to protect sensitive data. The Middle East Data Center Physical Security Market grows with cross-industry digitalization. Each vertical contributes to rising investments in high-security, high-availability facilities.

Regional Insights

GCC Dominates with Over 70% Market Share

The Gulf Cooperation Council region leads the market through large-scale hyperscale and colocation developments. Saudi Arabia, the UAE, and Qatar host multiple Tier III and Tier IV facilities under national digital transformation programs. High government spending, smart city initiatives, and regulatory enforcement support rapid expansion. The Middle East Data Center Physical Security Market benefits from continuous upgrades in access and surveillance frameworks. Investors favor these nations due to robust infrastructure, strategic location, and strong policy frameworks. GCC remains the primary hub for data center construction and physical security innovation.

- For instance, ICS Arabia’s Desert Dragon Data Centers total 187 MW across phases: 65 MW in Riyadh expected by March 2026, 50 MW in Jeddah, and 72 MW in Dammam and Neom planned through 2029

Levant Region Demonstrates Steady Modernization

Countries such as Israel, Jordan, and Lebanon show gradual progress in data center infrastructure. Israel leads through R&D in AI and biometric systems that strengthen regional competitiveness. Jordan invests in colocation centers serving enterprise clients, while Lebanon sees emerging interest in digital hosting. The Middle East Data Center Physical Security Market experiences increasing adoption in this subregion due to IT modernization. Limited energy resources and financial constraints moderate overall growth pace. However, technology partnerships and government support continue to drive market entry opportunities.

North Africa and Emerging Middle Eastern Economies Gaining Momentum

North African nations including Egypt and Morocco show growing investment in regional connectivity and edge computing. Egypt positions itself as a data gateway linking Europe, Africa, and the Middle East. Morocco fosters private investment in secure colocation infrastructure. The Middle East Data Center Physical Security Market expands as emerging economies strengthen their digital ecosystems. Investments in training and regulatory development promote regional competitiveness. Rising demand for cloud storage and security-certified facilities drives sustained momentum across new markets.

- For instance, Egypt serves as a key data transit hub between Europe, Africa, and the Middle East, hosting multiple submarine cable landing stations operated by Telecom Egypt. Systems such as SEA-ME-WE 4 and SEA-ME-WE 5 deliver multi-terabit-per-second bandwidth capacity, strengthening Egypt’s role in regional digital connectivity.

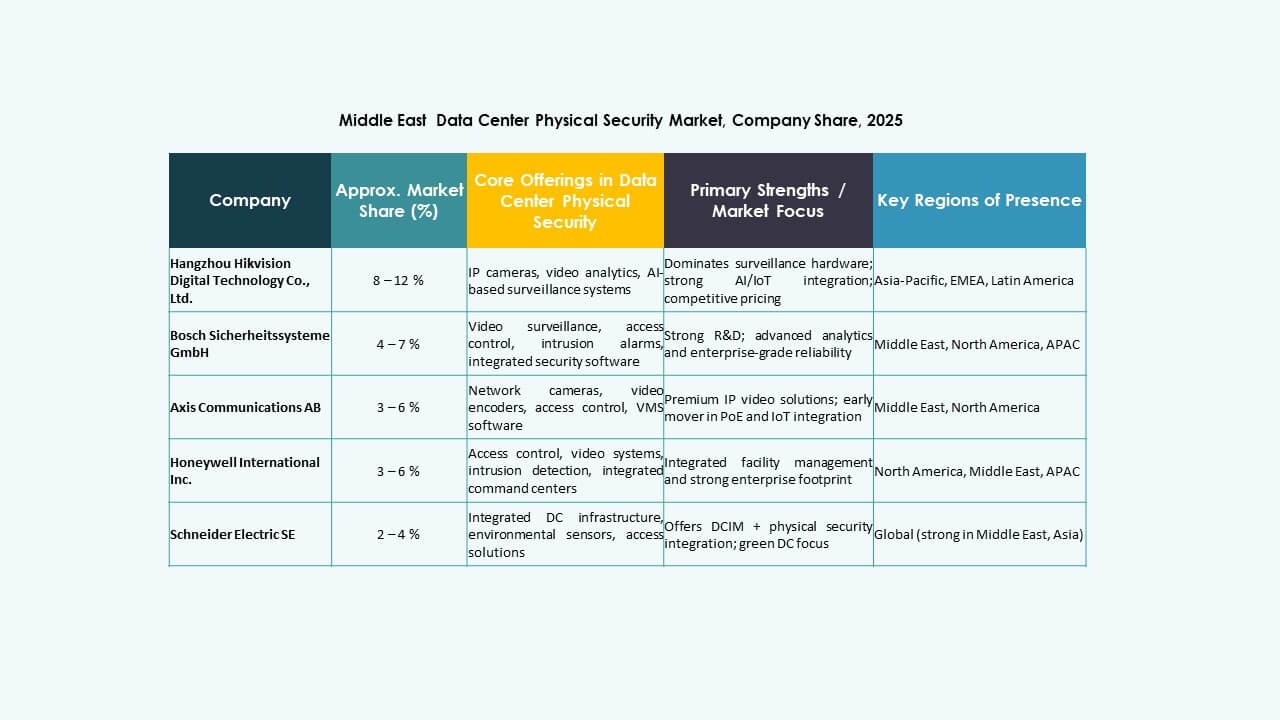

Competitive Insights:

Competitive Insights:

- Axis Communications AB

- Bosch Sicherheitssysteme GmbH

- Honeywell International Inc

- Schneider Electric SE

- Siemens AG

- Johnson Controls International plc

- Cisco Systems, Inc.

- Genetec Inc.

- ABB Ltd

- ASSA ABLOY Group

The competitive landscape centers around established security solution providers expanding presence in the Middle East. Leading vendors offer comprehensive portfolios—surveillance cameras, biometric access, integrated monitoring, and managed services. Companies like Bosch and Honeywell leverage global experience to assure reliability and compliance. Schneider Electric and Siemens deliver integrated infrastructure and energy-efficient security systems. Vendors such as Axis, Genetec, Cisco, and ABB compete by offering scalable video and network-based solutions tailored for large and hyperscale data centers. The market rewards firms that combine robust technology, local compliance knowledge, and service support. Strong competition encourages innovation and pushes vendors to offer differentiated, high-value security packages to attract data center operators and investors.

Recent Developments:

- In October 2025, ASSA ABLOY acquired Kentix GmbH, a German company specializing in monitoring and access control products designed for data centers, enhancing their capabilities in physical security for this sector.

- In April 2025, CPX acquired TSI Tech to bolster its physical security offerings, improve critical infrastructure protection including data centers, and extend its global presence with integrated physical and cyber security solutions relevant to Middle East markets.

- In January 2025, ASSA ABLOY also acquired InVue, a Charlotte-based provider of asset protection and access control solutions, aligning with their strategy to expand globally in access control and asset protection.

- In June 2024, Honeywell International Inc. completed the acquisition of Carrier Global Corporation’s Global Access Solutions business for $4.95 billion, enhancing its building automation portfolio with advanced access control solutions like LenelS2, Onity, and Supra, which support security needs in data centers including those in Spain.