Executive summary:

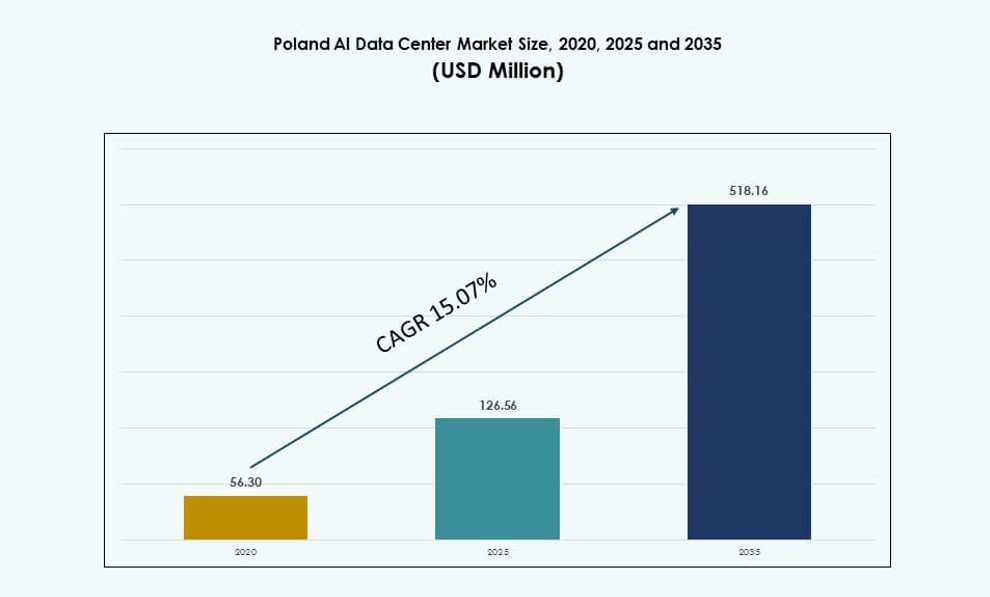

The Poland AI Data Center Market size was valued at USD 56.30 million in 2020 to USD 126.56 million in 2025 and is anticipated to reach USD 518.16 million by 2035, at a CAGR of 15.07% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Poland AI Data Center Market Size 2025 |

USD 126.56 Million |

| Poland AI Data Center Market, CAGR |

15.07% |

| Poland AI Data Center Market Size 2035 |

USD 518.16 Million |

Rapid AI adoption, enterprise modernization, and demand for GPU-optimized infrastructure are reshaping Poland’s digital backbone. Hyperscale expansions, hybrid deployments, and cloud-native workloads are driving infrastructure upgrades across industries. Companies are deploying AI for automation, fraud detection, and decision intelligence. Liquid cooling, smart orchestration, and power efficiency are key focus areas in new builds. Government incentives, digital policy clarity, and EU compliance norms make Poland a reliable destination for AI-hosting. Investors prioritize energy security, scalability, and latency performance.

Warsaw leads the market due to advanced connectivity, power reliability, and cloud region presence. It hosts major colocation and hyperscale operators, serving finance, telecom, and public sector clients. Kraków and Wrocław are emerging as secondary hubs, backed by strong R&D ecosystems and university collaboration. Gdańsk and Poznań see increased edge deployments due to proximity to logistics and manufacturing corridors. Poland’s central location supports low-latency cross-border workloads with Germany, Czechia, and the Baltics. Diverse regional growth strengthens infrastructure resilience and workload distribution. The Poland AI Data Center Market continues to attract both domestic and international operators.

Market Dynamics:

Market Drivers

Rise of AI-Intensive Workloads Accelerating Investments in Compute-Dense and Power-Efficient Data Centers

The Poland AI Data Center Market is expanding rapidly due to AI workloads demanding high-density compute environments. Enterprises are deploying GPU clusters and HPC systems to support training and inference at scale. Power efficiency has become critical, pushing adoption of liquid cooling and modular architecture. AI-specific demand from BFSI, healthcare, and manufacturing continues to expand IT infrastructure requirements. Operators are optimizing rack space and power draw to meet enterprise SLAs. It is becoming a priority location for resilient AI infrastructure in Central Europe. Real-time analytics, fraud detection, and process automation applications require low-latency, high-throughput systems. Investments are scaling due to hybrid AI workloads across edge and core deployments. The country is positioned as a strong growth zone for compute infrastructure.

- For instance, Beyond.pl operates a 100 MW data center campus in Poznań equipped to support high-density AI workloads with advanced cooling technologies. The site includes infrastructure optimized for rack densities of up to 140 kW and supports sovereign AI services aligned with EU compliance standards.

Cloud and Hybrid Models Driving New Infrastructure Standards and Deployment Flexibility

Flexible deployment models are enabling diverse AI applications across sectors. Enterprises are migrating legacy systems to hybrid environments combining on-premise control with cloud scalability. This shift is prompting demand for secure, modular data center facilities designed for variable workloads. Hyperscalers are investing in regions offering favorable energy pricing and tax incentives. The Poland AI Data Center Market supports containerized, AI-optimized workloads in both private and public environments. AI adoption in edge use cases is also growing, enabling fast inference closer to endpoints. Businesses demand infrastructure capable of managing increasing data gravity and workload shifts. It supports enterprises in accelerating time-to-insight with AI-native designs. Modernization efforts are transforming older facilities into GPU-ready environments.

- For instance, Atman secured PLN 1.35 billion in financing in April 2024 to expand its WAW‑3 data center campus near Warsaw, adding colocation space and supporting high‑density compute environments for AI workloads. This financing will help scale the campus to house more than 50,000 servers and significant IT capacity across multiple buildings.

Enterprise Digital Transformation and Local AI Policy Framework Fuel Infrastructure Demand

Government-led digital initiatives are fostering AI-driven modernization in public and private sectors. National strategies aim to develop smart infrastructure, digital health platforms, and intelligent transport systems. These require scalable, low-latency compute across distributed data center nodes. Public sector procurement frameworks now encourage domestic data hosting to align with sovereignty standards. The Poland AI Data Center Market benefits from this regulatory clarity, reducing operational risk for investors. Enterprise AI labs and R&D centers are adopting private clouds integrated with training clusters. Tax benefits, grants, and EU funding schemes support deployment of AI infrastructure. Public-private partnerships are advancing AI capabilities in industrial hubs. It is emerging as a testbed for sovereign AI innovation.

AI-Driven Automation Demands More Scalable, Intelligent, and Predictive Infrastructure Systems

Wider use of AI in IT operations is transforming how data centers are managed and maintained. Predictive analytics, automation, and DCIM platforms are now standard in new builds. These systems optimize power, cooling, and server utilization in real time. The Poland AI Data Center Market benefits from this shift toward self-operating infrastructure. AI workloads are also increasing the complexity of orchestration layers and container platforms. The need for software-defined architecture is growing alongside hardware upgrades. Investors view AI-ready facilities as long-term assets with high ROI potential. Strategic location and access to technical talent reinforce Poland’s competitiveness. It is helping to standardize next-generation infrastructure management across the region.

Market Trends

Liquid Cooling Adoption Gaining Momentum with High-Density Rack Deployments Across AI Facilities

Cooling innovation is reshaping facility design to support racks exceeding 40 kW density. Liquid-based systems, including rear-door heat exchangers and direct-to-chip, are being installed to reduce energy use. The Poland AI Data Center Market is witnessing pilot deployments in new enterprise and colocation facilities. Thermal performance, maintenance efficiency, and space optimization are driving the trend. Vendors are bundling servers with pre-integrated cooling components for quick deployment. Demand is growing in metro zones where land and energy constraints limit scale. Sustainability compliance is also influencing cooling technology choices. Operators aim to reduce PUE levels and qualify for EU green data funding. Rack density upgrades will remain a core trend in future builds.

AI-Enabled Energy and Capacity Management Tools Becoming Integral to Operational Efficiency Strategy

Operators are deploying AI-driven platforms to monitor load, energy use, and server health. Machine learning models predict faults, optimize cooling, and balance workloads across nodes. The Poland AI Data Center Market is integrating such tools into its high-performance clusters. Smart power management is essential to meet regulatory and enterprise sustainability targets. These systems reduce human error and improve decision-making speed. Operators rely on real-time insights to increase uptime and reduce operational cost. Facilities use intelligent orchestration to maximize GPU utilization during AI model training. AI adoption in data center management is scaling across Tier III and Tier IV builds. It supports long-term viability in a competitive and power-constrained environment.

Edge and Micro Data Center Models Expanding to Support AI Workloads in Industrial Zones

AI is moving closer to devices, sensors, and machines in localized environments. Micro data centers are gaining traction to process inference tasks without sending data to core facilities. In the Poland AI Data Center Market, operators are launching 5–10 rack systems near logistics hubs and smart factories. These systems are compact, energy-efficient, and optimized for real-time analytics. AI use in predictive maintenance, video analytics, and autonomous systems drives edge demand. Regional ISPs and mobile operators also integrate AI edge nodes for content delivery. Low-latency performance is essential for emerging 5G-enabled use cases. Businesses prefer local hosting to reduce cost and improve compliance. Growth of IoT platforms sustains this edge AI trend.

AI Data Sovereignty and Security Compliance Reshaping Infrastructure Procurement Requirements

Firms are adapting their infrastructure planning to align with EU digital sovereignty rules. This includes hosting sensitive AI data within national borders and securing it with zero-trust frameworks. The Poland AI Data Center Market sees increased demand for sovereign cloud zones and segmented environments. Enterprises in BFSI, healthcare, and government seek full control over AI training pipelines. This influences how compute clusters, storage arrays, and orchestration tools are deployed. Operators build secure AI-ready zones with physical and virtual isolation. Compliance is no longer optional, but a prerequisite for growth in sensitive sectors. Market players differentiate on security posture and regulatory alignment. Sovereignty is now a competitive advantage in winning large-scale AI contracts.

Market Challenges

Power Supply Constraints and Energy Pricing Volatility Limit Scalability of High-Density Infrastructure

Growing demand for AI compute clusters is placing stress on the national power grid. Many urban zones face limited substation capacity and slower permitting processes. The Poland AI Data Center Market is impacted by high electricity pricing volatility and uncertainty in energy contracts. These issues complicate ROI calculations for hyperscale and colocation investors. Operators require stable energy cost models to support long-term infrastructure planning. Grid resilience and renewable energy integration remain uneven across subregions. Cooling systems add further power demand, especially in high-density GPU clusters. Delays in grid upgrades threaten capacity expansion timelines. Energy security remains a top concern for operators and enterprise clients.

Workforce Gaps, Skill Shortages, and Regulatory Complexity Raise Barriers to AI Data Center Growth

Building and managing AI-ready facilities requires specialized design, operations, and software integration skills. The Poland AI Data Center Market faces talent shortages in fields like network automation, GPU orchestration, and liquid cooling systems. Educational and training pipelines are catching up but remain limited. Regulatory uncertainty around environmental standards and data localization adds further complexity. Navigating overlapping EU and national guidelines slows down site selection and compliance approvals. Small operators struggle to keep pace with changing technical and legal demands. Cybersecurity staffing gaps create risk in managing sovereign AI clusters. Policy and workforce gaps remain structural challenges for market acceleration.

Market Opportunities

Cross-Border AI Workloads and EU Sovereignty Mandates Unlock Long-Term Investment Potential

The Poland AI Data Center Market benefits from its position as a regional bridge for East–West data flows. Rising AI investments in nearby EU states make Poland an ideal hub for latency-sensitive training and inference. Businesses seek compliant, sovereign-aligned infrastructure that meets both EU and national standards. Proximity to Germany, Czechia, and Baltics adds to the strategic value. Investors view Poland as a resilient expansion market for AI-oriented campuses.

Public-Private Partnerships and Incentives Boost Infrastructure Build-Out in Emerging AI Zones

Government-backed initiatives aim to develop AI zones through subsidies, land grants, and training support. The Poland AI Data Center Market benefits from smart city plans, digital sovereignty incentives, and energy innovation zones. Partnerships with universities and local governments help de-risk new builds. It encourages startups and global players to co-develop scalable infrastructure.

Market Segmentation

By Type

The hyperscale segment dominates the Poland AI Data Center Market due to rising demand from cloud service providers and enterprise AI labs. Hyperscale operators are expanding their footprint in Warsaw and surrounding tech corridors to support training clusters and sovereign AI workloads. Colocation and enterprise data centers follow, driven by growing demand from BFSI and retail clients. Edge or micro data centers are emerging as localized nodes for real-time inference and IoT processing.

By Component

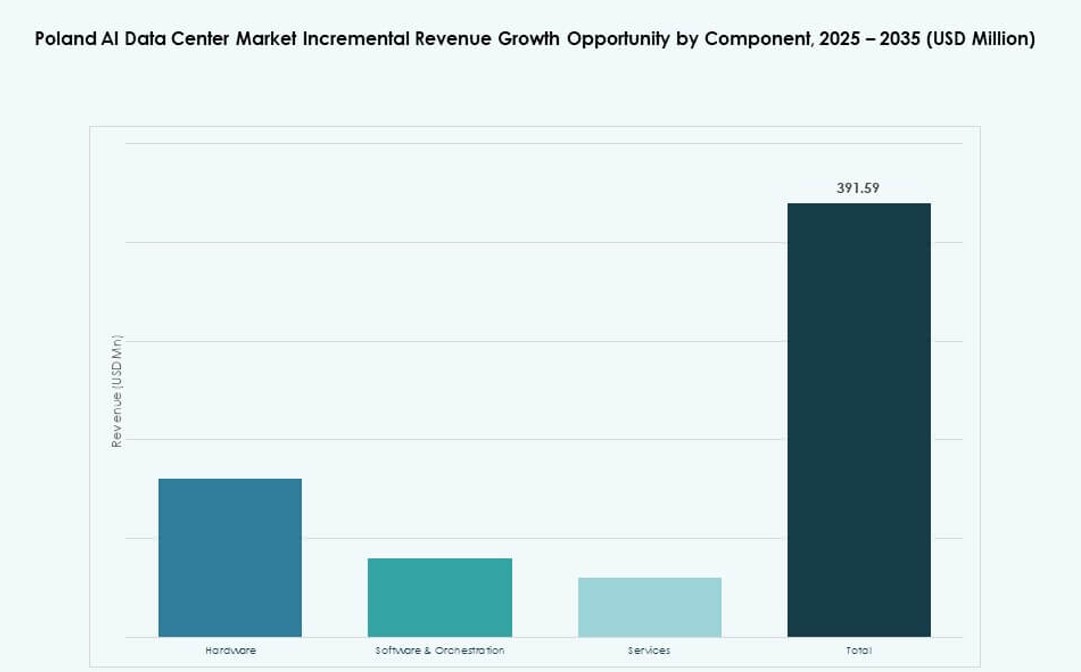

Hardware holds the largest share in the Poland AI Data Center Market due to increasing GPU cluster deployments, networking gear upgrades, and rack-level infrastructure improvements. Demand for liquid cooling units and high-speed interconnects supports the hardware lead. Software and orchestration are growing as enterprises adopt containerization, AI pipelines, and workload automation. Services are expanding as operators seek consulting, integration, and lifecycle management for complex deployments.

By Deployment

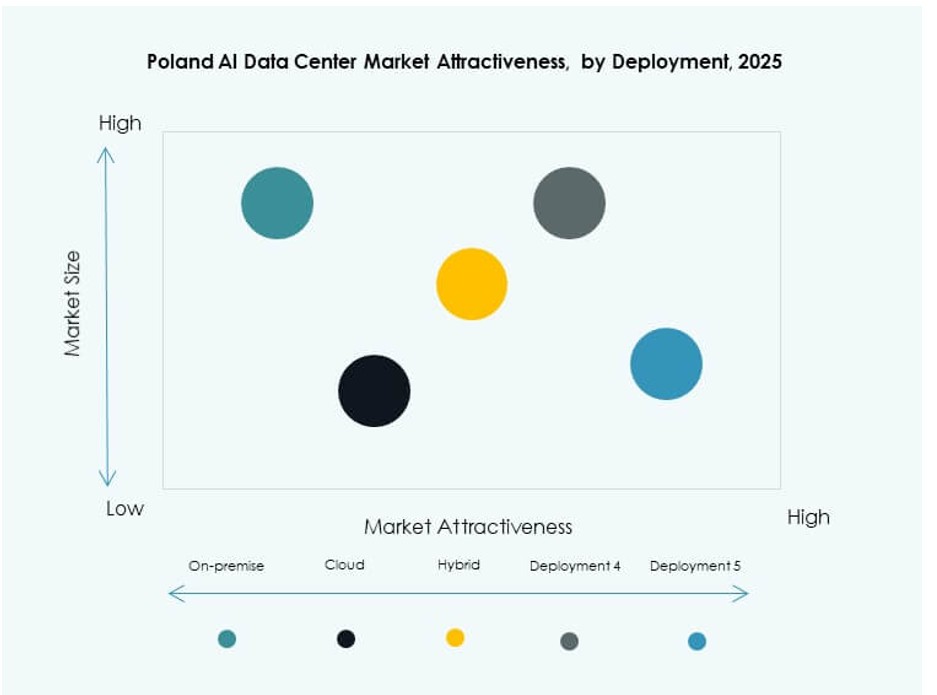

The cloud deployment model leads the Poland AI Data Center Market, driven by scalable, on-demand compute needs for AI training. Enterprises prefer cloud for cost-efficiency and rapid provisioning. On-premise models remain strong in public sector and regulated verticals requiring full data control. Hybrid deployment is growing rapidly, combining cloud agility with local compliance, especially in finance and healthcare.

By Application

Machine Learning (ML) leads application segments in the Poland AI Data Center Market due to wide enterprise adoption in analytics, automation, and modeling. Generative AI (GenAI) is the fastest-growing, with businesses exploring AI-assisted content, code, and media generation. Natural Language Processing (NLP) follows due to chatbot and document processing use cases. Computer Vision (CV) supports manufacturing, logistics, and surveillance. Others include speech recognition and recommendation engines.

By Vertical

The IT and telecom segment dominates the Poland AI Data Center Market due to native infrastructure demand and AI-driven services. BFSI and healthcare are key growth verticals for secure, compliant, and real-time processing. Manufacturing and automotive sectors adopt AI for quality control and predictive maintenance. Retail uses AI for personalization, while media and entertainment demand compute for rendering and content generation. Others include education and energy.

Regional Insights

Warsaw Region Leads with Over 65% Market Share Due to Infrastructure Density and Cloud Connectivity

The Warsaw metropolitan area accounts for over 65% of the Poland AI Data Center Market. It offers reliable power, advanced fiber networks, and access to skilled IT talent. Major cloud service providers and colocation operators anchor their Polish operations in this region. AI firms prefer Warsaw for hosting training clusters and compliance zones. The region continues to receive new investment in AI-ready capacity. It serves as Poland’s primary digital infrastructure hub.

- For instance, Google Cloud’s Warsaw region supports A2‑highgpu virtual machines with up to 8 NVIDIA A100 40GB GPUs per instance for AI workloads. These instances enable high‑performance training and inference operations across machine learning and data science applications in Central Europe.

Southern Poland Including Kraków and Wrocław Emerges with 20% Share Backed by Tech Ecosystems

Southern cities like Kraków and Wrocław contribute around 20% of the Poland AI Data Center Market. Presence of top universities, R&D centers, and software companies supports localized AI infrastructure demand. Colocation providers are launching compact, high-density facilities near tech parks. These regions attract enterprise clients in finance, education, and retail. Investments are driven by favorable land costs and growing digital services ecosystems. It strengthens regional diversity in infrastructure planning.

- For instance, Microsoft’s Poland Central region provides Azure services with availability zones designed to support enterprise and AI workloads. The region ensures in‑country data residency and low‑latency cloud access, serving public sector and commercial clients across Poland.

Northern and Western Poland Hold the Remaining 15% Driven by Edge Growth and Cross-Border Proximity

Northern and western parts of Poland, including Gdańsk and Poznań, contribute around 15% of the market. These zones are gaining relevance due to edge deployments, cross-border data flow, and improved energy availability. Operators are deploying micro data centers in logistics hubs and border zones. Access to Baltic and Western European fiber routes improves latency and service quality. It supports use cases like smart ports, autonomous transport, and content delivery. Regional growth reflects decentralization of compute.

Competitive Insights:

- Microsoft (Azure)

- Google Cloud / Alphabet

- Amazon Web Services (AWS)

- Equinix

- pl

- ATM S.A.

- Netia Data Centers

- Digital Realty Trust

- Dell Technologies

- NVIDIA

The Poland AI Data Center Market is shaped by a mix of global hyperscalers, regional colocation providers, and technology infrastructure vendors. Hyperscale players like AWS, Microsoft, and Google Cloud lead in AI workload hosting with GPU-rich architectures and scalable platforms. Local firms such as Beyond.pl and ATM S.A. offer sovereign-compliant, edge-ready infrastructure tailored for regulated sectors. Netia and Equinix support enterprise hybrid workloads with high connectivity and urban proximity. Infrastructure vendors like Dell, HPE, and NVIDIA are embedding AI optimization into hardware stacks. The market remains competitive with growing focus on liquid cooling, power efficiency, and AI-native orchestration. It is transitioning from traditional hosting to next-gen platforms that support GenAI, machine learning, and NLP at scale.

Recent Developments:

- In October 2025, Beyond.pl announced a partnership with Deloitte to deliver sovereign AI solutions for businesses in Poland. The collaboration focuses on combining Beyond.pl’s AI infrastructure with Deloitte’s consulting capabilities to support secure, compliant enterprise AI deployments.

- In May 2025, Beyond.pl launched a DGX B200 SuperPOD‑based AI factory at its Poznań data center campus in Poland. The facility offers AI and GPU‑as‑a‑Service support for enterprise clients and managed services, positioning it among the first full‑suite AI infrastructure platforms in Central and Eastern Europe.

- In February 2025, Microsoft announced a PLN 2.8 billion investment by June 2026 to expand its hyperscale cloud and AI infrastructure across existing data center campuses in Poland, enhancing Azure services to meet regional demand and support national cybersecurity collaboration with Polish National Defense.