Executive summary:

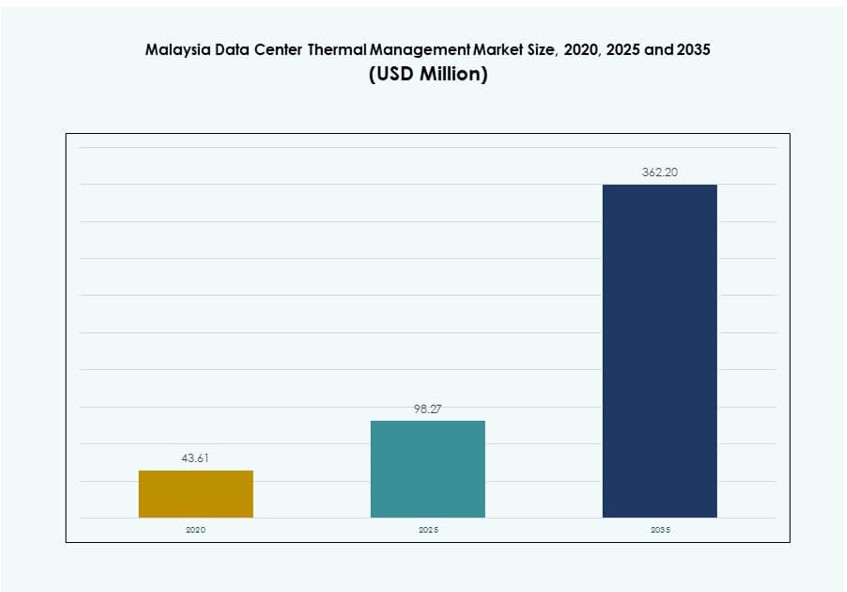

The Malaysia Data Center Thermal Management Market size was valued at USD 43.61 million in 2020 to USD 98.27 million in 2025 and is anticipated to reach USD 362.20 million by 2035, at a CAGR of 13.84% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Malaysia Data Center Thermal Management Market Size 2025 |

USD 1,282.37 Million |

| Malaysia Data Center Thermal Management Market, CAGR |

11.98% |

| Malaysia Data Center Thermal Management Market Size 2035 |

USD 4,000.51 Million |

Rising demand for high-performance computing, AI, and edge infrastructure is driving the adoption of advanced cooling systems. Businesses invest in liquid cooling, hybrid systems, and AI-powered thermal controls to support energy efficiency and uptime. These innovations reduce operational costs and carbon footprint while enabling scalable infrastructure. The market plays a strategic role in supporting digital growth, attracting hyperscale investments, and improving service delivery. Investors view thermal management as a key enabler of sustainable, high-density data centers in Southeast Asia.

The Klang Valley leads with the highest concentration of data centers due to strong connectivity, energy infrastructure, and enterprise demand. Johor is rapidly emerging as a hyperscale hub, supported by cross-border ties and industrial development. Penang and Sarawak show growth from localized edge deployments and smart city initiatives. These regions reflect varied demand profiles, making Malaysia a diverse and attractive market for thermal solution providers.

Market Dynamics:

Market Drivers

Rapid Expansion of AI and High-Density Workloads Drives Demand for Advanced Cooling Infrastructure

AI workloads and GPU-intensive applications require significantly more power and generate more heat. Data centers across Malaysia are scaling up rack densities to support high-performance computing. This shift places pressure on thermal management systems to operate efficiently under higher loads. Liquid cooling and hybrid systems are gaining traction due to their effectiveness at managing thermal stress. The Malaysia Data Center Thermal Management Market benefits from the need for precise, scalable, and low-latency cooling solutions. Facility planners prioritize solutions that reduce energy waste while maintaining reliability. Demand for adaptive, modular systems continues to grow among hyperscale and colocation providers. Businesses view these technologies as critical enablers of AI adoption and infrastructure modernization.

- For example, YTL Johor Data Center 3 is designed with an 80 MW IT load and direct‑to‑chip liquid cooling readiness for AI deployments, achieving a design PUE below 1.3 without raised floors. The facility has structural support for high rack loads up to 15 kN/sqm, making it suitable for high‑performance computing and dense server configurations.

Strong Push Toward Green Data Centers to Meet Energy Efficiency and Sustainability Goals

Sustainability regulations and green building mandates are influencing cooling system design. Companies in Malaysia adopt energy-efficient cooling methods to meet ESG targets. Thermal management solutions now focus on low PUE, water conservation, and refrigerant compliance. Organizations are retrofitting legacy data centers with advanced chillers, free cooling systems, and AI-driven airflow optimization. The Malaysia Data Center Thermal Management Market sees rising demand from operators aiming to reduce carbon footprint and operational costs. Local utilities also support green transitions with incentives for efficiency upgrades. Cooling becomes a strategic investment area aligned with carbon-neutral infrastructure planning. Energy usage transparency and green certifications now influence colocation contracts and investor interest.

Growing Hyperscale and Cloud Deployments Fuel Equipment and Software Cooling Needs

Malaysia is seeing rising investments from global hyperscale players and regional cloud providers. These large-scale data centers require sophisticated thermal architectures to manage mission-critical operations. Cooling hardware, airflow systems, and DCIM-integrated software are deployed at scale. The Malaysia Data Center Thermal Management Market expands as demand for automation and cooling analytics increases. Software layers like AI optimization and CFD simulation now complement physical systems. Vendors offer end-to-end packages tailored for hyperscale environments. Enterprises seek full-stack cooling frameworks that ensure SLA compliance and operational resilience. Cooling performance directly impacts rack utilization and service capacity planning.

- For example, YTL Johor Data Center 6 supports a 40 MW IT load with concurrently maintainable cooling systems and a design PUE under 1.4. The facility’s infrastructure includes distributed redundant power and chilled water systems to ensure reliable operations for hyperscale workloads.

Strategic Role of Malaysia in Regional Edge, Connectivity, and Data Sovereignty Ecosystems

Malaysia’s digital economy strategy and regional positioning create a strong case for data center investment. Proximity to Singapore and submarine cable access boost its role as an alternative hub. Edge and micro data centers in emerging zones need thermal systems designed for small footprints and localized conditions. The Malaysia Data Center Thermal Management Market supports edge buildouts with compact, row-based, and DCIM-monitored systems. Investors view Malaysia as a stable, cost-efficient location for edge and regional deployments. Demand for scalable cooling grows in industrial corridors and rural fiber expansion zones. These distributed deployments need reliable thermal systems that minimize maintenance and maximize uptime.

Market Trends

Adoption of Liquid Cooling for High-Density, AI, and GPU Workloads Across Hyperscale Sites

Liquid cooling gains momentum due to its ability to manage high thermal loads in compact spaces. Direct-to-chip and immersion cooling are increasingly used in new builds and AI-ready data halls. Hyperscale developers in Malaysia deploy these systems to enable higher rack densities. Vendors offer modular cooling designs tailored for GPU clusters. The Malaysia Data Center Thermal Management Market benefits from growing pilot deployments and adoption in AI zones. Enterprises also explore liquid cooling to reduce energy costs and water usage. Cooling innovation becomes critical in attracting advanced cloud and HPC tenants. These technologies enable next-gen infrastructure that meets digital economy demands.

AI-Powered Environmental Control Systems and Thermal Monitoring Tools Gain Adoption

AI and machine learning enable real-time optimization of cooling resources. Data center operators deploy intelligent control platforms to reduce energy consumption. Sensors track airflow, temperature zones, and equipment usage in granular detail. AI models predict thermal hotspots and automate fan speeds, coolant flow, and humidity settings. The Malaysia Data Center Thermal Management Market grows as operators invest in autonomous cooling systems. These solutions reduce manual intervention and ensure 24/7 efficiency. Predictive alerts help avoid downtime and increase operational transparency. Smart cooling becomes a value-added layer for colocation, enterprise, and hyperscale sites alike.

Rise of Modular Cooling Infrastructure for Fast, Scalable, and Location-Specific Deployments

Operators shift toward modular cooling solutions that align with prefabricated and containerized builds. These systems reduce construction time, improve serviceability, and simplify regional deployment. Vendors supply modular chillers, fan wall units, and power-cooling skids pre-integrated with software. The Malaysia Data Center Thermal Management Market sees growing interest in modularity for enterprise and edge builds. These solutions enable flexible infrastructure in industrial parks and remote areas. Deployment models become faster, while maintenance is centralized and predictable. Customers prefer standardized cooling units that can scale with IT needs and power availability.

Liquid-to-Air and Hybrid Cooling Solutions Emerge to Meet Sustainability and Regulatory Demands

Hybrid systems combine the best of air and liquid techniques to address complex thermal environments. Liquid-to-air heat exchangers, rear-door cooling units, and hybrid aisle containment gain traction. These systems allow for energy savings without full immersion infrastructure. The Malaysia Data Center Thermal Management Market benefits from increased investment in mixed-mode cooling. Such systems offer compliance with new energy efficiency standards and environmental certifications. Operators use hybrid models to retrofit existing sites without full redesign. Vendors now develop products specifically for Malaysian humidity and temperature profiles. These systems ensure cost-effective and regulation-aligned cooling performance.

Market Challenges

High Upfront Capital Investment and Return Uncertainty in Advanced Cooling Technologies

Deploying liquid cooling, AI-based airflow systems, and smart chillers requires substantial capital. Enterprises hesitate to invest without clear ROI projections or client commitments. Small and medium players struggle with budget constraints and prefer low-cost solutions. The Malaysia Data Center Thermal Management Market faces delays in widespread adoption of advanced systems. Limited technical expertise and vendor dependence further restrict innovation rollout. Some operators stick to legacy systems due to familiarity and lower integration complexity. Market penetration of high-efficiency solutions remains slow without bundled financing or managed service models. Scaling cooling innovation depends heavily on capex-friendly models and OEM collaboration.

Fragmented Standards and Limited Interoperability Between Cooling and IT Systems

The thermal management ecosystem lacks unified standards for equipment interoperability and control platforms. Integration challenges arise when linking cooling units, sensors, and DCIM dashboards from different vendors. The Malaysia Data Center Thermal Management Market sees inconsistent performance across multivendor deployments. Lack of open protocols limits flexibility and automation potential. Some software systems offer partial visibility or limited command functions. Operators face high integration costs and extended commissioning timelines. Standardization gaps reduce agility in responding to AI and high-density computing needs. Greater alignment among vendors, regulators, and users is critical for seamless operation.

Market Opportunities

Edge and Rural Data Center Growth Sparks Demand for Compact and Energy-Efficient Cooling

Edge deployments are increasing in Malaysia’s secondary cities, industrial zones, and telecom infrastructure hubs. These facilities need efficient, low-footprint cooling systems designed for constrained environments. The Malaysia Data Center Thermal Management Market finds strong opportunity in row-based, modular, and fan-assisted cooling products. OEMs that offer reliable, remotely monitored systems will lead in this space. Demand also rises for solar-integrated and low-maintenance solutions for hard-to-reach areas.

Integration of AI and Predictive Analytics into Cooling Platforms to Enhance Value Delivery

Operators seek intelligent cooling systems that offer real-time optimization and preventive maintenance. Solutions with AI layers, digital twins, and predictive alerts are in demand. The Malaysia Data Center Thermal Management Market is poised to benefit from innovations that deliver both efficiency and uptime assurance. Software-led cooling platforms create new revenue models for vendors.

Market Segmentation

By Data Center Size

Large data centers dominate the Malaysia Data Center Thermal Management Market due to investments from hyperscale and cloud providers. These facilities require robust, high-capacity cooling systems with advanced automation. Medium-sized data centers are growing with enterprise and government demand. Small facilities, including edge and on-premise deployments, favor compact and modular systems tailored for limited space and budget.

By Cooling Technology

Air-based cooling remains widely adopted, with hot/cold aisle containment and rear-door exchangers in use across many colocation sites. However, liquid-based cooling—particularly direct-to-chip and immersion—is gaining popularity for AI workloads. Hybrid systems that blend air and liquid are increasingly deployed to balance cost, performance, and efficiency. Emerging technologies like phase-change and thermoelectric cooling are still in early-stage deployment.

By Component

Hardware contributes the largest share in the Malaysia Data Center Thermal Management Market due to heavy spending on cooling infrastructure, chillers, heat exchangers, and airflow systems. Software is growing rapidly as DCIM platforms and AI tools optimize energy use. Services are essential, especially for preventive maintenance, commissioning, and retrofit projects in legacy sites.

By Hardware

Cooling units and chillers form the core of infrastructure investment, supported by heat sinks and airflow devices. Distribution piping, fans, and containment components support airflow regulation. These components are increasingly integrated with smart sensors for predictive maintenance and analytics. Adoption is strongest in hyperscale and retrofit projects.

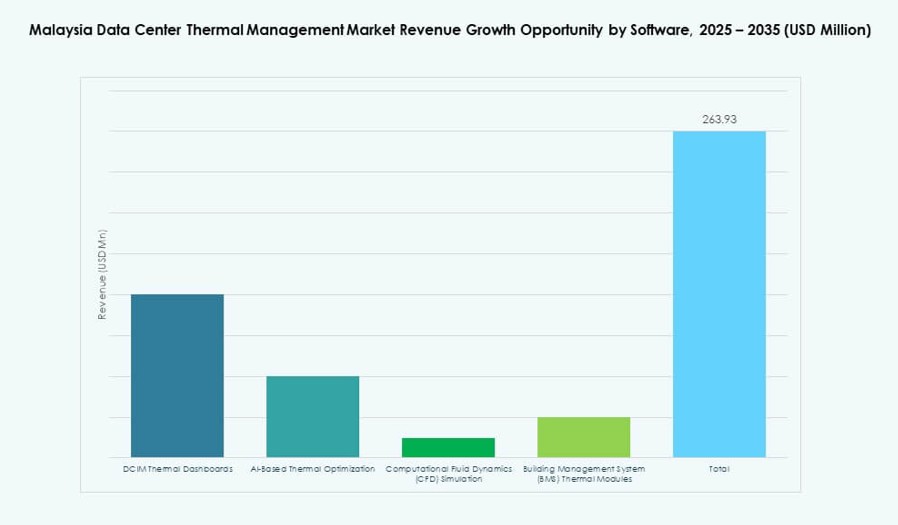

By Software

DCIM dashboards remain standard across most large data centers, offering thermal visibility and alerts. AI optimization tools now enhance cooling efficiency through automation. CFD simulation software supports pre-construction modeling, helping reduce thermal hotspots. BMS modules allow seamless integration with building and energy systems for centralized control.

By Services

Installation and commissioning lead the service category, especially in greenfield hyperscale and colocation builds. Preventive maintenance and monitoring services are growing in importance to ensure uptime. Retrofit services for older facilities support energy efficiency upgrades and compliance. Remote and AI-enabled services now add value for Tier II cities and remote sites.

By Data Center Type

Colocation and cloud data centers dominate, driven by demand from hyperscalers, fintech, and public sector projects. Hyperscale projects anchor new deployments and influence cooling trends. Enterprise facilities maintain steady demand with moderate cooling requirements. Edge and micro data centers are gaining share, especially in telecom and content delivery zones.

By Structure

Room-based cooling structures are standard in large, centralized data centers. Row-based cooling is growing among modular and edge deployments. Rack-based systems gain popularity in high-density zones and AI cluster applications. Each structure type aligns with specific IT load profiles and space constraints.

Regional Insights

Klang Valley Commands the Highest Market Share Due to Dense Facility Concentration

The Klang Valley leads the Malaysia Data Center Thermal Management Market with over 52% share. Its advantages include fiber connectivity, power infrastructure, and proximity to government and enterprise demand centers. The presence of international colocation hubs drives demand for high-efficiency cooling. It continues to attract hyperscale investments supported by urban digital economy strategies.

- For instance, Equinix’s KL1 facility in Cyberjaya provides 900 cabinets across 2,630 sqm of colocation space. It continues to attract hyperscale investments supported by urban digital economy strategies.

Johor Emerges as a Key Secondary Market with Strong Cross-Border and Industrial Appeal

Johor accounts for approximately 23% of the market share and is growing due to its proximity to Singapore. Large land banks and favorable utility pricing attract hyperscale developers. It benefits from government-backed industrial corridors and manufacturing zones. Demand for scalable and hybrid cooling systems is strong in both greenfield and retrofit projects.

Penang and Sabah/Sarawak Represent Emerging Zones with Rising Edge and Cloud Deployments

Penang contributes around 15% of the market and gains traction through its role in electronics and logistics. Cooling needs rise in smart factories, R&D centers, and cloud integration hubs. Sabah and Sarawak hold the remaining 10% share, with rising interest in rural connectivity and decentralized edge builds. Cooling providers explore compact, energy-efficient systems for regional use.

- For instance, Infinaxis Cyberjaya 1 spans 17,000 sqm and features 10 data halls supporting up to 1,830 cabinets. The facility is being developed to meet rising demand for high-density colocation in Malaysia’s digital hub.

Competitive Insights:

- Vertiv Group Corp.

- Schneider Electric

- Daikin Industries Ltd.

- Delta Electronics, Inc.

- LG Electronics

- Trane Technologies plc

- Mitsubishi Electric Corporation

- Airedale International Air Conditioning Ltd.

- Johnson Controls International plc

- NTT Facilities

The Malaysia Data Center Thermal Management Market remains competitive, led by global infrastructure and cooling system providers. Vertiv and Schneider Electric hold strong positions with full-stack thermal management portfolios. Companies like Daikin, Mitsubishi Electric, and LG Electronics offer robust HVAC systems tailored to tropical environments. Delta and Trane support modular cooling units for hyperscale and enterprise data centers. Airedale and Johnson Controls supply precision cooling and airflow systems to colocation operators. NTT Facilities focuses on integration and managed services. It continues to attract new players offering AI-powered thermal analytics and immersion cooling platforms. Competition centers around energy efficiency, rapid deployment, and AI integration. Companies target both greenfield and retrofit projects across hyperscale, colocation, and edge segments.

Recent Developments:

- In November 2025, Daikin Industries Ltd. acquired Chilldyne, a leader in negative pressure liquid cooling systems for AI data centers, adding direct-to-chip technology to its portfolio. The deal enhances Daikin’s high-efficiency cooling offerings for hyperscale environments, complementing prior acquisitions like DDC Solutions

- In March 2024, Bridge Data Centres partnered with Red Dot Analytics to leverage AI-driven digital twin technology for optimizing cooling efficiencies and managing thermal risks in its Malaysian data centers, including a pilot at the Cyberjaya facility. This strategic collaboration focuses on sustainable, energy-efficient solutions like waterless air-cooled and cold plate liquid cooling technologies