Executive summary:

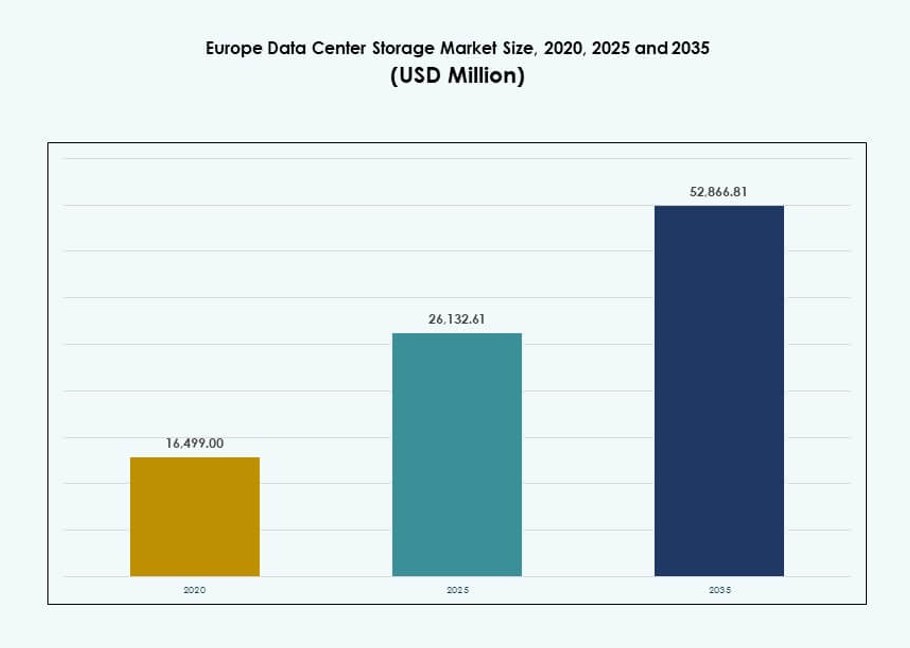

The Europe Data Center Storage Market size was valued at USD 16,499.00 million in 2020 to USD 26,132.61 million in 2025 and is anticipated to reach USD 52,866.81 million by 2035, at a CAGR of 7.24% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Europe Data Center Storage Market Size 2025 |

USD 283.83 Million |

| Europe Data Center Storage Market, CAGR |

6.13% |

| Europe Data Center Storage Market Size 2035 |

USD 517.40 Million |

The market is driven by growing enterprise adoption of hybrid and cloud-native infrastructure, increasing AI and analytics workloads, and the replacement of legacy storage with all-flash and software-defined systems. Innovation in NVMe, SDS, and orchestration technologies enhances scalability and efficiency across use cases. Regulatory compliance, data localization, and ESG mandates further shape storage strategies. Businesses prioritize performance, agility, and sustainability, making storage a vital part of digital transformation and infrastructure investment decisions.

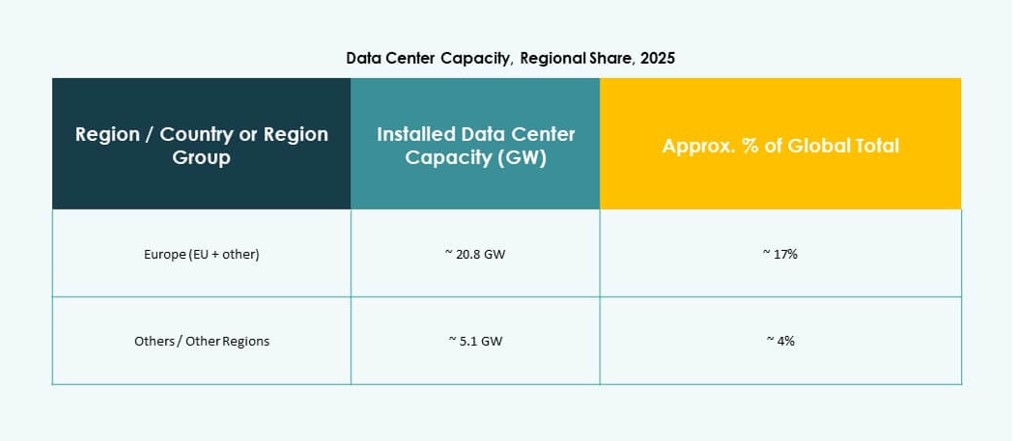

Western Europe leads the market with strong infrastructure density in Germany, the UK, France, and the Netherlands, supported by robust enterprise IT ecosystems. Nordic countries are gaining traction due to energy efficiency and green data center development. Southern and Eastern Europe are emerging with new investments, driven by digitalization efforts, growing enterprise demand, and government-led infrastructure programs that boost regional storage adoption.

Market Dynamics:

Market Drivers

Shift Toward Cloud-Native Architectures Driving Advanced Data Storage Adoption

European enterprises are shifting workloads to cloud-native environments, pushing demand for scalable storage. Businesses require low-latency and high-throughput systems to manage structured and unstructured data. The rise of containerization and microservices fuels interest in dynamic storage platforms. Software-defined storage (SDS) solutions offer agility and cost control in multicloud setups. Public and private cloud providers invest in expanding storage footprints in European Tier I cities. Data residency and compliance needs boost local storage infrastructure. The Europe Data Center Storage Market benefits from these hybrid environments. It supports workload portability, centralized control, and rapid provisioning. This driver reinforces storage as a core pillar in enterprise IT transformation.

- For instance, OVHcloud Public Cloud Object Storage supports virtually unlimited capacity with a theoretical maximum object size of 48 TB via multi-part upload (up to 10,000 parts of 5 GB each) and up to 300 write requests per second per bucket for multicloud SDS agility.

Surging AI and Analytics Workloads Accelerating Demand for High-Performance Storage Systems

Growing AI and analytics workloads increase data intensity and storage throughput needs. Organizations deploy NVMe and parallel file systems to support AI model training and inference. Structured datasets from IoT, ERP, and CRM systems require robust storage backbones. Real-time analytics and streaming platforms need fast, low-latency access to large volumes of data. The Europe Data Center Storage Market supports high-speed I/O, concurrent access, and GPU-based computing. R&D labs, financial services, and digital-native firms lead in adopting advanced storage types. AI applications drive hardware refresh cycles across enterprises. The trend positions storage as a foundational enabler of next-gen computing strategies. Investors view this demand as a long-term growth catalyst.

- For instance, Pure Storage FlashBlade//S delivers up to 50 GB/s read throughput and supports up to 15 PB effective capacity in a single platform for AI workloads.

Regulatory Compliance and Data Sovereignty Needs Boost On-Prem and Hybrid Storage Growth

Data sovereignty regulations such as GDPR and local compliance laws drive storage localization. European companies retain sensitive information in-country to reduce legal and regulatory risk. This demand supports the growth of on-premises and hybrid deployment models. Enterprises prioritize data control, encryption, and recovery planning within regional data centers. Vendors offer geo-redundant solutions to meet backup and disaster recovery standards. The Europe Data Center Storage Market adapts to strict regulatory landscapes with flexible deployment choices. It enables businesses to meet both agility and governance needs. Industry-specific compliance in banking, healthcare, and government further fuels this storage modernization trend.

Enterprise Modernization and Legacy Infrastructure Replacement Fuel Storage Investments

European enterprises are replacing aging storage systems with modular, efficient platforms. Legacy infrastructure limits scalability, performance, and interoperability in digital environments. Organizations adopt flash storage and virtual storage appliances for better utilization. Hardware refresh cycles accelerate as workloads outgrow legacy capabilities. Businesses seek integrated solutions that unify data access across hybrid IT. The Europe Data Center Storage Market supports this transition with flexible, vendor-neutral architectures. It enables seamless integration with compute and networking stacks. Investors see infrastructure replacement as a stable, recurring demand stream across verticals.

Market Trends

Rise of Storage-as-a-Service Models Transforming Capital Expenditure into Operational Spending

Storage-as-a-Service (STaaS) models gain traction among mid-sized and large European enterprises. Organizations prefer subscription-based models for scalability and predictability in IT budgets. STaaS enables flexible storage consumption aligned with changing workload needs. Vendors bundle hardware, software, and services into outcome-based contracts. This shift reduces upfront capital investment while accelerating infrastructure upgrades. The Europe Data Center Storage Market supports STaaS with hybrid-ready and cloud-integrated platforms. Managed service providers scale offerings to small and remote enterprises. Adoption is high in BFSI and healthcare sectors due to regulated, storage-intensive workloads. STaaS promotes standardization and centralized management of storage assets.

Integration of AI and ML Capabilities into Storage Management Systems

Vendors integrate AI and machine learning into storage platforms for predictive analytics. These capabilities automate tiering, fault detection, and capacity planning. AI-driven insights reduce human intervention and enable proactive maintenance. ML algorithms optimize data placement and reduce storage wastage. Enterprises deploy smart dashboards to monitor performance and usage trends. The Europe Data Center Storage Market benefits from AI-powered operations that enhance SLA adherence. These features appeal to IT teams managing complex, multi-site infrastructures. Intelligent storage plays a vital role in managing fast-growing data lakes and virtual workloads. Predictive systems help reduce downtime and improve ROI on storage investments.

Growing Importance of Data Lifecycle Management and Long-Term Archiving Solutions

Enterprises adopt lifecycle management tools to automate retention, archival, and deletion processes. Regulatory environments require strict handling of long-term data, especially in public and finance sectors. Storage vendors offer tiered solutions combining fast access with cost-efficient cold storage. Cloud-integrated tape and object storage find new relevance in archival strategies. The Europe Data Center Storage Market aligns with ESG goals by reducing energy consumption in inactive storage tiers. Businesses gain cost control while meeting compliance and audit readiness. Long-term archiving becomes critical with growing video, genomic, and transactional datasets. Automated policy-based storage is gaining widespread adoption.

Emergence of Edge Data Storage Supporting Remote and Latency-Sensitive Workloads

Edge data centers deploy localized storage solutions for real-time processing. Applications in retail, telecom, and manufacturing drive this distributed storage growth. Edge storage reduces latency, enhances security, and supports business continuity in disconnected scenarios. Modular and ruggedized storage systems serve urban and rural edge nodes. The Europe Data Center Storage Market supports edge deployments in regions with 5G expansion. Vendors offer lightweight SDS platforms and compact NAS units for edge scalability. Demand for content delivery, smart cities, and industrial IoT accelerates edge storage adoption. It complements core data centers and boosts regional IT infrastructure resilience.

Market Challenges

Rising Energy Costs and Power Efficiency Constraints in Storage Operations

Power consumption in high-performance storage arrays adds to data center operating costs. Energy efficiency mandates force vendors to redesign architectures around green storage goals. Cooling overhead increases with flash arrays and NVMe-intensive deployments. The Europe Data Center Storage Market must balance performance demands with carbon neutrality commitments. Power density challenges impact rack design and real estate planning. Organizations need visibility into energy consumption at the device level. Limited access to renewable power in some areas restricts expansion plans. Storage solutions that lack optimization tools become cost burdens for long-term operations. Efficiency pressures may delay adoption in cost-sensitive regions.

Complexity in Integrating Legacy Systems with Modern Storage Architectures

Enterprises face challenges in migrating from legacy systems to modern storage environments. Compatibility issues arise between older applications and newer flash or software-defined platforms. The lack of skilled IT staff complicates integration, especially across multi-vendor ecosystems. The Europe Data Center Storage Market must address these gaps through middleware and consulting services. Migration risks and downtime affect mission-critical workloads. Regulatory data handling adds extra layers of planning for certain sectors. Fragmented storage silos hinder centralized data governance. Without seamless interoperability, businesses risk performance bottlenecks and rising TCO.

Market Opportunities

Green Storage Solutions Aligned with EU Sustainability Mandates Offer Long-Term Potential

Sustainable storage products attract attention in carbon-conscious enterprise procurement strategies. Vendors develop low-power SSDs and smart tiering software to minimize energy use. European regulations support eco-friendly innovations in storage infrastructure. The Europe Data Center Storage Market benefits from funding and incentives for green tech adoption. Sustainability benchmarks influence data center expansion decisions across the region.

Demand for Sovereign Cloud and Decentralized Storage Architectures Across EU Nations

Sovereign cloud pushes demand for localized and secure data storage within national boundaries. Decentralized storage platforms appeal to governments and regulated sectors. Enterprises invest in colocation and regional cloud providers to retain control. The Europe Data Center Storage Market sees opportunity in privacy-driven storage deployments. Edge and fog storage gain ground in cross-border infrastructure projects.

Market Segmentation

By Storage Type

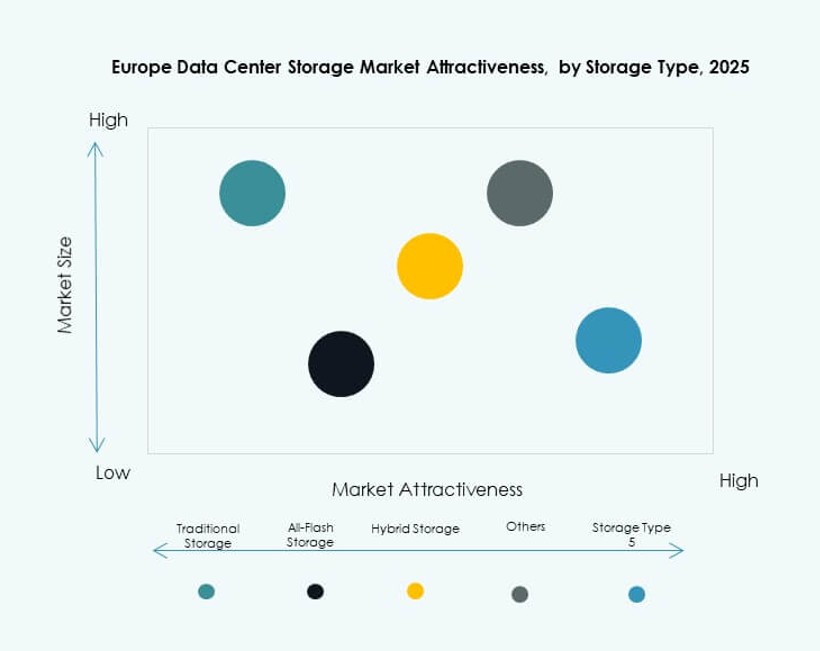

Traditional storage holds a steady presence in legacy-heavy sectors like government and BFSI. However, all-flash storage dominates in high-performance use cases due to its speed and reliability. Hybrid storage gains traction for its cost-to-performance balance. All-flash storage leads the Europe Data Center Storage Market in enterprise adoption, while hybrid systems support mid-sized firms seeking flexibility. Others segment includes object-based systems and archival options used in research and healthcare.

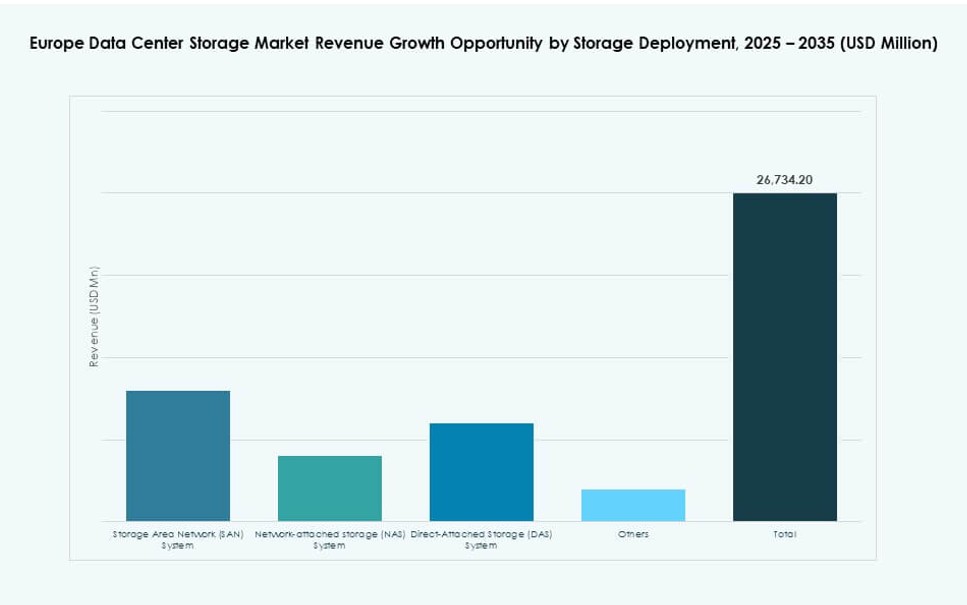

By Storage Deployment

Storage Area Network (SAN) systems dominate the market, driven by structured workloads in enterprises. Network-attached Storage (NAS) sees wide usage in file-heavy environments like media and design. Direct-attached Storage (DAS) remains relevant for edge and small-scale deployments. SAN leads in share due to its scalability and centralized management. Other deployment types include hyperconverged setups and specialized modular systems.

By Component

Hardware forms the largest component segment due to reliance on servers, arrays, and physical enclosures. Software adoption rises with demand for management platforms, virtualization, and automation tools. The Europe Data Center Storage Market shows strong momentum toward software-defined architectures. However, hardware continues to command majority share due to persistent infrastructure refresh cycles.

By Medium

Solid-State Drives (SSD) dominate over Hard Disk Drives (HDD) due to performance and energy efficiency. SSDs are widely used in enterprise arrays and AI applications. HDDs remain in use for cost-effective bulk storage. Tape storage continues in archival use cases, particularly in government and compliance-heavy sectors. SSDs lead in share due to falling costs and wide availability across product tiers.

By Deployment Model

On-premises storage maintains a large share in regulated and security-focused industries. Cloud-based models rise in adoption among tech firms and SMEs. Hybrid models gain ground as organizations blend control and scalability. The Europe Data Center Storage Market sees strong growth in hybrid deployments, especially in multi-cloud environments. Cloud-native deployments dominate in digital-native firms and content providers.

By Application

IT and telecommunications lead the market due to massive data throughput requirements. BFSI adopts secure and compliant storage frameworks to handle sensitive financial data. Government organizations deploy scalable systems for national digital services. Healthcare invests in high-capacity, compliant storage for imaging and records. Other applications include education, media, and logistics, which show steady growth in storage adoption.

Regional Insights

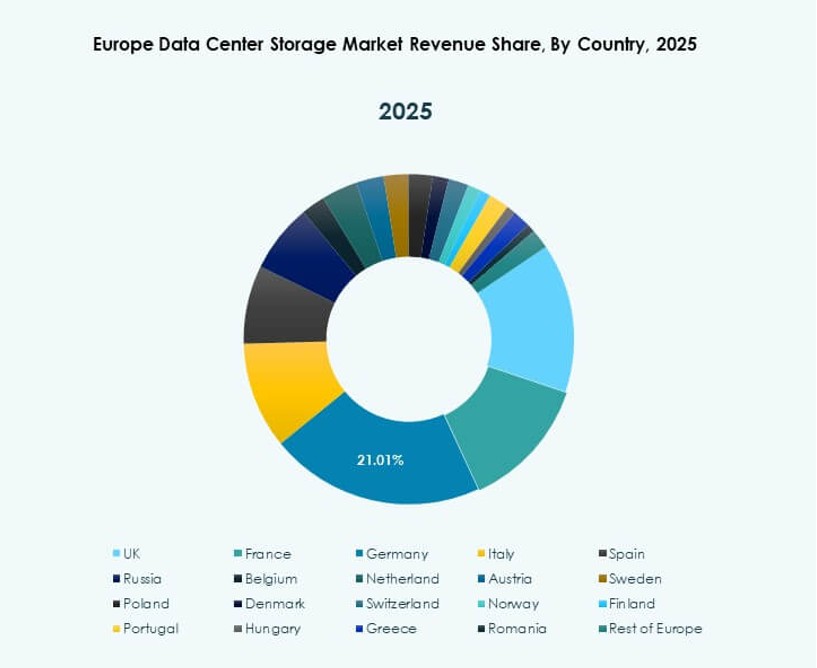

Western Europe Leads with 48% Share Due to Dense Data Center Clusters and Digital Maturity

Western Europe dominates the Europe Data Center Storage Market with 48% share. Germany, the UK, France, and the Netherlands host major data center hubs and cloud regions. Strong enterprise IT ecosystems and digital service demand support storage upgrades. Colocation providers and hyperscalers maintain dense infrastructure footprints in these markets. Advanced regulatory frameworks and energy availability encourage innovation in storage. Businesses across verticals prioritize investment in modern storage technologies to meet data growth and governance needs.

- For instance, Equinix operates over 45 International Business Exchange (IBX) data centers across Western Europe, including 12 in Germany and 11 in the UK, supporting scalable private and hybrid storage deployments for enterprise and government workloads.

Nordic Countries Hold 18% Market Share Due to Renewable Energy and Cold Climate Advantage

Nordic countries contribute 18% market share, benefiting from green energy and cooling efficiency. Sweden, Finland, Denmark, and Norway attract hyperscalers due to sustainable energy use. Storage infrastructure in the Nordics supports both primary and backup operations. Low latency and energy pricing attract global data workloads. Governments support tech investment and data center growth through policy and tax benefits. The region becomes a sustainability model in storage system deployment.

- For instance, Meta operates a large-scale data center in Odense, Denmark spanning about 84,000 square meters and powered entirely by renewable energy. The facility supports hyperscale cloud operations and reflects Europe’s focus on sustainable, high-capacity data center infrastructure.

Southern and Eastern Europe Account for 34% Share Driven by Infrastructure Expansion and Digitalization

Southern and Eastern Europe hold 34% combined share, led by Spain, Poland, Italy, and Czechia. These regions see rising investment in digital infrastructure and regional cloud deployments. Telecom modernization and public digitization projects boost storage demand. Data center expansion in Tier II cities attracts regional storage vendors. The Europe Data Center Storage Market benefits from growing small business digitization and e-government initiatives. Cost advantages and population density support growth in these emerging storage markets.

Competitive Insights:

- Dell Technologies

- Hewlett Packard Enterprise Development LP (HPE)

- IBM Corporation

- Cisco Systems, Inc.

- NetApp

- Huawei Technologies Co., Ltd.

- Lenovo Group

- Seagate Technology

- Fujitsu Limited

- Hitachi Vantara

The Europe Data Center Storage Market features strong competition among global and regional technology providers. Dell Technologies and HPE lead with broad portfolios in all-flash, hybrid, and software-defined storage. IBM and Cisco offer integrated cloud-ready systems supporting AI and analytics-driven workloads. NetApp and Huawei focus on high-density storage and NVMe integration across enterprise and hyperscale environments. Lenovo, Seagate, Fujitsu, and Hitachi Vantara serve both traditional and next-gen needs with modular and scalable systems. It is shaped by innovation in storage-class memory, AI operations, and hybrid deployment architectures. Vendors differentiate through service capabilities, sustainability features, and localized compliance support to meet diverse European data center requirements.

Recent Developments:

- In September 2025, Toshiba Electronics Europe formed a direct partnership with UK-based Titan Data Solutions to supply Enterprise HDDs for data centers, cloud, and AI infrastructure in the European market.

- In June 2025, Hewlett Packard Enterprise secured a major win with Digital Realty standardizing HPE Alletra Storage MP B10000 and Private Cloud Business Edition across over 300 global data centers, including European sites, for efficient mission-critical storage.

- In January 2025, Lenovo announced its acquisition of Infinidat to bolster high-end enterprise storage offerings, integrating petabyte-scale, cyber-resilient solutions for modern data centers across Europe and beyond.