Executive summary:

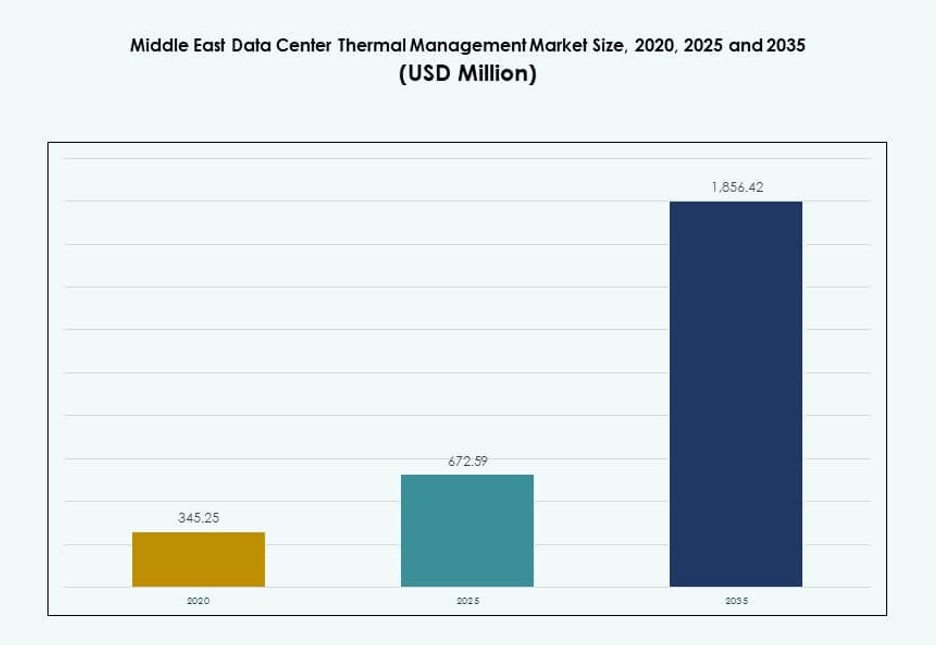

The Middle East Data Center Thermal Management Market size was valued at USD 345.25 million in 2020 to USD 672.59 million in 2025 and is anticipated to reach USD 1,856.42 million by 2035, at a CAGR of 10.56% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Middle East Data Center Thermal Management Market Size 2025 |

USD 672.59 Million |

| Middle East Data Center Thermal Management Market, CAGR |

10.56% |

| Middle East Data Center Thermal Management Market Size 2035 |

USD 1,856.42 Million |

Growth in the market is driven by rising AI workloads, liquid cooling adoption, and energy efficiency goals. Operators are investing in direct-to-chip cooling, smart airflow systems, and software-driven thermal optimization. Advanced thermal management helps reduce operational costs, extend equipment life, and meet environmental mandates. Businesses prioritize solutions that enable scalability, low latency, and sustainability. Innovation in cooling design is a strategic differentiator for hyperscale builds. Vendors focus on predictive control and modular hardware integration. The market offers strong value for investors targeting digital infrastructure growth in emerging tech zones.

UAE and Saudi Arabia lead the regional landscape, supported by hyperscale cloud zones and government-backed digital programs. Israel is an emerging market due to its AI and cybersecurity-focused data center growth. Qatar and Kuwait see expansion in enterprise and telecom deployments. Regional momentum is fueled by smart city projects, energy diversification, and regulatory support for green infrastructure. Each subregion presents varied infrastructure maturity, driving differentiated cooling demand.

Market Dynamics:

Market Drivers

Rising Adoption of Liquid Cooling and Free Cooling Solutions in High-Density Deployments

Data centers in the Middle East face extreme temperatures and growing AI workloads, pushing operators toward liquid and free cooling. These solutions offer higher efficiency and reduce energy consumption. High-density servers in hyperscale and enterprise facilities require thermal systems that maintain consistent uptime. Liquid cooling supports rack densities above 50 kW, which are now common across next-gen infrastructure. Free cooling, where applicable, helps lower power usage in colder subregions or at night. This shift directly impacts total cost of ownership and sustainability targets. The Middle East Data Center Thermal Management Market gains strong traction from this transition. It attracts both public and private sector investments seeking operational excellence.

- For instance, Microsoft disclosed lifecycle assessment results showing that cold plate liquid cooling can reduce total energy use by around 15–20% compared with traditional air cooling in high‑density data center environments. The company applies these findings across Azure facilities to guide deployment of liquid cooling for energy and sustainability optimization.

Technology Modernization Backed by AI, Digital Twins, and Smart Controllers

Thermal infrastructure upgrades involve AI-powered airflow controls, thermal modeling, and digital twin simulations. Operators implement predictive cooling to optimize fan speeds, reduce hot spots, and cut power usage. Software-defined controls with machine learning extend equipment life and enhance precision. AI integration enables dynamic workload-based thermal control, especially critical in multi-tenant environments. Digital twins allow real-time simulation and thermal scenario testing. These innovations reshape traditional HVAC operations. It gives facility managers deeper visibility and faster fault response. The Middle East Data Center Thermal Management Market gains strategic significance as innovation-led thermal designs attract global partnerships.

Growth in Colocation and Hyperscale Ecosystems Driving Standardization of Thermal Systems

Demand for hyperscale and colocation data centers is rising in UAE, Saudi Arabia, and Israel. These facilities require scalable and modular thermal systems with uniform operating parameters. Vendors standardize cooling architectures for quick deployments and seamless retrofits. Rack-based liquid cooling and scalable chilled water systems lead such designs. Large data center operators demand pre-engineered cooling modules with high redundancy. Global cloud providers ensure regional facilities comply with LEED and ASHRAE guidelines. Thermal standardization simplifies compliance and accelerates buildout timelines. The Middle East Data Center Thermal Management Market supports this trend by aligning product innovation with global hyperscale needs.

- For instance, Equinix is enabling liquid cooling deployments, including direct-to-chip systems, across its IBX data centers to support high-density AI workloads. These systems enhance thermal efficiency and allow greater rack power densities in select global locations.

Regulatory Pressure and Energy Efficiency Mandates Fueling Technology Adoption

Governments in the Middle East promote sustainability through green building codes and energy mandates. Countries like the UAE enforce thermal management requirements under national sustainability frameworks. Energy subsidies are reducing, pushing operators to cut cooling-related OPEX. Utility providers reward efficient thermal load distribution through pricing incentives. PUE targets below 1.4 have become a baseline for new projects. Builders use evaporative, indirect air, and hybrid cooling to meet these goals. Regulatory compliance drives design optimization, material selection, and cooling redundancy. The Middle East Data Center Thermal Management Market remains critical for achieving ESG alignment in digital infrastructure.

Market Trends

Rise of Modular and Containerized Cooling Units for Remote and Edge Deployments

Remote edge data centers in oilfields, border regions, and rural zones demand modular cooling. Prefabricated cooling containers with integrated fans and liquid loops are preferred. These systems allow plug-and-play functionality in low-infrastructure environments. Cooling loads up to 100 kW per container are now supported. Telecoms and government agencies deploy these for data security and fast latency. Mobile network upgrades push edge locations, requiring ruggedized thermal systems. Operators choose quick-to-deploy cooling pods to ensure continuity. The Middle East Data Center Thermal Management Market embraces modularity to serve distributed infrastructure efficiently.

Convergence of Cooling Systems with Renewable Energy Sources and Storage Solutions

Thermal systems are integrating with renewable energy and battery storage in data centers. Operators use solar-powered chillers and hybrid energy-cooling loops to reduce grid pressure. In the Gulf, solar cooling pairs with absorption systems and thermal energy storage. This reduces reliance on diesel backup systems and supports green goals. Cooling at night is supported by battery-powered air units. Combined systems provide energy load balancing and peak demand control. Developers align such solutions with national clean energy plans. The Middle East Data Center Thermal Management Market aligns with low-carbon strategies across new builds.

Development of Cooling-as-a-Service (CaaS) Models by Specialized Vendors

Cooling-as-a-Service is gaining adoption in large colocation and enterprise environments. Vendors offer performance-based contracts with outcome-linked billing. CaaS includes real-time monitoring, predictive maintenance, and remote operations. Clients benefit from predictable costs, SLA-backed uptime, and latest cooling tech. It reduces CAPEX and shifts thermal infrastructure to an OPEX model. Vendors retain ownership of cooling equipment, driving continuous upgrades. This model suits data centers seeking rapid scale without thermal downtime. The Middle East Data Center Thermal Management Market supports CaaS growth as buyers prefer outcome-linked cooling models.

Adoption of Immersion Cooling in AI and HPC Workloads Accelerates Thermal Innovation

High-performance computing and AI training workloads demand advanced cooling. Immersion cooling handles power densities above 100 kW per rack. Liquid submersion reduces the need for airflow, fans, or chillers. Early adopters include research labs, crypto miners, and defense contractors. Vendors now offer two-phase and single-phase systems tailored for Middle Eastern climates. Immersion setups support higher server lifespan and easier thermal management. Operators save space, energy, and operational complexity. The Middle East Data Center Thermal Management Market attracts advanced workloads requiring immersion-level performance.

Market Challenges

High Capital Requirements and Infrastructure Constraints for Next-Gen Thermal Systems

Advanced thermal systems require high upfront investment in both equipment and facility redesign. Retrofit projects face constraints due to legacy architecture and limited ceiling or floor space. Many data centers in the Middle East are older and built without liquid cooling pathways. Integrating rear door heat exchangers or direct-to-chip loops requires downtime and space planning. Utility infrastructure in some locations lacks stability for scalable thermal loads. Operators hesitate to adopt new systems that need heavy reconfiguration. The Middle East Data Center Thermal Management Market faces resistance from operators focused on short-term ROI or lacking retrofit capabilities.

Lack of Skilled Workforce and Thermal System Specialists in Emerging Data Center Hubs

Several Tier 2 cities and emerging hubs lack trained professionals in thermal system design and management. This creates dependence on global vendors or outsourced project teams. Long project timelines, import restrictions, and design mismatches often occur. Skilled technicians for immersion cooling or software-based thermal tuning remain scarce. Training gaps also affect maintenance quality and troubleshooting. Remote or hybrid facilities require 24/7 monitoring, which local teams often cannot support. The Middle East Data Center Thermal Management Market depends heavily on global players to bridge local talent gaps.

Market Opportunities

Surge in Government-Backed Smart City and AI Cloud Initiatives Across GCC Nations

Government initiatives in Saudi Arabia, UAE, and Qatar include smart cities, digital ID systems, and AI research zones. These demand scalable, energy-efficient, and low-latency data infrastructure. Thermal systems play a critical role in meeting uptime and sustainability goals. Cloud parks and tech free zones offer tax breaks for efficient designs. The Middle East Data Center Thermal Management Market offers vendors opportunities to deploy integrated thermal systems as part of national transformation plans.

Growing Demand for Retrofits, Upgrades, and Green Certifications Across Brownfield Sites

Operators across the Middle East are investing in cooling retrofits to meet ESG goals and reduce PUE. Certified upgrades help secure clients and government incentives. Software overlays and modular add-ons reduce disruption in ongoing operations. The retrofit segment offers strong opportunities in legacy facilities. The Middle East Data Center Thermal Management Market enables energy-saving retrofits with short ROI cycles.

Market Segmentation

By Data Center Size

Large data centers dominate the Middle East Data Center Thermal Management Market due to hyperscale cloud, telecom, and government projects. These centers host high-density workloads, pushing adoption of liquid cooling and AI-optimized airflow. Medium-sized facilities follow, especially among enterprises and colocation providers. Small data centers contribute a smaller share, but edge deployments are growing in remote and strategic locations.

By Cooling Technology

Air-based cooling remains dominant, especially hot/cold aisle setups and direct air systems in conventional builds. However, liquid-based cooling is gaining ground in AI and high-density racks, with direct-to-chip and immersion cooling deployed in newer facilities. Hybrid cooling is rising as operators balance efficiency and legacy compatibility. Phase-change and thermoelectric systems hold niche roles in specialized or rugged deployments.

By Component

Hardware components drive the largest revenue share in the Middle East Data Center Thermal Management Market. Chillers, heat exchangers, and airflow units are core to thermal infrastructure. Software components like AI optimization and DCIM tools are expanding fast. Services like preventive maintenance and retrofits offer recurring revenue streams and vendor lock-in potential.

By Hardware

Cooling units and chillers form the backbone of hardware demand. Fans and airflow devices follow, especially in air-cooled builds. Piping, sinks, and distribution systems grow with liquid cooling adoption. Vendors focus on modular and redundant hardware for high uptime facilities. Secondary components support backup systems and airflow balancing.

By Software

DCIM dashboards remain widespread for basic thermal visibility. AI-powered modules grow rapidly due to their impact on energy savings. CFD simulations support thermal modeling in high-density facilities. BMS modules integrate thermal systems with facility-wide operations. Software enables smarter cooling and predictive control.

By Services

Installation and commissioning are key for greenfield facilities, while retrofits dominate brownfield upgrades. Preventive maintenance ensures thermal performance and equipment life. Monitoring as a service gains traction among remote operators. Vendors offer bundled services to simplify lifecycle management.

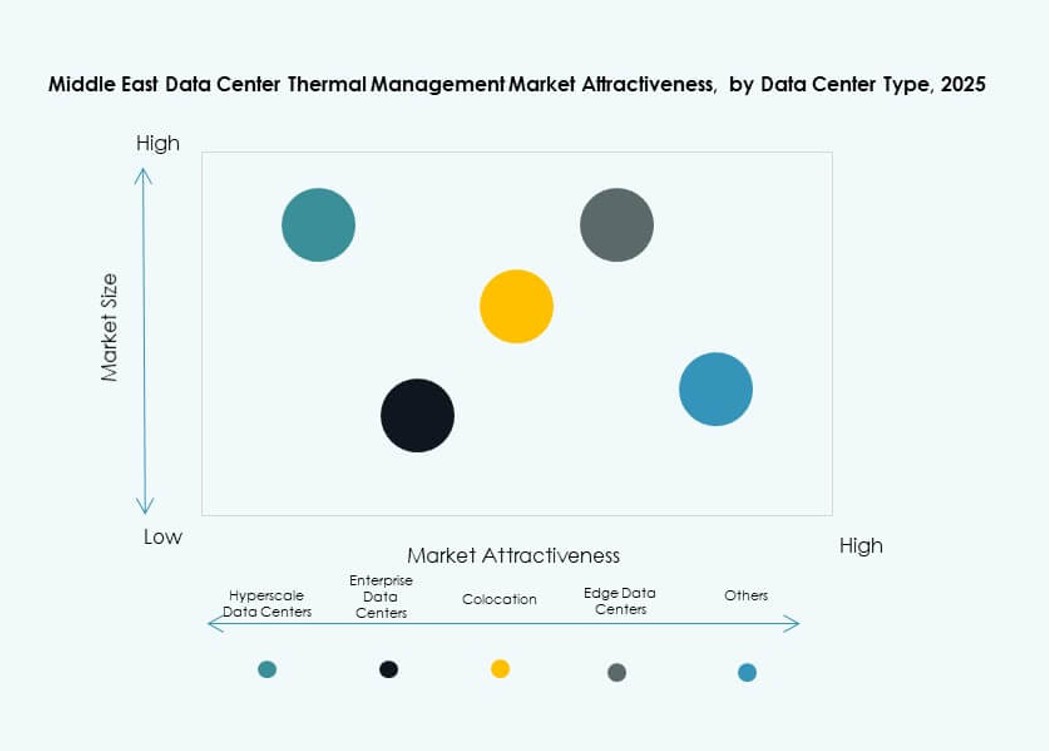

By Data Center Type

Hyperscale and colocation facilities lead the market due to massive workloads and density targets. Enterprise data centers follow, often prioritizing cost and uptime. Edge and micro data centers are rising, especially in remote or defense-linked applications. Their thermal needs push containerized or modular cooling innovation.

By Structure

Room-based cooling dominates legacy facilities but faces limits in scalability and control. Rack- and row-based cooling is expanding due to its efficiency and modularity. Liquid-cooled racks lead in AI-focused builds. Operators prefer flexible, scalable thermal layouts that match future workloads.

Regional Insights

Gulf Cooperation Council (GCC) Countries Hold Over 70% Market Share Due to High-Density Facilities and AI Workloads

Saudi Arabia, UAE, and Qatar dominate the Middle East Data Center Thermal Management Market with over 70% share. They host hyperscale builds, smart city projects, and sovereign cloud platforms. These require low PUE, advanced cooling, and 24/7 reliability. UAE’s Dubai and Abu Dhabi lead with energy-efficient designs in free zones. Saudi Arabia’s NEOM and Riyadh tech clusters drive future demand.

- For instance, Microsoft and G42 announced a 200 MW data center capacity expansion in the UAE in November 2025 to support AI and cloud infrastructure.

Levant Region and Israel Emerging with AI Research, Colocation Expansion, and Startup Cloud Clusters

Israel and Jordan show growing demand for high-performance thermal systems. Israel’s AI and cybersecurity startups require dense colocation spaces. Energy costs and environmental goals push advanced thermal solutions. Jordan’s rise in telecom infrastructure also supports regional demand. These countries contribute over 15% share, with rising vendor activity.

Rest of Middle East Including Iraq, Oman, Bahrain and Kuwait Showing Gradual Growth

Smaller Gulf nations are expanding enterprise and telecom data centers. Kuwait and Bahrain invest in national clouds and smart finance infrastructure. Oman and Iraq see edge facility growth linked to oil and logistics sectors. These regions together contribute close to 10–15% of the Middle East Data Center Thermal Management Market. Growth depends on stability, investment, and skilled resource availability.

- For instance, Qatar is investing in hyperscale data center builds that emphasize advanced cooling solutions to handle high‑density racks and support AI workloads. These projects reflect broader regional demand for efficient thermal management in large‑scale facilities.

Competitive Insights:

- Vertiv Group Corp.

- Schneider Electric

- Johnson Controls International plc

- Trane Technologies plc

- Daikin Industries Ltd.

- Huawei Technologies Co., Ltd.

- Fujitsu Limited

- Delta Electronics, Inc.

- Airedale International Air Conditioning Ltd.

- Munters Group AB

The Middle East Data Center Thermal Management Market is highly competitive, driven by the push for energy-efficient and high-density thermal solutions. Global vendors like Vertiv, Schneider Electric, and Johnson Controls lead the market with broad portfolios in air, liquid, and hybrid cooling systems. Regional expansions and partnerships help them secure contracts across hyperscale and colocation builds. Huawei and Delta Electronics focus on integrated power-cooling ecosystems, offering compact, modular solutions. Vendors invest in AI-based controls, direct-to-chip, and immersion cooling to meet rising thermal loads. The market favors those with service depth, retrofit capabilities, and energy performance guarantees. It continues to attract innovation-driven players looking to address climate-specific cooling needs in the region.

Recent Developments:

- In November 2025, Khazna Data Centers partnered with Eni to develop a 500 MW AI data center campus, marking a key step in its European expansion and sustainable AI infrastructure growth.

- In February 2024, MedOne Data Centers announced plans to build two new underground data centers near Tel Aviv, investing $270 million in facilities spanning over 85,000 square meters with 90 MW capacity across seven sites in Israel.