Executive summary:

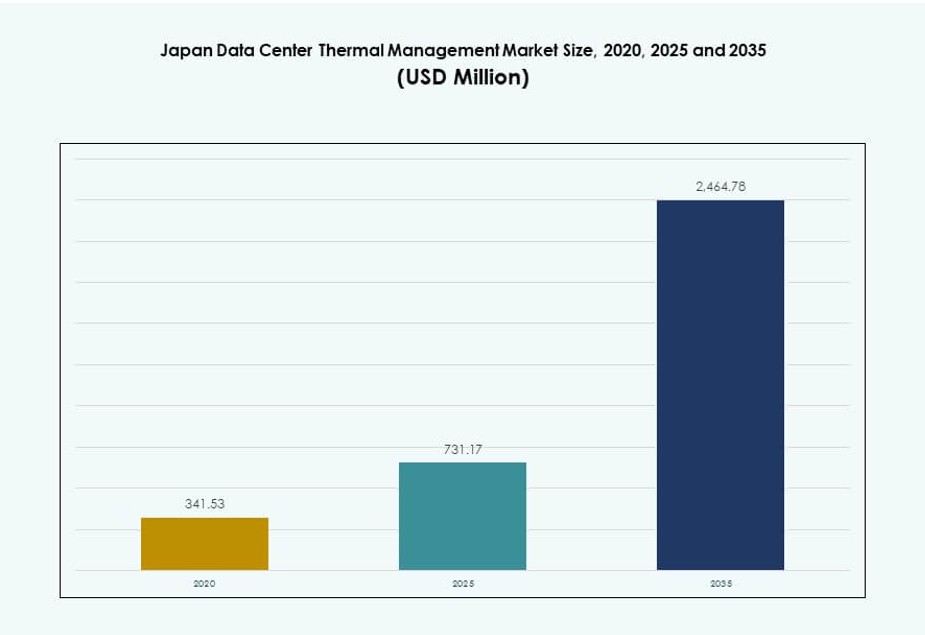

The Japan Data Center Thermal Management Market size was valued at USD 341.53 million in 2020, reached USD 731.17 million in 2025, and is anticipated to reach USD 2,464.78 million by 2035, at a CAGR of 12.83% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Japan Data Center Thermal Management Market Size 2025 |

USD 731.17 Million |

| Japan Data Center Thermal Management Market, CAGR |

12.83% |

| Japan Data Center Thermal Management Market Size 2035 |

USD 2,464.78 Million |

High-density AI computing, hyperscale expansion, and increased adoption of liquid-based cooling technologies are accelerating demand for advanced thermal systems. Data center operators are investing in direct-to-chip, immersion, and hybrid cooling to manage heat loads efficiently. Technology providers focus on modular systems, AI-driven optimization, and integration with smart building infrastructure. For investors, this market offers strong potential driven by Japan’s digitalization and sustainability mandates. Strategic importance lies in enabling uninterrupted operations while aligning with national energy efficiency goals.

Tokyo leads the market with a high concentration of hyperscale and colocation data centers requiring advanced thermal control. Osaka is growing as a secondary hub for disaster recovery and backup capacity. Emerging regions like Fukuoka and Hokkaido attract deployments due to favorable land costs, cooler climates, and supportive infrastructure. These areas offer expansion potential as operators diversify geographically to optimize efficiency and resilience. Regional dynamics shape demand patterns across thermal system types and deployment models.

Market Dynamics:

Market Drivers

Widespread Deployment of High-Density IT Loads Is Elevating Thermal Management Needs

The Japan Data Center Thermal Management Market is seeing heightened demand due to growing installation of high-density computing systems. AI, machine learning, and high-performance computing push rack power densities beyond 20 kW, necessitating efficient cooling. Traditional air-based cooling methods struggle to maintain operational thresholds, prompting interest in direct-to-chip and immersion cooling. Data center operators are adopting new layouts, better airflow control, and heat reuse techniques. This shift supports regulatory energy efficiency goals while lowering OPEX. Businesses value the operational stability this enables. The ability to support dense workloads attracts hyperscale investments. Thermal management has become a critical enabler for Japan’s digital transformation initiatives.

- For instance, NTT Data opened a 75 kW liquid cooling trial facility in Chiba Prefecture in late 2024, testing immersion and direct-to-chip systems across multiple vendors to verify performance in high-density racks.

Edge and Modular Data Center Deployments Are Driving Compact and Adaptive Cooling Architectures

The rise of edge computing across Japan calls for modular data centers in urban and remote regions. These smaller sites require compact cooling systems tailored for space-constrained environments. Direct-to-chip and rack-based systems are gaining popularity due to low latency needs and hardware precision. Telco players and enterprises leverage modular deployments to support 5G rollouts, smart infrastructure, and local processing. The Japan Data Center Thermal Management Market benefits from these deployments as they expand cooling demand beyond traditional hubs. Cooling technology must adapt to site-specific requirements while maintaining energy efficiency. Innovation in scalable and smart systems improves reliability. The shift toward modularity strengthens investor confidence in long-term infrastructure returns.

Sustainability Goals and PUE Mandates Encourage Energy-Efficient Cooling Retrofits and Designs

Operators in Japan prioritize low-PUE designs to meet national and corporate sustainability goals. Regulatory bodies are pushing for PUE reporting, waste heat reuse, and carbon footprint transparency. Existing facilities are undergoing cooling retrofits to adopt cold/hot aisle containment, variable fan speeds, and chilled water systems. Data centers designed with free cooling and heat reuse gain cost savings and ESG benefits. The Japan Data Center Thermal Management Market responds with innovation in airflow optimization and integrated controls. It drives demand for CFD tools, AI-led system tuning, and sensor-based automation. Businesses and investors view this alignment with green targets as essential for reputational and operational resilience.

- For instance, NTT Facilities’ 2024 next-generation data center project targets liquid cooling to reduce facility cooling power by 50% and support 40 kW per rack densities through hybrid air-liquid systems.

Strategic Interest from Global Cloud Providers Strengthens the Innovation Pipeline in Thermal Management

Japan’s role as a key Asia Pacific cloud hub attracts hyperscalers like Google, AWS, and Microsoft. These players bring advanced cooling strategies such as closed-loop liquid systems, immersion cooling, and AI-managed airflow. It raises local industry benchmarks and encourages domestic players to innovate. The Japan Data Center Thermal Management Market supports these shifts with local R&D, component manufacturing, and smart control integration. Strategic alliances with equipment vendors and utility providers further enhance deployment success. Such collaboration encourages job creation and tech transfer. Global investment elevates the innovation pipeline, reinforcing Japan’s strategic value in data infrastructure.

Market Trends

AI-Centric Design Requirements Are Reshaping Cooling Infrastructure Across New and Existing Facilities

Data centers supporting AI workloads increasingly need specialized cooling tailored to GPUs and TPUs. Japan-based and global firms now design facilities around liquid cooling as default. This includes cold plate systems, immersion tanks, and hybrid configurations. It reflects an industry shift from retrofit solutions to AI-first infrastructure. The Japan Data Center Thermal Management Market responds with customized offerings that enable precise heat management. AI workloads produce uneven heat profiles, requiring dynamic flow control. Intelligent sensors and DCIM platforms optimize thermal zones. Facilities that offer AI-optimized cooling attract higher rack utilization and revenue per square foot.

Liquid Cooling Ecosystems Gain Traction with Expanded Vendor Support and Standardization

In Japan, the supply chain supporting liquid cooling—from pumps and tanks to coolants and valves—is maturing. Companies are forming partnerships to ensure parts compatibility, safety, and support. Vendors offer turnkey liquid cooling systems compliant with Japanese fire, safety, and seismic standards. The Japan Data Center Thermal Management Market sees this standardization enabling broader adoption. Enterprise users are more willing to adopt liquid cooling now that ecosystem gaps are closing. Equipment reliability and maintenance cycles also improve. Increased availability of support services strengthens operator confidence. Growth in liquid cooling aligns with Japan’s need for efficient land and energy use.

Digital Twins and Computational Fluid Dynamics Tools Are Becoming Standard in Design and Monitoring

Operators are using digital twin models to simulate thermal performance before construction. These tools help optimize layout, equipment placement, and airflow systems. In Japan, CFD-based planning is increasingly used for upgrades and new builds. The Japan Data Center Thermal Management Market adopts this trend as a means to reduce trial-and-error costs. Vendors offer integrated toolkits that connect to DCIM and BMS platforms. These enable real-time monitoring and adjustment. Simulations guide investment in containment, aisle configurations, and ventilation equipment. Developers and investors use these tools to minimize risk and ensure regulatory compliance.

Heat Reuse and District Heating Integration Drive New Cooling Revenue Models

Waste heat capture is gaining interest in Japan’s urban regions where real estate is dense. Data centers explore heat reuse for district heating, greenhouses, and nearby industrial users. Government incentives support projects that export excess heat. The Japan Data Center Thermal Management Market develops modular heat exchange units and piping systems to support this model. Some operators now monetize heat rather than vent it. It enables diversification of revenue and improved environmental reporting. Cooling becomes both an expense and a strategic asset. This trend aligns with Japan’s urban planning and circular economy goals.

Market Challenges

Land Constraints and Urban Density Limit Optimal Cooling Design and Infrastructure Expansion

Japan’s dense urban environments restrict large-scale data center layouts. Cooling systems must fit within tight site footprints, limiting airflow paths and equipment access. It challenges conventional air-cooled systems and raises CAPEX for liquid systems. Urban heat islands reduce cooling efficiency. The Japan Data Center Thermal Management Market must solve these constraints through compact, high-efficiency systems. Equipment noise and vibration also face zoning restrictions. Infrastructure upgrades like chilled water lines and outdoor heat rejection units often face permit delays. Operators require solutions that maximize performance within strict physical and regulatory limits.

Aging Infrastructure and Skills Gap Impede Seamless Cooling Technology Upgrades in Legacy Facilities

Many Japanese data centers are over a decade old and were not designed for modern cooling loads. Retrofitting these sites for liquid or hybrid cooling is complex and costly. Limited availability of skilled technicians for newer cooling technologies slows deployment. The Japan Data Center Thermal Management Market needs coordinated upskilling and certification programs. Integration with legacy BMS platforms also presents compatibility issues. Downtime risk during retrofits causes hesitation among operators. Businesses often delay upgrades due to limited short-term ROI visibility. Bridging the gap between old and new infrastructure remains a major industry barrier.

Market Opportunities

Surging AI and HPC Demand in Financial and Research Sectors Unlocks High-Density Cooling Needs

Japan’s financial institutions and research universities are deploying dense AI clusters. These workloads require direct liquid cooling and real-time thermal optimization. The Japan Data Center Thermal Management Market has strong growth potential in this segment. Local system integrators and global vendors can offer specialized cooling-as-a-service models. The demand supports software optimization tools, sensors, and control platforms. Opportunities exist to create AI-ready modular pods with preconfigured thermal systems. Strong domestic demand aligns with government tech innovation goals.

Government Incentives for Green Data Centers Accelerate Adoption of Sustainable Cooling Systems

Japan promotes energy-efficient IT infrastructure through green data center guidelines and carbon neutrality goals. Cooling vendors can benefit from subsidies for heat reuse, renewable integration, and water-saving designs. The Japan Data Center Thermal Management Market supports this by enabling modular, scalable, and ESG-compliant deployments. Investors show interest in sustainability-aligned portfolios. Opportunities lie in retrofitting Tier II and III facilities with energy-saving upgrades. Cooling systems with WUE and PUE benchmarks gain procurement preference.

Market Segmentation

By Data Center Size

Large data centers dominate the Japan Data Center Thermal Management Market due to hyperscale and colocation expansion. These facilities often exceed 10 MW and deploy advanced cooling such as liquid immersion or direct-to-chip. Medium-sized facilities also show growth as enterprises modernize infrastructure. Small data centers are common in edge deployments but contribute a lower share. Growth in all sizes reflects AI workloads and local compute requirements.

By Cooling Technology

Air-based cooling, especially rear door heat exchangers and hot/cold aisle containment, leads in legacy deployments. However, liquid-based cooling is rapidly gaining traction in high-density racks. Direct-to-chip and immersion cooling show high growth rates due to AI adoption. Hybrid cooling designs support flexibility and retrofit needs. Thermoelectric and phase-change systems are niche but emerging for compact deployments. The Japan Data Center Thermal Management Market shows a strong tilt toward liquid cooling dominance over the next decade.

By Component

Hardware forms the largest share in the Japan Data Center Thermal Management Market. It includes chillers, piping, heat exchangers, and fans that drive CAPEX. Software and services are growing faster due to rising automation and monitoring needs. Software’s role is expanding with AI-based optimization and simulation. Services like retrofits and preventive maintenance ensure long-term performance. Vendors bundle hardware with managed services to offer turnkey solutions.

By Hardware

Cooling units and chillers lead in value contribution. Piping, heat exchangers, and airflow devices support modular and row-based cooling configurations. Heat exchangers are gaining demand in liquid cooling and reuse applications. The market sees a shift toward integrated hardware packages with sensors and control systems. Compact form factors support edge and containerized data centers. Reliability, energy savings, and system lifespan drive vendor differentiation.

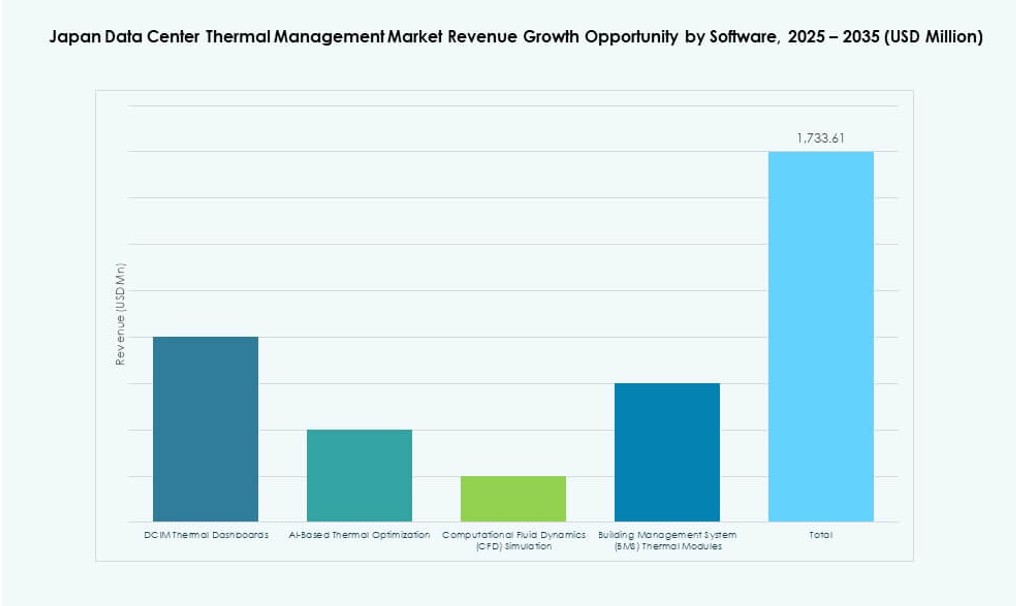

By Software

DCIM dashboards remain dominant, offering centralized visibility and control. AI optimization software enables dynamic fan speed, coolant flow, and thermal mapping. CFD simulation tools assist in planning and retrofitting. BMS modules help integrate cooling with facility systems. The Japan Data Center Thermal Management Market supports increased digitalization to reduce energy waste and improve uptime. Software plays a key role in unlocking efficiency at scale.

By Services

Installation and commissioning account for major revenue share, especially in new builds and retrofits. Preventive maintenance and retrofitting are crucial for legacy upgrades. Monitoring-as-a-service and upgrades help operators stay compliant and efficient. Custom services tailored to specific facility needs are rising. Training and remote support also show growth. Service models are evolving toward subscription-based engagements with performance-linked SLAs.

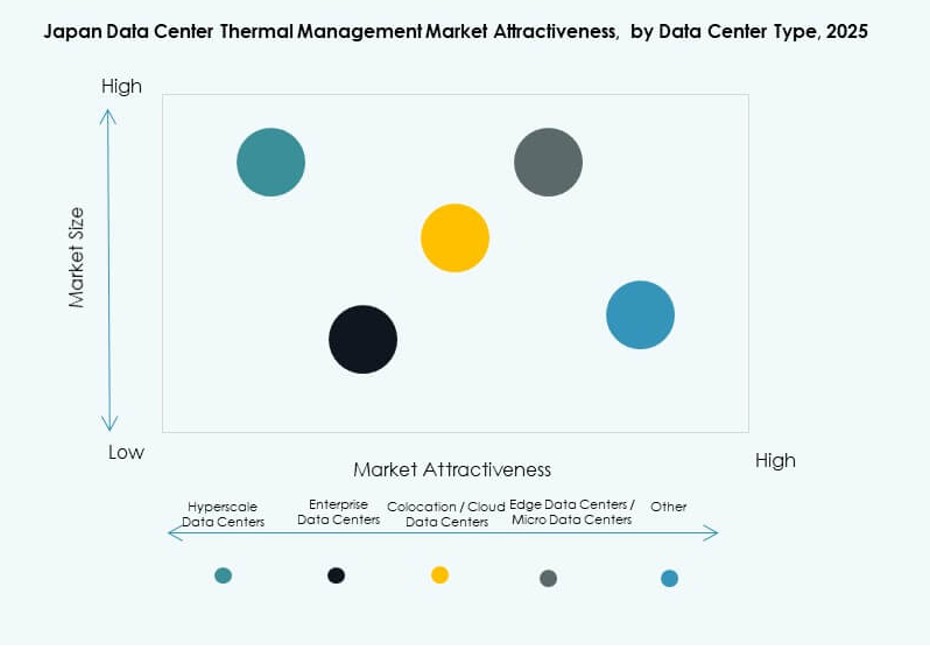

By Data Center Type

Hyperscale and colocation facilities lead due to AI and cloud workloads. Enterprise data centers are modernizing slowly but show potential. Edge and micro data centers are gaining relevance with IoT and 5G, requiring compact cooling. Colocation facilities often deploy flexible cooling to serve varied tenant needs. Hyperscale operators invest in closed-loop and liquid systems. The Japan Data Center Thermal Management Market aligns well with these types across scales.

By Structure

Rack-based and row-based structures dominate modern deployments due to modularity and space efficiency. Room-based cooling persists in older facilities but is declining. Rack-based systems align with direct-to-chip cooling and enable high-density configurations. Row-based cooling supports scalable growth and hybrid cooling systems. Room-based systems are often upgraded with aisle containment. Structure types affect airflow patterns and cooling system selection.

Regional Insights

Tokyo Metropolitan Region Leads With Over 42% Market Share Due to Dense Hyperscale and Colocation Presence

The Tokyo region dominates the Japan Data Center Thermal Management Market due to its high concentration of cloud, enterprise, and telecom data centers. Its advanced utility infrastructure and connectivity attract hyperscale investment. Cooling systems here adopt the latest innovations including liquid-to-liquid CDUs, AI-driven airflow management, and waste heat reuse. Tokyo’s urban heat profile requires precision thermal control. Real estate scarcity drives interest in compact, high-efficiency systems. Local government incentives support green retrofits and carbon reduction goals.

- For instance, Vertiv’s Liebert XDU1350 provides 1350kW cooling capacity using liquid-to-liquid heat exchange to support high-density racks up to 60kW+ per rack.

Osaka Region Holds 26% Market Share as a Key Disaster Recovery and Secondary Hub

Osaka is a preferred secondary region for data center operators due to lower earthquake risk compared to Tokyo. It serves as a disaster recovery zone and supports enterprise and colocation demand. The region has seen multiple recent investments from global hyperscalers. Cooling solutions in Osaka emphasize power reliability and cost-efficiency. Natural cooling opportunities are more feasible due to climate conditions. Its role is expanding with regional edge and smart city projects.

Emerging Regions Like Fukuoka and Hokkaido Account for 18% Share Due to Climate and Cost Advantages

Fukuoka and Hokkaido are emerging zones with growing interest due to cooler climates and lower land prices. Operators explore free cooling and heat reuse in these areas. Hokkaido’s natural environment allows more use of indirect air cooling and outdoor heat exchangers. Fukuoka benefits from its proximity to East Asian fiber routes. These regions support energy-efficient deployments and sustainable infrastructure. They represent strategic long-term growth corridors in the Japan Data Center Thermal Management Market.

- For instance, Vertiv’s Liebert XDU series, including the XDU450 variant, delivers 450kW capacity with redundant pumps and filtration for efficient deployment in cooler climates.

Competitive Insights:

- Mitsubishi Electric

- Daikin Industries Ltd.

- Delta Electronics, Inc.

- Fujitsu Limited

- Vertiv Group Corp.

- Schneider Electric

- Hitachi

- Johnson Controls International plc

- Eaton Corporation

- NTT Facilities

The competitive landscape shows strong presence of global and domestic players offering comprehensive cooling hardware and software solutions tailored for Japan’s data center ecosystem. Leading companies invest in research and development to enhance energy efficiency, system reliability, and integration with AI‑enabled management platforms. It drives technology differentiation and strengthens customer value propositions focused on reduced total cost and improved uptime. Partnerships and local service networks support faster deployment and maintenance across enterprise, hyperscale, and edge facilities. Some players leverage modular and liquid cooling platforms to meet high‑density workloads. Service and software portfolios expand through strategic alliances and targeted acquisitions. Competitive dynamics emphasize customization and compliance with local standards, which bolsters confidence among Japanese and multinational data center operators seeking long‑term performance and sustainability.

Recent Developments:

- In December 2025, Itochu Corporation signed a memorandum of understanding (MoU) with Castrol for liquid cooling solutions.

- In June 2025, Panasonic launched its next-generation cooling water circulation pump marking entry into liquid cooling components as part of its 2025 data center cooling strategy targeting Japan

- In November 2024, NTT launched two distinct liquid cooling initiatives in Japan to address the extreme heat of AI-density workloads