Executive summary:

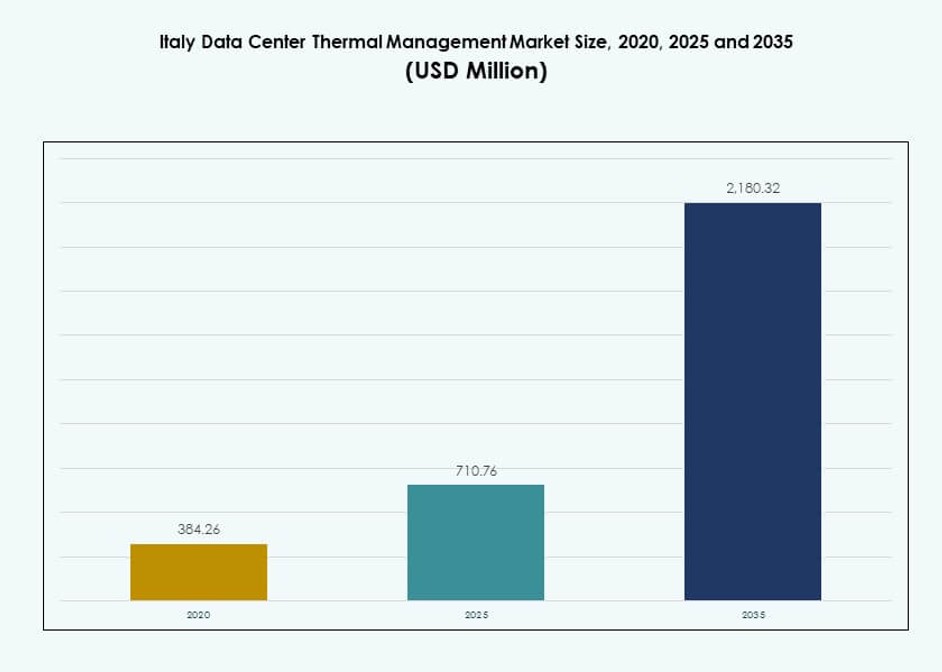

The Italy Data Center Thermal Management Market size was valued at USD 384.26 million in 2020 to USD 710.76 million in 2025 and is anticipated to reach USD 2,180.32 million by 2035, at a CAGR of 11.80% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Italy Data Center Thermal Management Market Size 2025 |

USD 710.76 Million |

| Italy Data Center Thermal Management Market, CAGR |

11.80% |

| Italy Data Center Thermal Management Market Size 2035 |

USD 2,180.32 Million |

Growing demand for high-performance computing, AI workloads, and increased cloud adoption is pushing data centers toward advanced thermal solutions. Operators are deploying liquid cooling, hot aisle containment, and AI-powered control systems to optimize energy use. Smart airflow management and predictive maintenance are becoming standard practices. These shifts make thermal management a strategic lever for uptime, cost control, and sustainability. For investors, the sector presents long-term value backed by Italy’s digital infrastructure growth and regulatory push toward energy efficiency.

Northern Italy leads due to its strong hyperscale and colocation presence, especially in Milan and surrounding areas. Central regions, including Rome, show growing enterprise and government-backed activity. Southern regions and islands are emerging with edge and renewable-powered facilities due to land availability and lower saturation. This geographic spread reflects both consolidation in urban hubs and decentralization through edge-ready deployments. The market adapts to diverse needs shaped by climate, density, and energy access.

Market Dynamics:

Market Drivers

Digital Infrastructure Expansion and High-Density Workloads Drive Thermal Management Demands in Italy

Italy’s digital economy is expanding fast with rising cloud, AI, and enterprise service workloads. Data center operators are scaling facilities with rack densities crossing 15 kW, driving heat output. This pushes demand for precision thermal control using modern technologies. The Italy Data Center Thermal Management Market responds with efficient liquid cooling and hot aisle containment solutions. New colocation builds demand modular thermal systems to match dynamic loads. The market serves hyperscale and enterprise alike, with flexibility and uptime as top priorities. Government incentives for digital infrastructure further push deployment. Businesses and investors see thermal management as a key cost and performance driver.

Shift Towards Energy-Efficient Cooling Technologies Across Italian Data Centers

Operators focus on reducing power usage effectiveness (PUE) amid stricter energy regulations. Italy’s thermal management vendors deliver energy savings through air-side economizers, direct-to-chip cooling, and smart airflow systems. Artificial intelligence aids in predictive cooling to lower fan loads and avoid thermal stress. The Italy Data Center Thermal Management Market plays a strategic role in helping firms meet carbon goals while improving operational continuity. EU mandates reinforce this direction, prioritizing green infrastructure. High-performance computing sites adopt liquid and hybrid cooling to address rising thermal footprints. Energy efficiency is now integral to site selection and ROI planning. The market becomes essential for optimizing lifecycle costs.

- For instance, Equinix’s ML5 data center in Milan holds LEED certification and incorporates water mist fire suppression systems in its data halls, supporting efficient colocation and cooling infrastructure in a facility certified under global environmental and energy standards.

Widespread Adoption of Automation and AI in Monitoring Cooling Performance

Smart cooling controls now influence procurement decisions in new data center projects. Operators deploy sensors, AI dashboards, and CFD simulations to analyze thermal flow and optimize performance. These tools reduce energy waste and ensure balanced airflow distribution. The Italy Data Center Thermal Management Market benefits from rising automation maturity among edge and colocation facilities. Real-time feedback loops improve uptime and resilience. Predictive maintenance reduces the risk of hardware failure caused by overheating. Italy’s strategic digital transformation roadmap supports these upgrades. Investors favor vendors offering integrated thermal intelligence with fast deployment models.

- For instance, A2A and Qarnot inaugurated a liquid‑cooled data center in Brescia that captures waste heat and feeds it into the city’s district heating network, producing enough thermal energy to heat approximately 1,350 apartments each year.

Modular Cooling Solutions Enable Scalable and Rapid Deployment for New Builds

Demand for scalable builds, edge sites, and retrofits fuels modular thermal systems. Rack-based and row-based designs suit distributed sites that lack legacy chilled water systems. The Italy Data Center Thermal Management Market supports this shift with plug-and-play units and prefabricated thermal kits. Deployment timeframes shrink as pre-engineered modules lower on-site complexity. Growing colocation demand outside Milan strengthens modular adoption. Enterprises prefer standardized cooling blocks to simplify facility upgrades. The market aligns with global best practices in thermal design innovation. Modular systems enable compliance with evolving regulations and sustainability targets.

Market Trends

Immersion and Direct-to-Chip Cooling Gain Ground Across High-Performance Sites

Operators are exploring advanced liquid cooling to support AI clusters and dense compute racks. Direct-to-chip cooling systems enable higher rack densities without thermal throttling. Immersion cooling eliminates the need for fans, reducing power draw and vibration risks. The Italy Data Center Thermal Management Market tracks this trend as GPU-rich workloads expand. Colocation players experiment with hybrid cooling setups to offer flexible rack configurations. Liquid cooling supports facilities constrained by floor space. It opens new performance benchmarks for cloud and edge sites. Strategic deployments mark a shift from traditional CRAC systems.

Free Cooling and Ambient-Assisted Techniques Leverage Italy’s Climate Conditions

Free cooling techniques exploit Italy’s seasonal climate for efficient thermal performance. Operators deploy adiabatic cooling and dry coolers to reduce compressor use. Air-side economizers support cooling during cooler months, reducing energy bills. The Italy Data Center Thermal Management Market sees growth in ambient-assisted designs, especially in Northern and Central Italy. These approaches lower total cost of ownership and simplify infrastructure. Regional operators report improved PUE with minimal retrofits. Greenfield builds now include passive cooling in the design stage. Market players innovate with thermally adaptive components.

Data Center Integration with District Heating and Heat Reuse Networks Expands

Heat reuse gains traction in urban projects where excess heat from data centers feeds nearby buildings. Operators collaborate with municipalities to channel waste heat into district systems. The Italy Data Center Thermal Management Market advances thermal integration technologies to support this trend. Heat exchangers and smart routing modules become essential hardware. These models improve ESG scores and strengthen community partnerships. Rome and Milan show early adoption through public-private cooperation. Heat reuse offsets grid strain and boosts project approvals. Vendors build products specifically for circular energy loops.

AI-Based Thermal Digital Twins Streamline Planning and Operational Optimization

Simulation tools enable precise thermal planning before facility buildouts. AI-based digital twins simulate airflow, equipment layout, and thermal risks. The Italy Data Center Thermal Management Market supports design accuracy with such platforms to reduce capital waste. Thermal models now guide component placement, airflow zoning, and room orientation. These insights cut overprovisioning and unplanned outages. Operators deploy twins for live feedback and real-time tuning. It allows centralized management across multisite deployments. Thermal twins integrate with broader DCIM platforms for seamless visibility.

Market Challenges

High Upfront Investment and Complexity in Liquid and Hybrid Cooling Systems

Implementing advanced cooling technologies often involves significant capital investment. Liquid-based and hybrid systems require new infrastructure, staff training, and design modifications. The Italy Data Center Thermal Management Market faces friction in legacy environments where budgets are constrained. Operators hesitate to shift from tried-and-tested CRAC units due to reliability concerns. Integration of new systems delays deployment schedules. Smaller facilities avoid complex systems without guaranteed returns. Complexity in design and maintenance further limits uptake. It stalls broad adoption across traditional enterprise facilities.

Shortage of Specialized Workforce and Thermal Engineering Talent

Deploying modern cooling systems demands technical knowledge in thermodynamics and data center operations. The Italy Data Center Thermal Management Market struggles with a limited pool of certified HVAC and thermal design experts. Staffing shortages slow commissioning and troubleshooting cycles. Vendors compete for skilled engineers, raising service costs. Training programs lag behind technology adoption, affecting support quality. Edge deployments lack local talent for maintenance, increasing downtime risks. The skill gap impacts the speed and scale of market maturity. Stakeholders must invest in talent pipelines for sustained growth.

Market Opportunities

Growth of Edge and Micro Data Centers Unlocks New Thermal Design Revenue

Edge deployments increase thermal design requirements for small-scale, modular setups. The Italy Data Center Thermal Management Market benefits from demand for compact, self-contained cooling systems. Vendors offering low-footprint solutions see rising inquiries. Telecoms and smart city projects seek resilient, remote-controlled cooling. These formats drive retrofit and new-build demand alike. Cooling-as-a-service models also gain visibility among mid-sized customers.

Sustainability Mandates Drive Demand for Greener and Adaptive Thermal Systems

EU energy mandates and carbon-neutral targets shape purchase priorities. The Italy Data Center Thermal Management Market becomes key to achieving energy benchmarks. Vendors offering refrigerant-free and renewable-powered cooling see preference. Smart systems with performance telemetry align with ESG goals. Customers seek green certifications and cost transparency.

Market Segmentation

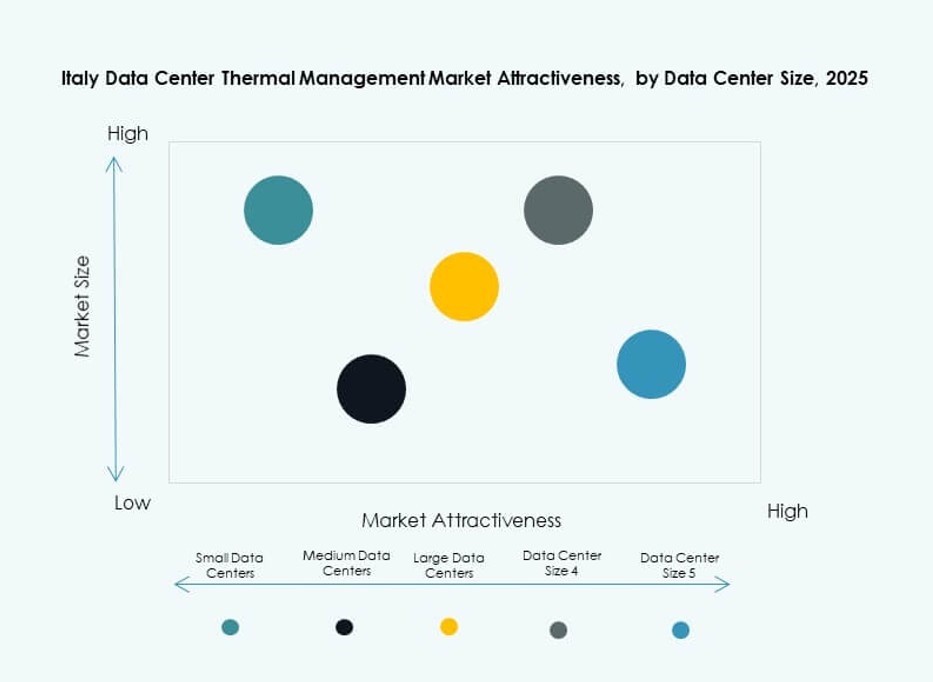

By Data Center Size

Large data centers dominate the Italy Data Center Thermal Management Market due to high concentration in Milan and Rome. These facilities prioritize scalable, efficient cooling for racks above 20 kW. Medium centers follow, driven by enterprise and telecom colocation. Small centers adopt modular solutions for quick deployments. Growth in edge zones expands the medium segment’s importance. Large centers remain key revenue contributors due to their size and workload volume.

By Cooling Technology

Air-based cooling systems lead due to familiarity, ease of setup, and low cost. Direct air and hot/cold aisle designs remain popular in traditional enterprise sites. Liquid-based cooling is growing fast, especially direct-to-chip and immersion, driven by AI workloads. Hybrid cooling gains traction for dense colocation racks. Thermoelectric and phase-change remain niche but show potential for micro and edge deployments. The Italy Data Center Thermal Management Market sees technology diversification across new builds.

By Component

Hardware holds the largest share due to chillers, cooling units, and airflow systems forming core infrastructure. Software is growing rapidly as AI, DCIM, and BMS modules enhance performance. Services play a vital role in installation, retrofitting, and continuous monitoring. Growth in service contracts reflects complexity and need for uptime. The Italy Data Center Thermal Management Market balances hardware demand with rising smart software integration.

By Hardware

Cooling units and chillers dominate hardware revenue due to their role in regulating temperatures at scale. Fans and heat exchangers support airflow and thermal exchange. Distribution systems and piping also see strong uptake, especially in retrofits. The Italy Data Center Thermal Management Market supports modular and efficient setups with vendor-customized equipment. Component-level innovation is a key competitive differentiator.

By Software

AI optimization and DCIM dashboards lead software demand. These tools manage energy use, track PUE, and allow predictive adjustments. CFD simulation enables precision planning and airflow tuning. BMS modules ensure integration with broader building systems. The Italy Data Center Thermal Management Market depends on software to increase visibility and reduce cooling waste. Software adoption grows with facility complexity.

By Services

Preventive maintenance and retrofits lead the services segment. Monitoring-as-a-service gains attention for smaller firms lacking in-house teams. Installation and commissioning are vital in new builds. The Italy Data Center Thermal Management Market supports lifecycle-based service models, especially in colocation and enterprise setups. Service bundling boosts value and improves reliability for operators.

By Data Center Type

Hyperscale and colocation/cloud facilities hold the majority share. Enterprise sites follow with slower but stable adoption. Edge and micro data centers grow fastest due to 5G, IoT, and remote work. These require compact, intelligent cooling systems. The Italy Data Center Thermal Management Market tailors designs based on type and thermal density. High-density racks accelerate liquid cooling use.

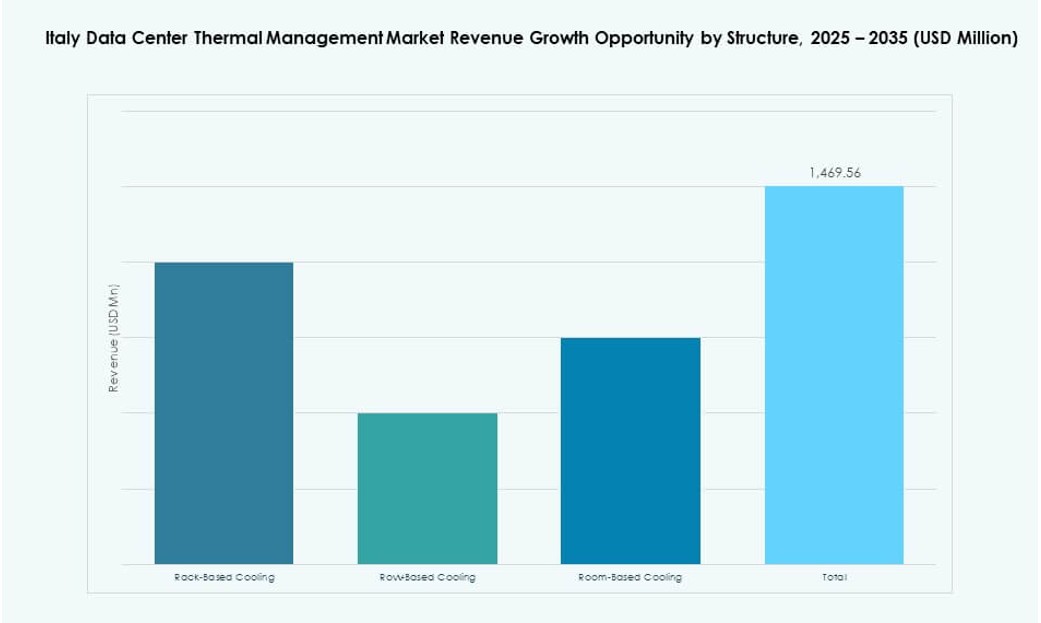

By Structure

Room-based cooling remains common in legacy facilities. Rack-based and row-based structures dominate new builds for energy and space efficiency. Modular rack-based setups allow better control and zoning. Row-based offers performance for medium-sized builds. The Italy Data Center Thermal Management Market supports structure-specific product portfolios and service plans.

Regional Insights

Northern Italy Leads with 45% Market Share Driven by Hyperscale and Carrier-Neutral Growth

Lombardy and Piedmont dominate due to Milan’s role as Italy’s tech and cloud capital. Milan hosts most hyperscale, colocation, and international cable landing stations. Northern Italy benefits from strong grid infrastructure and access to skilled labor. The Italy Data Center Thermal Management Market is concentrated here due to dense IT clusters and consistent investments. Vendors operate regional hubs to serve both legacy and greenfield facilities. Milan-based projects drive innovation and thermal upgrades.

- For instance, Retelit’s Avalon 3 data center in Milan recovers waste heat to deliver 2.5 MWt of annual thermal power and 15 GWh of recoverable energy, heating 1,250 households while avoiding 3,300 tons of CO2 emissions yearly.

Central Italy Accounts for 30% Share with Strong Government and Enterprise Backing

Rome and Lazio form the core of Central Italy’s data center expansion. Public sector digitization and smart city projects fuel demand. Government agencies deploy secure cloud and thermal-ready facilities. The Italy Data Center Thermal Management Market sees steady investments here in air-liquid hybrid systems and predictive cooling tools. Public-private partnerships and regional funding schemes support deployment. The area attracts operators targeting enterprise workloads and compliance-critical data.

- For instance, Equinix operates multiple data centers in Italy, including its RO1 facility in Rome, which supports enterprise and cloud deployments with energy-efficient infrastructure and scalable cooling systems aligned with global sustainability targets.

Southern Italy and Islands Hold 25% Share but Show Fastest Growth in Edge Zones

Apulia, Sicily, and Sardinia emerge as growth hotspots due to renewable energy availability and land affordability. Edge and colocation deployments grow in less saturated markets. The Italy Data Center Thermal Management Market sees increased demand for modular cooling systems in these regions. Operators leverage ambient cooling with solar or wind integration. Southern Italy’s strategic location enables future Mediterranean digital traffic handling. Growth here reflects decentralization and sustainability alignment.

Competitive Insights:

- Schneider Electric

- Vertiv Group Corp.

- HiRef S.p.A.

- Clivet Group

- Blue Box Group

- Airedale International Air Conditioning Ltd.

- Daikin Industries Ltd.

- Huawei Technologies Co., Ltd.

- Johnson Controls International plc

- Mitsubishi Electric Corporation

The Italy Data Center Thermal Management Market features strong competition among both global and domestic players. Vertiv and Schneider Electric lead the market with broad thermal portfolios and integrated cooling systems for colocation and hyperscale facilities. HiRef, Clivet, and Blue Box offer region-specific HVAC solutions tailored to Italy’s climatic conditions and modular data centers. Companies like Airedale and Daikin compete in precision cooling and energy-efficient air systems. Huawei and Mitsubishi focus on scalable, AI-enabled cooling technologies for high-density deployments. It favors vendors offering smart monitoring, liquid-based systems, and free-cooling solutions. Strategic partnerships and regional customization drive competitive advantage in this evolving market.

Recent Developments:

- In December 2024, SchneiderElectric introduced a new liquid-cooling–ready data center reference design that supports high‑efficiency thermal management for AI servers, using a non‑water refrigerant to minimize water use while enabling higher rack densities.

- In October 2024, Black Box Corporation opened a new Hyperscale Data Center of Excellence, enhancing its ability to deliver integrated infrastructure and services for large data centers, including network and systems solutions that support efficient cooling and high‑density deployments.

- In April 2024, Asetek, Inc. expanded its data center liquid‑cooling offering with the InRackCDU warm‑water Cooling Distribution Unit, capable of removing up to 80 kW of heat per rack while working with direct‑to‑chip loops that capture most server heat, helping operators cut reliance on traditional chillers.