Executive summary:

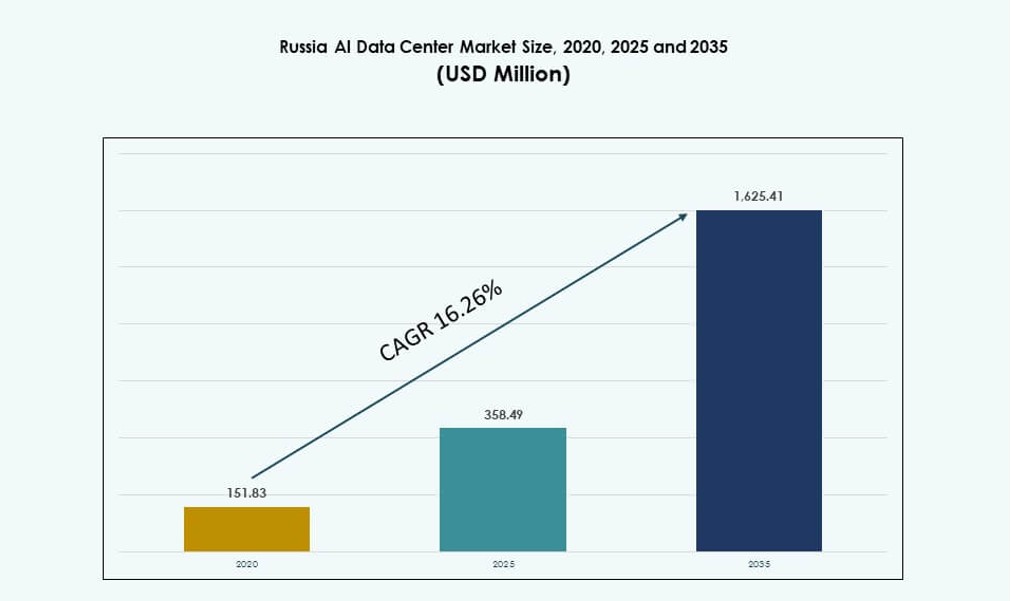

The Russia AI Data Center Market size was valued at USD 151.83 million in 2020 to USD 358.49 million in 2025 and is anticipated to reach USD 1,625.41 million by 2035, at a CAGR of 16.26% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Russia AI Data Center Market Size 2025 |

USD 358.49 Million |

| Russia AI Data Center Market, CAGR |

16.26% |

| Russia AI Data Center Market Size 2035 |

USD 1,625.41 Million |

Strong government backing for digital sovereignty, rapid AI model deployment, and rising adoption of hybrid infrastructure are fueling market expansion. Enterprises invest in GPU-powered platforms, while state-backed projects anchor high-density compute zones. Innovation in open-source AI and national hardware ecosystems aligns with data localization laws. This transformation shapes demand for scalable and secure AI-ready facilities. The market plays a strategic role in supporting national technology independence. It is also attracting institutional investment as AI infrastructure becomes a critical digital backbone.

The Central Federal District leads due to Moscow’s dominance in connectivity, data traffic, and enterprise density. Northwestern regions, particularly St. Petersburg, are emerging through academic and research-driven collaborations. Industrial zones in Volga and Siberia are expanding edge deployments for remote and resource-heavy workloads. Climate suitability and power availability also influence regional distribution. These patterns reflect strategic planning aligned with national AI development goals. The Russia AI Data Center Market continues to grow through geographically diverse but policy-driven infrastructure rollouts.

Market Dynamics:

Market Drivers

Rising National Investment in Digital Sovereignty and Domestic AI Capabilities

Government strategies in Russia are driving local AI innovation and data center growth. National initiatives focus on reducing dependence on foreign platforms and boosting sovereign compute capacity. State-backed firms invest in scalable infrastructure to host advanced AI workloads. Edge and hyperscale projects receive funding aligned with AI development goals. Domestic chipset development supports this ambition. New laws also mandate local data storage, expanding infrastructure demand. The Russia AI Data Center Market benefits from this ecosystem of policy, funding, and strategic autonomy. It enables enterprises to comply with data sovereignty rules while innovating. These drivers make the market critical for domestic and regional stakeholders.

High-Density Infrastructure Demand Across Public and Private Sectors

Sectors including defense, finance, and energy deploy AI-driven models requiring high compute density. These use cases push data centers toward GPU-enabled, high-rack-density architectures. Operators invest in liquid cooling and modular designs to meet thermal loads. Advanced AI tasks such as LLMs and CV demand low-latency environments. State-linked industries adopt private cloud models optimized for AI. These sectors generate long-term infrastructure demand. It supports recurring upgrades across critical facilities. The Russia AI Data Center Market benefits from sustained growth in both state and commercial AI applications. It positions infrastructure as the backbone of future digital services.

AI Innovation Hubs in Tech Clusters Boosting Infrastructure Demand

Cities like Moscow, Kazan, and St. Petersburg host major AI R&D hubs. These zones anchor startup accelerators and corporate innovation centers. Local demand for compute expands with each new AI deployment. Data centers grow alongside university-linked AI labs and incubators. Their need for training infrastructure drives investment in scalable platforms. National programs support knowledge transfer between academia and enterprise. This concentration of users accelerates infrastructure buildout. The Russia AI Data Center Market thrives near these clusters. It creates regional growth hotspots tied to innovation activity.

- For instance, the Skolkovo Innovation Center in Moscow has supported over 2,500 tech companies since 2010, including many AI firms that rely on local compute and data center resources to develop and scale advanced solutions.

Hybrid Cloud Expansion Driven by Enterprise AI Adoption

Russian enterprises are adopting hybrid models for AI workloads. On-premise systems support sensitive data, while cloud platforms handle scale. Telecom and BFSI sectors lead this dual-stack transformation. Operators provide customized infrastructure combining control and elasticity. Enterprise AI adoption involves training, inference, and edge analytics. These workflows need diverse architectures across regions. Multi-zone and hybrid deployments become standard. The Russia AI Data Center Market is shaped by these evolving enterprise preferences. It supports demand for flexible, high-performance solutions across industries.

- For instance, YandexGPT models participated in the WMT25 translation tasks, leveraging hybrid training pipelines to improve English‑to‑Russian translation performance in competitive benchmarks.

Market Trends

Shift Toward Domestic Hardware and Open-Source AI Platforms

Import substitution policies are encouraging adoption of Russian-made hardware. Firms prioritize domestic GPU and CPU options for AI workloads. Baikal and Elbrus chips gain traction in compliance-driven sectors. Open-source frameworks like Sberbank’s RuGPT gain market share. Operators integrate these stacks into custom deployments. It reduces foreign dependency in infrastructure. Data centers focus on localized compatibility. The Russia AI Data Center Market supports this ecosystem shift. It leads to hardware-software alignment tailored to national needs.

Edge Infrastructure Growth to Support Remote and Industrial Workloads

Mining, oil, and logistics sectors require AI inferencing near operation sites. Edge data centers enable low-latency AI at remote and industrial zones. Ruggedized and modular facilities are deployed across Eastern and Northern Russia. These setups support computer vision, predictive maintenance, and telemetry tasks. AI clusters handle on-site processing before sending metadata to core centers. Edge facilities integrate with satellite and private 5G links. It unlocks AI for sectors outside metro zones. The Russia AI Data Center Market sees edge as an enabler of distributed intelligence.

Energy Optimization and Liquid Cooling Adoption Accelerating

Operators invest in energy-efficient infrastructure to manage rising AI power loads. Liquid cooling sees strong uptake in new builds with 30–50 kW rack densities. Free-air and immersion methods are tested in colder northern zones. These reduce operational costs while supporting high-density compute. AI workloads require sustained thermal stability. Power usage effectiveness (PUE) targets fall below 1.3 in advanced deployments. Incentives favor efficient builds under state-backed green tech programs. The Russia AI Data Center Market integrates energy and thermal innovation for AI-readiness.

AI Workload Customization for Russian Language and Regulation

Natural language models tailored for Cyrillic use cases gain traction. Enterprises deploy models fine-tuned for local compliance, finance, and legal domains. Public-sector use of AI in social services and urban planning fuels NLP growth. Custom AI stacks include language engines trained on Russian datasets. These require fine-tuned training clusters with regulatory controls. Content moderation and governance models integrate national policy standards. The Russia AI Data Center Market supports AI localization through secure compute platforms. It creates a unique layer of language-specific AI infrastructure.

Market Challenges

Limited Access to Global Semiconductor Supply Chains and Ecosystem Tools

Global export restrictions limit access to high-performance AI chips and support software. Domestic manufacturers struggle to match global performance benchmarks. Imports of GPUs and advanced accelerators remain unpredictable. This impacts rollout of high-density racks for training and inference. Cloud operators face delays in system integration and scaling. Vendor lock-in risks increase where local substitutes are not available. These barriers slow deployment cycles and limit performance gains. The Russia AI Data Center Market faces long-term capacity planning issues due to uncertain hardware access.

Operational Constraints in Expanding Beyond Metro Zones

Regional infrastructure faces power reliability, limited fiber, and harsh climate conditions. Building scalable AI-ready data centers outside urban cores remains difficult. Cooling systems require adjustments for extreme winter temperatures. Remote workforce training and retention further complicate operations. Local governments lack frameworks for AI facility approvals in rural zones. Logistics delays impact delivery of modular infrastructure components. These issues make regional AI infrastructure costlier and slower to deploy. The Russia AI Data Center Market contends with major hurdles outside key metro areas.

Market Opportunities

AI-Specific Cloud Services Expansion Across Regulated Industries

Enterprises demand private cloud solutions tuned for AI model training and governance. Operators can offer GPU-as-a-Service with compliance controls for sectors like BFSI and healthcare. These services enable fast scaling without losing control over data flows. The Russia AI Data Center Market can capture this demand by expanding vertical-specific AI cloud offerings.

Localized AI Training for National Language and Legal Domains

Opportunities exist in AI infrastructure tailored for Russian law, finance, and public sector systems. Government agencies and legal institutions require secure training environments. Specialized clusters can serve models optimized for local data, formats, and policy requirements. The Russia AI Data Center Market can enable these deployments through compliance-first architectures.

Market Segmentation

By Type

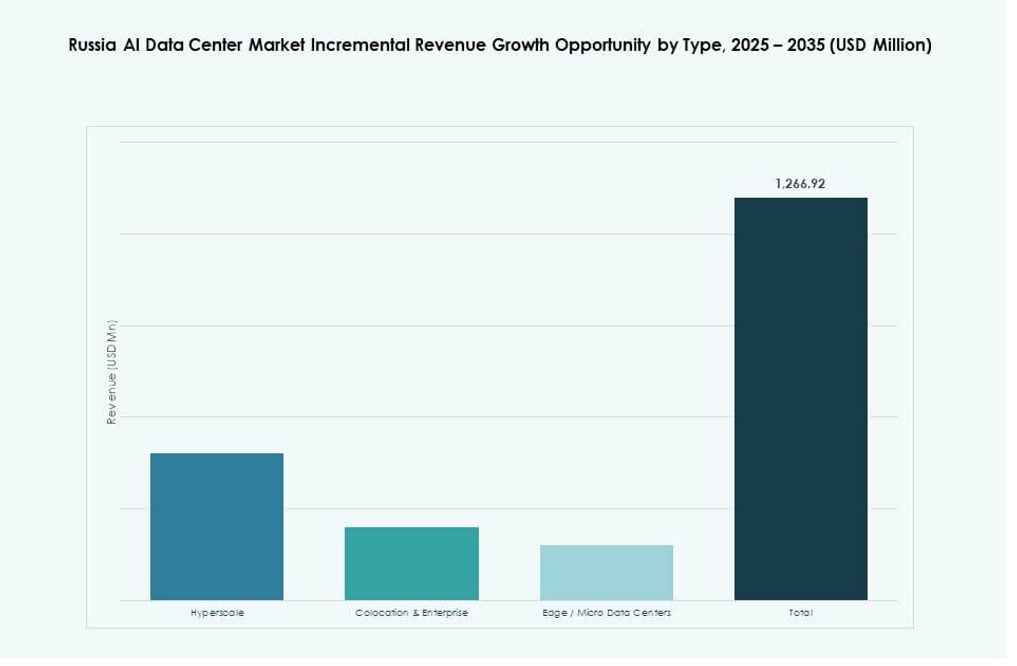

Hyperscale data centers dominate the Russia AI Data Center Market, supported by national AI infrastructure programs and public cloud growth. These large-scale deployments host most AI training workloads and offer strong scalability. Colocation and enterprise data centers serve regulated sectors needing physical control. Edge and micro data centers are emerging across industrial and remote zones. Edge adoption grows in energy and logistics, but hyperscale holds the majority share due to national AI projects.

By Component

Hardware holds the highest share in the Russia AI Data Center Market, driven by large-scale investment in GPU clusters, AI chips, and high-density racks. Infrastructure modernization prioritizes AI-ready servers and advanced cooling systems. Software and orchestration platforms grow steadily to manage AI workload pipelines. Services such as managed AI training environments and workload optimization tools gain traction in cloud-native and hybrid deployments. Hardware dominance reflects foundational investment trends in performance and capacity.

By Deployment

Hybrid deployment leads the Russia AI Data Center Market, balancing data sovereignty and AI scale requirements. Enterprises choose hybrid to manage sensitive workloads on-premise while using cloud for elasticity. On-premise models remain strong in government, defense, and banking, where compliance drives architecture. Cloud deployments grow among startups, research institutes, and tech firms. The hybrid model supports AI lifecycle management and compliance together. It enables flexible expansion while meeting sector-specific requirements.

By Application

Machine learning (ML) holds the largest share in the Russia AI Data Center Market, applied across defense, banking, and logistics. ML underpins recommendation engines, fraud detection, and industrial analytics. Natural language processing (NLP) gains momentum in legal, government, and enterprise chatbots. Computer vision (CV) grows in traffic monitoring, manufacturing, and security. Generative AI (GenAI) adoption remains nascent but rising in media and enterprise content tools. ML’s wide utility across sectors secures its dominance in application share.

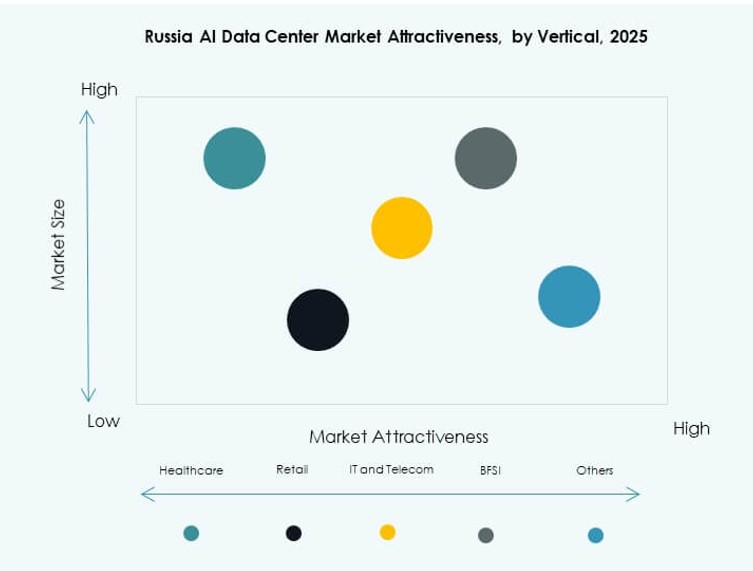

By Vertical

IT and telecom lead the Russia AI Data Center Market, leveraging infrastructure for both internal AI and customer services. BFSI and government follow closely, driven by automation, compliance, and AI innovation targets. Healthcare uses AI for imaging and diagnostics, fueling demand for secure and specialized facilities. Manufacturing and automotive apply AI to robotics, quality control, and logistics. Retail and media deploy AI for personalization and audience analytics. IT and telecom maintain dominance due to scale and ecosystem maturity.

Regional Insights

Central Federal District Holds Over 60% Share with Dense AI and Cloud Infrastructure

The Central Federal District, led by Moscow, holds over 60% market share in the Russia AI Data Center Market. It benefits from advanced power infrastructure, dense network interconnectivity, and regulatory oversight proximity. Moscow’s status as a tech and enterprise hub drives hyperscale and private cloud builds. National programs also concentrate R&D and funding within this zone. Operators prefer the region for pilot deployments and AI cluster development. This subregion maintains its leadership through policy, investment, and compute density alignment.

- For instance, Yandex announced the development of its largest data center in Kaluga Oblast, designed for over 3,800 server racks with a planned power capacity of 63 MW. The facility was planned to support Yandex’s core digital services and cloud infrastructure, strengthening compute capacity near the Moscow region.

Northwestern Federal District Emerging with 15% Share and Research-Driven Demand

The Northwestern Federal District, anchored by St. Petersburg, accounts for approximately 15% of the Russia AI Data Center Market. The area supports academic and enterprise collaborations in AI. Research institutions and government-backed accelerators drive infrastructure growth. Data centers in this region support training, simulation, and modeling for public sector projects. Proximity to Finland and the Baltics fosters cross-border knowledge exchange. While smaller than Central, the district attracts sustained public-private partnerships. It emerges as a regional AI innovation node.

- For instance, Rostelecom’s St. Petersburg data center in Kalininsky district opened in 2021 with 800 racks and 7.4 MW capacity. By 2024, it became part of a geo-distributed network optimized for AI workloads, supporting GPU-based clusters for machine learning and public sector services under its “Business Strategy 2025

Volga and Siberian Federal Districts Gain 10–12% Share from Edge and Industrial Deployments

Volga and Siberian Federal Districts hold a combined 10–12% share due to rising industrial AI use. Oil, gas, and mining sectors deploy edge data centers to process remote workloads. Cities like Kazan and Novosibirsk invest in tech hubs to support regional growth. Power availability and cold climates help optimize thermal costs. Local governments promote digitalization under national roadmaps. These districts show early signs of growth in AI-aligned infrastructure. The Russia AI Data Center Market expands cautiously into these regions.

Competitive Insights:

- Rostelecom Data Centers

- DataLine

- IXcellerate

- Microsoft (Azure)

- Amazon Web Services (AWS)

- Google Cloud

- Equinix

- Digital Realty Trust

- CoreWeave

- NVIDIA

The Russia AI Data Center Market features a mix of domestic operators and global cloud providers. Local players like Rostelecom, DataLine, and IXcellerate dominate compliance-driven deployments and serve public sector demand. Global hyperscalers such as Microsoft, AWS, and Google expand through joint ventures and strategic partnerships. Hardware and AI infrastructure vendors like NVIDIA and HPE support back-end integration, while colocation giants like Equinix and Digital Realty offer scalable capacity. It remains competitive due to sovereign infrastructure needs, with localized hardware, regulatory compliance, and edge deployments shaping differentiation. New entrants focus on AI-specific clusters, energy-efficient builds, and GPU-as-a-Service models. The market rewards players that align with regional policies, latency demands, and sector-specific use cases.

Recent Developments:

- In November 2025, IXcellerate completed land acquisition for its third Moscow campus near Vёshki. The expansion will deliver 7,500 rack spaces and over 130 MW of power across two new facilities, reinforcing it’s position as a key infrastructure provider in Russia’s digital economy.

- In July 2025, Russian telecom Megafon launched two new data centers in Yekaterinburg and Tver, each offering 1 MW capacity. The facilities expand the company’s infrastructure footprint and improve regional compute availability.