Executive summary:

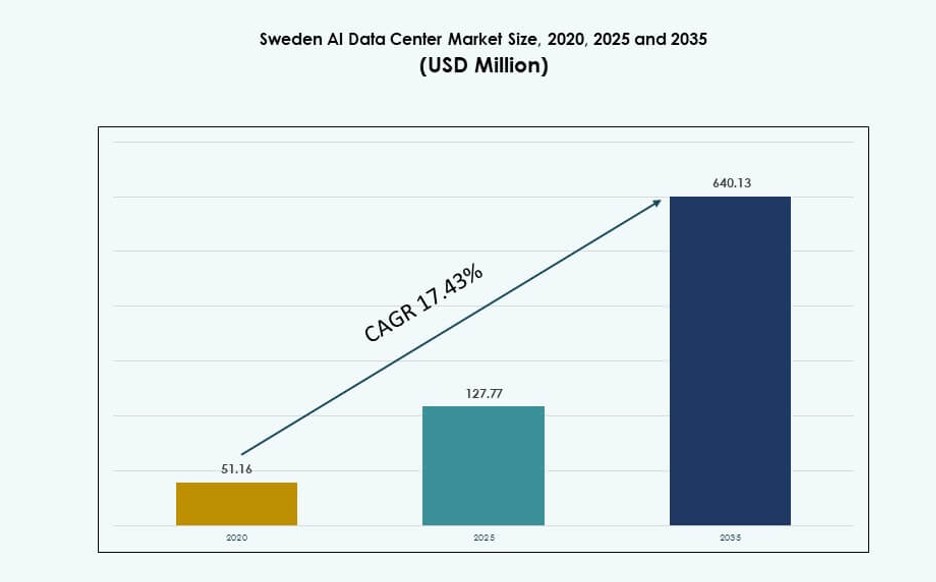

The Sweden AI Data Center Market size was valued at USD 51.16 million in 2020 to USD 127.77 million in 2025 and is anticipated to reach USD 640.13 million by 2035, at a CAGR of 17.43% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Sweden AI Data Center Market Size 2025 |

USD 127.77 Million |

| Sweden AI Data Center Market, CAGR |

17.43% |

| Sweden AI Data Center Market Size 2035 |

USD 640.13 Million |

The market is expanding due to strong national digital policies, abundant renewable energy, and advanced AI use cases across industries. Sweden supports high-performance infrastructure through cold climate advantages and a stable energy grid. Enterprises adopt AI for automation, analytics, and smart operations, driving demand for GPU-intensive data centers. Innovation in cooling technologies, sustainability, and workload orchestration is reshaping facility design. Investors benefit from long-term power contracts, ESG-aligned assets, and stable regulatory frameworks. Strategic partnerships between hyperscalers and local players enhance capacity. It creates strong momentum for building scalable and secure AI infrastructure. Sweden positions itself as a preferred Nordic destination for AI-driven digital transformation.

Stockholm leads the market due to its hyperscale campuses, fiber networks, and enterprise demand concentration. Northern regions like Luleå and Piteå are emerging due to low energy prices and land availability. These areas attract sustainable AI projects using hydropower and direct liquid cooling systems. Gothenburg and Malmö grow steadily as regional hubs for enterprise and edge deployments. Proximity to key European markets makes Sweden a strategic gateway for cross-border AI workloads. The geographic balance between urban connectivity and rural sustainability supports market resilience. It enables diverse infrastructure strategies aligned with specific AI compute needs.

Market Dynamics:

Market Drivers

Government Policies, Renewable Energy Supply, and Climate Conditions Supporting AI-Driven Infrastructure

Sweden’s digital roadmap, sustainability mandates, and AI development frameworks continue to push infrastructure investment. The country’s access to 98% renewable electricity and naturally cool climate ensures energy efficiency in high-density facilities. These environmental benefits reduce operating costs and emissions, making Sweden a prime AI data center hub. Global hyperscalers and local enterprises benefit from green branding and reduced long-term TCO. The Sweden AI Data Center Market gains investor confidence through policy transparency and regulatory ease. It also aligns with ESG goals of major cloud and AI service providers. Energy and climate advantages enhance deployment of AI workloads needing massive GPU compute. Data center operators view Sweden as a long-term strategic location for scaling AI clusters. Growth is secured by long-term energy price stability and low environmental risk.

- For instance, Microsoft’s datacenter region in Gävle, Sandviken, and Staffanstorp has operated with 100% carbon-free energy via 24/7 hourly matching from Vattenfall since 2021, using EPD-labeled hydro and wind power across three facilities.

Surging Demand for High-Performance Compute from AI Workloads and Digital Economy Expansion

Rising demand for generative AI, deep learning, and data-intensive applications fuels GPU-based compute infrastructure. The growing adoption of autonomous systems, AI-powered analytics, and cognitive automation increases need for AI-ready data centers. AI is now deeply embedded in banking, manufacturing, and healthcare operations. These verticals seek secure and scalable environments to deploy advanced inference and training models. The Sweden AI Data Center Market benefits from strong enterprise cloud adoption and public-private R&D partnerships. It attracts firms seeking to optimize training latency and data locality. Many data centers deploy liquid cooling and 100 kW+ racks for AI clusters. Technology vendors and developers find Sweden attractive for regional model testing and deployment. Digital-first business models drive consistent growth in AI infrastructure needs.

Expansion of Edge and Hybrid Cloud Infrastructure for Localized AI Model Training and Inference

Edge and hybrid deployments are accelerating across urban and remote Swedish regions. Enterprises require faster inference, real-time decision-making, and local data processing. Micro data centers offer low latency for edge AI use cases in logistics, manufacturing, and smart cities. The Sweden AI Data Center Market evolves with growing 5G rollouts, IoT adoption, and sensor-based applications. AI use cases such as industrial inspection and predictive maintenance depend on edge clusters. These needs push local deployment models over centralized training in some sectors. Strategic locations like Gothenburg and Malmö support regional GPU compute zones. Hybrid clouds integrate private and public infrastructure, ensuring flexibility and control. National AI strategies encourage localized innovation through smaller yet powerful infrastructure.

Rising Investments from Hyperscale Operators and Local Enterprises in AI-Optimized Facilities

International hyperscalers like Google, Microsoft, and Meta have expanded capacity in Sweden using AI-ready designs. Facilities now include direct-to-chip liquid cooling, scalable AI fabrics, and 50 kW+ rack densities. Local telecom and cloud firms also deploy clusters for enterprise-grade AI workloads. The Sweden AI Data Center Market benefits from land availability, fiber connectivity, and stable grid supply. Competitive electricity prices and mature ICT infrastructure reduce entry barriers for investors. New data centers focus on sustainability, modularity, and integration with AI frameworks. Enterprises adopt AI for cybersecurity, analytics, and customer experience use cases. Regional innovation hubs fuel demand for colocated AI environments. Sweden’s reputation for data privacy and resilience makes it a secure base for AI infrastructure.

- For instance, Microsoft committed $3.2 billion through 2026 for data center construction and AI infrastructure in Sweden, including GPU deployments.

Market Trends

Shift Toward AI-Specific GPU Infrastructure and Liquid-Cooled Rack Systems in Core Facilities

Data centers increasingly invest in racks with 50 kW or higher capacities using liquid cooling for thermal efficiency. Demand for GPU clusters tailored for AI training workloads grows across both hyperscale and colocation facilities. These systems support generative models, transformer-based architectures, and large-scale simulations. AI infrastructure in Sweden includes high-throughput interconnects and custom AI accelerators. The Sweden AI Data Center Market adopts liquid immersion and rear-door heat exchangers. Facilities reduce energy use while improving AI system uptime and density. Rack-level monitoring enables real-time insights on thermal load distribution. Operators retrofit existing spaces or design purpose-built AI environments. Energy reuse innovations also emerge in Sweden’s colder regions.

Emergence of Colocation Hubs Offering AI-as-a-Service Models and Flexible AI Workload Deployment

Colocation providers expand service portfolios by offering AI-ready infrastructure bundles. Clients get access to GPU instances, storage, and orchestration layers without owning physical infrastructure. This model supports startups and enterprises exploring new AI use cases. The Sweden AI Data Center Market aligns with demand for flexible capacity consumption. Operators integrate containerized platforms and orchestration tools to manage AI workflows. AI-as-a-Service offerings include model training, fine-tuning, and edge deployment capabilities. Clients value localized compute with low-latency access and regional compliance. These trends increase the adoption of multi-tenant AI environments in urban and secondary cities. Data center campuses now prioritize modular growth and short provisioning cycles.

Rise in AI Integration Across Industrial Verticals Fueling Tailored Infrastructure Requirements

AI is becoming core to business strategies across manufacturing, logistics, and energy sectors. AI workloads differ by use case—requiring specific infrastructure designs. The Sweden AI Data Center Market responds with domain-specific compute environments. Some facilities cater to automotive AI simulation, others focus on medical imaging or NLP. Operators provide customizable AI clusters with high-bandwidth storage and AI accelerators. This sectoral diversification fuels continuous infrastructure evolution. Industry 4.0 and digital twin projects gain traction in regions like Västerås and Umeå. Sweden’s innovation ecosystems support AI toolchains linked to localized training nodes. Companies integrate AI into operations faster using regional compute capabilities.

Integration of DCIM, AI-Orchestrated Systems, and Real-Time Monitoring Across AI Clusters

Operators implement DCIM systems that support real-time AI workload management, predictive maintenance, and thermal mapping. These platforms monitor infrastructure performance and optimize resource utilization dynamically. The Sweden AI Data Center Market adopts AI-powered orchestration for workload balancing. It enables dynamic allocation of GPUs and power based on model intensity. AI agents forecast system failures and thermal anomalies, reducing downtime. Facilities integrate telemetry data into operations dashboards. Smart systems reduce operating costs and improve sustainability metrics. Real-time feedback loops help scale AI environments in line with workload growth. Infrastructure becomes adaptive, resilient, and aligned with AI training life cycles.

Market Challenges

High Capital Expenditure and Lead Time for Building AI-Optimized Infrastructure at National Scale

AI data centers require high-density racks, advanced cooling, and custom hardware—all of which increase upfront costs. Many operators face long planning and construction lead times. Sweden’s construction regulations and environmental compliance rules can delay deployment. The Sweden AI Data Center Market contends with capital access challenges for local players. Financing constraints affect edge deployments and AI-specific retrofitting. Hyperscalers often outcompete smaller firms for resources and land. Sourcing skilled labor and specialized hardware remains difficult. Grid upgrades and substation availability also affect project timelines. Cost and time bottlenecks limit scalability and delay AI adoption at smaller enterprise levels.

Limited Domestic Chip Manufacturing and High Dependency on Imported AI Hardware and Components

Sweden lacks advanced domestic semiconductor manufacturing for GPUs and AI accelerators. The market depends on imports from the U.S. and Asia for critical AI infrastructure. The Sweden AI Data Center Market faces supply chain risks and lead time variability. Global chip shortages or export controls impact deployment cycles. Shipping delays and import costs raise infrastructure TCO for smaller operators. AI model performance hinges on timely access to high-bandwidth memory and next-gen GPUs. Maintenance and upgrade cycles stretch longer without local component access. The dependency slows innovation velocity and limits custom AI hardware deployment options.

Market Opportunities

Integration of Sweden’s Renewable Grid and Cold Climate into Sustainable AI Infrastructure Models

Operators use 100% clean electricity from hydro and wind sources to power AI clusters. The cold Nordic climate cuts cooling costs and supports high-density racks. The Sweden AI Data Center Market can lead in net-zero AI infrastructure. It offers operators long-term savings and aligns with ESG targets. Sustainability attracts global cloud and AI leaders to the region. Policy alignment and power availability further support expansion. New projects include energy reuse and heat recovery into district heating systems. Investors benefit from long asset life and compliance ease.

Strategic Position as a Low-Latency Hub Connecting Northern and Central Europe for AI Workloads

Sweden provides low-latency access to both Nordic and continental European markets. Its fiber networks, proximity to Germany and Finland, and stable policies make it ideal. The Sweden AI Data Center Market plays a growing role in regional AI workload distribution. Operators deploy training zones in Sweden while inference runs near urban users. This hub role supports edge-AI and sovereign compute trends. Sweden’s neutrality and digital resilience enhance its strategic position. Investors can leverage proximity to EU regulatory frameworks and data privacy norms.

Market Segmentation

By Type

The hyperscale segment dominates the Sweden AI Data Center Market due to continued investment from global cloud service providers. Hyperscalers focus on AI-specific infrastructure with 50–100 kW rack densities and advanced cooling. Colocation and enterprise segments serve mid-size firms requiring AI workload flexibility. Edge and micro data centers are emerging in secondary cities to support real-time inference and IoT use cases. Hyperscale facilities hold the largest share, driven by expansion near Stockholm and northern sites with abundant renewable energy.

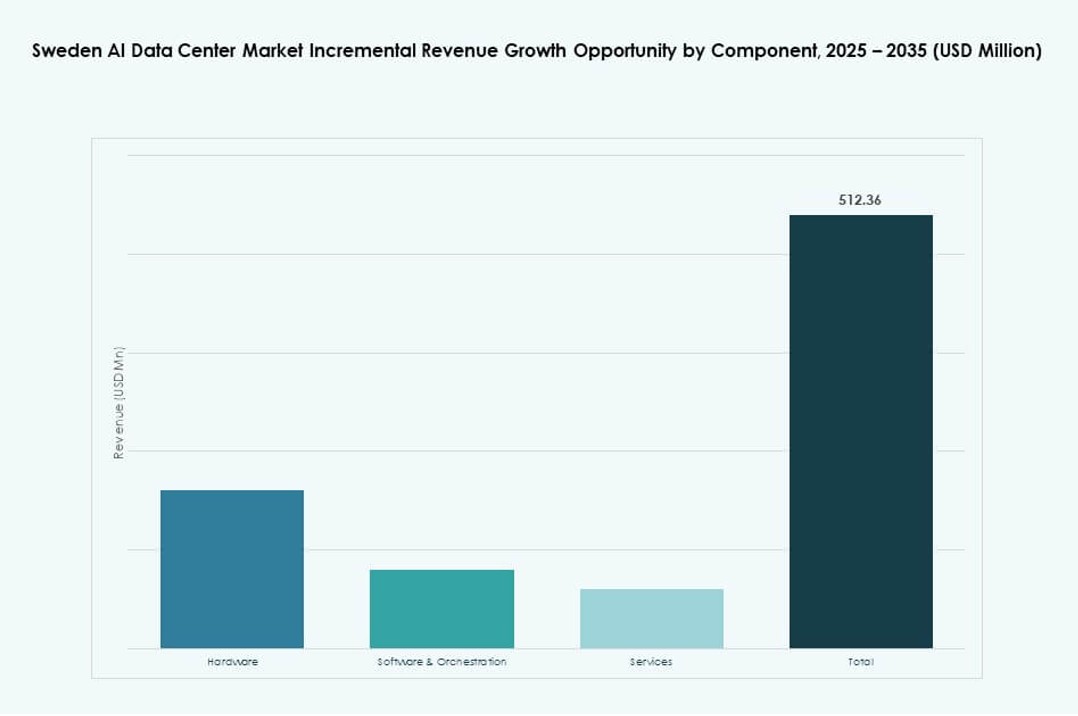

By Component

Hardware accounts for the largest share in the Sweden AI Data Center Market, led by demand for GPUs, high-density racks, and AI accelerators. AI workloads require performance-optimized components with integrated memory and compute. Software and orchestration layers grow rapidly with AI model lifecycle management needs. Services, including integration and monitoring, remain essential for ongoing AI operations. The hardware segment dominates due to high upfront investment in AI-specific infrastructure components across Sweden.

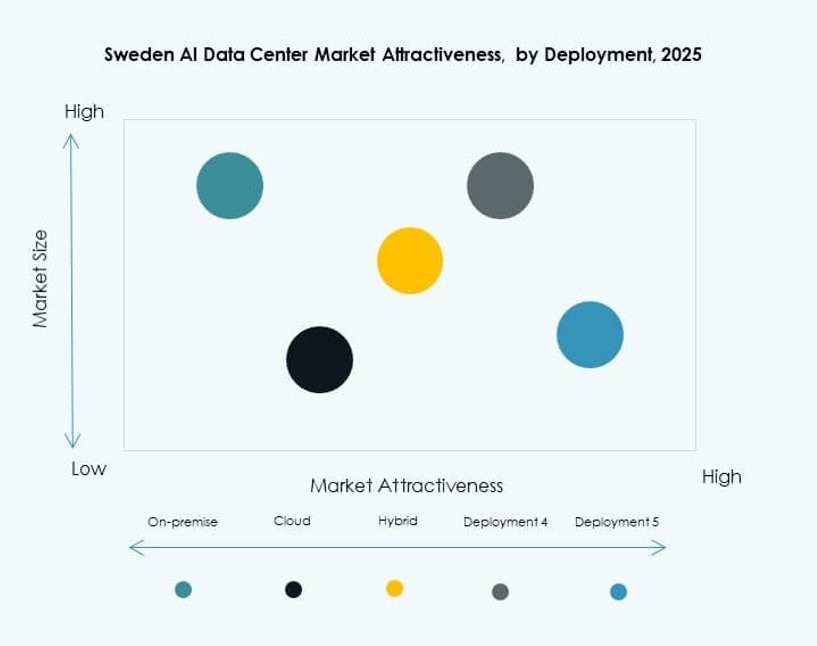

By Deployment

The cloud deployment model leads the Sweden AI Data Center Market due to flexibility and scalability benefits. Enterprises opt for cloud-based AI training and inference across verticals. Hybrid models are gaining momentum, combining public cloud scalability with private control. On-premise deployments persist in regulated sectors like BFSI and healthcare. The hybrid model grows fastest due to demand for data localization and AI governance. Cloud retains the largest share, supported by hyperscaler investments and SaaS adoption.

By Application

Machine learning (ML) holds the highest market share in the Sweden AI Data Center Market. ML applications span across predictive analytics, fraud detection, and demand forecasting. Generative AI grows fastest with demand from media, marketing, and R&D. Computer vision and NLP expand through industrial automation and customer experience tools. Other applications include reinforcement learning and edge AI. ML remains dominant due to broad enterprise adoption and model deployment needs.

By Vertical

The IT and telecom segment dominates the Sweden AI Data Center Market by vertical due to early AI adoption and digital infrastructure maturity. BFSI, retail, and manufacturing sectors rapidly increase AI usage for operational and customer insights. Healthcare and automotive drive demand for AI model accuracy and real-time analytics. Media and entertainment lead in GenAI deployment for content creation. The IT and telecom sector maintains the lead due to continuous cloud-native transformation.

Regional Insights

Stockholm Region Commands Over 55% Market Share Due to Hyperscaler Presence and Fiber Connectivity

Stockholm leads the Sweden AI Data Center Market with more than 55% share. It hosts major campuses by global cloud providers and colocation operators. The region offers dense fiber infrastructure, low-latency access, and skilled workforce availability. Proximity to government agencies and enterprise hubs supports demand. AI workloads in this region span finance, cloud-native tech, and digital media. Stockholm remains the primary landing point for subsea and terrestrial network connections. It also benefits from policy stability and green power supply.

Northern Sweden Accounts for 30% Share Due to Energy Availability and AI-Ready Land Parcels

Northern regions such as Luleå and Boden represent 30% of the Sweden AI Data Center Market. They provide access to low-cost hydroelectric power and cool temperatures, ideal for high-density AI clusters. Land availability and government support enable hyperscale deployment. Data centers in the north often include energy reuse systems and advanced cooling. The area attracts operators building sustainable AI infrastructure. Its growing importance aligns with Sweden’s digital sustainability goals.

- For instance, Meta’s Luleå data center operates with a PUE of 1.08 using 100% renewable hydroelectric power.

Southern and Secondary Cities Hold 15% Share with Growing AI Edge and Hybrid Infrastructure Activity

Cities like Gothenburg, Malmö, and Uppsala make up the remaining 15% of the Sweden AI Data Center Market. These areas support edge computing for logistics, mobility, and retail AI applications. Local operators deploy containerized units and modular clusters. Proximity to urban consumers enables fast model inference and low-latency analytics. AI deployments in these zones focus on hybrid models and regulatory compliance. Growth is supported by urban digitization and smart city investments.

- For instance, EcoDataCenter in Falun launched a wooden modular data center in 2023 focused on sustainability with heat recovery systems.

Competitive Insights:

- EcoDataCenter

- GleSYS

- Portlane

- Digital Realty Trust

- Equinix

- Microsoft Azure

- Amazon Web Services

- Google Cloud

- Meta Platforms

The competitive landscape of the Sweden AI Data Center Market reflects a mix of global hyperscalers and strong domestic operators. Hyperscale cloud providers lead capacity expansion through large AI-ready campuses powered by renewable energy. Local specialists compete on sustainability, low-latency services, and tailored enterprise offerings. It shows high capital intensity, which favors firms with scale, energy contracts, and advanced cooling expertise. Partnerships with hardware and AI platform vendors strengthen positioning. Competition centers on power availability, rack density, and speed of deployment. Operators differentiate through green credentials, heat reuse, and compliance strength. Consolidation remains limited, yet strategic alliances increase. The market structure supports long-term players with strong balance sheets and AI infrastructure depth.

Recent Developments:

- In June 2025, Brookfield Asset Management announced plans to invest SEK 95 billion (about USD 9.9 billion) in a massive AI data center campus in Strängnäs, Sweden, initially planned for 300 MW capacity expandable to 750 MW over 10-15 years.

- In April 2025, CapMan Infra acquired three high-quality data centers from EcoDataCenter two in Stockholm and one in Piteå to expand its Nordic platform supporting AI workloads.