Executive summary:

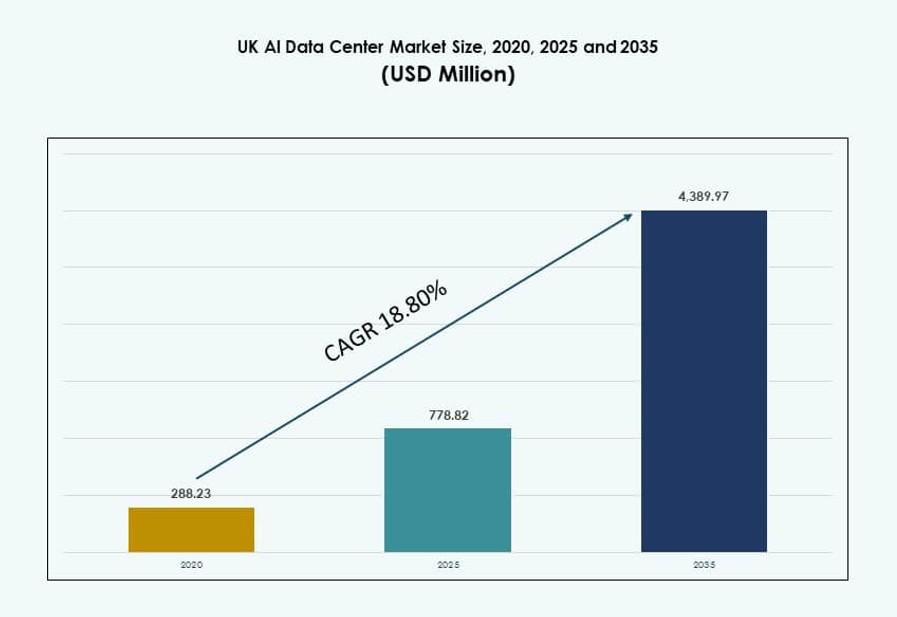

The UK AI Data Center Market size was valued at USD 288.23 million in 2020 to USD 778.82 million in 2025 and is anticipated to reach USD 4,389.97 million by 2035, at a CAGR of 18.80% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| UK AI Data Center Market Size 2025 |

USD 778.82 Million |

| UK AI Data Center Market, CAGR |

18.80% |

| UK AI Data Center Market Size 2035 |

USD 4,389.97 Million |

Growth in the market is driven by rising demand for high-density AI compute infrastructure, fueled by large language models and real-time inference applications. Organizations are deploying GPU clusters, liquid-cooling systems, and smart rack architectures to support evolving AI workloads. Public-private partnerships, national AI policies, and cloud-native adoption are accelerating deployment timelines. Investors view the UK as a strategic hub for sovereign AI infrastructure, supported by strong compliance, connectivity, and talent availability. Hyperscalers are expanding capacity in line with rising enterprise AI demand. The shift toward energy-efficient data centers is also influencing technology choices across deployments.

London and the Greater South East region lead the market due to dense hyperscale zones, enterprise demand, and strong fiber interconnectivity. The Midlands and North West are emerging as AI corridors through government incentives and campus expansions. Academic hubs in Scotland and research-backed zones in Wales support regional AI growth through innovation clusters. Geographic diversity enables distributed workloads and resilience across the national compute landscape. Strong power availability and land access in non-metro areas support future expansion potential.

Market Dynamics:

Market Drivers

Strong Demand for High-Density AI Compute Driving Investment in Energy-Efficient Data Center Infrastructure

The UK AI Data Center Market is driven by rising demand for high-density compute infrastructure to support AI model training and inference. Generative AI, LLMs, and edge intelligence require scalable power and cooling systems. Operators deploy advanced rack designs and adopt direct-to-chip and liquid-cooling systems to support power loads above 30 kW per rack. The market benefits from high demand across industries such as finance, healthcare, and logistics. UK’s hyperscale and colocation providers continue expanding capacities to host large AI clusters. Businesses are prioritizing AI workloads with long-term data center leases and infrastructure modernization. Government-led initiatives to build sovereign compute zones also support demand. The focus on energy-efficient and sustainable AI operations boosts data center redevelopment and greenfield investments.

- For instance, Microsoft Azure’s ND H100 v5-series virtual machines are available in UK regions, offering up to 8 NVIDIA H100 GPUs per instance with 700GB GPU memory. These instances run on liquid-cooled racks designed for over 30 kW densities to support advanced AI model training.

Cloud-Native AI Workload Proliferation Across Verticals Fueling AI-Optimized Facility Expansions

AI adoption across sectors is driving cloud-native architectures, increasing reliance on AI-optimized data center clusters. Enterprises shift toward containerized and disaggregated compute stacks integrated with GPUs and accelerators. Providers in the UK AI Data Center Market focus on offering GPU-as-a-Service and AI infrastructure-as-a-service to support training and inference models. It enables dynamic scaling, real-time analytics, and secure inference pipelines. This transformation supports steady growth across colocation, edge, and hyperscale facilities. Telecom and BFSI verticals lead demand for secure and latency-sensitive compute zones. Investments in DCIM and workload orchestration further drive efficiency. Software-defined control of GPU clusters helps improve capacity management and TCO outcomes for clients.

Strategic Position of the UK in AI Governance and Compute Sovereignty Programs Boosts Investment Confidence

The UK plays a key role in setting international standards for responsible AI and compute regulation. Its position as an AI governance leader aligns with investments in domestic compute capacity. The UK AI Data Center Market benefits from policies prioritizing AI readiness, infrastructure security, and digital sovereignty. Recent government commitments and AI compute grant programs attract global investors and hyperscale tenants. It reinforces the UK’s importance in supporting foundation model development and large-scale research. These factors create confidence for long-term capital deployment into scalable facilities. National AI infrastructure hubs support regional workload distribution and reduce pressure on London-centric capacity. Strategic partnerships between cloud providers and public agencies accelerate deployment timelines.

- For instance, the Isambard-AI supercomputer at the National Composites Centre integrates 5,448 NVIDIA GH200 Grace Hopper Superchips, delivering over 21 exaflops of AI compute performance (FP8). Housed in Cray EX2500 liquid-cooled racks from HPE, it anchors the UK’s £1 billion AI Research Resource initiative.

Shift Toward GPU-Centric Architectures and R&D Clusters Backed by University-Industry Collaboration

Leading UK universities and research institutions work with industry players to establish AI innovation centers. These centers require specialized infrastructure with rack densities above traditional enterprise workloads. The UK AI Data Center Market supports collaborative compute environments focused on model development and fine-tuning. It enables fast provisioning and model retraining through AI-integrated orchestration platforms. These trends foster demand for scalable racks, intelligent PDUs, and liquid-ready cooling systems. Adoption of modular and prefabricated data halls also rises. AI-focused clusters near Oxford, Cambridge, and Edinburgh benefit from joint funding and regional incentives. Technology parks and R&D campuses integrate data centers as critical assets in AI innovation pipelines.

Market Trends

Rapid Uptake of Liquid-Cooled Racks for AI Workloads Requiring Higher Thermal Efficiency and Power Density

The UK AI Data Center Market is witnessing strong uptake of liquid cooling to meet AI compute demands. Rack densities for AI workloads now exceed 30–50 kW in many training zones. Operators are adopting direct-to-chip, immersion, and rear-door heat exchanger systems to manage thermal loads. Liquid cooling improves energy efficiency and aligns with ESG mandates for reduced PUE. Deployment of liquid-ready modules supports quicker installation of GPU clusters. Hyperscalers build liquid-cooled campuses near power-dense zones. Liquid cooling also enables flexible space management by reducing air conditioning load. It has become a key differentiator in new AI facility designs across the UK.

Integration of Smart Racks and DCIM Platforms for AI-Centric Infrastructure Management and Optimization

AI data centers in the UK increasingly adopt intelligent racks with integrated sensors, telemetry, and DCIM interfaces. These platforms enable predictive maintenance, load balancing, and real-time power control. The UK AI Data Center Market sees rising deployment of rack-level performance monitoring tools to manage GPUs and accelerators. Smart racks support AI-driven fault detection and energy use optimization. Operators use DCIM to orchestrate compute, cooling, and storage in real time. These tools help operators meet SLA targets for AI workloads requiring continuous availability. It supports operational resilience and sustainability tracking. AI-centric infrastructure management platforms also improve capacity forecasting and asset lifecycle planning.

Rise of Sovereign AI Zones and Public-Private Consortiums Creating Tiered Infrastructure Clusters Across Regions

National focus on digital sovereignty is encouraging the development of AI-ready zones compliant with data residency rules. The UK AI Data Center Market is aligning with these priorities through regional clusters focused on secure AI compute. Public-private partnerships support infrastructure development near education hubs, government centers, and fintech corridors. These clusters enable model hosting, citizen services, and regulated AI applications. Tiered zones help balance training workloads across central and edge facilities. Investment models include joint funding, leasing incentives, and regulatory streamlining. Deployment of 5G and fiber enhances cluster connectivity. Infrastructure segmentation supports differentiated AI use cases by sector and workload type.

Growth of AI Workload Disaggregation and Storage-Rack Decoupling Across Hyperscale Architectures

To optimize infrastructure for foundation models and GenAI training, operators decouple compute and storage layers. Disaggregated architectures enhance flexibility in GPU scaling and memory pooling. The UK AI Data Center Market is moving toward rack-level modularization, where GPU, CPU, and NVMe clusters operate independently. This model improves airflow, rack power utilization, and failure isolation. Storage-rich racks are deployed separately to meet large-scale inference latency demands. Disaggregation supports varied AI deployment needs without full facility upgrades. It also allows for software-defined scaling through APIs. Providers now deliver these features in both hyperscale and enterprise-grade colocation facilities.

Market Challenges

Grid Congestion, Power Constraints, and Permitting Delays Affecting Timely Expansion of AI-Ready Data Centers

The UK AI Data Center Market faces challenges from grid congestion and limited access to high-capacity power sources. AI-ready racks require 30–100 kW per rack, straining traditional data center load profiles. Delays in grid upgrades and substation approvals slow new campus developments. Planning approval timelines often stretch due to regulatory and environmental assessments. Power pricing volatility adds uncertainty to long-term TCO modeling. Developers must secure energy purchase agreements and backup sources, which increases complexity. Operators compete for limited megawatts across regions with growing hyperscale presence. These factors affect project timelines and cost optimization strategies for AI deployments.

Shortage of Skilled Workforce and Specialized AI Infrastructure Talent Delaying Operational Ramp-Up

Hiring skilled staff for high-performance AI infrastructure remains a concern across many regions. The UK AI Data Center Market requires engineers trained in GPU optimization, liquid cooling systems, and orchestration platforms. Labor shortages in data center operations, compliance, and network engineering affect large-scale AI cluster ramp-ups. Training programs are catching up, but talent remains concentrated in metro areas. This limits geographic diversification of AI zones. Cross-training traditional IT staff adds cost and onboarding delays. The market requires strategic coordination among operators, universities, and workforce agencies to bridge this talent gap. Lack of specialized professionals could limit AI workload readiness.

Market Opportunities

Emerging Edge AI Applications Across Healthcare, Retail, and Smart Infrastructure Driving Distributed Deployment

Edge AI adoption is growing in sectors like diagnostics, retail analytics, and urban infrastructure. The UK AI Data Center Market has an opportunity to expand micro and modular edge nodes supporting low-latency AI inference. Healthcare providers use edge data centers for real-time patient data processing. Smart retail stores and IoT-driven cities require compute capacity close to endpoints. This trend drives demand for compact, secure, and energy-efficient AI-ready racks outside major metros. New use cases drive service provider partnerships in rural and semi-urban zones.

Integration of AI with Renewable Energy Optimization and Grid Analytics Supporting Sustainable AI Infrastructure

AI plays a growing role in optimizing renewable energy integration and grid balancing. The UK AI Data Center Market can support this by hosting training workloads for energy optimization models. Operators deploying AI models to improve demand prediction and energy routing create new workloads. AI-optimized data centers become part of national climate infrastructure. Partnerships with energy firms and utilities open new infrastructure investment channels.

Market Segmentation

By Type

The hyperscale segment dominates the UK AI Data Center Market due to aggressive capacity expansion by global cloud providers. Hyperscale campuses support high-density training clusters and large model hosting. Colocation and enterprise deployments also grow steadily, targeting regulated sectors and data sovereignty compliance. Edge and micro data centers see traction in smart cities and healthcare, supporting low-latency inference.

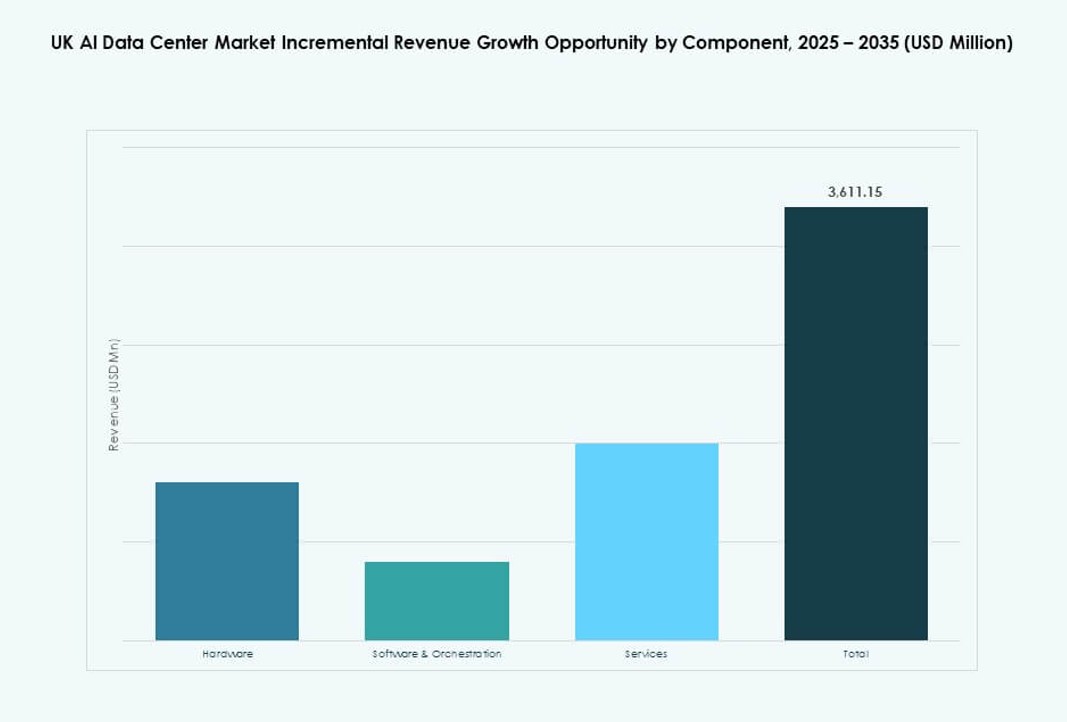

By Component

Hardware leads the market as operators invest heavily in high-performance racks, GPUs, and cooling infrastructure. Software and orchestration tools follow, enabling intelligent workload placement and dynamic scaling. Services grow through demand for infrastructure management, DCIM integration, and AI workload consulting. Growth in orchestration platforms reflects rising complexity in multi-rack AI clusters.

By Deployment

Cloud-based deployments dominate due to scalability and seamless integration with global AI pipelines. Hybrid models gain momentum across BFSI, healthcare, and public sectors requiring partial data residency. On-premise deployments remain relevant in research institutions and government facilities focused on control and sovereignty.

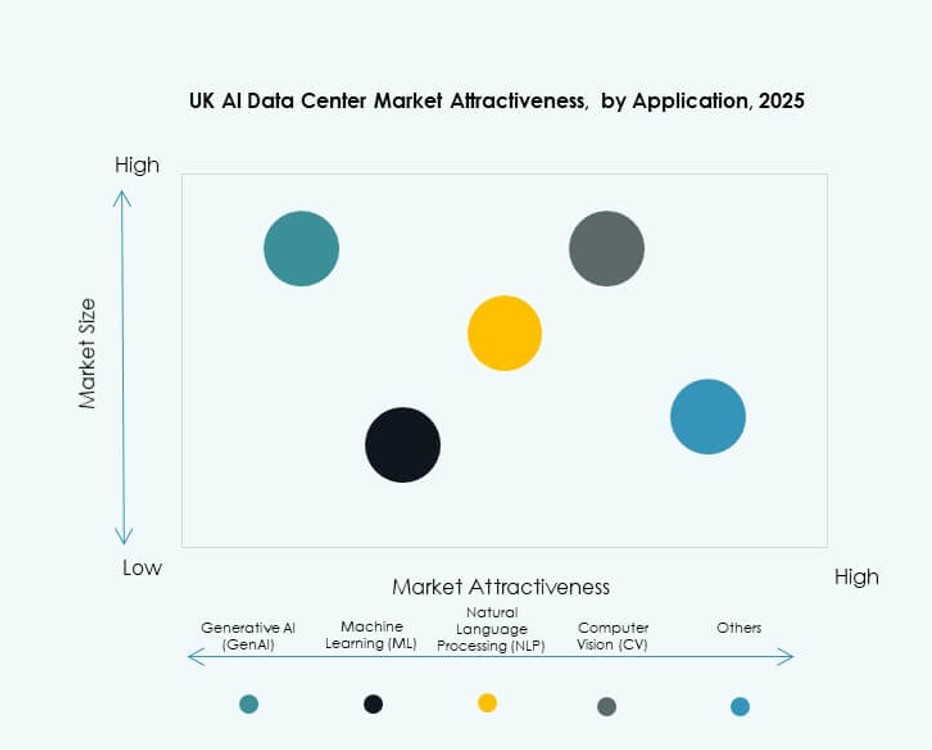

By Application

Machine learning leads the market share in the UK AI Data Center Market, driven by cross-sector AI application development. Generative AI is the fastest-growing segment with high compute demands. NLP and CV workloads grow through adoption in enterprise automation, surveillance, and smart mobility systems. Other applications include robotics and AI-enhanced analytics.

By Vertical

The BFSI and IT & telecom sectors dominate adoption due to early AI integration and compliance needs. Healthcare and retail sectors adopt AI workloads for diagnostics and customer behavior modeling. Manufacturing and automotive drive investment in AI for automation and predictive maintenance. Media and entertainment apply AI to content generation and audience analytics.

Regional Insights

London and Greater South East Lead with Over 55% Share Backed by Hyperscale and Financial AI Workloads

The London metropolitan region leads the UK AI Data Center Market with over 55% share. Strong connectivity, hyperscaler presence, and dense enterprise clusters support AI demand. London’s position as a financial hub drives early adoption of GenAI and predictive models. Proximity to government and public sector agencies further supports infrastructure expansion. Greater South East benefits from renewable energy availability and land access near power infrastructure.

- For instance, Google began construction of its Waltham Cross data center in early 2024 to support AI workloads across Google Cloud and DeepMind. The facility is part of a broader UK infrastructure investment focused on sustainable, high-performance compute.

Midlands and North West Regions Emerging as AI Data Center Corridors with Public-Private Partnerships

The Midlands and North West account for around 25% market share. Regions such as Birmingham and Manchester attract investment through government-backed innovation zones. Tech workforce availability, access to Tier II fiber, and incentives support AI workload deployment. These areas host new colocation and modular facilities to serve regional clients. Public-private initiatives improve site readiness and streamline approvals.

Scotland, Wales, and Northern Ireland Hold 20% Combined Share with Focus on Edge AI and Research-Linked Workloads

Scotland, Wales, and Northern Ireland contribute a combined 20% share of the UK AI Data Center Market. These regions focus on edge AI use cases and research workloads linked to academic institutions. Edinburgh and Cardiff support AI innovation hubs with sovereign data zones. Infrastructure in these areas targets latency-sensitive workloads and AI research clusters. Geographic diversity helps balance national compute infrastructure planning.

- For instance, the University of Edinburgh’s EPCC hosts the UK’s ARCHER2 supercomputer, featuring over 750,000 CPU cores to support advanced research, including AI and machine learning workloads across national academic institutions.

Competitive Insights:

- Amazon Web Services (AWS)

- Microsoft (Azure)

- Microsoft (Azure)

- Google Cloud / Alphabet

- Meta Platforms

- NVIDIA

- ARK Data Centres

- Virtus Data Centres

- Equinix

- Global Switch

- Digital Realty Trust

The UK AI Data Center Market features a dynamic mix of global hyperscalers, regional colocation operators, and AI infrastructure providers. AWS, Microsoft, and Google lead in hyperscale AI infrastructure, investing in high-density GPU clusters and sovereign cloud regions. Meta and NVIDIA focus on AI model training and hardware integration, driving demand for liquid-cooled environments. UK-based players like ARK and Virtus expand campus footprints to host AI-specific workloads. Equinix and Digital Realty serve multi-tenant and interconnect-rich environments for hybrid deployments. The market is marked by aggressive capacity expansion, liquid cooling upgrades, and regional diversification. Strategic partnerships and sovereign AI requirements shape provider decisions on location, design, and scalability. It continues to attract investment from cloud-native and AI-specialized firms looking to support foundation model growth.

Recent Developments:

- In November 2025, Zoom announced plans to open its first UK data center designed for AI‑first services. The London‑based facility will support local infrastructure needs, improve data residency compliance, and offer enhanced AI‑powered collaboration tools. Zoom’s investment in this UK data center underscores its strategy to tailor services for regulated industries such as public sector, healthcare, and financial services.

- In September 2025, NVIDIA announced a major expansion of its AI infrastructure partnership with UK‑based AI infrastructure firm Nscale. The collaboration includes scaling up deployment of up to 60,000 NVIDIA GPUs in the UK as part of a broader commitment to build AI “factories” and support advanced compute workloads.

- In September 2025, CoreWeave revealed a £1.5 billion commitment to expand AI data center capacity in the United Kingdom. This investment builds on previous commitments and targets next‑generation sustainable computing infrastructure.

- In January 2025, Nscale announced a £2 billion investment to build advanced AI data centers in the UK. The investment includes development of modular and fixed AI data center facilities equipped with leading AI compute and liquid‑cooling technologies.