Executive summary:

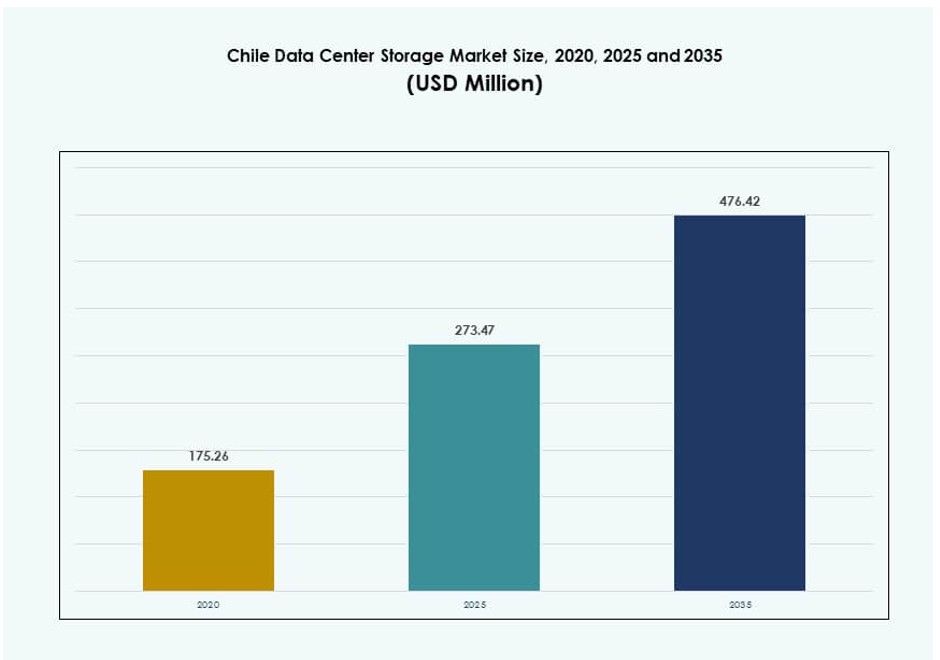

The Chile Data Center Storage Market size was valued at USD 175.26 million in 2020 to USD 273.47 million in 2025 and is anticipated to reach USD 476.42 million by 2035, at a CAGR of 5.65% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Chile Data Center Storage Market Size 2025 |

USD 273.47 Million |

| Chile Data Center Storage Market, CAGR |

5.65% |

| Chile Data Center Storage Market Size 2035 |

USD 476.42 Million |

Cloud-first adoption, growing demand for sovereign infrastructure, and digital transformation across public and private sectors are key market drivers. Enterprises are modernizing IT with hybrid storage platforms to support scalability and compliance. Industries such as BFSI, telecom, and government rely on low-latency, secure data handling for mission-critical operations. The rise of AI, analytics, and edge workloads is accelerating the transition to flash and software-defined storage. The market holds strategic value for global investors looking to tap into Latin America’s stable and expanding digital economy.

The Santiago Metropolitan Region leads the market due to its strong fiber backbone, enterprise density, and proximity to submarine cables. Valparaíso is emerging as a secondary data center zone with resilience potential and lower operational costs. Northern and southern regions are gaining traction for localized services, driven by mining and education sectors. Chile’s geographic diversity supports a distributed model for storage deployment, enabling both central and edge data storage use cases.

Market Dynamics:

Market Drivers

Strong Digital Economy Growth and Enterprise Cloud Adoption Stimulating Storage Investments

Chile’s digital economy has expanded rapidly due to rising cloud services, digital banking, and e-commerce penetration. Enterprises are accelerating cloud migration and hybrid IT models to support scalability. This shift requires high-performance, secure storage systems that can handle structured and unstructured data. It creates demand for both all-flash arrays and scalable software-defined storage platforms. Businesses rely on modern infrastructure for latency-sensitive applications and compliance workloads. Storage systems with advanced analytics and automation tools help reduce operational complexity. Enterprises prefer platforms that integrate with public cloud and AI frameworks. The Chile Data Center Storage Market plays a key role in supporting these enterprise modernization efforts. Storage capacity planning is now critical to long-term digital competitiveness.

- For instance, Entel Chile partnered with AWS to expand hybrid cloud services, leveraging AWS Direct Connect and Local Zones in Santiago to deliver low-latency enterprise storage and cloud solutions across regulated industries.

National Connectivity Improvements and Fiber Infrastructure Supporting Edge Storage Deployment

Chile’s robust fiber optic backbone and submarine cable access provide a strong foundation for storage expansion. National efforts to strengthen 5G and broadband coverage promote edge storage investments across remote areas. Telecom operators are enabling distributed storage solutions to serve rural IoT and video traffic. This reduces latency and enhances user experience for regional workloads. Storage systems deployed at the edge must support real-time processing and localized caching. It fuels demand for compact, rugged, and energy-efficient storage appliances. The Chile Data Center Storage Market benefits from these distributed architecture trends. Government policies promoting regional digital inclusion further drive investments in edge nodes. Storage plays a key role in enabling secure, localized data retention.

Strategic Enterprise Demand for Data Sovereignty and Compliance-Ready Storage Platforms

Growing sensitivity to data privacy has pushed organizations toward onshore storage platforms. Financial, healthcare, and public sector entities need sovereign infrastructure that meets local compliance mandates. This trend supports demand for colocation and private cloud deployments with in-country storage. Enterprises require granular control over data access, retention, and backup policies. The Chile Data Center Storage Market provides secure hosting environments that align with national regulations. Vendors offering encryption, RBAC, and tiered storage gain competitive edge. Storage platforms must also support audit readiness and business continuity planning. The preference for localized control strengthens demand for sovereign-ready storage environments. It reflects the market’s growing role in national digital resilience.

- For instance, BancoEstado updated its information security and cybersecurity policy in 2025 to strengthen protection of customer data and align with Chile’s Personal Data Protection law and Cybersecurity Framework Law

Tech-Driven Industries and AI/ML Workloads Creating Pressure for High-Throughput Storage Platforms

Industries using artificial intelligence, video analytics, and simulation workloads need high-throughput storage. The mining, healthcare, and media sectors generate large volumes of data requiring low-latency access. It drives demand for all-flash storage, GPU-optimized systems, and NVMe-based architecture. Companies are redesigning their storage frameworks to reduce bottlenecks in data pipelines. The Chile Data Center Storage Market supports these innovation cycles with scalable storage solutions. Technology providers offering AI-integrated data management tools are gaining traction. Workload-specific appliances support real-time analysis in scientific and operational use cases. It fuels migration toward high-performance, modular storage systems. This storage evolution is vital for keeping pace with emerging industrial applications.

Market Trends

Shift Toward Hybrid Cloud Storage Platforms Across Mid-Sized and Large Enterprises

Enterprises in Chile are adopting hybrid cloud strategies to balance flexibility with control. Organizations deploy critical workloads on private infrastructure while leveraging public cloud for non-sensitive data. This structure requires seamless storage integration across platforms and APIs. Vendors offering unified data management gain traction among IT teams. The Chile Data Center Storage Market supports this trend through platforms that enable orchestration across storage pools. Demand grows for metadata indexing, tiering automation, and cross-platform snapshotting. Enterprises aim to avoid vendor lock-in while maintaining performance and compliance. It creates a push for software-defined storage with cloud-native interfaces. Growth of SaaS platforms further fuels hybrid adoption.

Rising Adoption of Object Storage for Scalability and Cost Optimization Needs

Object-based storage gains momentum due to its scalability, flexibility, and lower cost per GB. Businesses generating video, image, and archival data seek durable storage that supports massive growth. Traditional file and block storage lack efficiency for these workloads. Object storage supports modern protocols like S3 and integrates easily with cloud services. It becomes the preferred architecture for backup, analytics, and content delivery networks. The Chile Data Center Storage Market aligns with this trend by enabling cost-effective long-term storage. Enterprises leverage object stores for scalable disaster recovery and data lakes. It positions object-based storage as a strategic enabler of digital continuity.

Adoption of AI-Based Storage Management Tools for Automation and Analytics

IT teams increasingly depend on AI-driven storage tools for system monitoring, performance tuning, and cost visibility. These platforms use telemetry and machine learning to optimize capacity planning. Predictive analytics prevent outages by identifying hardware issues early. The Chile Data Center Storage Market embraces these tools for operational efficiency. Businesses want platforms that reduce human error and improve uptime. Storage software with real-time dashboards and anomaly detection is in high demand. AI-integrated storage aligns with broader enterprise automation goals. It reduces manual effort while improving scalability and workload adaptability. Demand for intelligent storage continues to rise across enterprise sectors.

Energy-Efficient Storage Solutions in Response to Sustainability Goals and Cost Pressures

Enterprises face growing pressure to reduce carbon footprints and manage energy costs. Power-efficient storage systems with low thermal output are favored in green data center designs. SSDs and tiered storage reduce energy consumption per IOPS delivered. Chile’s energy pricing structure also incentivizes efficiency in infrastructure decisions. The Chile Data Center Storage Market responds with products optimized for power and space. Vendors highlight Energy Star certifications and carbon-aware data placement features. Demand is strong for platforms that balance performance with sustainability. Organizations align storage choices with broader ESG goals and operational cost savings. It strengthens focus on green storage innovations.

Market Challenges

High Capital Expenditure and Long Procurement Cycles for Enterprise Storage Infrastructure

The cost of deploying advanced storage platforms remains a barrier for many mid-sized enterprises. Flash arrays, AI-ready storage, and hybrid systems involve significant upfront investment. Long evaluation cycles and rigid procurement policies delay adoption. Smaller firms hesitate to commit to long-term vendor contracts. The Chile Data Center Storage Market faces this challenge due to budget constraints and ROI uncertainty. Businesses seek flexible leasing and as-a-service models to reduce capital burden. Vendor financing programs are evolving but remain limited. Price-sensitive buyers need better visibility into total cost of ownership. It slows modernization in sectors with constrained IT budgets.

Shortage of Skilled Workforce for Managing Advanced Storage Architectures and Tools

Managing hybrid and AI-integrated storage systems requires specialized expertise. Chile faces a talent gap in data center engineering and infrastructure automation. Many enterprises lack in-house teams skilled in storage orchestration, cybersecurity, and workload optimization. The Chile Data Center Storage Market is impacted by this skills mismatch. It increases reliance on managed services and outsourcing models. Vendors offer training and certifications, but adoption remains slow. Complexity in multi-cloud and software-defined setups adds to staffing challenges. It limits the pace at which businesses can transition to modern storage architectures.

Market Opportunities

Rise in Digital Government and Smart City Initiatives Expanding Demand for Compliant Storage

Public sector transformation creates demand for secure, sovereign storage platforms. Government agencies require onshore systems for sensitive citizen and infrastructure data. The Chile Data Center Storage Market supports these initiatives with regulatory-aligned infrastructure. It opens opportunities for vendors offering certified, high-availability storage for public cloud and hybrid deployments. Smart city rollouts also drive sensor data storage across urban networks.

Emerging Startup Ecosystem Driving Cloud-Native Storage Consumption

Chile’s tech startup landscape is expanding in fintech, healthtech, and logistics sectors. These digital-native businesses adopt cloud-first strategies with API-driven storage. The Chile Data Center Storage Market benefits from demand for fast-deploying, scalable platforms. Object storage, DRaaS, and tiered models are favored by startups scaling operations. It encourages innovation in pay-per-use and subscription-based storage offerings.

Market Segmentation

By Storage Type

Hybrid storage leads the Chile Data Center Storage Market, combining flash for speed and HDDs for cost-efficiency. All-flash arrays are gaining adoption in high-performance environments, especially for banking and video analytics workloads. Traditional storage continues to serve legacy systems but is declining in preference. Hybrid storage offers scalability and flexibility, making it the most preferred architecture for diverse enterprise needs.

By Storage Deployment

Storage Area Network (SAN) systems dominate due to their high speed and reliability for mission-critical applications. Network-Attached Storage (NAS) is common among mid-sized enterprises for file-based collaboration. Direct-Attached Storage (DAS) supports smaller setups and edge deployments. SAN leads in market share, driven by data-intensive sectors like telecom, BFSI, and government.

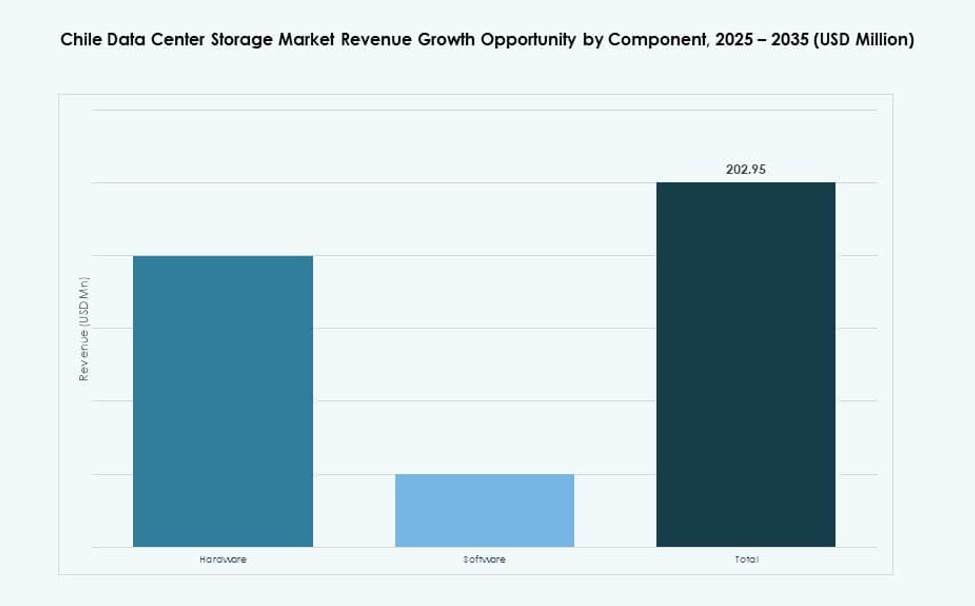

By Component

Hardware accounts for the largest share in the Chile Data Center Storage Market, driven by investments in racks, drives, and enclosures. Software is growing due to demand for automation, monitoring, and data mobility tools. Enterprises prefer integrated solutions that combine hardware with intelligent software layers. The shift toward software-defined infrastructure is accelerating.

By Medium

Solid-State Drives (SSD) are growing rapidly, driven by the need for high-speed access in performance-sensitive environments. HDDs continue to serve backup and archival needs due to their lower cost. Tape storage is limited to long-term archival and regulatory retention use cases. SSD adoption continues to rise due to falling costs and better power efficiency.

By Deployment Model

Cloud-based deployments are gaining strong traction, especially among startups and SMBs needing scalability. On-premises storage remains dominant in regulated sectors and for latency-sensitive workloads. Hybrid models are growing fastest due to flexibility and workload-specific optimization. The hybrid approach allows enterprises to align storage strategy with evolving digital transformation goals.

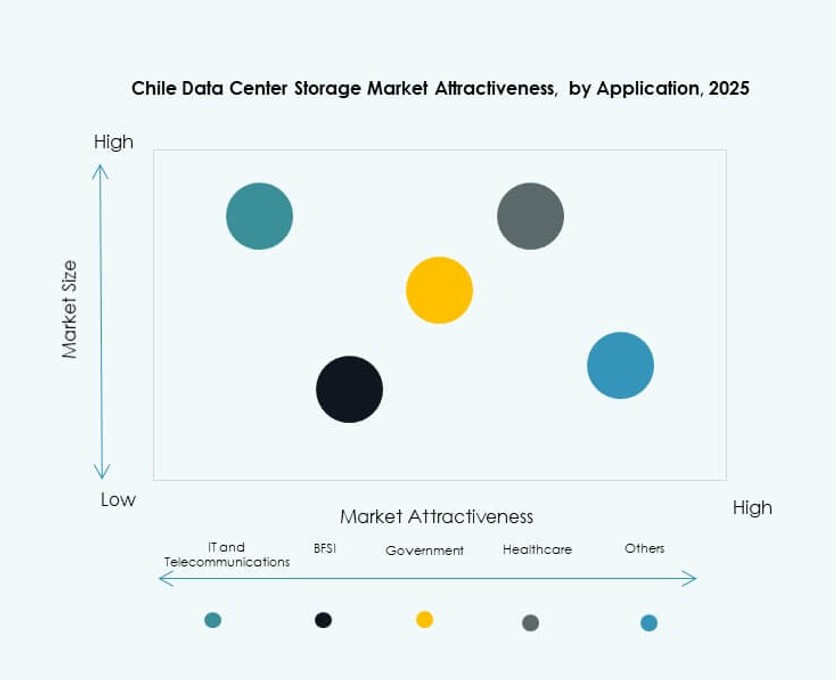

By Application

IT and Telecommunications lead the Chile Data Center Storage Market, driven by cloud hosting and mobile data growth. BFSI follows with strong demand for secure, low-latency storage. Government and healthcare sectors require compliant, high-availability platforms. Other segments like retail and education contribute through content and analytics-driven applications.

Regional Insights

Santiago Metropolitan Region Commands Over 65% Share Due to Infrastructure and Connectivity

Santiago hosts most of Chile’s hyperscale and enterprise-grade data centers. The region offers robust power availability, advanced fiber networks, and high enterprise density. It supports telecom, banking, and cloud providers operating large-scale workloads. The Chile Data Center Storage Market concentrates in this region due to demand for low-latency and high-reliability platforms. Businesses in the capital prefer colocated and hybrid infrastructure for scalability. The strong talent pool and policy support encourage further storage capacity expansions.

- For instance, Equinix’s existing ST1-ST4 facilities in Santiago provide a combined 7,536 sqm of colocation space and over 7.5MW IT capacity, supporting telecom providers like Entel after their 2022 acquisition by Equinix.

Valparaíso Region Holds Around 15% Market Share with Growth in Backup and Edge Storage Zones

Valparaíso benefits from proximity to Santiago while offering geographic resilience. It is emerging as a preferred location for disaster recovery and secondary data center sites. Cooler climate conditions reduce operational costs for storage cooling. The region attracts firms focused on backup, content caching, and regional edge deployment. It plays a growing role in business continuity planning across sectors. The Chile Data Center Storage Market supports distributed models with edge-ready infrastructure in this region.

- For instance, Gtd operates multiple data centers across Chile, including facilities in Valparaíso, offering colocation, backup, and disaster recovery services as part of its national infrastructure portfolio.

Northern and Southern Regions Share the Remaining 20% with Emerging Data Localization Demand

Northern regions, including Antofagasta, are seeing gradual investments driven by mining sector digitization. Southern cities like Temuco and Concepción support education, healthcare, and public service workloads. Limited fiber density and energy constraints slow rapid scaling. Still, digital inclusion programs and localized government IT expansion create future demand. The Chile Data Center Storage Market responds with compact, modular storage units suited for rural deployments. Growth remains moderate but strategic in underserved regions.

Competitive Insights:

- Gtd

- Sonda

- Claro Chile Data Centers

- Dell Technologies

- Hewlett Packard Enterprise

- NetApp

- IBM Corporation

- Huawei Technologies Co., Ltd.

- Nutanix, Inc.

The Chile Data Center Storage Market shows a balanced mix of global vendors and strong local operators. Multinational players lead high-performance storage, hybrid platforms, and software-defined solutions. Local providers focus on colocation, sovereign hosting, and enterprise proximity needs. Competition centers on scalability, latency control, and compliance-ready design. Vendors compete through integrated hardware and software stacks rather than standalone products. Partnerships with telecom operators strengthen market access and service reach. Pricing models emphasize flexibility through managed and hybrid offerings. Innovation targets NVMe, automation, and workload-aware storage control. It remains competitive due to steady enterprise demand and rising cloud adoption.

Recent Developments:

- In October 2025, GTD partnered with Peru’s Grupo Romero, through its InfraCorp arm, to jointly develop its data center business across Chile, Peru, and Colombia. Infracorp acquired a 49% stake in Gtdata Holdco, GTD’s data center subsidiary, for US$118 million, enabling the operation of 11 interconnected data centers, several Tier III certified.

- In July 2025, Scala Data Centers secured USD 328 million in international funding for three hyperscale data centers and a substation in Curauma, Lampa, and Huechuraba. The project supports 23 MW of contracted IT capacity for storage-heavy hyperscale needs.

- In June 2025, ACS Group’s DRAGADOS acquired 100% of Fleischmann S.A., a Chilean firm expert in data center assembly and energy systems. The deal strengthens end-to-end digital infrastructure services, including advanced storage solutions.

- In May 2025, TECfusions signed a binding Letter of Intent with Baeza Group for land to develop Chile’s largest planned data center campus. This partnership targets sustainable high-density storage infrastructure amid rising Latin American demand.