Executive summary:

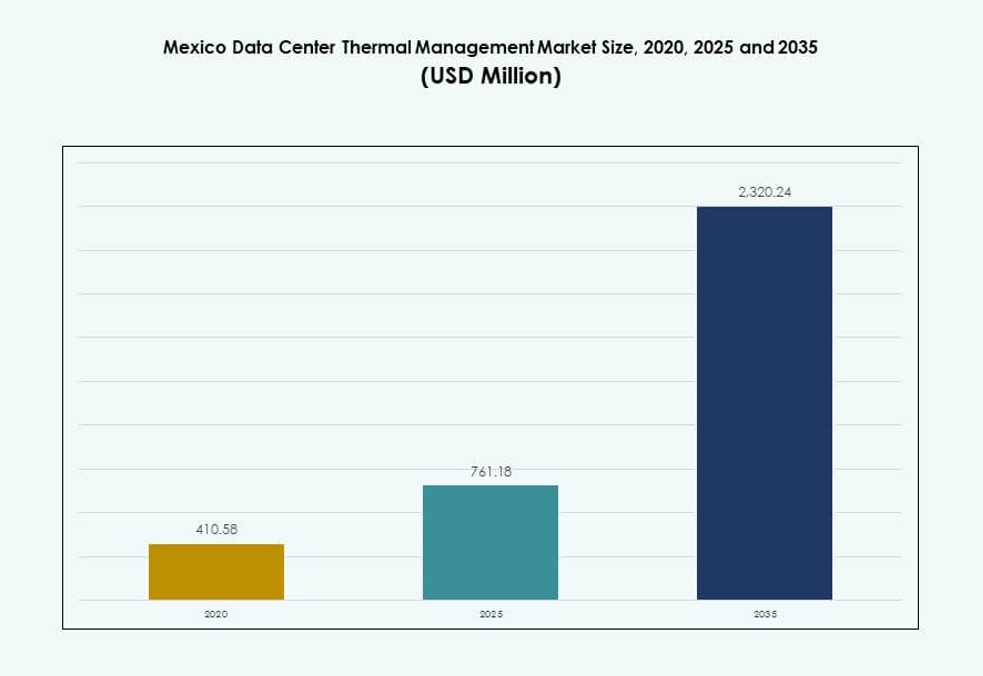

The Mexico Data Center Thermal Management Market size was valued at USD 410.58 million in 2020, grew to USD 761.18 million in 2025, and is anticipated to reach USD 2,320.24 million by 2035, at a CAGR of 11.73% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Mexico Data Center Thermal Management Market Size 2025 |

USD 761.18 Million |

| Mexico Data Center Thermal Management Market, CAGR |

11.73% |

| Mexico Data Center Thermal Management Market Size 2035 |

USD 2,320.24 Million |

The market is driven by rising deployments of hyperscale and colocation facilities, especially in Querétaro and Mexico City. Liquid cooling systems and hot aisle containment are widely adopted for high-density racks. AI-powered thermal optimization and predictive maintenance tools enhance energy efficiency and reduce operational costs. Cloud providers and telecom operators seek scalable cooling solutions aligned with PUE targets. Businesses value these technologies for lowering OPEX and meeting ESG mandates. It becomes a strategic investment area for operators targeting Tier III and Tier IV reliability. Investors also view the market as a thermal innovation hub for Latin America.

Central Mexico leads the market due to power access, connectivity, and infrastructure maturity. Querétaro and Mexico City host major facilities with multi-MW cooling loads. Guadalajara is emerging with growing edge deployments and enterprise demand. Northern cities like Monterrey show potential from cross-border digital operations. Each region adopts distinct cooling designs based on density, land cost, and grid resilience. The regional spread reflects evolving digital transformation priorities across the country. It creates varied opportunities for cooling vendors and integrators.

Market Dynamics:

Market Drivers

Rising Investments in Hyperscale and Colocation Data Centers Across Core Urban Regions

The Mexico Data Center Thermal Management Market benefits from rapid investment in hyperscale and colocation infrastructure. Global operators are expanding footprints in Mexico City and Querétaro, driving high thermal design densities. It supports cooling demand for racks exceeding 20 kW, prompting deployment of advanced systems. Liquid cooling, in-row air containment, and chilled water technologies gain momentum. Facilities aim to reduce energy consumption while maintaining uptime standards. Regulatory incentives and growing digital activity push developers to scale with efficient cooling. This shift enhances infrastructure readiness for AI and edge computing. Global firms see Mexico as a Latin American anchor for cross-border data flow.

- For instance, Equinix expanded its Mexico operations through capacity additions at MX2 and MX3 facilities in Mexico City and Querétaro. MX2 added over 1,000 cabinets during its expansion phase, while MX3 scaled to a total IT capacity of around 14 MW. These developments confirm strong hyperscale and colocation infrastructure growth in Mexico, without disclosed details on rack-level thermal densities or specific cooling architectures.

Adoption of AI-Driven Thermal Management to Improve Efficiency and Predictive Control

AI-led thermal optimization is reshaping data center design in Mexico. It allows real-time performance tuning, identifying hotspots and reducing power use. Intelligent software improves cooling system response times under varying workloads. Operators integrate predictive control to anticipate temperature swings, reducing manual intervention. This improves uptime and reduces operational risk. The Mexico Data Center Thermal Management Market sees demand from firms aiming to hit PUE targets below 1.3. Government efficiency mandates also support AI software deployment. Investors back facilities with such systems due to their long-term cost and energy benefits.

Migration Toward Liquid-Based Cooling Systems in High-Density Server Environments

Liquid cooling systems gain traction in new and retrofit projects. Direct-to-chip and rear-door liquid solutions reduce airflow dependence in compact layouts. Operators deploying GPUs for AI workloads require better thermal handling per square foot. Liquid systems deliver higher heat rejection per unit of energy. The Mexico Data Center Thermal Management Market benefits from rising chip density and rack consolidation. Engineering teams prefer liquid systems for precision and reduced footprint. It helps operators meet ESG targets and grid load limitations. Higher efficiency lowers carbon impact in energy-constrained zones.

Strategic Shifts from Legacy HVAC Toward Modular and Scalable Thermal Infrastructures

The thermal strategy focus shifts from traditional HVAC to modular scalable systems. Facilities adopt rack-based and row-based designs that allow flexible growth. Edge and micro data centers benefit from compact, prefabricated cooling solutions. The Mexico Data Center Thermal Management Market supports distributed infrastructure with site-specific needs. Businesses prefer systems that grow with load without over-provisioning. This ensures lower capital costs and better ROI. Modular designs also reduce construction time and complexity. It improves investment returns in emerging regions.

- For instance, Ascenty’s México 1 and 2 facilities provide a combined capacity of 52 MW with approximately 2,700 racks, supporting large-scale colocation demand in the country.

Market Trends

Integration of Renewable Energy with Thermal Systems for Sustainable Cooling Goals

Operators integrate renewable energy with thermal management for sustainability. On-site solar and green power purchase agreements are paired with efficient cooling. It supports better carbon reporting and energy transparency. Liquid cooling systems benefit from renewable power due to steady energy needs. The Mexico Data Center Thermal Management Market reflects a broader push toward net-zero targets. Companies align cooling systems with low-carbon operations to meet client and regulatory expectations. Sustainability-linked financing adds pressure for green cooling innovation. ESG reporting norms create a strong trend for hybrid energy-cooled facilities.

Rise of Edge and Micro Data Centers Driving Compact Cooling System Deployments

Edge and micro data centers emerge across Tier II cities. These sites need compact, energy-efficient cooling with rapid deployment ability. Rack-mounted chillers and modular in-rack liquid systems dominate such setups. The Mexico Data Center Thermal Management Market sees deployments in logistics hubs, telecom towers, and industrial zones. Cooling systems for these units must operate in varied ambient conditions. Developers demand plug-and-play setups with minimal integration delays. Compact cooling reduces land use and supports lower power footprints. Market shifts reflect digital expansion beyond core cities.

Advanced Simulation Tools Enabling Smarter Cooling System Design and Performance Testing

Thermal simulation tools allow better design and validation. CFD and digital twins support modeling airflow, heat zones, and capacity scenarios. They help reduce over-engineering and optimize component placement. The Mexico Data Center Thermal Management Market benefits from growing adoption of pre-construction modeling. Design teams predict thermal behavior under live loads and emergencies. This cuts rework costs and improves energy profiles. These tools also support retrofit planning and performance upgrades. Vendors offering integrated software gain share in design-build projects.

Focus on High-PUE Sites to Upgrade to Low-PUE, Energy-Efficient Cooling Models

Older facilities undergo retrofit programs to reduce energy waste. Operators replace traditional HVAC with hot/cold aisle containment and liquid systems. The Mexico Data Center Thermal Management Market sees strong interest in upgrades among enterprise sites. Many Tier III and Tier IV facilities still run with 1.8+ PUE values. Firms aim to cut OPEX and improve cooling redundancy. Vendors offer retrofit kits and modular cooling to meet these demands. Upgrading old cooling improves sustainability scores and futureproofs the asset value.

Market Challenges

High Energy Prices and Grid Instability Create Operational Constraints for Cooling Systems

Energy cost inflation pressures thermal budgets in Mexico. Data center operators face frequent power price swings due to grid instability. It impacts large-scale cooling operations that run 24/7. Grid congestion during peak hours limits cooling capacity planning. The Mexico Data Center Thermal Management Market faces reliability concerns during demand spikes. Load shedding and brownouts push operators to invest in backup cooling, increasing capex. Cooling designs must now factor power supply volatility. It raises overall infrastructure cost per rack.

Lack of Skilled Workforce for Liquid Cooling Maintenance and Advanced Software Operations

The skilled labor shortage limits advanced cooling deployments. Maintenance of direct-to-chip and immersion systems requires specialized knowledge. The local ecosystem lacks training programs for precision cooling. The Mexico Data Center Thermal Management Market depends on external experts for complex installations. Software systems like AI thermal control and CFD modeling also face adoption gaps. Operators struggle with staff upskilling, delaying technology integration. This barrier affects facility uptime and deployment timelines.

Market Opportunities

Growing Government Support and Policy Push for Green and Efficient Infrastructure

Federal and state programs support green digital infrastructure development. Tax breaks and zoning support for energy-efficient data centers expand investment appeal. The Mexico Data Center Thermal Management Market can benefit from these incentives. Efficient thermal systems directly qualify for sustainability-linked capital and carbon credits. It helps global firms meet regional compliance and ESG mandates.

Expansion of Cloud and AI Workloads Driving Thermal Demand Beyond Core Hubs

Cloud providers and AI startups expand presence beyond Mexico City. Querétaro, Guadalajara, and Monterrey see strong data center announcements. This pushes thermal demand across a wider geographic footprint. The Mexico Data Center Thermal Management Market gains scope from this decentralization. Cooling firms that offer region-specific designs stand to benefit from early mover advantage.

Market Segmentation

By Data Center Size

Large data centers dominate the Mexico Data Center Thermal Management Market due to hyperscale and colocation growth in Mexico City and Querétaro. These facilities drive high rack densities and consistent thermal loads. Medium-sized data centers follow, mainly from enterprise expansion. Small data centers have slower growth due to limited investment scalability. Demand correlates with IT load concentration and power access.

By Cooling Technology

Air-based cooling systems remain the most widely used, especially direct air and hot/cold aisle designs. Liquid-based cooling is gaining traction, particularly direct-to-chip and immersion systems in AI workloads. Hybrid cooling systems, combining air and liquid, are adopted in high-density zones. Emerging technologies like thermoelectric and phase-change cooling remain niche but show potential in edge environments. Liquid cooling is set to outpace air systems in hyperscale builds.

By Component

Hardware leads the segment, with chillers, piping systems, and airflow devices accounting for the largest share. Software components are growing, driven by demand for AI optimization and DCIM platforms. Services are crucial in upgrades and retrofits, with monitoring and preventive maintenance dominating recurring revenue streams. The Mexico Data Center Thermal Management Market favors complete integrated solutions over standalone components.

By Hardware

Cooling units and chillers form the backbone of thermal setups. Heat exchangers and fans play key roles in rack- and row-level designs. Piping and distribution systems support modular deployment. Other components include actuators, dampers, and flow control valves. The market is driven by efficient integration and redundancy needs.

By Software

AI optimization tools lead due to growing demand for predictive thermal control. DCIM dashboards and CFD simulation platforms support real-time monitoring and design planning. BMS modules help in integrating thermal systems with power and building systems. Software usage increases in hyperscale and colocation facilities with dynamic thermal loads.

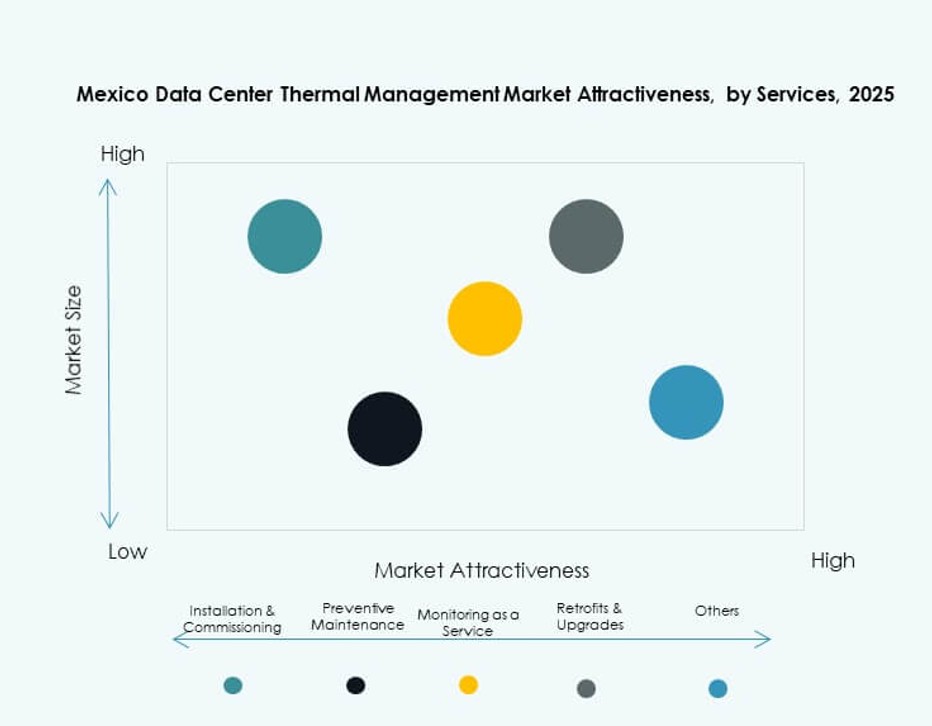

By Services

Preventive maintenance and retrofits see the highest uptake, followed by installation services. Monitoring-as-a-Service grows in multi-site operations for centralized visibility. The market supports bundled services that reduce operational risks. Retrofits are driven by older data centers migrating to liquid and hybrid cooling.

By Data Center Type

Colocation and cloud data centers dominate demand due to their rapid expansion. Hyperscale deployments push cooling technology innovation. Edge and micro centers are emerging segments with niche cooling needs. Enterprise data centers grow steadily but at a slower pace. The Mexico Data Center Thermal Management Market aligns with rising multi-tenant infrastructure builds.

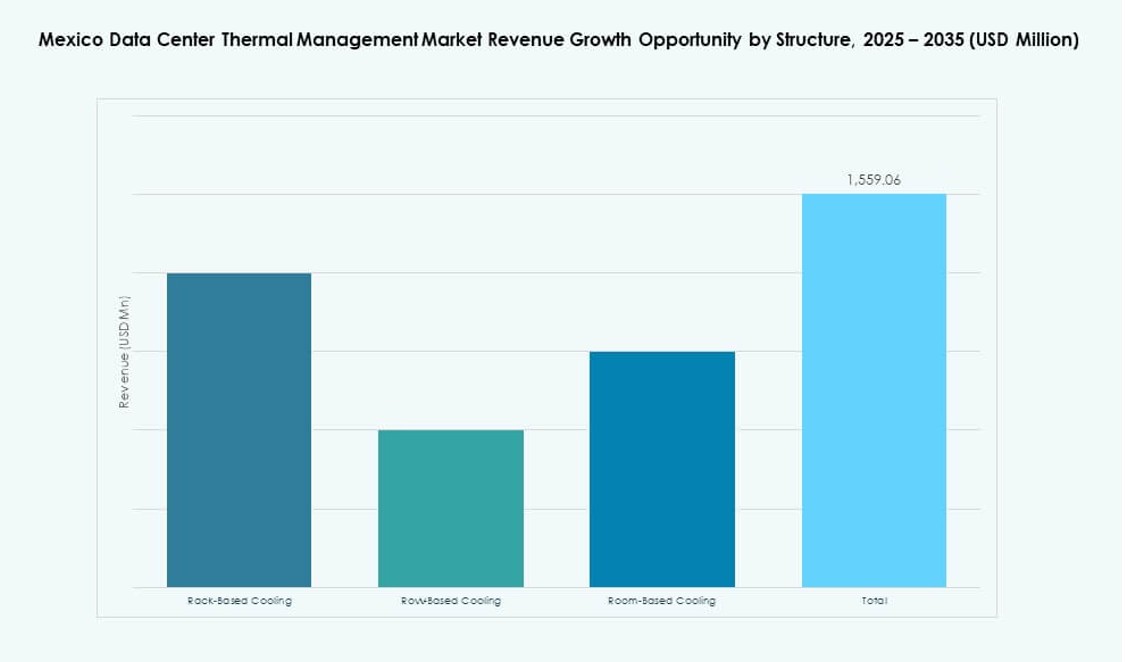

By Structure

Room-based cooling remains the standard for legacy facilities, while row- and rack-based systems grow in newer builds. Rack-based systems support AI and GPU workloads with high thermal densities. Row-based cooling offers scalability and modular deployment. Modern designs favor structure-integrated cooling systems for footprint and efficiency gains.

Regional Insights

Central Mexico Leads the Market with Over 70% Share Due to Power, Connectivity, and Demand

Mexico City and Querétaro dominate the Mexico Data Center Thermal Management Market, together accounting for over 70% of installations. These areas benefit from better fiber connectivity, robust energy infrastructure, and enterprise demand. Querétaro is home to hyperscale campuses from major providers. Cooling demand here is high due to dense server deployment and high power usage effectiveness targets. Proximity to cloud zones and business districts further boosts investment appeal.

- For instance, CloudHQ’s QRO Campus in Querétaro spans 55 hectares, featuring six planned data center buildings with a total critical IT load of 360 MW, supported by a dedicated 400 kV onsite substation reinforcing Mexico’s emergence as a strategic hyperscale destination.

Western Mexico Gains Momentum with Guadalajara Becoming a Secondary Data Center Hub

Guadalajara is emerging as a strong secondary region with 15% market share. It attracts edge and enterprise deployments backed by industrial and telecom demand. The city offers skilled labor and expanding connectivity corridors. Thermal demand in Guadalajara includes modular and row-based cooling systems. It is strategically positioned for west coast operations and digital services expansion. Vendors position scalable cooling portfolios to tap into this fast-growing node.

Northern Mexico Shows Rising Potential Driven by Cross-Border Digital Trade

Monterrey and adjacent northern cities hold close to 10% market share. These areas benefit from industrial activity and proximity to U.S. markets. Colocation providers and manufacturing firms drive IT infrastructure demand. The Mexico Data Center Thermal Management Market in this region requires cooling systems that handle high temperatures and dust exposure. Northern cities also serve as gateways for U.S.–Mexico digital trade zones. Thermal vendors develop robust and reliable designs for harsh conditions.

- For instance, KIO Networks’ MTY1 facility in Monterrey offers Tier III certified colocation with over 5 MW of IT capacity, featuring robust cooling infrastructure engineered to maintain thermal stability in high-temperature regional conditions.

Competitive Insights:

- Vertiv Group Corp.

- Schneider Electric

- Stulz GmbH

- Trane Technologies plc

- Daikin Industries Ltd.

- Rittal GmbH & Co. KG

- Johnson Controls International plc

- Delta Electronics, Inc.

- Airedale International Air Conditioning Ltd.

- Huawei Technologies Co., Ltd.

The Mexico Data Center Thermal Management Market is highly competitive, with multinational firms leading thermal innovation across hyperscale and colocation projects. Vertiv, Schneider Electric, and Stulz dominate due to strong hardware portfolios, retrofit solutions, and modular cooling systems. These vendors integrate AI-based optimization and predictive maintenance software with large-scale deployments. Trane, Daikin, and Johnson Controls serve enterprise and mid-sized centers through energy-efficient air-cooled and liquid-cooled systems. Rittal and Delta focus on scalable rack and row solutions. Huawei enhances its share by bundling power and cooling infrastructure. It reflects vendor strategies that blend performance, sustainability, and fast installation. Partnerships with Mexican operators and cloud firms strengthen local footholds.

Recent Developments:

- In September 2025, Johnson Controls International plc launched the Silent-Aire Coolant Distribution Unit (CDU) platform offering scalable liquid cooling from 500kW to over 10MW for high-density AI data center racks.

- In August 2025, OData inaugurated its fourth hyperscale data center, QR04, also in Querétaro, with the initial 12 MW phase operational and featuring the Delta³ air-cooling technology supporting up to 50 kW per rack.

- In May 2025, OData launched the first phase of its DC QR03 data center in Querétaro, Mexico, introducing Aligned Data Centers’ proprietary Delta Cube (Delta³) cooling solution to the Mexican market for enhanced thermal management.