Executive summary:

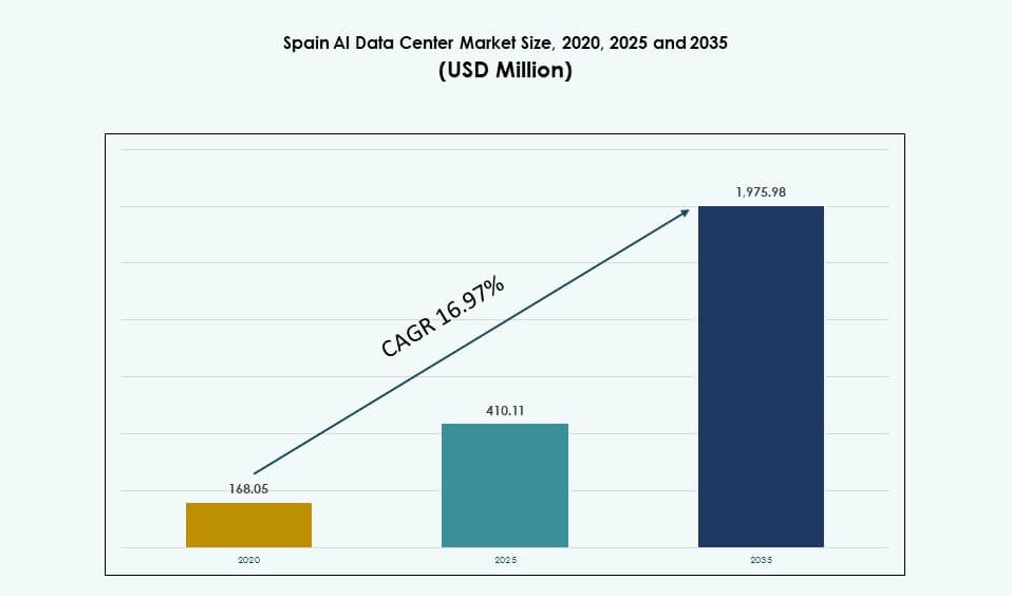

The Spain AI Data Center Market size was valued at USD 168.05 million in 2020 to USD 410.11 million in 2025 and is anticipated to reach USD 1,975.98 million by 2035, at a CAGR of 16.97% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Spain AI Data Center Market Size 2025 |

USD 410.11 Million |

| Spain AI Data Center Market, CAGR |

16.97% |

| Spain AI Data Center Market Size 2035 |

USD 1,975.98 Million |

Rising AI adoption across industries such as telecom, BFSI, healthcare, and manufacturing is transforming the data infrastructure landscape in Spain. Enterprises are scaling AI workloads for model training, analytics, and real-time automation, which drives demand for high-density data centers. Innovation in liquid cooling, GPU clusters, and edge computing continues to evolve. Spain’s supportive energy policies and cloud expansion initiatives strengthen its AI readiness. The market plays a key role for businesses seeking sovereign AI zones with sustainable performance. Its growth signals long-term opportunities for investors targeting AI-optimized infrastructure in Southern Europe.

Madrid leads the Spain AI Data Center Market with its dense enterprise base, robust connectivity, and hyperscale deployments. Barcelona is growing quickly, backed by tech talent, R&D hubs, and proximity to subsea cables. Cities like Valencia and Bilbao are emerging due to increased interest in edge and sovereign deployments. Regional strategies are shaped by zoning ease, green energy access, and low-latency demands. Spain’s geographic positioning supports both European and cross-border workloads. Infrastructure investments are expanding beyond core metros to serve distributed AI applications and industry-specific zones.

Market Dynamics:

Market Drivers

Government Digitalization Push and AI-Focused Policy Frameworks Fuel Infrastructure Modernization

Spain’s national digital strategy supports AI integration across public and private sectors. The Digital Spain 2026 initiative drives investments in AI and cloud infrastructure. It encourages data center deployment through subsidies, AI research funding, and 5G rollout. Public-private collaborations strengthen innovation and local workload processing. Regulatory stability makes Spain attractive for long-term capital investments. Smart city projects and public services modernization accelerate demand for localized compute. The Spain AI Data Center Market benefits from this multi-sector push. AI centers must meet growing government needs in healthcare, mobility, and public administration. It forms a reliable foundation for growth across AI infrastructure tiers.

- For instance, Telefónica expanded its 5G network to cover 94% of Spain’s population across 5,700 municipalities by late 2025, using 700 MHz and 3.5 GHz bands for advanced services.

AI Workload Growth Across Telecom, BFSI, and Healthcare Sectors Drives Compute Demand

The telecom sector upgrades its core networks with AI-optimized systems to manage traffic and security. BFSI players deploy AI for fraud detection, trading algorithms, and real-time decision engines. Healthcare groups rely on AI for diagnostics, imaging analysis, and electronic record systems. These sectors require powerful and scalable infrastructure. It increases demand for AI-ready data centers equipped with GPUs, accelerators, and low-latency storage. The Spain AI Data Center Market aligns with this industry-specific compute evolution. Operators tailor capacity for AI inferencing, training, and regulatory compliance. Sector-level AI adoption sets a sustained demand pipeline for high-density facilities.

Rising Renewable Energy Availability Enables Scalable and Sustainable Facility Expansion

Spain’s rich solar and wind energy base supports green data center development. The availability of renewable energy attracts global investors focused on carbon neutrality. It reduces long-term operating costs and aligns with sustainability commitments. AI workloads require dense, power-hungry compute nodes. Operators deploy liquid cooling and energy-efficient architectures to manage this demand. Government incentives for clean energy sourcing further strengthen the market. The Spain AI Data Center Market leverages these conditions to support high-density AI racks. Facilities in solar-rich southern regions attract large-scale builds. Environmental compliance and power resilience act as competitive differentiators.

- For instance, Google signed a 35 MW wind power purchase agreement with Exus Renewables in March 2025 to support its Spanish data center operations with clean energy, aligning with its carbon‑free energy goals.

AI and Edge Use Cases Expand Across Retail, Manufacturing, and Logistics Verticals

Retailers adopt AI for recommendation engines, demand forecasting, and cashierless stores. Manufacturers deploy computer vision and predictive analytics for quality control and automation. Logistics firms use AI for route optimization and last-mile tracking. These use cases require localized, high-speed compute infrastructure. It drives demand for smaller edge deployments in urban and industrial zones. The Spain AI Data Center Market sees rising investment in micro facilities supporting such latency-sensitive AI workloads. Edge-ready modules and regional deployments allow scaling closer to the application layer. It enables faster AI decisions and improved customer experiences.

Market Trends

Liquid Cooling and High-Density Rack Adoption Gain Traction to Support GPU Workloads

Spain-based facilities now deploy racks with densities exceeding 50 kW to run large-scale training models. Traditional air-cooled systems are being replaced with direct-to-chip and immersion cooling. Liquid-based solutions improve thermal efficiency and reduce energy consumption. Hyperscale and colocation providers retrofit sites to meet AI-specific thermal loads. High-performance GPUs like NVIDIA H100 require liquid-based infrastructure. It makes thermal design a core planning factor. The Spain AI Data Center Market reflects this with rising adoption of heat-reducing technologies. Operators align with global cooling trends to enable dense AI cluster growth.

AI-Optimized Interconnects and Storage Solutions Integrated Across Core and Edge Sites

AI workloads require ultra-low latency networks and fast NVMe-based storage stacks. Data centers in Spain invest in high-throughput fabrics and tiered memory systems. GPU-to-GPU interconnects such as NVLink become standard in high-performance clusters. Storage disaggregation allows flexible scaling of AI model data needs. The Spain AI Data Center Market shows this trend across both core and edge deployments. Edge facilities integrate compact, AI-ready storage with fast I/O pipelines. It helps meet compute demands for streaming, analytics, and AI at the edge.

AI-Specific Zoning, Permitting, and Data Sovereignty Rules Drive Location Preferences

Local governments streamline zoning approvals for AI and cloud data center builds. Compliance with Spain’s AI and data protection laws influences deployment zones. Operators prioritize regions with favorable tax policies and reduced bureaucratic hurdles. It impacts land acquisition and buildout timelines. The Spain AI Data Center Market aligns with regulations such as GDPR, AEPD guidelines, and EU AI Act. Sovereign cloud projects fuel growth near government hubs. New AI-specific legal frameworks shape site strategy across hyperscale and enterprise operators.

Integration of AI with Renewable-Powered Microgrids to Improve Operational Resilience

Operators design facilities with AI-driven energy optimization using onsite renewables and microgrids. AI models forecast power demand, balance loads, and support outage recovery. Spain’s solar-rich zones allow hybrid energy models combining grid and local generation. It improves uptime and reduces reliance on utility fluctuations. The Spain AI Data Center Market sees innovation in AI-backed energy management. Smart energy orchestration becomes a value proposition for high-availability AI training sites. It combines power efficiency and service reliability under one platform.

Market Challenges

Power Availability, Grid Latency, and Regional Interconnectivity Create Bottlenecks

Despite strong solar and wind availability, grid readiness lags behind AI infrastructure demands. Power latency and availability differ significantly across regions. Grid congestion near hyperscale zones limits large-scale deployment timelines. AI training clusters require constant, high-density power flow with minimal downtime. Spain’s north-central regions face higher load balancing risks. The Spain AI Data Center Market must address these grid constraints through partnerships with utilities and smart grid upgrades. Operators that fail to ensure stable power risk service disruptions and SLA breaches.

Skill Shortage and Regulatory Complexity Slow AI Infrastructure Scalability

Building AI-ready infrastructure needs professionals skilled in GPU orchestration, HPC design, and cooling integration. Spain faces a shortfall in talent with AI-specific data center experience. Training cycles and workforce migration programs remain underdeveloped. Also, regional permitting rules vary across provinces. Complex zoning, construction, and emissions compliance delay deployment. AI projects under sovereign frameworks face additional cybersecurity audits and vendor restrictions. It slows time-to-market and increases compliance overhead. The Spain AI Data Center Market needs unified policy pathways and specialized workforce upskilling to overcome these gaps.

Market Opportunities

Rising Interest from Global Cloud and AI Providers to Localize European AI Workloads

Spain serves as a bridge between European and LatAm workloads for multinational operators. Global AI firms seek regional hubs to meet EU data rules and latency needs. Cloud players expand presence in Spain for AI deployment zones. The Spain AI Data Center Market stands to gain from such local expansions. Providers focus on building scalable, AI-dedicated capacity zones tied to enterprise demands. Early movers will secure long-term contracts for localized AI compute.

Edge AI, Sovereign Cloud, and Industry-Specific AI Zones Offer Niche Growth Avenues

Spain’s government supports sovereign data projects across healthcare and public services. Operators can create zones tailored to specific industry use cases. Retail, logistics, and mobility AI applications benefit from edge facility rollouts. It opens up localized, application-tuned AI zones. The Spain AI Data Center Market can attract specialized operators in edge, sovereign, and vertical AI domains. Growth lies in building flexible, secure, and sector-compliant infrastructure layers.

Market Segmentation

By Type

The hyperscale segment leads the Spain AI Data Center Market, accounting for the largest share due to rapid enterprise and cloud provider demand. Hyperscale builds support large-scale training and inferencing workloads, often exceeding 50 kW per rack. Colocation and enterprise facilities follow, offering hybrid capacity for regulated sectors. Edge and micro data centers are gaining traction, especially in urban centers for latency-sensitive AI use cases. This segment supports video analytics, mobility AI, and near-device compute models.

By Component

Hardware dominates the component segment of the Spain AI Data Center Market, driven by high-density GPU racks, accelerators, and liquid cooling systems. Investments in servers, racks, power units, and network fabrics continue to rise. Software and orchestration are growing rapidly, enabling AI workload scheduling, GPU pooling, and AIOps. Services contribute a steady share, covering facility management, integration, and monitoring. Software-defined management tools enable scalable, automated AI resource handling across distributed sites.

By Deployment

Cloud-based deployment leads the market, supported by hyperscale AI providers expanding their regional presence. On-premise deployment remains strong in BFSI and government sectors for data sovereignty needs. Hybrid deployment is rapidly rising as organizations blend cloud flexibility with localized control. The Spain AI Data Center Market sees increasing demand for hybrid solutions across AI use cases, balancing performance and compliance. Enterprises opt for split deployments to optimize latency and cost structures.

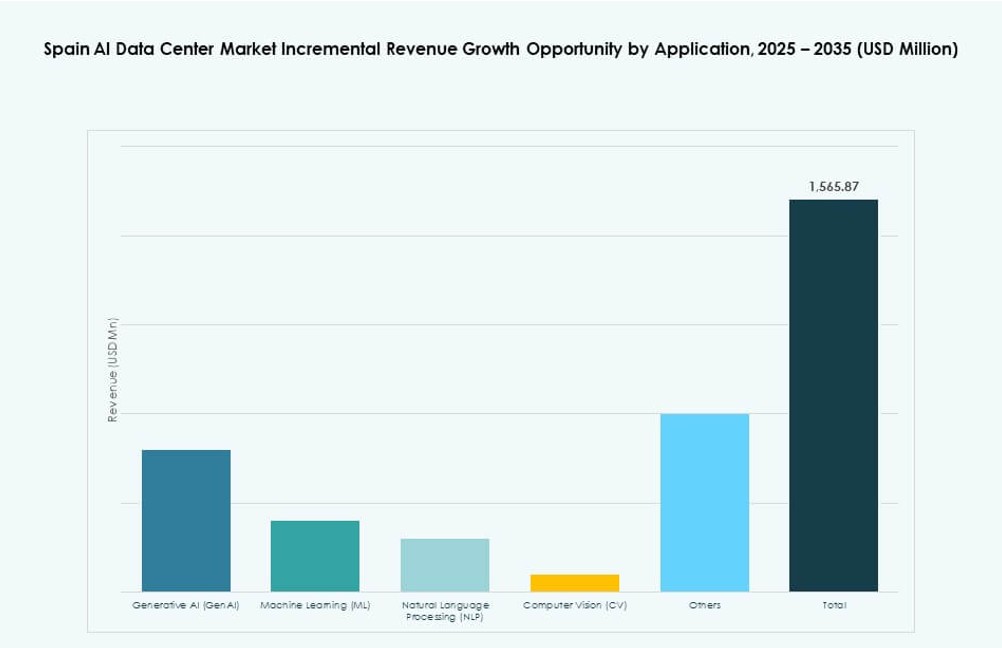

By Application

Machine Learning (ML) leads the application segment, used across banking, retail, and healthcare operations. Generative AI (GenAI) adoption is surging, requiring larger models and high-throughput systems. NLP supports chatbots, voice assistants, and document analytics in Spanish-language models. Computer Vision (CV) grows in retail, automotive, and manufacturing, supporting surveillance and automation. Other applications include robotics, recommendation engines, and scientific simulations. The Spain AI Data Center Market aligns infrastructure with evolving AI workload needs.

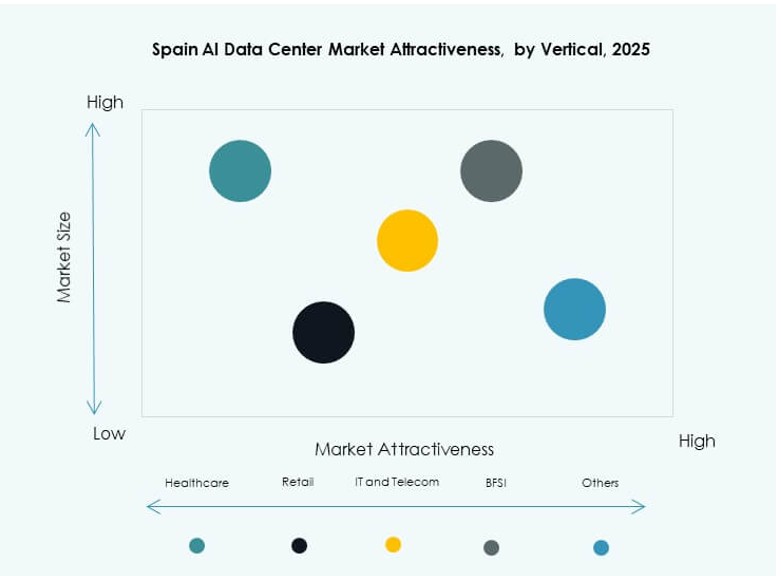

By Vertical

IT and telecom dominate vertical adoption, driven by AI-powered service delivery, predictive analytics, and customer experience tools. BFSI ranks second, using AI for fraud detection, trading platforms, and financial insights. Healthcare adoption grows with imaging diagnostics, genomic analysis, and patient data models. Retail and media sectors invest in AI for personalization, ad optimization, and content generation. Manufacturing and automotive deploy AI for process automation and digital twin simulations. The Spain AI Data Center Market supports these verticals with AI-tuned infrastructure.

Regional Insights

Madrid holds the highest share in the Spain AI Data Center Market, accounting for over 45% of the national capacity. It benefits from strong network backbones, access to renewable power, and enterprise demand. Major cloud players, financial institutions, and government agencies prefer Madrid for AI deployments. The city leads in high-density rack installations and training infrastructure. Local incentives and talent availability support continued investment.

- For instance, in May 2024, AWS announced a €15.7 billion investment to expand its cloud infrastructure in Spain’s Aragón region through 2033. The expansion supports the AWS Europe (Spain) Region and aims to meet growing demand for advanced cloud and AI workloads.

Barcelona contributes around 25% to the national market, making it the second-largest regional hub. Its proximity to innovation centers and a strong tech workforce enable faster AI workload adoption. Barcelona-based data centers cater to healthcare, manufacturing, and public sector AI applications. The region shows growth in hybrid and edge deployments. It also serves as a regional gateway for Southern European AI workloads.

Emerging regions such as Valencia, Bilbao, and Málaga collectively contribute 30% to the market. These zones gain interest for edge AI facilities targeting logistics, tourism, and smart city initiatives. Favorable zoning, land availability, and renewable energy access support future builds. These cities serve distributed AI processing demands across Spain. The Spain AI Data Center Market sees these regions becoming key expansion points for mid-size and edge-focused operators.

- For instance, EDGNEX Data Centers by DAMAC announced plans in October 2024 to develop a 40 MW AI-ready facility in Madrid, Spain, aimed at supporting high-performance computing and hyperscale workloads.

Competitive Insights:

- Nabiax

- Adam Data Center

- Gigas Hosting

- Microsoft (Azure)

- Amazon Web Services (AWS)

- Google Cloud

- Equinix

- Digital Realty Trust

- Meta Platforms

- CoreWeave

The Spain AI Data Center Market is driven by a mix of domestic providers and global hyperscale firms. Nabiax, Adam, and Gigas Hosting maintain strong local presence through colocation and enterprise services. Microsoft, AWS, and Google Cloud lead in hyperscale AI deployment zones, supported by scalable infrastructure and deep capital investment. Equinix and Digital Realty strengthen regional interconnectivity and hybrid deployments. Meta and CoreWeave focus on dense GPU clusters to support AI training and inference. It is seeing rising competition in edge and sovereign AI zones. Vendors differentiate through power density, liquid cooling readiness, and sustainability certifications. Strategic partnerships, real estate control, and data compliance influence long-term positioning. Growth favors players with AI-optimized hardware and multi-region presence.

Recent Developments:

- In December 2025, Nostrum Group selected AECOM to design a 500 MW AI data center campus in Badajoz, Spain, for growing cloud and AI compute demand. AECOM will lead the design and construction management of this major campus, aimed at meeting high‑density AI infrastructure requirements across Europe. This project reflects rising demand for scalable AI and cloud services capacity

- In September 2025, EdgeMode announced a definitive agreement with Blackberry AIF to acquire five major data center sites in Spain, creating a portfolio targeting 1.5 GW of planned AI‑ready infrastructure.

- In June 2025, NVIDIA announced plans to establish and expand AI technology centers across Europe, including a new AI factory in Spain to accelerate AI research and applications.