Executive summary:

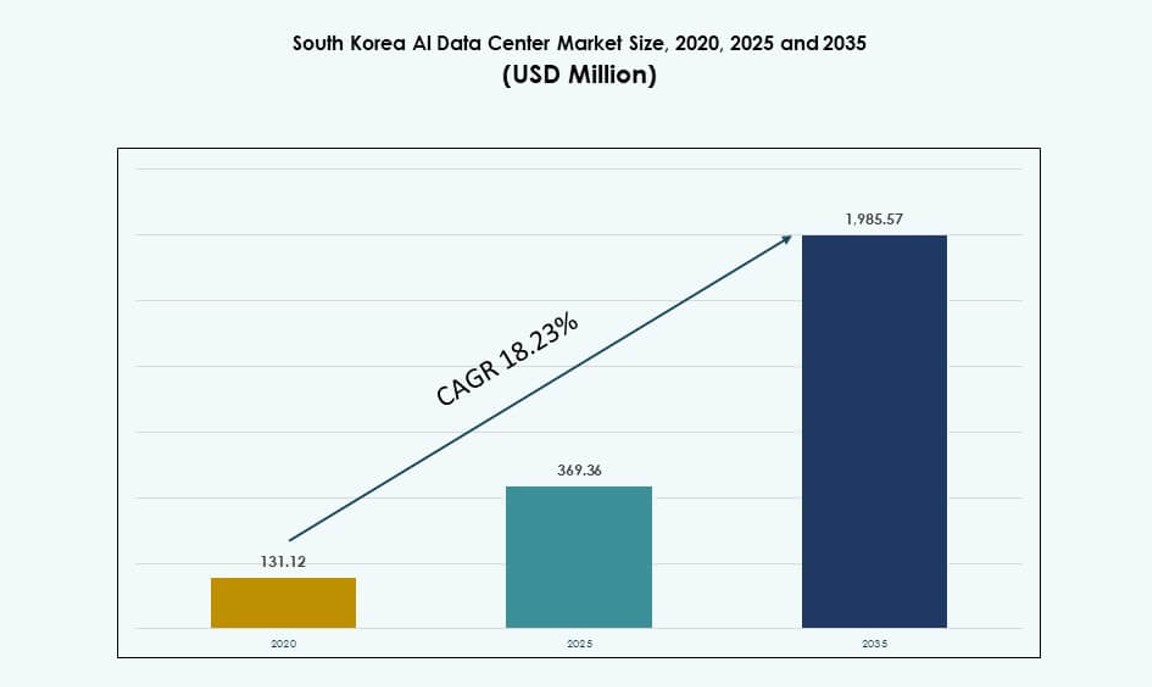

The South Korea AI Data Center Market size was valued at USD 131.12 million in 2020 to USD 369.36 million in 2025 and is anticipated to reach USD 1,985.57 million by 2035, at a CAGR of 18.23% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| South Korea AI Data Center Market Size 2025 |

USD 369.36 Million |

| South Korea AI Data Center Market, CAGR |

18.23% |

| South Korea AI Data Center Market Size 2035 |

USD 1,985.57 Million |

The market is fueled by rapid enterprise adoption of AI applications, sovereign cloud initiatives, and increasing deployment of GPU-accelerated infrastructure. Leading telecom firms and cloud providers are investing in AI-optimized facilities to support machine learning, generative AI, and high-density compute workloads. Liquid cooling, automation, and smart orchestration platforms are transforming facility operations. These shifts are reshaping infrastructure strategies across industries. Businesses and investors see the market as a critical node in Asia-Pacific’s AI ecosystem, with strong policy and commercial support driving forward-looking deployments.

Seoul remains the dominant region due to its dense network infrastructure, enterprise clusters, and data demand. Incheon and Gyeonggi are growing rapidly due to favorable zoning, power availability, and proximity to the capital. Ulsan is emerging as a major hub due to large-scale projects backed by strategic public-private partnerships. Secondary cities such as Daejeon and Busan are also gaining traction as edge and industrial AI deployments expand beyond metro cores.

Market Dynamics:

Market Drivers

Government-Led AI Policies and Digital Transformation Fuel Infrastructure Expansion

South Korea’s AI Blueprint and Digital New Deal programs directly boost AI infrastructure investment. Public funding helps accelerate data center development in AI-focused industrial clusters. The Ministry of Science and ICT supports sovereign cloud and AI infrastructure upgrades. These initiatives strengthen AI model deployment, edge applications, and data localization. The South Korea AI Data Center Market benefits from coordinated public-private digital innovation. It supports local inference capabilities, large-scale model training, and R&D workloads. Strategic policy alignment reduces regulatory delays and encourages green data infrastructure. Government support builds investor confidence and aligns national goals with AI growth.

- For instance, in 2025, South Korea’s Ministry of Science and ICT announced a record KRW 24.8 trillion national R&D budget, prioritizing AI, semiconductors, and digital innovation to strengthen technological competitiveness.

Surging Demand for GPU-Based Clusters and Liquid Cooling Infrastructure

AI workloads demand high-density infrastructure powered by specialized GPU systems. South Korean operators are rapidly adopting liquid cooling to manage heat from AI chips. Enterprise AI deployments and hyperscale workloads rely on high-performance compute clusters. Market players are expanding rack power capacity beyond 30 kW per rack. Liquid cooling systems are becoming standard for supporting AI training and inference models. The South Korea AI Data Center Market supports thermal innovation and power optimization. Equipment upgrades are aligned with sustainability goals and net-zero ambitions. Strategic focus on advanced hardware supports hyperscale buildouts and edge deployments.

Enterprise Cloud Shift and Adoption of Hybrid AI Workloads

South Korean enterprises are transitioning to hybrid AI cloud environments for scalable compute access. On-premise data centers are integrating with public and sovereign AI clouds for seamless deployment. Hybrid architecture supports security, latency, and compliance requirements. Enterprises in sectors like finance, telecom, and healthcare are accelerating AI adoption. These workloads demand both centralized training and localized inference environments. The South Korea AI Data Center Market enables flexible AI workload orchestration. It helps meet cross-industry demand for hybrid AI deployment. Strategic shifts in enterprise infrastructure drive long-term market stickiness.

5G, Edge Computing, and Smart Infrastructure Integration

The integration of 5G and edge computing reshapes South Korea’s digital infrastructure. Telcos and data center operators collaborate to support AI inference at low latency. Real-time AI processing is crucial for smart cities, autonomous systems, and industrial automation. Edge-ready facilities are deployed across metro and Tier-2 regions. The South Korea AI Data Center Market links national AI goals with edge AI scale-up. Network latency reduction improves AI workload efficiency and responsiveness. 5G connectivity enhances last-mile performance and data pipeline efficiency. This shift supports distributed AI compute models and unlocks location-driven applications.

- For instance, in August 2025, KT launched South Korea’s first commercial AI-powered RAN trial on its live 5G network in Naju, using Nokia’s ReefShark-based base stations to enable real-time AI-based channel estimation and improve edge performance.

Market Trends

Emergence of Sovereign AI Cloud Platforms Anchored in Domestic Infrastructure

South Korea is prioritizing sovereign AI clouds to protect data sovereignty and national security. Domestic hyperscale players are developing sovereign AI platforms backed by local infrastructure. These clouds support compliance with South Korean data protection laws. Sovereign frameworks enable government and defense AI model hosting. The South Korea AI Data Center Market aligns infrastructure with geopolitical data control. Sovereign clouds create trusted environments for sensitive AI workloads. Demand is growing from BFSI and healthcare sectors for compliant compute zones. It creates a differentiated layer in the national cloud ecosystem.

Growth in AI-Optimized Colocation Facilities with High Power Density

Colocation providers are shifting toward AI-optimized designs that support HPC and GPU clusters. Facilities offer 30–50 kW per rack with immersion or direct-to-chip cooling. Clients include AI start-ups, research institutions, and enterprise AI teams. The South Korea AI Data Center Market sees demand rising for modular GPU pods and pre-configured AI nodes. Operators expand sites near urban hubs like Seoul, Incheon, and Daejeon. Colocation providers compete on AI-readiness and interconnectivity. This trend redefines traditional colocation business models and attracts high-value AI tenants. Power and cooling scalability has become a core selling point.

AI Training Workloads Drive Demand for On-Demand Capacity and Cloud Bursting

Model training creates unpredictable spikes in compute and storage needs. South Korean data centers are evolving to support burstable cloud environments for AI. This architecture blends steady-state workloads with elastic AI compute bursts. The South Korea AI Data Center Market supports dynamic capacity provisioning. Cloud-native orchestration and DCIM platforms optimize AI workload scheduling. Enterprises prioritize agility and OPEX control when training models. High-performance nodes are designed to handle compute peaks with minimal latency. Flexibility is key for industries deploying real-time or iterative AI models.

Integration of AI-Driven Automation for Data Center Operations and Monitoring

AI is being deployed to optimize operations within South Korean data centers. AI tools manage airflow, predict failures, and automate energy use. It improves uptime, reduces manual intervention, and enhances power usage efficiency (PUE). DCIM solutions embedded with ML algorithms support real-time system intelligence. The South Korea AI Data Center Market becomes self-optimizing through intelligent infrastructure layers. Predictive cooling, power balancing, and fault detection improve O&M economics. This trend reduces labor overhead while improving SLA performance. Operational AI becomes a value layer within physical infrastructure.

Market Challenges

Land Scarcity, Grid Constraints, and Urban Buildout Limitations

Dense metropolitan areas face critical challenges in land availability for hyperscale data centers. Real estate costs in Seoul and surrounding cities continue to rise, affecting site feasibility. High electricity demand from AI infrastructure puts pressure on local power grids. Energy provisioning timelines often delay project execution. The South Korea AI Data Center Market faces difficulty scaling capacity in constrained urban zones. Permitting and environmental approvals take longer in Tier-1 locations. Power-intensive AI clusters require specialized energy infrastructure that many existing zones lack. Location planning becomes a bottleneck for AI facility expansion.

Workforce Limitations and Regulatory Gaps for AI-Specific Infrastructure

South Korea has strong IT talent but lacks specialized AI infrastructure professionals. Engineering, thermal design, and GPU architecture expertise are in short supply. Regulatory frameworks for AI data centers are still evolving. There is no unified code for liquid cooling safety or rack power density above 30 kW. The South Korea AI Data Center Market requires clear standards to streamline approvals. Delays in regulation affect innovation in high-density infrastructure and sustainability. Operator compliance burdens increase due to fragmented standards and overlapping jurisdiction. Talent shortages and unclear policy slow transformation in critical segments.

Market Opportunities

Edge-AI Use Cases and Smart City Infrastructure Accelerate Regional Expansion

Emerging demand from smart transportation, public safety, and factory automation drives edge-AI growth. Municipalities and developers seek local AI inference nodes to serve real-time applications. The South Korea AI Data Center Market enables city-level AI processing at low latency. It helps operators deploy distributed infrastructure across smart regions and SEZs. Demand for AI co-location within telecom and metro fiber hubs is rising.

Global AI Cloud Providers and Semiconductor Players Expand Local Investments

Global tech firms target South Korea for regional AI data center hubs. Strategic location, skilled talent, and 5G penetration attract hyperscale expansions. The South Korea AI Data Center Market gains from supply chain integration with chipmakers and hardware OEMs. AI ecosystem maturity and cloud interconnectivity raise investment confidence. This supports new site development and technology upgrades.

Market Segmentation

By Type

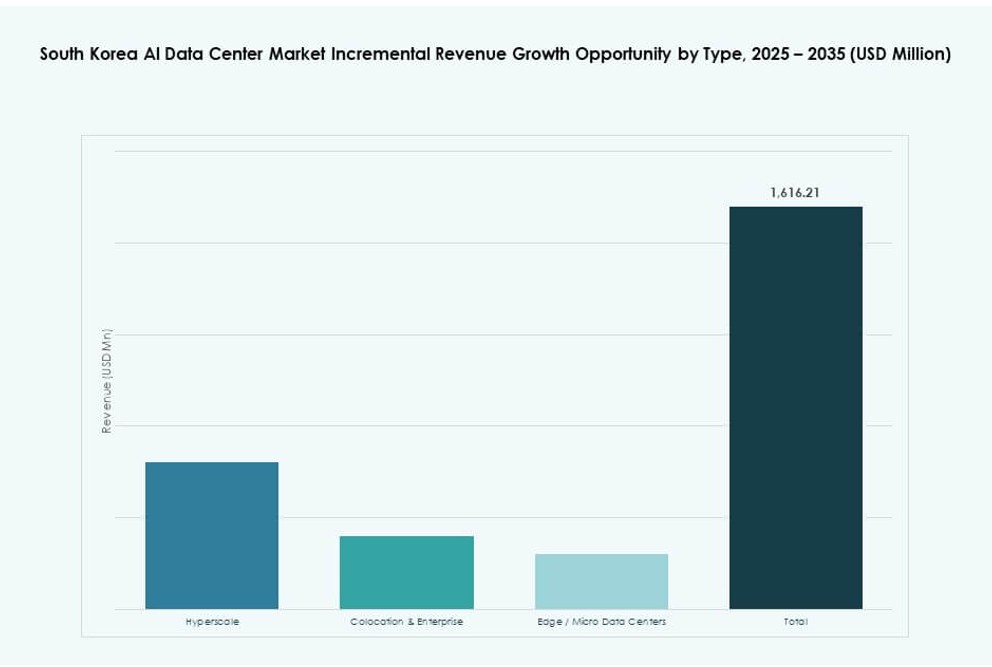

The South Korea AI Data Center Market is dominated by hyperscale data centers due to heavy AI compute demands from cloud giants and telecom firms. These facilities offer over 50 MW capacity with high-density racks for model training and inference. Colocation and enterprise segments also grow steadily, serving regional banks and large corporates. Edge and micro data centers emerge in smart city deployments, offering AI at the network edge.

By Component

Hardware is the largest segment in the South Korea AI Data Center Market due to GPU server clusters, high-performance storage, and liquid cooling systems. Software and orchestration solutions gain traction with the rise of AI workload management tools. Services, including integration, consulting, and maintenance, grow with demand for managed AI-ready infrastructure. Operators rely on hardware-software synergy to support hybrid and sovereign AI platforms.

By Deployment

Hybrid deployments dominate the South Korea AI Data Center Market due to enterprises combining public and private AI infrastructure. This model balances compliance, latency, and scalability. Cloud-based AI deployments grow rapidly, supported by hyperscale availability zones and sovereign cloud push. On-premise deployment continues among telecoms, financial institutions, and government data hubs that prioritize full control.

By Application

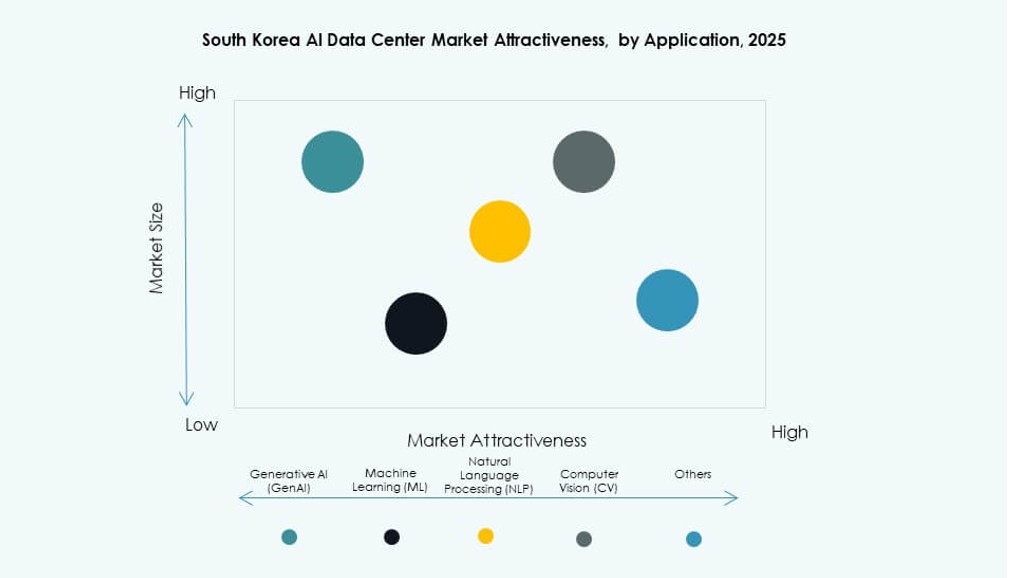

Machine Learning (ML) leads in the South Korea AI Data Center Market as enterprises automate operations and decision-making. Generative AI applications see sharp growth in creative sectors and enterprise productivity. Natural Language Processing (NLP) supports AI customer service and language-based analytics. Computer Vision (CV) use expands in security, healthcare, and smart manufacturing. Other applications include recommendation engines and AI simulation.

By Vertical

IT and Telecom lead the South Korea AI Data Center Market due to large AI infrastructure investments by operators and cloud providers. BFSI is a strong adopter with demand for fraud detection, risk modeling, and intelligent automation. Manufacturing and automotive sectors implement AI in smart factories and autonomous systems. Healthcare and media segments grow through medical AI imaging and content creation. Retail also adopts AI for personalization and inventory automation.

Regional Insights

Seoul Metropolitan Area Holds Over 60% Share with Dense Infrastructure and AI Demand

Seoul, Incheon, and Gyeonggi Province dominate the South Korea AI Data Center Market with over 60% market share. These areas concentrate enterprise headquarters, R&D centers, and network exchanges. Dense connectivity and proximity to users drive AI deployment. Urban zoning limitations and power scarcity challenge large-scale expansions. Still, demand remains steady due to smart city programs and AI-led digital transformation.

- For instance, in December 2024, SK Telecom launched its Gasan AI Data Center in Seoul in partnership with Lambda, featuring 44 kW rack density and deploying NVIDIA H100 GPUs to support GPU-as-a-Service for AI workloads.

Chungcheong Region Emerges as an Expansion Corridor with Favorable Zoning

The Chungcheong region, including Daejeon and Cheonan, holds around 20% share of the South Korea AI Data Center Market. Operators favor this zone for its land availability, power reliability, and proximity to Seoul. The region attracts AI cloud providers and colocation players seeking scalable development zones. Government support accelerates digital infrastructure in these mid-tier cities. Strategic connectivity and smart logistics improve site competitiveness.

- For instance, in November 2023, Naver launched its Gak Sejong data center in Sejong City, featuring a supercomputer cluster with 2,240 NVIDIA A100 GPUs and 3.6 petabytes of storage to support AI cloud workloads across South Korea.

Gwangju and Busan-Ulsan Regions Offer Growth Opportunities for Edge and Industrial AI

Southern regions such as Gwangju, Busan, and Ulsan collectively contribute 15–18% of the market. These areas benefit from industrial base, port connectivity, and renewable energy resources. AI data centers support smart manufacturing, maritime AI, and regional R&D clusters. Operators explore micro data centers and regional edge sites to serve real-time workloads. This segment of the South Korea AI Data Center Market grows with regional digital economy initiatives.

Competitive Insights:

- KT Cloud

- LG CNS

- SK Broadband Data Centers

- Amazon Web Services (AWS)

- Microsoft (Azure)

- Google Cloud / Alphabet

- Meta Platforms

- Equinix

- Digital Realty Trust

- CoreWeave

The South Korea AI Data Center Market features a mix of global hyperscalers and domestic cloud firms. KT Cloud, LG CNS, and SK Broadband lead local infrastructure initiatives with government and telecom support. AWS, Microsoft, and Google expand GPU-rich zones to meet enterprise AI demand. Global AI-native players like CoreWeave and Meta are increasing their local footprint, focusing on high-density training clusters. Colocation specialists Equinix and Digital Realty offer AI-ready campuses with scalable power and liquid cooling. Competition centers around compute density, location efficiency, and AI workload customization. It drives aggressive buildout cycles, deep interconnectivity, and smart cooling innovation across the country.

Recent Developments:

- In November 2025, South Korea agreed to join the UAE’s Stargate AI data centre project, partnering on a global AI campus initiative backed by the United States. The agreement focuses on building computing power and energy infrastructure for one of the world’s largest AI data centre clusters, expanding South Korean influence in AI infrastructure development beyond domestic borders.

- In November 2025, PDG (Princeton Digital Group) announced entry into the South Korea AI data center sector, planning multiple campuses totaling up to 500 MW, beginning with a 48 MW flagship campus near Seoul.

- In May 2025, KT Cloud launched a 10MW AI cloud data center in Yecheon-gun, Gyeongsangbuk-do, South Korea, as part of a public-private partnership, with completion celebrated.