Executive summary:

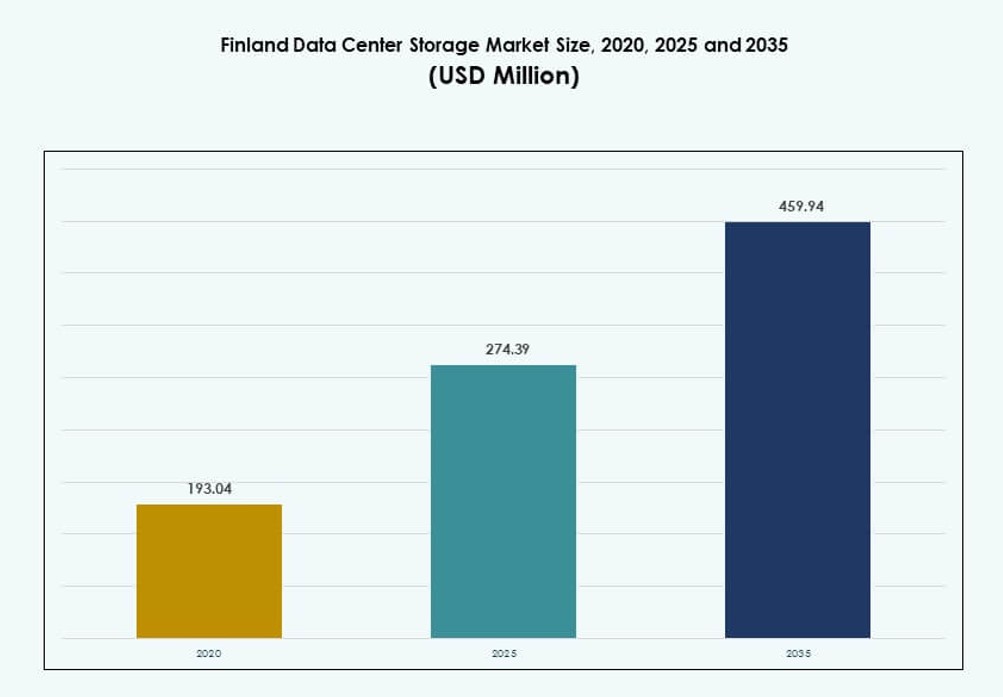

The Finland Data Center Storage Market size was valued at USD 193.04 million in 2020 to USD 274.39 million in 2025 and is anticipated to reach USD 459.94 million by 2035, at a CAGR of 5.24% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Finland Data Center Storage Market Size 2025 |

USD 274.39 Million |

| Finland Data Center Storage Market, CAGR |

5.24% |

| Finland Data Center Storage Market Size 2035 |

USD 459.94 Million |

Rapid digitalization across enterprises and public sector institutions is pushing demand for advanced data storage infrastructure. Businesses in Finland are adopting flash storage, software-defined platforms, and hybrid architectures to manage high-performance workloads. Innovation in edge computing, AI, and data compliance is reshaping storage priorities. Operators are deploying modular and scalable systems that align with green energy standards. This makes the market strategic for both domestic and international investors focused on reliability and sustainability.

Southern Finland, particularly the Helsinki metropolitan area, dominates the storage market due to robust connectivity and power availability. Secondary hubs like Tampere and Turku are expanding with localized deployments to meet growing enterprise needs. Northern regions such as Oulu are emerging due to strategic projects combining data center and energy storage. This regional diversity enhances Finland’s position as a balanced and future-ready digital infrastructure hub.

Market Dynamics:

Market Drivers

Rapid Enterprise Digitalization and the Shift Toward Next-Gen Storage Infrastructure

Finland’s data-intensive industries are scaling up IT workloads, driving higher demand for modern storage. Enterprises are upgrading legacy infrastructure to support cloud-native applications and edge services. This migration accelerates the adoption of software-defined storage and hyperconverged systems. Businesses seek low-latency and high-throughput performance for AI, analytics, and IoT. The Finland Data Center Storage Market reflects a growing need for scalable and flexible solutions. Cloud providers and hyperscale operators are expanding their infrastructure footprints. These trends improve digital readiness for local and global firms. Investors view the country as a reliable market for long-term digital storage investments. Public and private sectors both prioritize resilient and energy-efficient storage models.

Integration of Green Energy and Eco-Friendly Data Storage Infrastructure

Finland’s strong renewable energy base makes it a favorable location for sustainable storage systems. Operators prioritize low-carbon infrastructure and energy-efficient technologies. The use of free cooling, liquid cooling, and low-emission power sources supports sustainable data operations. Data centers in Finland are aligning with the EU’s green digital agenda. The market adopts solutions that balance performance and sustainability goals. This dual focus attracts ESG-focused investors and enterprise clients. It enhances trust in data infrastructure among stakeholders. The Finland Data Center Storage Market gains relevance by offering greener alternatives to other European hubs. The shift reinforces Finland’s position as a responsible and efficient data center destination.

- For instance, Storadera provides S3-compatible object storage from Hetzner’s data center in Finland, which operates on 100% renewable energy. The service targets MSPs and European businesses seeking scalable and compliant cloud storage.

Government Incentives and Strong Connectivity Driving Infrastructure Investments

The government supports data infrastructure through tax incentives and zoning flexibility. These policies attract international colocation and cloud players to expand in Finland. The country also offers reliable fiber connectivity and proximity to key EU markets. Strategic initiatives like the Aurora Line project strengthen cross-border digital routes. These elements make Finland a competitive storage hub for regional and global access. The Finland Data Center Storage Market benefits from reduced latency and improved accessibility. Operators invest in Tier III and IV facilities that meet international security standards. Strong regulatory frameworks and data protection laws add another layer of confidence. These factors boost investor interest in high-availability storage assets.

- For instance, FCDC Corp secured development approval in 2025 for a 66,000 square meter data center campus in Vaasa, supporting scalable storage infrastructure and direct access to Nordic fiber corridors for high-speed enterprise connectivity.

Growing Role of AI, ML, and Edge Workloads Accelerating Storage Adoption

Artificial intelligence and machine learning workloads generate massive data volumes requiring advanced storage. Finland’s tech ecosystem is adopting AI at scale across sectors like healthcare and smart cities. Edge data centers near population centers handle real-time processing and local caching. These changes demand high IOPS storage and intelligent data management platforms. Vendors in Finland deploy flash arrays, object storage, and software-driven platforms. This supports dynamic workloads without compromising speed or capacity. The Finland Data Center Storage Market adapts rapidly to support emerging digital needs. It enables future-ready architecture for enterprise innovation. Demand will continue rising with the expansion of AI and automation technologies.

Market Trends

High Demand for All-Flash and NVM

e-Based Storage to Support Performance-Intensive Workloads

All-flash arrays and NVMe-based storage are replacing traditional drives across data centers in Finland. These technologies deliver faster throughput, improved latency, and energy savings. They support modern applications such as real-time analytics and media processing. Flash storage is being adopted in BFSI, telecom, and government sectors for critical applications. Vendors now offer tiered solutions combining SSD and HDD for cost efficiency. The Finland Data Center Storage Market is shifting toward flash as the default medium. The trend supports green computing targets while enhancing performance. Enterprises increasingly select flash-based storage to meet digital acceleration goals. It drives both modernization and energy efficiency.

Cloud-Native Workloads Influencing Shift to Software-Defined and Hyperconverged Architectures

Cloud-native applications dominate enterprise IT plans in Finland, pushing storage modernization. Software-defined storage (SDS) and hyperconverged infrastructure (HCI) enable scale-out models for public and private cloud. These platforms reduce hardware dependence and improve data agility. IT teams benefit from central management, automation, and real-time scaling. Hybrid deployments combining on-prem and cloud systems are becoming standard. The Finland Data Center Storage Market is evolving toward flexible, workload-centric solutions. Service providers tailor offerings for AI, IoT, and big data use cases. SDS platforms help optimize infrastructure costs while maintaining control. Adoption of cloud-native storage will continue to shape product strategies.

Growing Investments in Edge Data Centers Fueling Localized Storage Demand

Edge computing is gaining traction across healthcare, retail, and industrial applications in Finland. These industries demand low-latency and secure data storage near point-of-use. Edge data centers in urban and remote regions store and process real-time data locally. Storage systems with small footprints and high resilience are in demand. The Finland Data Center Storage Market is adapting to decentralized infrastructure trends. Vendors provide modular, edge-ready storage solutions integrated with edge compute. This decentralization reduces bandwidth pressure and enhances end-user experiences. The trend is supported by smart city projects and 5G rollouts. Edge storage demand is set to increase with wider IoT adoption.

Data Sovereignty, Compliance, and Backup Driving Demand for Localized Storage Models

Enterprises prioritize data localization and backup to meet EU compliance standards. GDPR regulations increase demand for in-country storage infrastructure. Finnish organizations seek secure, compliant storage for sensitive data, particularly in healthcare and finance. Backup and disaster recovery solutions gain relevance amid rising cyber threats. The Finland Data Center Storage Market addresses these needs through localized cloud and private hosting. Vendors offer advanced encryption, data lifecycle management, and regulatory reporting features. Organizations are building resilience through redundant storage nodes and DR sites. The focus on data sovereignty drives growth in secure storage deployments. This aligns with enterprise risk mitigation and legal compliance goals.

Market Challenges

High Cost of Technology Upgrades and Limited Availability of Skilled Workforce

The adoption of advanced storage infrastructure often involves high capital and operational costs. Smaller enterprises in Finland face difficulty upgrading to flash-based or software-defined systems. Managing costs becomes harder with frequent technology refresh cycles. Data centers also face a talent shortage in areas like storage architecture and cloud orchestration. Lack of skilled professionals slows project implementation and optimization. The Finland Data Center Storage Market is affected by this gap in technical capacity. Vendors must invest in local training, support, and managed services. These constraints limit how quickly storage infrastructure can evolve. Market scalability depends on bridging these workforce and cost barriers.

Geographic and Climatic Limitations for Widespread Infrastructure Expansion

While Finland offers natural advantages like a cold climate, its geographic spread poses logistical issues. Remote and rural areas often lack the infrastructure required for large-scale data centers. Fiber connectivity and consistent power supply may not reach all potential locations. This limits the uniform deployment of storage infrastructure across the country. The Finland Data Center Storage Market faces barriers in serving decentralized workloads. It may restrict service availability to Tier II and III cities. Operators also face high costs to build in sparsely populated regions. Expansion is focused in key urban zones, which leads to capacity clustering.

Market Opportunities

Rising Demand for AI-Ready Infrastructure Creates New Storage Growth Avenues

AI and analytics workloads need specialized storage with high throughput and low latency. Finland’s research sector and smart city projects are driving interest in AI-ready storage. Vendors can offer solutions optimized for inference, training, and model management. This opens new opportunities in education, manufacturing, and public services. The Finland Data Center Storage Market can scale by supporting evolving AI deployments. Flash storage, GPU-optimized arrays, and data lakes will see strong adoption. It enhances Finland’s digital competitiveness and opens export potential for storage innovation.

Sustainability-Focused Investors and Green Data Center Growth Fuel Long-Term Prospects

Global ESG investors are looking for low-carbon storage infrastructure in developed markets. Finland’s green energy mix and cold climate give it a competitive edge. Operators can tap these strengths to market sustainable storage as a service. Government support for circular economy and smart energy further boosts interest. The Finland Data Center Storage Market aligns with green digital strategies. Storage vendors can collaborate with green data center providers to co-develop efficient systems. These synergies create new channels for international partnerships and funding.

Market Segmentation

By Storage Type

Traditional storage continues to serve archival and less time-sensitive applications across industries. However, all-flash storage leads the Finland Data Center Storage Market due to faster data throughput and low latency. Hybrid storage systems that combine flash and HDD are growing among mid-sized enterprises seeking cost-performance balance. All-flash accounts for the largest revenue share, driven by its performance in AI, analytics, and real-time applications. Other storage types such as object and block storage are also seeing integration in modern deployments.

By Storage Deployment

Storage Area Network (SAN) systems dominate the market, especially in large-scale enterprise environments needing high availability. SAN provides efficient data block transfer, making it vital for critical applications in telecom and finance. Network-attached Storage (NAS) is preferred in content-driven sectors such as education and media. Direct-attached Storage (DAS) is declining but still used in legacy or edge environments. The Finland Data Center Storage Market is shifting toward hybrid models combining NAS and SAN for flexibility.

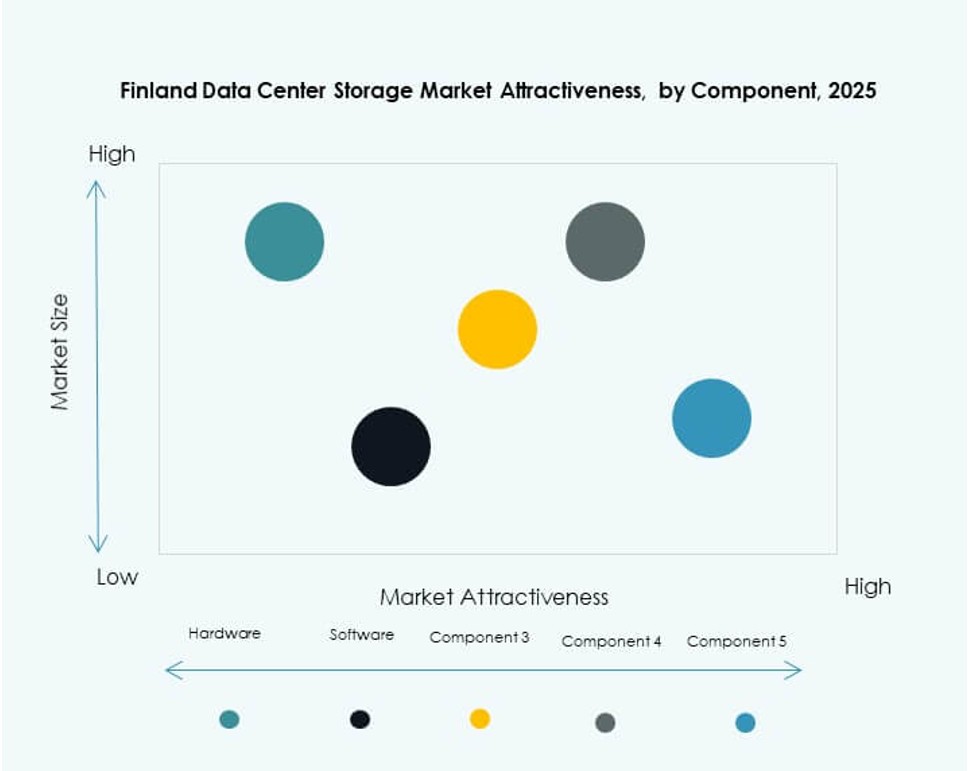

By Component

Hardware holds the major share in the Finland Data Center Storage Market, covering servers, storage drives, enclosures, and controllers. Increasing demand for SSDs and flash modules boosts hardware sales. Software components are growing due to demand for SDS, data management, and automation platforms. The combination of both is vital for building scalable, flexible storage infrastructure. Software also enables centralized control and disaster recovery. Investments in AI-driven storage software are rising.

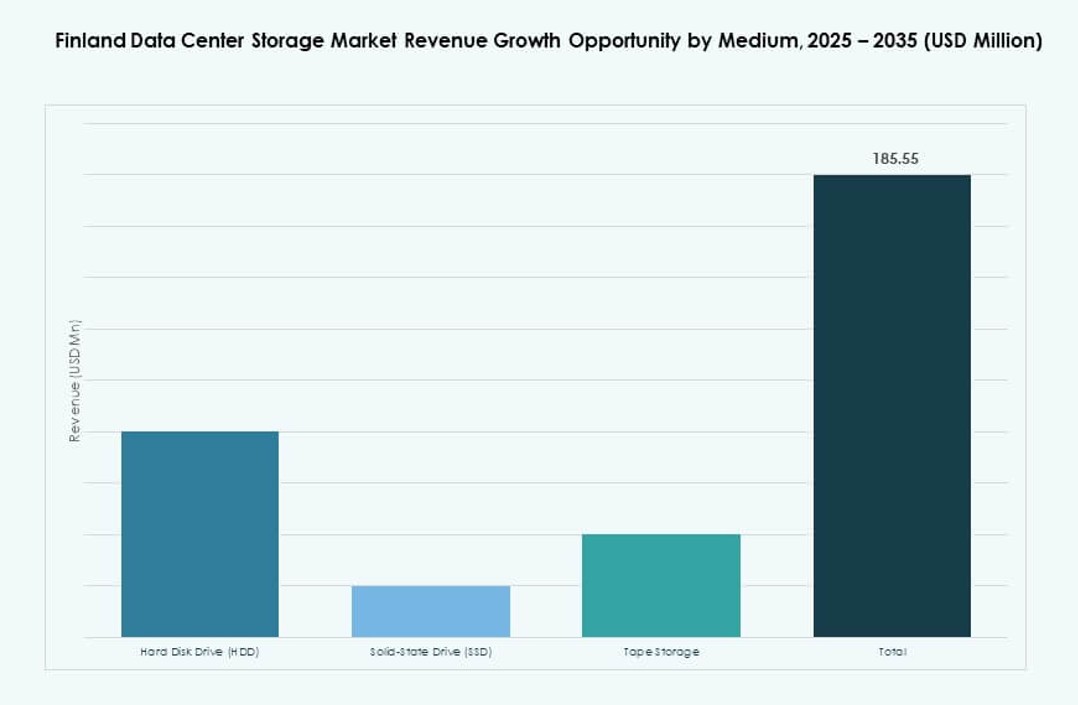

By Medium

Solid-State Drives (SSD) lead the market due to their performance and lower power usage. SSDs are becoming affordable, prompting adoption across new deployments. Hard Disk Drives (HDD) remain important for bulk storage and archiving use cases. Tape storage has niche demand in government and research sectors requiring long-term archival. The Finland Data Center Storage Market increasingly shifts to SSDs for primary workloads. Enterprises focus on storage media that balance speed, endurance, and cost.

By Deployment Model

Cloud-based deployments are gaining share as enterprises migrate workloads to the cloud. On-premises deployments remain relevant for compliance-sensitive and latency-critical workloads. Hybrid models dominate due to flexibility and business continuity advantages. Organizations integrate private and public cloud storage for optimized cost and control. The Finland Data Center Storage Market supports a mix of models tailored to enterprise needs. Growth in hybrid and multicloud strategies drives demand for unified storage platforms.

By Application

IT and Telecommunications hold the largest share, driven by growing data volumes and need for rapid access. BFSI adopts secure and high-performance storage for real-time transactions and analytics. Government agencies demand compliance-ready and energy-efficient systems. Healthcare shows strong growth due to medical imaging and patient record digitization. Other segments include education and manufacturing adopting AI-driven storage tools. The Finland Data Center Storage Market aligns solutions based on specific data sensitivity and performance needs.

Regional Insights

Southern Finland (Helsinki Metropolitan Region) Leads with Over 60% Market Share

Helsinki and surrounding cities account for the bulk of data center storage infrastructure in Finland. The region offers strong connectivity, skilled workforce, and proximity to major enterprises. Major colocation and cloud providers have facilities in Espoo, Vantaa, and Helsinki. It supports mission-critical operations for finance, telecom, and tech sectors. The Finland Data Center Storage Market centers much of its development here due to infrastructure readiness. The metro region remains the primary hub for future expansions.

- For instance, Equinix’s HE3 facility in Helsinki’s Suvilahti district provides 1,050 square meters of net IT space and 1.35 MW customer power capacity, expandable to 1,300 square meters and 3.2 MW.

Western Finland (Tampere, Turku) Emerging as Secondary Data Center Zones

Cities like Tampere and Turku are witnessing steady growth in data infrastructure. These areas benefit from local innovation hubs and university-linked research activity. Enterprises in manufacturing and logistics seek local data storage to support digitalization. The subregion holds around 20% market share and is expanding with new modular facilities. The Finland Data Center Storage Market sees growing interest here due to lower costs and space availability. These cities provide resilience and geographic redundancy.

- For instance, FCDC plans a 66,000 sqm data center campus in Vaasa (nearby Western region), incorporating modular designs for phased capacity growth up to several MW.

Northern and Eastern Finland (Oulu, Kuopio) See Gradual Uptake in Edge and Private Deployments

Northern and Eastern regions are less dense but have potential in edge computing and private IT hosting. Oulu and Kuopio serve as emerging tech centers, particularly for public sector and regional firms. These areas account for roughly 15–20% of the market share. Their colder climate favors energy efficiency, but infrastructure limitations persist. The Finland Data Center Storage Market sees steady but limited growth outside core urban areas. Incentives and improved connectivity may unlock more deployments.

Competitive Insights:

- Tietoevry

- Nokia

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- IBM Corporation

- NetApp

- Cisco Systems, Inc.

- Lenovo Group

- Cohesity, Inc.

- Hitachi Vantara

The Finland Data Center Storage Market includes a mix of local and global players competing on performance, efficiency, and security. Tietoevry and Nokia lead local initiatives, offering tailored solutions for public and enterprise needs. Global companies like Dell Technologies, HPE, and IBM provide modular, scalable platforms supporting flash, SDS, and hybrid storage. NetApp and Cohesity focus on data protection and software-defined storage integration. It shows strong momentum toward all-flash arrays, green data centers, and hybrid cloud models. Competitive advantage often comes from ecosystem partnerships, managed services, and adherence to data localization rules. Vendors invest in edge-ready storage and orchestration tools to meet changing workloads. The market remains highly fragmented, but innovation-led players steadily gain share through local adaptation and energy-efficient designs.

Recent Developments:

- In December 2025, ASP DC acquired a major data center development site in Pori, Finland. In this move, Norwegian data center developer ASP DC announced the acquisition of the CompassForge Real Estate I project site in Pori, Finland, marking its expansion into the Finnish data center landscape.

- In October 2025, 3E Network and Orka Technologies agreed to develop an AI‑focused data center in Finland. Chinese tech firm 3E Network signed a Master Services Agreement with Orka Technologies Oy to jointly build an AI‑ready data center project in Finland.

- In September 2025, AmpTank unveiled plans for a 100 MW data center outside Oulu, Finland. Energy storage developer AmpTank, through its project company Data Tank Nordic Oy, announced plans to build a 100 MW facility in the Mustikkakangas industrial area near Oulu.