Executive summary:

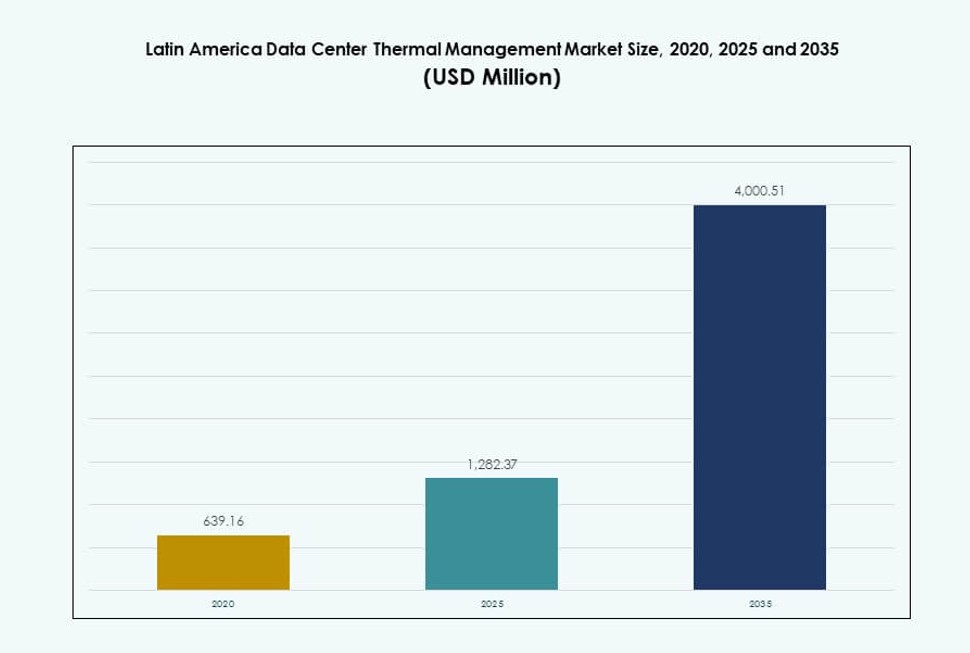

The Latin America Data Center Thermal Management Market size was valued at USD 639.16 million in 2020 to USD 1,282.37 million in 2025 and is anticipated to reach USD 4,000.51 million by 2035, at a CAGR of 11.98% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Latin America Data Center Thermal Management Market Size 2025 |

USD 1,282.37 Million |

| Latin America Data Center Thermal Management Market, CAGR |

11.98% |

| Latin America Data Center Thermal Management Market Size 2035 |

USD 4,000.51 Million |

Growth in hyperscale and cloud deployments is fueling demand for advanced thermal systems. Operators are adopting hybrid cooling, AI-optimized controls, and liquid cooling technologies to handle high-density workloads. Sustainability requirements and energy efficiency targets are accelerating this shift, making thermal design a core infrastructure concern. The market plays a strategic role for data center operators looking to optimize operational costs and uptime. For investors, it offers long-term value as thermal performance directly impacts facility scalability and reliability.

Brazil leads the region, supported by hyperscale builds and strong urban data demand. Mexico and Chile are emerging with new AI-focused campuses and renewable energy integration. Colombia and Peru show growing edge deployments tied to regional cloud zones and localized workloads. The Latin America Data Center Thermal Management Market is shaped by both large-scale central hubs and distributed regional facilities adapting to local conditions.

Market Dynamics:

Market Drivers

Hyperscale Expansion and AI Workloads Drive Demand for High-Performance Thermal Solutions

Hyperscale data centers are expanding rapidly in Latin America, especially in Brazil, Chile, and Mexico. These facilities require advanced thermal management systems to support high-density computing and AI workloads. The growing use of GPUs and AI chips generates more heat, making traditional cooling methods less effective. Liquid-based and hybrid systems are gaining adoption to maintain efficiency. The Latin America Data Center Thermal Management Market is benefiting from rising hyperscale investments. Operators prioritize energy-efficient cooling to reduce PUE and operating costs. Investments are shifting toward future-proof infrastructure capable of scaling. Businesses and investors view thermal solutions as essential to reduce downtime and extend equipment life.

- For instance, Vertiv’s Liebert XDU450 Coolant Distribution Unit delivers a nominal cooling capacity of 453 kW at a 4°C approach temperature difference.

Sustainability Goals Accelerate Adoption of Energy-Efficient Cooling Technologies

Governments and enterprises are emphasizing carbon reduction and green data center development. Efficient thermal systems help reduce power consumption and support ESG compliance. Demand for technologies that use less water and electricity is rising. AI-based cooling control, free-air cooling, and immersion systems align with climate-conscious mandates. Enterprises seek to lower total cost of ownership and meet internal sustainability KPIs. The Latin America Data Center Thermal Management Market enables operators to meet energy goals while maintaining uptime. Stakeholders invest in systems that provide real-time monitoring and autonomous cooling. ESG-aligned infrastructure receives preference from both customers and regulators.

Edge Computing and Regional Cloud Expansion Necessitate Compact, Scalable Cooling Systems

Edge deployments in second-tier cities are rising, driven by demand for local content and low latency. These sites require compact, modular cooling units with flexible scalability. Cooling challenges intensify due to smaller footprints and limited ventilation. Solutions like rear-door heat exchangers and rack-based liquid cooling help optimize space. The Latin America Data Center Thermal Management Market supports regional digitalization through tailored infrastructure. Operators need cooling systems that adapt to varied climates and space constraints. Investors are funding agile infrastructure to meet regional demand. This drives product innovation focused on dense compute zones and distributed assets.

AI-Based Thermal Optimization Software Enhances System Efficiency and Control

Software-defined cooling is transforming thermal management across Latin American data centers. Tools like AI optimization, DCIM dashboards, and BMS modules allow operators to monitor, predict, and control temperature. Integration with smart infrastructure enables proactive thermal tuning based on real-time loads. The Latin America Data Center Thermal Management Market is moving toward intelligent automation. These platforms reduce human error, increase system responsiveness, and extend equipment life. Businesses gain from improved uptime and better operational control. Investors favor data centers with smart energy optimization as they lower OPEX and improve sustainability metrics.

- For instance, Vertiv’s Liebert XDU series features redundant pumps supporting maximum flows of 450 l/m at 2.0 bar differential pressure for reliable operation. Integration with smart infrastructure enables proactive thermal tuning based on real-time loads.

Market Trends

Hybrid Cooling Architectures Gain Traction Amid High-Density Server Deployments

Operators are adopting hybrid thermal solutions combining air and liquid systems to manage heat more effectively. High-density compute environments driven by AI, cloud, and content streaming are common. Pure air-cooling fails under such load, while full liquid systems remain costly. The Latin America Data Center Thermal Management Market sees rising integration of hybrid models that balance efficiency and cost. Rear-door liquid cooling, hot aisle containment, and direct-to-chip modules operate in synergy. Vendors develop modular solutions that adapt to site-specific conditions. Operators value flexibility in transitioning between cooling types over time.

Phase-Change and Immersion Cooling Emerge as Niche but Growing Technologies

Innovative technologies like phase-change materials and immersion cooling are entering pilot and small-scale deployments. These systems provide ultra-efficient thermal control for specialized environments. While not mainstream, their use in blockchain, AI, and HPC clusters is increasing. The Latin America Data Center Thermal Management Market reflects early experimentation with these alternatives. Operators test them for energy savings and sustainability gains. Immersion systems reduce water use, while phase-change offers passive heat transfer. Both align with long-term environmental goals. Adoption remains slow but steady, supported by vendor R&D and government interest in green tech.

Demand Grows for Monitoring-as-a-Service and Predictive Thermal Analytics

Operators seek outsourced monitoring and predictive analytics for thermal performance. Vendors offer platforms that provide real-time cooling diagnostics and forecasting tools. These services reduce downtime and prevent system failure. The Latin America Data Center Thermal Management Market is witnessing a shift from manual inspection to intelligent service delivery. Predictive models detect airflow obstructions and hot spots before they affect performance. Clients favor service-based contracts that reduce capex burden. This trend supports recurring revenue for vendors and proactive maintenance for operators.

Integration of Thermal Management with Renewable-Powered Infrastructure Designs

New data centers are being designed to pair with solar, hydro, and wind energy sources. Cooling systems must function efficiently under variable power supply conditions. Thermal units optimized for load balancing and temperature regulation under grid fluctuations are in demand. The Latin America Data Center Thermal Management Market benefits from renewable-linked infrastructure. Cooling solutions are tailored for sustainability certification and low-energy operation. Green-certified cooling helps operators attract hyperscale and enterprise clients. Vendors design systems to sync with microgrids and renewable energy profiles.

Market Challenges

High Capital Costs and Infrastructure Limitations Restrain Technology Penetration Across Secondary Markets

Deploying advanced thermal systems requires significant capital, which smaller operators often lack. Liquid cooling, hybrid systems, and smart monitoring demand upfront investment in specialized equipment and facility redesign. Many legacy facilities in Latin America still operate on basic air-based systems. The Latin America Data Center Thermal Management Market faces slow adoption outside key metros due to limited financing. Secondary cities lack reliable power infrastructure, complicating integration of advanced systems. Cost-conscious buyers delay adoption despite long-term benefits. This gap restricts widespread modernization.

Skilled Workforce Shortage and Complex System Maintenance Create Operational Bottlenecks

Data center thermal systems require trained personnel for configuration, monitoring, and maintenance. Latin America faces a shortage of skilled engineers with expertise in liquid cooling and predictive software. Vendors often rely on international teams for commissioning and troubleshooting. The Latin America Data Center Thermal Management Market needs local workforce development to support growth. Operators struggle to scale due to talent gaps and high training costs. Maintenance of mixed-mode cooling also adds complexity to operations. This creates service delays and reliability risks for newer deployments.

Market Opportunities

Hyperscale and Cloud Investments in Brazil, Chile, and Mexico Drive Future Growth Potential

Large-scale investments by global cloud providers and colocation players are expanding capacity in key Latin American markets. New projects in Brazil’s São Paulo, Chile’s Santiago, and northern Mexico require advanced thermal infrastructure. The Latin America Data Center Thermal Management Market stands to benefit from these hyperscale projects, which demand high-performance, energy-efficient cooling systems. It opens opportunities for hardware vendors, software providers, and service specialists.

Edge Deployments and 5G Rollouts Open New Avenues for Compact and Modular Cooling Systems

Edge computing is expanding rapidly to serve content closer to end users. 5G networks amplify this trend, especially in urban centers and industrial zones. These edge sites need compact, reliable thermal systems with remote monitoring. The Latin America Data Center Thermal Management Market is positioned to serve this segment with modular, rack-based solutions and AI-enabled maintenance platforms.

Market Segmentation

By Data Center Size

Large data centers dominate the Latin America Data Center Thermal Management Market due to rising hyperscale deployments across Brazil, Mexico, and Chile. They require complex thermal systems to manage high rack densities. Medium-sized centers also hold notable share, driven by enterprise adoption. Small data centers are growing with the edge trend but contribute less revenue currently. The shift toward centralized processing has made large facilities key revenue generators in the market.

By Cooling Technology

Air-based cooling, especially rear-door heat exchangers and hot/cold aisle containment, remains the most deployed due to lower cost and familiarity. However, liquid-based cooling, particularly direct-to-chip and immersion, is gaining share with AI and GPU-heavy workloads. Hybrid systems are expanding fastest, offering the flexibility to balance legacy and modern infrastructure. Thermoelectric and phase-change remain niche, used for specific applications requiring ultra-low energy use.

By Component

Hardware leads the Latin America Data Center Thermal Management Market due to physical infrastructure needs. Chillers, heat exchangers, fans, and airflow devices dominate capital expenditure. Software is growing due to demand for predictive analytics, AI optimization, and DCIM platforms. Services contribute through installation, upgrades, and remote monitoring, with vendors offering managed support models to smaller operators.

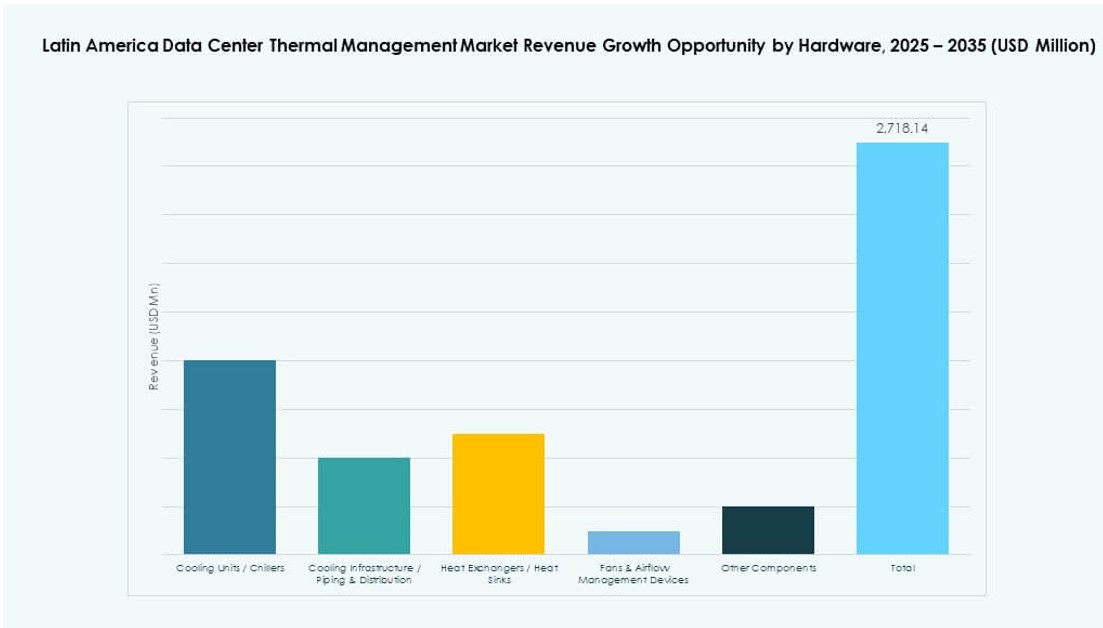

By Hardware

Cooling units and chillers account for the largest share due to widespread use in traditional facilities. Heat exchangers and piping systems follow, especially in liquid and hybrid setups. Fans and airflow devices see steady demand from air-cooled setups. Vendors also offer high-efficiency retrofits and replacements to upgrade older systems without full overhauls. Innovation in energy use, noise control, and modularity is shaping this segment.

By Software

AI optimization software is gaining adoption for real-time thermal control, especially in high-density environments. DCIM dashboards remain popular for basic temperature and power monitoring. CFD simulation tools help design efficient layouts and airflow paths. BMS modules offer integration across facility operations. This segment enables operators to reduce power usage and automate response to workload shifts.

By Services

Installation and commissioning services see strong demand across new builds and retrofit projects. Preventive maintenance and monitoring-as-a-service are gaining traction among small and mid-sized players. Retrofits and system upgrades are essential for legacy facilities aiming to meet new cooling needs. Vendors are bundling software and services to offer end-to-end cooling lifecycle support.

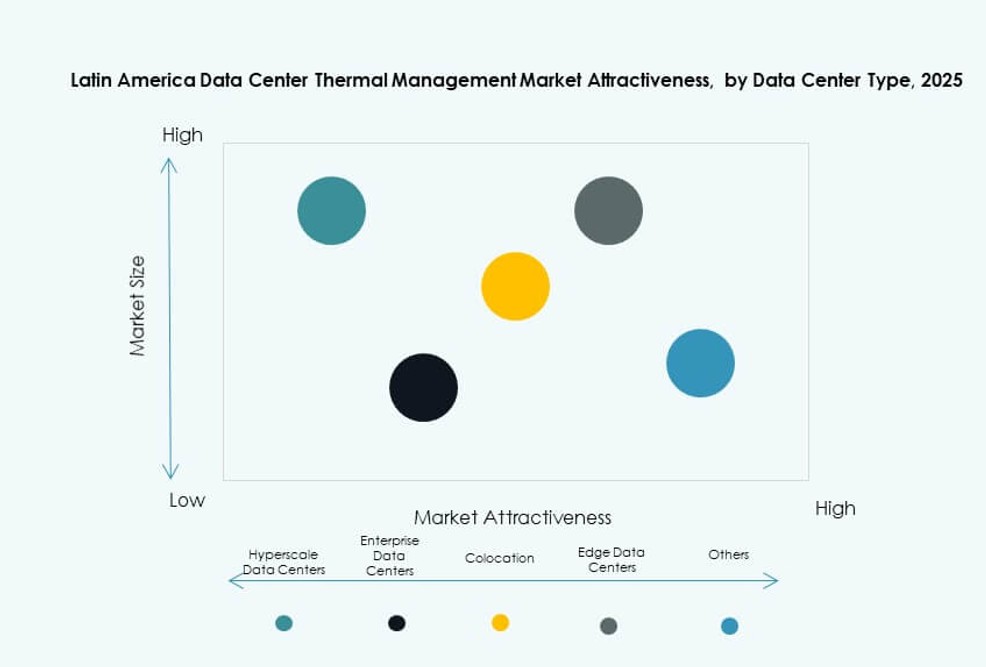

By Data Center Type

Hyperscale and colocation/cloud facilities are the largest consumers of thermal management systems in Latin America. Hyperscale players demand liquid and AI-managed cooling due to extreme densities. Colocation providers need scalable systems for multi-tenant operations. Enterprise and edge data centers follow, with edge facilities favoring compact, modular solutions. Others include specialized data centers in banking, telecom, and research.

By Structure

Room-based cooling is still dominant, particularly in traditional facilities. However, rack-based and row-based cooling systems are growing quickly in modern builds. Rack-based systems offer precision cooling, ideal for high-density and edge deployments. Row-based units support modular growth and flexible layouts. Vendors provide options tailored to both legacy and new-generation designs.

Regional Insights

Brazil Leads with Over 42% Share Driven by Hyperscale Investments and Urban Data Demand

Brazil dominates the Latin America Data Center Thermal Management Market with over 42% share. São Paulo is a major hub for hyperscale and cloud providers. New colocation campuses and AI-ready facilities demand advanced thermal systems. Local operators and global players like Scala and Elea lead deployments. Government incentives and strong digital demand support continued growth. Brazil remains the primary destination for thermal tech vendors.

- For instance, Scala Data Centers deployed Vertiv thermal solutions delivering 93 MW cooling capacity across Brazilian sites including Tamboré campus, using 364 CRAH units and 58 chillers with free cooling and adiabatic features.

Mexico and Chile Hold 29% Combined Share Supported by Renewable Energy and Strategic Location

Mexico and Chile collectively hold 29% of the market. Mexico benefits from proximity to the U.S., expanding cloud zones, and nearshoring trends. Chile offers renewable energy and cool climates ideal for free-air cooling. Santiago is a rising hub with multiple hyperscale developments. These countries attract investment for their infrastructure stability and policy support. Both play key roles in the regional thermal ecosystem.

- For instance, Ascenty (Digital Realty) activated its Santiago data center in 2024 with 12 MW IT capacity using air handling units optimized for 90% renewable energy integration and PUE below 1.3.

Emerging Markets Like Colombia, Argentina, and Peru Capture 12–15% Share with Edge Expansion

Colombia, Argentina, and Peru hold around 12–15% of market share. Growth comes from government-led digitalization and edge deployments in second-tier cities. These regions show rising demand for compact and resilient cooling systems. Operators are testing AI-optimized and modular thermal units in space-limited environments. The Latin America Data Center Thermal Management Market sees opportunity in these markets as connectivity and 5G adoption grow.

Competitive Insights:

- Vertiv Group Corp.

- Schneider Electric

- Stulz GmbH

- Daikin Industries Ltd.

- Delta Electronics, Inc.

- Trane Technologies plc

- Asetek, Inc.

- Rittal GmbH & Co. KG

- Fujitsu Limited

- Johnson Controls International plc

The Latin America Data Center Thermal Management Market features a competitive mix of global OEMs and regional providers. Vertiv, Schneider Electric, and Stulz lead with extensive portfolios across air, liquid, and hybrid cooling technologies. These firms target hyperscale and colocation deployments with scalable infrastructure and advanced controls. Companies like Delta Electronics, Trane, and Daikin focus on energy-efficient HVAC systems for retrofit and new builds. Asetek and Fujitsu push innovation in direct-to-chip and immersion cooling. Localized support, service capability, and integration with smart monitoring platforms are critical differentiators. Product launches, partnerships, and software-led cooling optimization are driving competition. It is shifting toward sustainability-aligned and AI-enhanced solutions, as operators prioritize reliability, modularity, and energy savings.

Recent Developments:

- In August 2024, Scala Data Centers partnered with Serena to secure renewable energy supply agreements, delivering 393 MW of wind power from Bahia, Brazil, starting in 2025 to support hyperscale data centers including AI workloads in Latin America.

- In May 2024, Rittal, in collaboration with multiple hyperscale data center operators, developed a modular cooling system exceeding 1 MW capacity using direct water cooling tailored for high-power AI applications in the Latin America data center cooling sector.

- In May 2024, Stulz unveiled the CyberCool Coolant Management and Distribution Unit (CDU), designed to optimize heat exchange in liquid cooling systems with capacities from 345 kW to 1,380 kW for data center thermal management.

- In January 2024, Aligned Data Centers introduced its DeltaFlow liquid cooling technology to meet high-density compute needs for next-generation applications, high-performance computing, AI, and machine learning within Latin American data centers.