Executive summary:

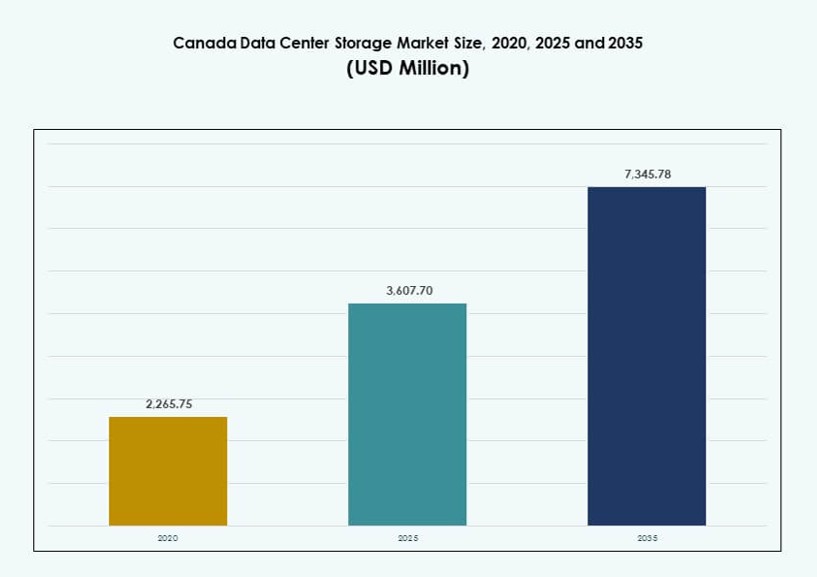

The Canada Data Center Storage Market size was valued at USD 2,265.75 million in 2020 to USD 3,607.70 million in 2025 and is anticipated to reach USD 7,345.78 million by 2035, at a CAGR of 7.31% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Canada Data Center Storage Market Size 2025 |

USD 3,607.70 Million |

| Canada Data Center Storage Market, CAGR |

7.31% |

| Canada Data Center Storage Market Size 2035 |

USD 7,345.78 Million |

The market is evolving rapidly with rising adoption of hybrid cloud and edge computing. Enterprises across industries are upgrading legacy systems with scalable, high-throughput storage to support AI, big data, and real-time analytics. Software-defined storage and all-flash arrays are being deployed to ensure performance, resilience, and compliance. The market plays a strategic role in supporting digital infrastructure needs, making it a priority area for both domestic and foreign investors focused on long-term technology growth in Canada.

Ontario leads the market due to its strong enterprise base, hyperscale presence, and dense cloud interconnectivity. Quebec is emerging fast, supported by low-cost hydroelectric power and green data center initiatives. British Columbia and Alberta are growing as secondary hubs, offering regional storage capacity, energy-sector demand, and proximity to edge workloads. These regions collectively shape Canada’s distributed digital backbone, enabling diversified and resilient storage infrastructure nationwide.

Market Dynamics:

Market Drivers

Cloud Adoption and Digital Infrastructure Modernization Are Driving Data Storage Overhaul Across Canada

The shift toward cloud-first strategies is transforming enterprise IT operations in Canada. Organizations in sectors like BFSI, healthcare, and telecom are rapidly modernizing legacy systems. This shift fuels high demand for scalable, low-latency, and secure data storage. Enterprises require robust infrastructure to support AI, analytics, and mission-critical workloads. The Canada Data Center Storage Market plays a key role in enabling this transition. Businesses are focusing on hybrid cloud environments and flexible architectures. New storage solutions must meet growing data privacy and compliance demands. The adoption of intelligent storage systems ensures better data lifecycle management. These drivers make the market essential for tech investment.

Edge Computing and IoT Applications Increase Demand for Decentralized Storage Architecture

Canada’s distributed population and large geography promote edge computing adoption. This creates strong demand for regionalized data centers with localized storage. Use cases such as real-time analytics, smart cities, and autonomous systems depend on low-latency data access. To support this, organizations are investing in hyperconverged storage infrastructure. It improves performance and reduces transmission delays in edge environments. The Canada Data Center Storage Market supports critical use cases in northern provinces and remote areas. It enables storage closer to users and devices. Enterprises benefit from lower latency, greater reliability, and regulatory alignment. The trend aligns with growing regional digitization efforts.

Rising AI and HPC Workloads Require High-Throughput, Scalable Storage Systems

Artificial intelligence, deep learning, and high-performance computing are increasing storage requirements. Organizations across Canada are deploying GPU-accelerated servers and advanced analytics tools. These technologies demand fast, high-bandwidth storage to function efficiently. The Canada Data Center Storage Market is adapting by integrating NVMe-based all-flash arrays and hybrid setups. These systems support massive IOPS and throughput, critical for AI workloads. Research institutions and tech hubs in Toronto and Montreal lead this shift. Storage solutions must offer scalability, performance, and reliability. Vendors optimize offerings to meet evolving workload needs. Innovation in AI-ready storage is reshaping purchasing decisions across verticals.

- For instance, in H1 2025, CoreWeave pre-leased 52 MW across colocation sites in the Greater Toronto Area to support GPU-intensive workloads, signaling the region’s rapid rise in AI-driven storage demand.

Government Policies and Data Sovereignty Drive On-Prem and Cloud Storage Growth

Canada’s strong data privacy laws and local hosting requirements are influencing storage decisions. Federal mandates and provincial regulations push for greater control over sensitive data. Public sector agencies and regulated industries prefer Canadian-hosted infrastructure. This expands demand for on-premises storage and sovereign cloud environments. The Canada Data Center Storage Market benefits from these legal dynamics. Domestic cloud providers and global firms with local presence gain traction. Investors find value in infrastructure compliant with Canadian and international data standards. This driver reinforces market resilience and long-term growth potential across public and private sectors.

- For instance, in October 2024, Cologix secured USD 1.5 billion in funding to expand its data center footprint across Canada, including storage infrastructure aligned with data sovereignty and regulatory compliance for enterprise and public sector clients.

Market Trends

AI-Powered Storage Platforms and Automation Tools Are Reshaping Data Center Operations

The use of AI in storage management is transforming how enterprises optimize performance. Vendors offer tools that predict failures, reduce downtime, and auto-tier data across devices. In the Canada Data Center Storage Market, AI-driven platforms help manage complex multi-cloud and hybrid setups. These tools ensure data availability, reduce human intervention, and lower operating costs. Businesses rely on analytics to align storage decisions with usage patterns. This trend is vital in sectors handling sensitive or regulated data. AI also improves compliance and threat detection. Automated storage orchestration is becoming a standard for efficiency-focused enterprises.

Energy-Efficient and Sustainable Storage Infrastructure Gains Strategic Priority

Sustainability is now integral to data center investment decisions in Canada. Enterprises are choosing energy-efficient storage to align with ESG goals and reduce carbon footprints. Storage solutions with reduced power consumption and thermal output are in high demand. The Canada Data Center Storage Market reflects this trend in new green data centers. Operators adopt storage technologies that meet LEED and carbon-neutral standards. Investors prefer assets with strong sustainability credentials. This trend supports long-term operational savings and brand positioning. It reflects Canada’s wider clean technology shift and renewable energy push.

Cloud-Native Storage Solutions Drive SaaS and DevOps Enablement

Software-as-a-Service (SaaS) adoption in Canada drives interest in storage tailored for cloud-native workloads. Businesses prioritize systems that support containerized applications and CI/CD pipelines. Object storage, distributed file systems, and API-based access are now essential. The Canada Data Center Storage Market is responding with solutions optimized for multitenant cloud platforms. These systems support microservices and dynamic scaling. Vendors offer tools for seamless data movement across environments. This trend enables agility and faster deployment cycles for businesses. It enhances developer productivity and supports modern application architectures.

Zero-Trust Architecture and Ransomware Protection Reshape Storage Priorities

Cybersecurity concerns are reshaping storage procurement strategies across Canada. Zero-trust architecture and immutable backups are top priorities for IT leaders. Businesses are investing in solutions with encryption, data air-gapping, and anomaly detection. The Canada Data Center Storage Market integrates these features into hardware and software offerings. Data integrity and disaster recovery capabilities are must-haves. Storage systems now function as part of broader security postures. Enterprises rely on storage not just for performance, but for resilience. This trend influences both procurement criteria and vendor differentiation strategies.

Market Challenges

High Capital and Operational Costs Limit Broader Storage Modernization Across Mid-Sized Enterprises

While large enterprises adopt next-gen storage solutions, smaller firms face cost constraints. Advanced storage technologies often require high upfront investment and skilled personnel. The Canada Data Center Storage Market reflects a gap in affordability and access for mid-tier businesses. These firms struggle to transition from aging infrastructure due to budget limits. Operating expenses also increase with advanced cooling and energy requirements. Vendors must address the cost-to-performance ratio for wider adoption. This challenge slows modernization across rural and underserved areas. Government incentives could ease the financial burden and support infrastructure parity.

Data Fragmentation, Vendor Lock-In, and Skills Gap Create Operational Complexity

Managing data across hybrid and multi-cloud environments leads to fragmentation. Businesses find it difficult to unify storage policies and visibility across platforms. The Canada Data Center Storage Market also faces risks of vendor lock-in, limiting flexibility. Migrating data between systems can involve compatibility issues and downtime risks. Organizations require skilled professionals to manage evolving storage technologies. However, the talent pool for these roles remains limited. Without standardization and interoperable tools, businesses face rising complexity. Addressing this challenge requires open standards, cross-platform tools, and workforce upskilling initiatives.

Market Opportunities

Expansion of Hyperscale Data Centers and AI Workloads Unlocks Premium Storage Demand

Canada is experiencing growth in hyperscale data center deployments, particularly in Toronto and Montreal. These facilities require robust storage systems to support AI, cloud gaming, and video streaming. The Canada Data Center Storage Market is well-positioned to meet this demand with high-density, scalable infrastructure. New facilities also attract colocation clients seeking low-latency and secure storage. Investors benefit from predictable demand curves driven by digital consumption patterns.

Edge and Regional Storage Infrastructure Development Creates New Revenue Streams

Growing demand for low-latency data access in edge locations supports decentralized storage deployment. Industries such as mining, logistics, and utilities in remote areas depend on reliable storage. The Canada Data Center Storage Market presents opportunity in building small-scale, edge-ready systems. Vendors offering modular and ruggedized storage units can tap into untapped regional potential.

Market Segmentation

By Storage Type

Hybrid storage leads the Canada Data Center Storage Market due to its ability to balance performance and cost. Enterprises prefer hybrid setups for managing active and archival data simultaneously. All-flash storage is gaining traction in AI and financial sectors that demand speed and reliability. Traditional storage still holds value for legacy systems, though its share is declining. Other niche storage formats cater to specialized workloads in healthcare and research.

By Storage Deployment

Storage Area Network (SAN) systems dominate this segment due to their performance in handling block-level workloads. Enterprises with high-throughput needs prefer SAN for mission-critical applications. Network-attached Storage (NAS) sees growth in collaborative environments, such as education and media. Direct-attached Storage (DAS) remains relevant in edge setups and small-scale environments. Other emerging deployments include disaggregated and composable storage.

By Component

Hardware accounts for the largest share in the Canada Data Center Storage Market, driven by demand for SSDs, enclosures, and controllers. Physical infrastructure remains core to data center investments. Software, however, is rising fast, with storage virtualization, data management, and orchestration platforms expanding rapidly. Software-defined storage solutions offer scalability and lower TCO, attracting cloud-native businesses.

By Medium

Solid-State Drives (SSD) dominate due to superior performance, durability, and energy efficiency. They are widely used in AI and HPC applications. Hard Disk Drives (HDD) remain relevant for bulk storage due to lower costs per terabyte. Tape storage holds niche value in long-term archival, particularly in compliance-heavy sectors. Each medium serves specific use cases based on capacity, speed, and cost.

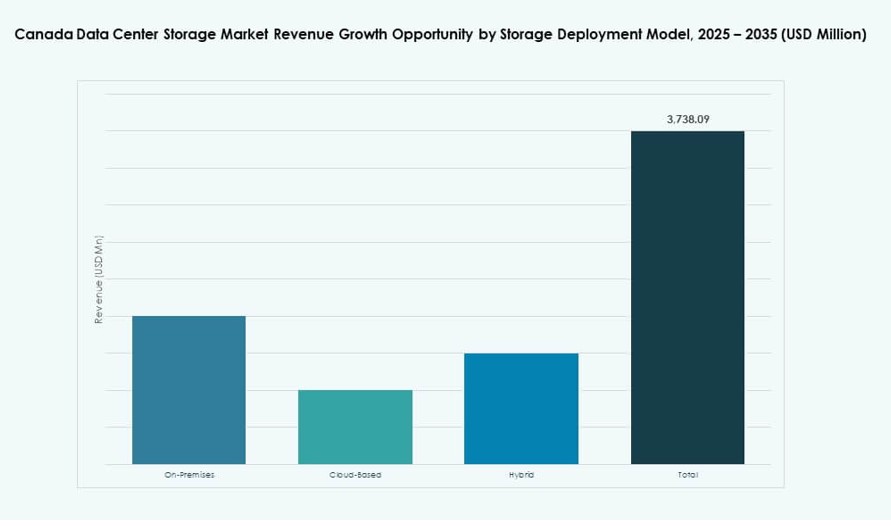

By Deployment Model

Hybrid deployment is leading the market, offering a balance between control and scalability. It allows businesses to combine on-premises storage with cloud environments. Cloud-based storage is growing rapidly, favored by startups and SaaS providers. On-premises deployment still holds significance in sectors like government and healthcare where data control is essential. The diversity in models supports evolving enterprise needs.

By Application

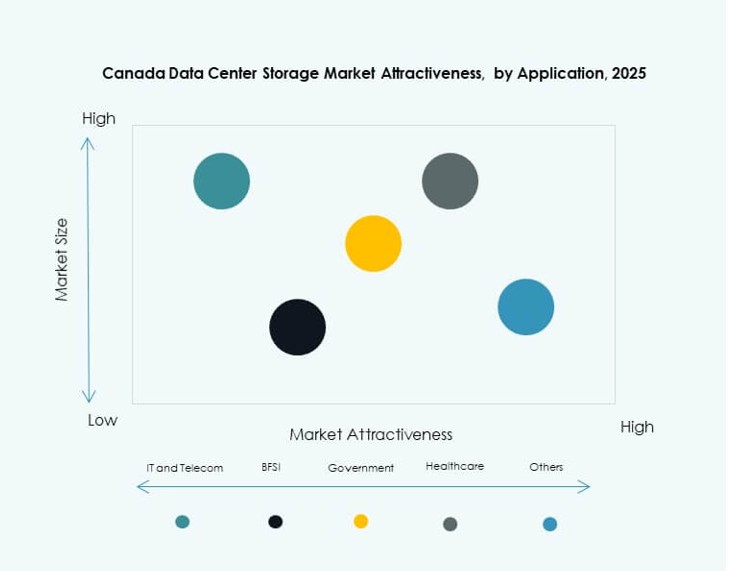

IT and Telecommunications hold the highest share in the Canada Data Center Storage Market. These sectors need scalable, resilient storage for handling user data and network services. BFSI follows closely due to increasing digital banking and regulatory storage needs. Healthcare is growing due to digital records and imaging systems. Government and other sectors contribute steadily, focusing on compliance and data protection.

Regional Insights

Ontario Leads with Over 50% Market Share Due to Strong Enterprise Base and Cloud Connectivity

Ontario dominates the Canada Data Center Storage Market, with over half the market share. Toronto acts as the central hub due to its enterprise density, hyperscale investments, and network access. The region hosts major cloud providers and internet exchange points. It supports a mature digital ecosystem and high storage demand. Enterprises in finance, tech, and media drive continuous infrastructure growth. Ontario’s energy availability and policy support attract sustained investment. It remains the core driver of Canada’s digital storage landscape.

- For instance, CoreWeave led the market in H1 2025 with 52 MW of preleased capacity across wholesale colocation facilities in the Greater Toronto Area, driven by demand for AI and GPU-based storage workloads.

Quebec Emerges as a Green Data Storage Hub Backed by Renewable Energy and Cost Efficiency

Quebec holds around 20–25% of the market, led by cities like Montreal. Low electricity costs and abundant hydroelectric power make it ideal for sustainable data storage. Montreal attracts hyperscalers and colocation providers due to green energy and bilingual services. Quebec also benefits from favorable land and cooling conditions. The government promotes digital infrastructure with targeted incentives. It is a key region for carbon-conscious enterprises and backup operations.

- For instance, Quebec’s data center development pipeline exceeded 600 MW in 2025, driven by access to low-carbon hydroelectricity priced at CAD 0.0537 per kWh, making it one of North America’s most cost-efficient and sustainable locations for storage infrastructure deployment.

Western and Atlantic Canada Offer Emerging Growth Zones for Regional and Edge Deployments

British Columbia and Alberta collectively account for 15–18% of the Canada Data Center Storage Market. Vancouver benefits from subsea cable connectivity and proximity to the U.S. West Coast. Calgary supports energy sector demand and growing enterprise tech ecosystems. Atlantic Canada, though smaller in share, is gaining attention for backup, DR, and regional edge deployments. Local governments support digital expansion with funding and incentives. These regions offer future growth potential in decentralized storage solutions.

Competitive Insights:

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- IBM Corporation

- NetApp

- Cisco Systems, Inc.

- Lenovo Group

- Seagate Technology

- Veeam Software

- Hitachi Vantara

- Huawei Technologies Co., Ltd.

The Canada Data Center Storage Market features a competitive mix of global OEMs, storage software vendors, and integrated infrastructure providers. Dell Technologies and HPE lead with broad portfolios across hardware, software-defined storage, and all-flash arrays. IBM and NetApp remain strong in hybrid cloud and AI storage solutions. Cisco supports integrated network-storage systems for enterprise deployments. Lenovo and Huawei cater to enterprise and hyperscale segments with performance-driven platforms. Seagate and Veeam dominate in HDD and data protection software, respectively. The market is innovation-led, with vendors focusing on energy efficiency, AI-powered storage management, and support for multi-cloud environments. It continues to attract investment through high-growth opportunities in hybrid storage, edge deployment, and sustainability-aligned infrastructure.

Recent Developments:

- In January 2025, Backblaze launched a new data region (CA East) in Toronto, Ontario, and formed a partnership with Opti9 Technologies, Canada’s largest Veeam Cloud Service Provider, to provide compliant, affordable cloud storage solutions emphasizing data sovereignty.

- In October 2024, Cologix secured USD 1.5 billion in capital to fund new data center developments and expand its footprint across Canada, supporting growth in storage infrastructure.