Executive summary:

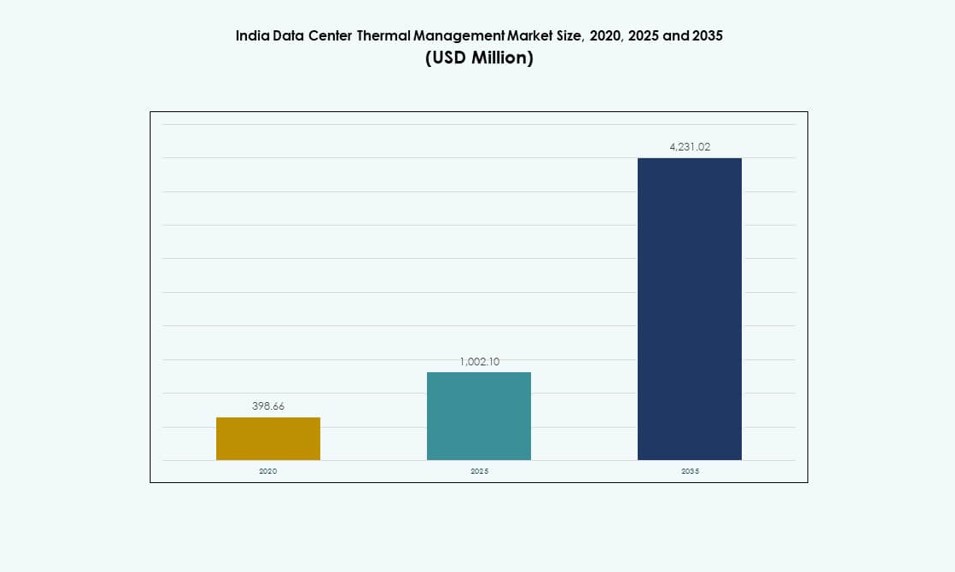

The India Data Center Thermal Management Market size was valued at USD 398.66 million in 2020, increased to USD 1,002.10 million in 2025, and is anticipated to reach USD 4,231.02 million by 2035, at a CAGR of 15.43% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| India Data Center Thermal Management Market Size 2025 |

USD 1,002.10 Million |

| India Data Center Thermal Management Market, CAGR |

15.43% |

| India Data Center Thermal Management Market Size 2035 |

USD 4,231.02 Million |

Growth in high-density workloads, AI model training, and GPU adoption is accelerating the shift toward advanced thermal solutions. Direct-to-chip and immersion cooling gain momentum, while AI-based optimization systems enhance energy efficiency. The rising demand for uptime, sustainability, and SLA compliance is driving rapid investment in smart cooling infrastructure. Strategic interest in this market is high due to its direct impact on operational reliability, power savings, and data center competitiveness across hyperscale, colocation, and enterprise deployments.

West India leads due to strong subsea connectivity and hyperscale concentration in Mumbai. South India, led by Chennai, Hyderabad, and Bengaluru, is growing fast due to IT activity and renewable energy support. North India sees rising demand in NCR for government and telecom workloads. East India is emerging with localized builds in cities like Kolkata, benefiting from regional infrastructure push and data localization policies.

Market Dynamics:

Market Drivers

Rapid Surge in AI Workloads and High-Density Rack Deployments Demands Advanced Thermal Control

The rise in AI model training, HPC workloads, and GPU-based architectures has pushed Indian data centers to support rack densities of 30–60 kW and beyond. This shift requires advanced thermal systems, moving beyond traditional air-cooled CRACs to liquid-cooled or hybrid cooling systems. It makes high-performance thermal management essential to protect equipment, reduce failures, and support uptime. The India Data Center Thermal Management Market has responded with rapid adoption of direct-to-chip and immersion cooling technologies. OEMs and hyperscalers are aligning with newer cooling strategies to meet compute intensity. Businesses investing in AI and HPC clusters now prioritize cooling efficiency as a top infrastructure metric. Equipment reliability under higher thermal loads shapes purchasing strategies. Cooling architecture is now considered a business-critical asset for performance and longevity.

Energy Efficiency and Sustainability Targets Are Driving Next-Generation Cooling Innovation

The need to reduce electricity use from thermal operations drives design changes across India’s hyperscale and colocation data centers. Cooling alone can consume up to 40% of total facility energy, raising pressure to deploy efficient systems. New government and state-level carbon reduction policies reinforce this trend. The India Data Center Thermal Management Market is seeing high adoption of AI-based control systems, liquid loop setups, and modular chilled water units. Data centers increasingly use free cooling and low-WUE systems to meet ESG benchmarks. Companies benchmark facilities against global PUE and WUE leaders to improve credibility. Energy-efficient thermal solutions are now factored into investor decision-making. Optimized cooling directly influences operating costs, offering major cost savings and faster ROI.

- For instance, CtrlS Datacenters operates facilities with a verified PUE of 1.35 through closed-loop cooling and AI-optimized chillers, as certified in their LEED Platinum Mumbai 2 data center.

Data Localization, Government Support, and Digital India Are Fueling Thermal Infrastructure Expansion

India’s data localization rules, combined with Smart Cities and Digital India programs, push for localized hyperscale and colocation buildouts. Government-backed infrastructure pushes have expanded power availability, enabling new thermal deployments. The India Data Center Thermal Management Market benefits from these projects through consistent demand for efficient cooling across Tier I and emerging Tier II cities. Firms like AdaniConneX, Yotta, and CtrlS have ramped up localized capacity with thermal planning integrated from the design phase. Domestic production of thermal components also reduces cost and import dependence. State-level IT parks in Tamil Nadu, Telangana, and Gujarat attract new thermal investments. These trends cement India as a preferred digital hub and thermal systems become a cornerstone of reliability and compliance.

Increased Focus on Uptime, Reliability, and SLA Commitments Accelerates Thermal System Upgrades

Data centers supporting BFSI, telecom, government, and manufacturing sectors require near-zero downtime. SLAs now mandate stricter thermal tolerances, driving upgrades from legacy air systems to precision liquid and hybrid setups. In the India Data Center Thermal Management Market, operators redesign airflow and containment to maintain performance under variable workloads. Businesses also adopt modular cooling to support phased expansion while optimizing capital costs. Remote thermal monitoring and analytics enhance predictive maintenance and prevent unplanned outages. Enterprises view thermal infrastructure as key to data availability and SLA performance. Operators use cooling performance metrics to differentiate in a competitive colocation landscape. These shifts reinforce thermal investment as a strategic lever for client trust and competitive advantage.

- For instance, STT GDC India maintains 99.999% uptime SLAs at multiple locations using N+1 redundant cooling systems with remote thermal monitoring.

Market Trends

Growing Shift Toward Liquid Cooling Systems in New Hyperscale and AI-Centric Facilities

The push toward liquid cooling has intensified across India’s hyperscale facilities, especially in AI and blockchain-based workloads. These require more compact, efficient thermal solutions that conventional air systems cannot match. The India Data Center Thermal Management Market is witnessing interest in direct-to-chip and immersion cooling from major cloud and enterprise players. Suppliers expand offerings to match demand for low-latency, high-performance cooling under 1.2 PUE. Liquid systems are also used in retrofits where rack density upgrades stress existing airflow systems. Facilities using GPUs benefit from lower thermal resistance and footprint with fluid-based solutions. Cooling manufacturers form partnerships with chip vendors for seamless compatibility. Liquid cooling is emerging as a standard for future-ready data centers in India.

Rise in Use of AI and Machine Learning Tools for Thermal Optimization and Predictive Maintenance

Data center operators increasingly apply AI to manage and automate cooling tasks in real time. Smart sensors and software adjust fan speeds, chiller loads, and airflow paths without manual input. The India Data Center Thermal Management Market is now adopting AI-driven DCIM modules and BMS upgrades that cut energy costs and extend asset lifespan. These systems improve visibility and optimize performance based on live workloads. Predictive analytics help reduce equipment failure and schedule targeted maintenance. AI also supports compliance reporting with granular thermal metrics. Operators use machine learning to simulate temperature changes and prevent hot spots. This reduces cooling-related energy use and enhances operational resilience across hyperscale and colocation sites.

Adoption of Modular, Scalable Cooling Systems for Phased Expansion in Colocation and Edge Sites

Phased expansion and flexibility requirements have made modular cooling essential for Indian colocation providers. Operators now deploy scalable cooling systems aligned with IT growth, reducing upfront capex. The India Data Center Thermal Management Market sees modular CRAH/CRAC units, in-row cooling, and containerized cooling pods gain strong traction. These designs allow quick integration with power and IT gear. They also support upgrades without full system downtime. Such setups are popular in Pune, Hyderabad, and Kolkata, where new tenants and workloads emerge dynamically. Edge and micro facilities also benefit from compact modular systems. These trends support faster deployment, improve PUE, and align with distributed data center strategies.

Expansion of Sustainability Certifications Encourages Low-WUE and Free Cooling Deployments

Sustainability benchmarks such as IGBC, LEED, and BEE star ratings are now standard in thermal system design. Certifications demand energy- and water-efficient cooling that minimizes environmental impact. The India Data Center Thermal Management Market shows wider adoption of free cooling, evaporative cooling, and chilled water loops using ambient air in colder climates. Data centers in Bengaluru, Noida, and Manesar integrate rooftop units, economizers, and advanced airflow controls. Free cooling usage is expanding during cooler seasons in north and west India. Some facilities combine multiple methods to balance cost, performance, and sustainability. These efforts also help firms meet investor ESG mandates and support green digital infrastructure targets.

Market Challenges

High Power Consumption and Cooling Efficiency Limitations Constrain Growth of Thermal Systems

Thermal systems remain among the highest energy consumers in a data center, contributing to rising operational costs. Despite upgrades, inefficient thermal designs and poor airflow control persist across legacy Indian facilities. The India Data Center Thermal Management Market must address these gaps to enable sustainable growth. Cooling inefficiencies limit the ability to scale high-density workloads. Power shortages in Tier II cities further strain system reliability. These issues delay expansions or increase reliance on expensive diesel backups. Operators face difficulty balancing IT load with cooling budgets under strict PUE goals. Lack of localized R&D and limited domestic manufacturing raises input costs. These structural constraints reduce flexibility and competitiveness in global colocation markets.

Limited Skilled Workforce and Complex Integration Requirements Delay Advanced Cooling Deployments

Deploying advanced thermal systems like immersion or direct-to-chip cooling involves complex design, integration, and maintenance. The limited availability of trained thermal engineers across Indian regions slows rollout timelines. The India Data Center Thermal Management Market often relies on foreign experts or outsourced consultants for critical deployments. Small and mid-scale operators find it hard to justify such investments. Retrofitting older sites also introduces layout and compatibility issues. Component delays and long lead times affect thermal project scheduling. Coordinating between civil, electrical, and IT teams during cooling deployment adds further complexity. These challenges hinder faster adoption of innovative systems in India’s evolving thermal landscape.

Market Opportunities

Edge and AI Data Centers Present Strong Growth Prospects for Compact and Efficient Thermal Systems

Edge and AI-focused micro data centers are gaining traction in Tier II and remote locations. These setups demand compact cooling systems with high energy efficiency and minimal maintenance. The India Data Center Thermal Management Market can benefit by offering modular and passive thermal solutions tailored for these segments. AI training also accelerates demand for high-density rack cooling, presenting opportunities for liquid-cooled deployments. Vendors who localize products for India’s climate and power constraints stand to gain.

Public-Private Investments and Localization of Cooling Components Unlock New Supply Chain Opportunities

India’s push for electronics and cooling equipment manufacturing under the PLI scheme offers incentives for thermal hardware localization. This improves availability, lowers costs, and reduces dependency on imports. The India Data Center Thermal Management Market is well-positioned to attract component makers, including those focused on chillers, sensors, and fans. Partnerships with global OEMs and Indian infrastructure players can create end-to-end thermal supply chains.

Market Segmentation

By Data Center Size

Large data centers dominate the India Data Center Thermal Management Market due to hyperscale and cloud facility expansion across major cities. They hold the highest market share, supported by high-density racks and complex cooling needs. Medium-sized facilities also grow steadily, driven by demand from IT services and BFSI sectors. Small data centers, while less prevalent, are rising in edge and remote deployments with modular cooling.

By Cooling Technology

Air-based cooling remains dominant due to legacy installations, especially direct air and hot/cold aisle configurations. However, liquid-based cooling is expanding, particularly direct-to-chip systems for AI and GPU workloads. Hybrid solutions are also gaining ground as facilities transition in phases. The India Data Center Thermal Management Market shows increasing interest in phase-change and thermoelectric methods for niche applications.

By Component

Hardware accounts for the largest share of the India Data Center Thermal Management Market, driven by infrastructure investments. Software adoption is growing due to AI-driven optimization and real-time monitoring needs. Services like retrofitting, commissioning, and monitoring support legacy system upgrades and SLA compliance. Demand for integrated solutions spanning all three components is rising.

By Hardware

Cooling units and chillers hold the largest market share in hardware, followed by airflow devices and heat exchangers. Piping and distribution remain essential in liquid systems. Fans and other mechanical components remain vital for airflow management. The India Data Center Thermal Management Market prioritizes efficiency, making high-performance hardware critical for compliance and uptime.

By Software

DCIM dashboards and BMS modules dominate the software landscape, offering centralized thermal monitoring. AI-based optimization software sees fast growth as data centers scale. CFD simulation tools are used during planning and retrofits. The India Data Center Thermal Management Market is investing in predictive software to reduce downtime and improve cooling efficiency across all sizes of facilities.

By Services

Installation and commissioning services lead the services segment, especially for hyperscale and cloud facilities. Preventive maintenance and real-time monitoring services are also rising. Retrofits and upgrades gain traction as existing facilities modernize. The India Data Center Thermal Management Market continues to evolve, with service providers playing a key role in long-term operational stability.

By Data Center Type

Hyperscale data centers dominate thermal demand, followed by colocation/cloud sites. Enterprise data centers contribute to steady demand, particularly in the IT and BFSI sectors. Edge and micro data centers are rising with AI and IoT workloads. The India Data Center Thermal Management Market supports all these types with scalable and tailored thermal solutions.

By Structure

Room-based cooling is still widespread in legacy facilities, but rack-based and row-based systems are rising rapidly. In-row and in-rack cooling support higher densities and modular deployments. These systems are preferred in new AI and colocation sites. The India Data Center Thermal Management Market is shifting toward decentralized cooling designs to improve efficiency and PUE scores.

Regional Insights

West India Leads the Market with Mumbai as the Core Hyperscale and Subsea Connectivity Hub

West India holds the largest share of the India Data Center Thermal Management Market, accounting for nearly 38% of overall demand. Mumbai’s proximity to subsea cable landing stations and financial institutions makes it the dominant data center location. The city’s facilities deploy high-density thermal systems to support BFSI and AI-driven loads. Pune is also emerging, with several edge and enterprise deployments driving modular cooling demand. Infrastructure maturity and availability of skilled workforce continue to support market leadership in this subregion.

- For instance, CtrlS Mumbai DC4 facility supports 36 MW power capacity across 2,936 racks with Rated-4 N+N redundant cooling systems designed for high-density BFSI workloads.

South India Emerges as a Major Growth Engine with High Investments in Colocation and Cloud

South India contributes approximately 32% to the India Data Center Thermal Management Market, led by cities like Chennai, Hyderabad, and Bengaluru. Chennai benefits from cable landing stations and free cooling-friendly climate. Hyderabad sees major investments from hyperscalers and IT companies, leading to demand for scalable thermal infrastructure. Bengaluru drives R&D and software-driven thermal system adoption. Favorable state policies and access to renewable energy boost this region’s growth potential. Regional hubs in Kochi and Visakhapatnam are also gaining traction.

- For instance, Yotta’s NM1 data center in Navi Mumbai is designed for 50 MW IT load and achieves a targeted PUE of 1.4, supporting hyperscale colocation from its initial phase.

North and East India Show Rising Demand with Focus on Edge, AI, and Government Infrastructure

North India accounts for around 20%, while East India contributes nearly 10% of the India Data Center Thermal Management Market. NCR (Delhi, Noida, Gurugram) supports government, telecom, and public cloud workloads, requiring diverse cooling systems. East India’s growth is led by Kolkata and Bhubaneswar, where smaller edge sites and public-sector IT projects drive demand. The market in these subregions is shaped by climate diversity, infrastructure constraints, and cost-sensitive designs. Both regions are critical for future expansion and decentralized deployments.

Competitive Insights:

- Vertiv Group Corp.

- Schneider Electric

- Stulz GmbH

- Mitsubishi Electric Corporation

- Delta Electronics, Inc.

- Daikin Industries Ltd.

- Blue Star Ltd.

- Johnson Controls International plc

- Asetek, Inc.

- Rittal GmbH & Co. KG

The India Data Center Thermal Management Market features strong competition among global thermal technology providers and established Indian infrastructure firms. Vertiv and Schneider Electric lead with integrated cooling ecosystems tailored for high-density and hyperscale needs. Stulz and Rittal focus on precision cooling and modular designs for colocation and enterprise deployments. Mitsubishi Electric and Daikin strengthen their share with energy-efficient chillers and hybrid HVAC units. Domestic firms like Blue Star gain traction through local manufacturing, service support, and government project participation. Delta and Johnson Controls drive adoption of intelligent control systems with AI features. It continues to evolve rapidly, where differentiation comes from energy savings, workload adaptability, service footprint, and modular innovation. Strategic partnerships, AI-enabled platforms, and liquid cooling deployments shape the next phase of competition.

Recent Developments:

- In November 2025, Tata Consultancy Services (TCS), part of the Tata Group alongside Tata Projects, partnered with TPG to invest up to $2 billion in HyperVault, developing liquid-cooled, high-density data centers tailored for AI workloads in India.

- In January 2025, Modine announced plans to open a new manufacturing facility in Chennai, India, to produce Airedale by Modine advanced cooling technologies for data centers, with the facility officially opening in August 2025