Executive summary:

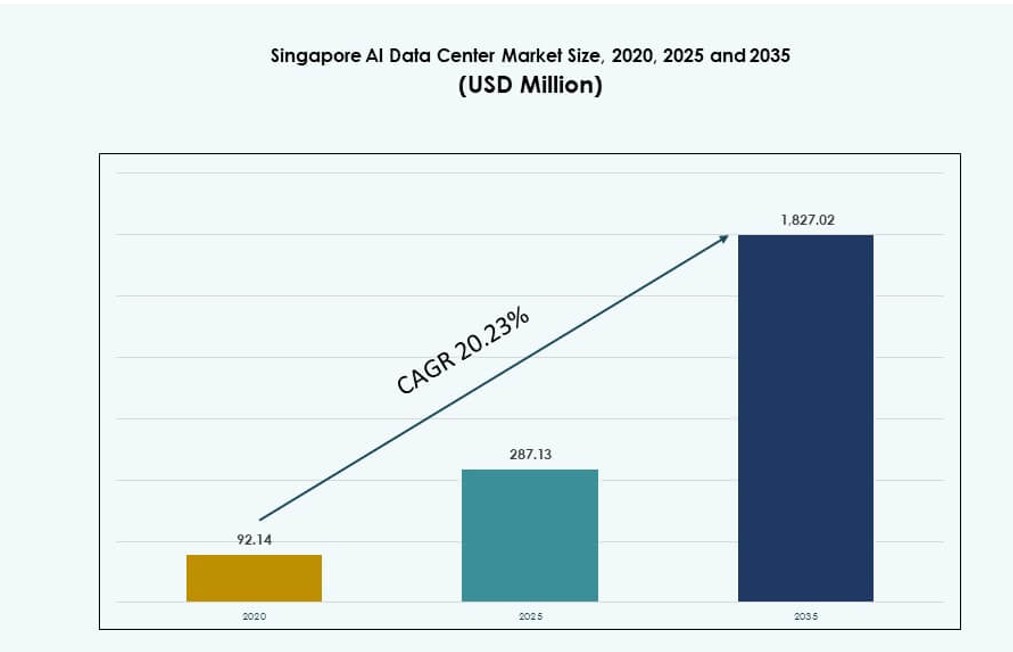

The Singapore AI Data Center Market size was valued at USD 92.14 million in 2020 to USD 287.13 million in 2025 and is anticipated to reach USD 1,827.02 million by 2035, at a CAGR of 20.23% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Singapore AI Data Center Market Size 2025 |

USD 287.13 Million |

| Singapore AI Data Center Market, CAGR |

20.23% |

| Singapore AI Data Center Market Size 2035 |

USD 1,827.02 Million |

Strong government policies, Smart Nation initiatives, and enterprise AI demand are driving the market’s rapid growth. Businesses are deploying high-density compute infrastructure to support large AI models and real-time analytics. Operators invest in liquid cooling, renewable energy integration, and GPU-optimized designs to meet AI needs. Singapore’s strategic location and connectivity make it a preferred hub for regional AI services. Investors see long-term value in its regulatory clarity, scalability, and access to regional markets.

Singapore leads Southeast Asia in AI data center infrastructure due to its digital maturity, subsea cable access, and stable energy policies. It accounts for a dominant share of regional capacity while supporting AI deployment in Malaysia, Indonesia, Thailand, Vietnam, and the Philippines. These emerging markets rely on Singapore’s interconnectivity for low-latency AI applications. This regional integration strengthens Singapore’s leadership and makes it a core base for AI infrastructure expansion in ASEAN.

Market Dynamics:

Market Drivers

AI-Driven Infrastructure Adoption and Accelerated Enterprise Digitalization

AI workloads are reshaping how data centers are designed, operated, and optimized. Enterprises are modernizing IT systems to handle expanding AI demands, including large model training and high-volume inference. Singapore offers stable power, submarine cable routes, and neutral access, attracting global tech giants. Hyperscalers and colocation providers are scaling operations to meet this shift. The Singapore AI Data Center Market supports AI-ready rack density, GPU clusters, and low-latency infrastructure. It enables rapid deployment of AI-based services across finance, healthcare, and logistics. Businesses view it as a strategic location for APAC AI operations. Investors see long-term value in Singapore’s policy stability and network reach. Government support for AI, talent development, and sustainability boosts investor confidence.

- For instance, Google completed its fourth data center facility in Singapore in 2024, bringing total local investments to about US$5 billion. The expansion strengthens Singapore’s cloud infrastructure and enables AI services such as Search and Workspace from its regional cloud region.

Government Support for AI-First Digital Economy and Smart Nation Initiatives

Singapore’s Smart Nation and Digital Economy strategies prioritize AI deployment across critical sectors. National AI programs encourage industry-wide transformation by promoting AI research, public-private partnerships, and regulatory clarity. These policies enhance AI compute access and support advanced data centers. Public agencies integrate AI in services, boosting demand for secure cloud and edge infrastructure. The Singapore AI Data Center Market benefits from coordinated planning between technology and sustainability. Clear guidelines for green building codes, carbon reporting, and energy use efficiency support responsible growth. Developers align facility design with AI-centric requirements and future power scalability. Data center players receive incentives to adopt sustainable cooling and software-defined power systems. This government-led push makes Singapore a model for regulated AI growth.

- For instance, under National AI Strategy 2.0, IMDA partnered with Google on programs like AI Trailblazers to support AI compute infrastructure. This effort aligns with Singapore’s goal to grow its data center hub and drive AI‑led economic development.

Strategic Location, Subsea Connectivity, and AI Workload Interoperability

Singapore sits at the intersection of major undersea cable systems, enabling high-speed data exchange with Asia, Europe, and the U.S. It plays a critical role in global AI data flows. Interconnected data centers ensure low-latency delivery of AI services and real-time decision-making across borders. The Singapore AI Data Center Market gains from its hub status for international cloud, enterprise, and AI ecosystems. It supports federated learning, distributed inference, and hybrid cloud models. Enterprises rely on Singapore to bridge regional compute gaps and manage data compliance. AI workloads spanning multiple geographies benefit from the location’s bandwidth availability and network resiliency. Developers deploy high-density GPU servers in Singapore to anchor AI training. This strategic value drives long-term infrastructure commitments from global players.

Rapid Enterprise AI Adoption and Vertical-Specific Use Case Expansion

Enterprises across finance, manufacturing, retail, and media are deploying AI in core operations. Use cases like fraud detection, visual inspection, predictive analytics, and real-time personalization increase AI computing needs. Singapore’s mature digital economy provides a fertile base for AI deployment. The Singapore AI Data Center Market serves as a critical backbone for these workloads, delivering power, network, and thermal reliability. It enables organizations to experiment, scale, and refine AI systems securely. Colocation providers offer dedicated AI zones with pre-configured racks and scalable power. Tailored service offerings align with vertical-specific AI tools and latency demands. This evolution supports faster go-to-market cycles for enterprise AI projects and encourages ongoing data center investment.

Market Trends

Rise of AI-Specific Zones and GPU-Ready Colocation Configurations

Colocation providers are designing purpose-built zones for AI workloads with specialized power and cooling support. These zones feature high rack density, liquid cooling, and dedicated network fabrics. The Singapore AI Data Center Market sees rising interest in environments that support NVIDIA H100 or AMD MI300-based systems. Operators market AI-ready modules as premium services. GPU configurations require tailored power delivery and airflow strategies. Customers expect flexibility in AI workload scheduling, power provisioning, and data transfer. These upgrades mark a shift from general-purpose to AI-centric colocation. It reflects a trend toward workload-aware facility design and operations. Singapore is positioning itself to become a leader in scalable GPU-as-a-service infrastructure.

Sustainable AI Data Center Operations and Green AI Compute Practices

Singapore’s data center ecosystem is evolving toward sustainability-focused AI infrastructure. Operators use AI to optimize energy usage, airflow, and equipment lifecycle. Liquid cooling, AI-integrated BMS, and modular designs reduce operational carbon. The Singapore AI Data Center Market supports this trend by adopting renewable energy procurement and green building standards. Developers partner with utilities and research labs to improve energy use models. AI compute facilities are expected to balance scale with emissions goals. Carbon-conscious enterprise clients prefer operators with net-zero roadmaps. Sustainability is becoming a differentiator in AI data center procurement. This trend aligns with Singapore’s broader environmental and ESG objectives.

Edge AI and Federated Learning Supporting Low-Latency Applications

The demand for real-time AI services drives investments in edge AI infrastructure. Use cases like autonomous vehicles, smart surveillance, and AR/VR rely on inference near the data source. Singapore supports this trend by fostering micro data centers and high-speed network slices. The Singapore AI Data Center Market sees integration of edge zones within core facilities. Federated learning enables localized AI model updates without central data transfer. These shifts require interoperable infrastructure with AI acceleration at multiple tiers. Telecom providers and cloud players collaborate to deliver edge compute in smart city deployments. It strengthens Singapore’s role in latency-sensitive AI application delivery.

AI-Driven Automation in Facility Management and Predictive Maintenance

Operators adopt AI for predictive equipment maintenance, resource allocation, and security. Facility automation tools analyze sensor data to detect thermal hotspots, airflow inefficiencies, or energy leaks. The Singapore AI Data Center Market supports adoption of autonomous operations to reduce human error. Predictive analytics extends hardware life and improves uptime. AI systems detect anomalies and automate remedial actions. This improves resilience and lowers total cost of ownership. AI-enabled DCIM platforms offer real-time visibility and optimization. Operators compete on intelligent infrastructure and software-defined control. These trends reshape how AI data centers are managed and monitored in Singapore.

Market Challenges

Land, Power, and Cooling Constraints Limiting Expansion Scope and Operational Flexibility

Singapore’s limited land availability restricts large-scale data center expansion. Zoning regulations and green building standards constrain development options. The Singapore AI Data Center Market faces pressure to innovate within limited space. Power availability remains tightly regulated and subject to allocation approval. AI workloads demand dense power provisioning and specialized cooling, straining existing facility designs. Developers must secure long-term power access aligned with AI capacity planning. Cooling system upgrades add complexity and capital cost. Operators must balance performance with sustainability and compliance. These constraints slow hyperscale growth and increase deployment lead times.

Talent Shortage and Complex AI Infrastructure Integration Hindering Scalability

Specialized AI data center deployment needs skilled talent in power systems, AI workloads, and thermal management. Singapore faces talent supply gaps in these areas. The Singapore AI Data Center Market contends with workforce limitations across operations, software, and hardware layers. Integrating AI hardware and orchestration tools into existing facilities presents engineering challenges. Operators must train staff to manage AI-specific configurations and hybrid environments. Vendor lock-in and rapid hardware obsolescence increase operational risk. Clients demand agile infrastructure with evolving workload needs. Addressing these constraints is critical to support scalable, future-ready AI deployment in Singapore.

Market Opportunities

Emerging Demand from Southeast Asia and Enterprise AI Rollouts in ASEAN Markets

Singapore serves as a regional hub for AI services flowing to Indonesia, Malaysia, Thailand, and Vietnam. Enterprises across ASEAN seek AI-enabled platforms but lack local infrastructure. The Singapore AI Data Center Market offers a base for regional AI delivery with proximity and compliance. Multinational firms route AI workloads through Singapore for latency and regulatory advantages. This cross-border demand expands capacity needs and fuels colocation growth. AI platforms integrate into BFSI, logistics, and manufacturing sectors across ASEAN.

Government Incentives and Sustainability Innovation Driving Next-Gen Data Center Builds

Government initiatives support green AI infrastructure, pilot projects, and R&D. The Singapore AI Data Center Market benefits from partnerships that promote sustainability, AI development, and workforce training. New incentive schemes focus on energy-efficient technologies, AI-integrated cooling, and hybrid power setups. These programs reduce capital risks and promote early adoption. Operators experiment with AI-native architecture, making Singapore a testbed for innovative deployments.

Market Segmentation

By Type

The Singapore AI Data Center Market is dominated by hyperscale facilities due to global cloud and AI firms anchoring regional infrastructure in the country. Hyperscale data centers account for the largest share, driven by demand for AI training clusters and distributed workloads. Colocation and enterprise segments are also growing, supported by flexible deployment models and power availability. Edge/micro data centers remain small but gain relevance with low-latency applications and urban deployments.

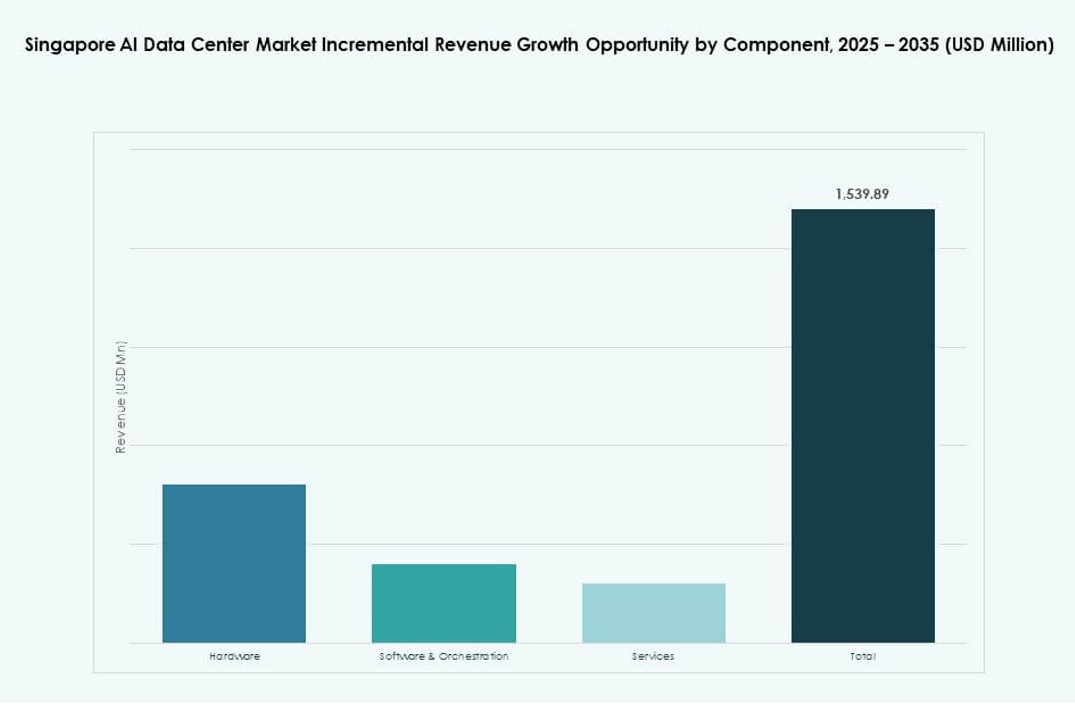

By Component

Hardware dominates the Singapore AI Data Center Market due to the intensive computing power required for AI training and inference. GPU servers, NVMe storage, and high-speed networking equipment drive capital investment. Software and orchestration platforms are gaining momentum, especially for AI workload scheduling and resource optimization. Services are growing steadily as operators offer end-to-end deployment, monitoring, and optimization support for enterprise clients.

By Deployment

Hybrid deployments hold a strong position in the Singapore AI Data Center Market, as enterprises combine on-premise and cloud resources to meet compliance and performance needs. Cloud deployment is growing fast due to public cloud expansion and AI model hosting. On-premise deployments remain relevant for sectors like banking and healthcare, where control and latency are critical. AI adoption accelerates the shift toward dynamic, multi-layered deployment strategies.

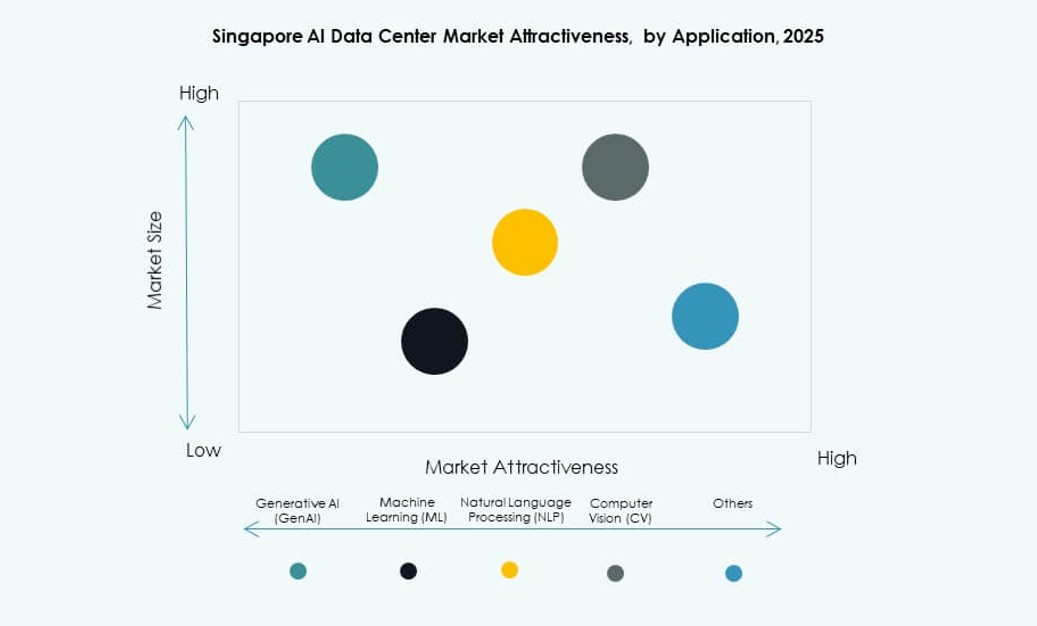

By Application

Machine Learning (ML) holds the highest share in the Singapore AI Data Center Market due to widespread enterprise use across predictive analytics, fraud detection, and automation. Generative AI (GenAI) is rapidly growing, fueled by innovation in content creation, chatbots, and synthetic media. NLP and CV applications support use cases in customer service, surveillance, and healthcare. Other applications include recommendation systems and robotic process automation across various industries.

By Vertical

The IT and Telecom sector dominates the Singapore AI Data Center Market, acting as the foundation for cloud and network-intensive AI applications. BFSI and Healthcare sectors follow, driven by demand for real-time insights, automation, and regulatory-compliant hosting. Retail and media sectors are integrating GenAI and personalization tools, while manufacturing and automotive use AI for process optimization. These verticals shape the demand profile and facility specifications for Singapore’s AI data centers.

Regional Insights

Singapore leads the AI data center market in Southeast Asia, commanding over 60% share of regional capacity. It serves as the primary location for hyperscale and regional colocation hubs. The Singapore AI Data Center Market functions as a gateway for AI services distributed across ASEAN. Strategic location, robust connectivity, and government policy support give Singapore a strong lead.

- For instance, ST Telemedia Global Data Centres operates more than 110 MW of IT load capacity across its Singapore facilities. These data centers support high-density enterprise and AI workloads, reflecting how major operators scale infrastructure to meet rising AI compute demand in the Singapore AI Data Center Market.

Malaysia and Indonesia are emerging subregional hubs, accounting for about 25% of Southeast Asia’s AI-related data center expansion. These countries offer land and power advantages for large deployments. Many AI workloads hosted in Singapore extend into these markets via edge compute. Singapore’s strong peering and subsea links support these operations.

Thailand, Vietnam, and the Philippines represent the remaining 15%, growing steadily due to digitalization and enterprise AI interest. Singapore plays a supporting role in their AI adoption by offering cross-border infrastructure. It enables scalable compute and compliance for AI development across Southeast Asia. This regional integration strengthens Singapore’s AI ecosystem leadership.

- For instance, in October 2025, Singapore announced a 700 MW low-carbon data center park on Jurong Island. The project aims to support next-generation compute and AI workloads using sustainable shared infrastructure and cleaner energy sources.

Competitive Insights:

- ST Telemedia Global Data Centres

- Keppel Data Centres

- Empyrion Digital

- Equinix

- Digital Realty Trust

- Amazon Web Services (AWS)

- Microsoft Azure

- Google Cloud

- NVIDIA

- Hewlett Packard Enterprise (HPE)

The Singapore AI Data Center Market is highly competitive, shaped by local operators and global hyperscale cloud players. ST Telemedia and Keppel dominate the domestic infrastructure space, offering scalable and sustainable AI-ready facilities. Global leaders like Equinix and Digital Realty provide interconnection-rich platforms tailored for AI workloads. Cloud hyperscalers such as AWS, Microsoft, and Google are expanding GPU-optimized infrastructure to support AI model training and inference. Hardware vendors like NVIDIA and HPE supply high-density compute systems crucial to AI deployments. It thrives on strong demand for hybrid infrastructure, regulatory clarity, and proximity to Southeast Asian digital economies. Competitive differentiation centers around energy efficiency, liquid cooling integration, and edge AI enablement.

Recent Developments:

- In November 2025, KKR and Singtel advanced talks to acquire full ownership of ST Telemedia Global Data Centres for over S$5 billion ($3.9 billion), enhancing its AI-driven data center capabilities in Singapore.

- In September 2025, BDx Data Centers announced a strategic partnership with HEXA Renewables to support a 50 MW green energy model for the Singapore and Malaysia grid. The agreement will channel clean power into data center operations. This collaboration emphasizes sustainability and decarbonization of digital infrastructure to support AI workloads in the region.

- In July 2025, DayOne Data Centers broke ground on its first hyperscale AI‑focused data center in Jurong, Singapore. The 20 MW facility aims to meet rising AI demand in Southeast Asia and accelerate the company’s expansion. DayOne also secured renewable energy partnerships and research ties with local institutions to foster sustainable data center innovations.

- In March 2025. STT GDC achieved NVIDIA DGX-Ready Data Center Program certification.This milestone equips their facilities with advanced liquid cooling and rack systems tailored for high-density AI workloads, positioning them to attract premium GPU cluster hosting from global clients.