Executive summary:

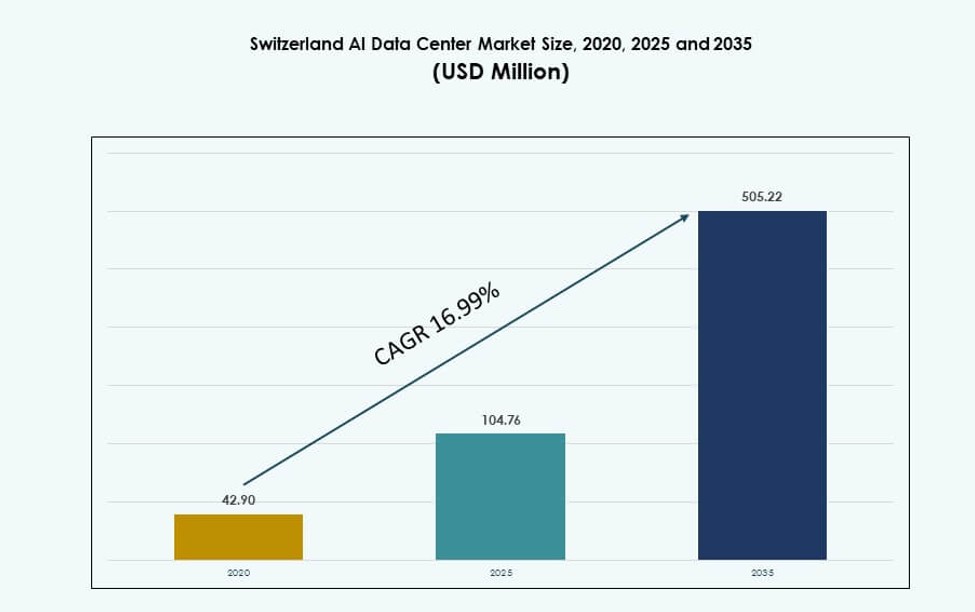

The Switzerland AI Data Center Market size was valued at USD 42.90 million in 2020 to USD 104.76 million in 2025 and is anticipated to reach USD 505.22 million by 2035, at a CAGR of 16.99% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Switzerland AI Data Center Market Size 2025 |

USD 104.76 Million |

| Switzerland AI Data Center Market, CAGR |

16.99% |

| Switzerland AI Data Center Market Size 2035 |

USD 505.22 Million |

The market is witnessing rapid growth driven by high adoption of GPU-based AI infrastructure and compliance-focused deployments. Enterprises prioritize sovereign AI infrastructure aligned with national and European data protection regulations. Leading sectors like BFSI, healthcare, and manufacturing accelerate demand for AI-ready compute clusters. The introduction of liquid-cooled racks, hybrid deployments, and workload-specific zoning has reshaped facility designs. Microsoft’s ongoing investments and ABB’s AI-ready power innovations further enhance infrastructure capabilities. The market’s strategic value lies in its ability to offer secure, scalable, and regulation-compliant environments for enterprise-grade AI development and deployment.

Zurich leads the regional landscape due to its hyperscale presence and strong enterprise base, holding the largest share of the market. Geneva follows as a key hub for research-driven and regulated workloads, with robust connectivity and sovereign cloud initiatives. Bern and surrounding regions are gaining attention for edge AI and university-linked deployments. Each region offers distinct advantages from latency reduction to compliance alignment which strengthens Switzerland’s overall position as a critical node in Europe’s AI infrastructure ecosystem.

Market Dynamics:

Market Drivers

Strong Government Support, Strategic Location, and Data Sovereignty Priorities Shape the Infrastructure Demand

The Switzerland AI Data Center Market benefits from strong regulatory frameworks and national digital strategies that emphasize data sovereignty. Government policies promote the establishment of secure and sovereign AI infrastructure within national borders. Enterprises seek AI infrastructure that complies with Swiss data protection laws and GDPR alignment. Its central European location makes Switzerland ideal for latency-sensitive AI workloads serving regional users. Neutral positioning and political stability attract global firms managing regulated data. Investors prioritize the region for its legal stability and operational continuity. Data-intensive verticals like finance and healthcare further increase infrastructure demand. Strategic colocation near economic hubs drives consistent investments. These drivers collectively strengthen market attractiveness for long-term deployments.

- For instance, Swisscom launched its Swiss AI Platform in November 2024, operated from data centers in Switzerland with Switzerland’s first NVIDIA SuperPOD system, ensuring guaranteed data storage and processing within national borders to comply with Swiss data protection laws.

Advanced AI Workload Demands Fuel Hardware Innovations and High-Density Deployments Across Clusters

AI workload intensification pushes operators to deploy high-density GPU clusters with advanced liquid cooling in Swiss facilities. The Switzerland AI Data Center Market experiences growing demand for high-performance computing tailored to training and inference use cases. Operators integrate direct-to-chip cooling, immersion tanks, and rear door heat exchangers to support thermal loads. Infrastructure providers develop modular data halls that adapt to future AI capacity needs. Strong enterprise adoption of AI analytics, predictive tools, and cognitive models sustains compute demands. BFSI, healthcare, and industrial clients adopt local GPU clusters to meet real-time requirements. Operators use advanced telemetry for energy-efficient workload scheduling. Innovation around rack design and airflow optimization further boosts thermal performance. These technological shifts encourage long-term facility investments.

- For instance, Infomaniak opened a new data center in Geneva in January 2025, powered entirely by renewable hydroelectric energy to handle surging AI compute demands sustainably.

Private AI Cloud, Industry Cloud Models, and Hybrid Deployments Drive Infrastructure Customization

The market gains momentum from enterprise migration toward private AI cloud and hybrid cloud architectures. Enterprises prioritize sovereignty and compliance, pushing demand for custom AI data center configurations. The Switzerland AI Data Center Market supports deployments that blend on-premise security with public cloud agility. Financial institutions and research centers build dedicated AI environments for model training and fine-tuning. Industry-specific AI cloud models emerge in healthcare, manufacturing, and automotive verticals. High-performance edge zones integrate seamlessly with centralized compute for hybrid workflows. This shift encourages facilities to offer flexible rack densities, interconnect options, and GPU-as-a-Service features. Customization drives differentiation and increases investor confidence in future infrastructure returns.

Digital Twin, Simulation, and Language Model Training Accelerate AI Infrastructure Buildout

The rise of foundation models, multimodal architectures, and digital twin simulations boosts AI infrastructure requirements. The Switzerland AI Data Center Market sees demand from enterprises developing proprietary LLMs and industry-specific AI agents. These use cases require dense, scalable infrastructure backed by high interconnect speeds and low-latency nodes. Operators deploy DCIM software with AI-assisted control over power and thermal loads. Enterprise digital twin environments for precision manufacturing and logistics modeling require continuous compute availability. Multilingual AI research efforts further benefit from local model training capacity. Facility operators adapt with custom GPU clusters, smart racks, and edge pods. This workload evolution positions the market as a critical AI infrastructure enabler in Europe.

Market Trends

High-Density Rack Adoption and Liquid-Cooled Infrastructure Expansion Shape Facility Design

The Switzerland AI Data Center Market trends toward AI-ready infrastructure featuring 50–100 kW per rack capacity. Operators deploy liquid-cooled racks using immersion or rear-door liquid systems to manage heat from GPU clusters. Facility designs now prioritize thermally optimized zones with smart rack-level controls. Energy modeling and CFD-based airflow planning become essential during construction. Clients request dense rack configurations with power-usage effectiveness (PUE) below 1.3. Infrastructure suppliers innovate in cabinet design, busway integration, and cable management to meet AI density needs. AI-driven facility optimization software automates cooling and workload balancing. This rack-level shift shapes future design frameworks and investment strategies.

AI-Specific Zoning Within Multi-Tenant and Hyperscale Sites Enhances Workload Segmentation and Resource Allocation

Operators introduce dedicated AI zones within colocation and hyperscale sites to separate AI workloads from standard enterprise compute. The Switzerland AI Data Center Market incorporates zoning to reduce thermal interference, network congestion, and latency issues. Clients reserve isolated AI-ready rooms with dedicated power and cooling pathways. Separate AI clusters reduce contention risks for training jobs involving large-scale datasets. Facility operators offer tiered access models based on workload priority, uptime needs, and fault tolerance. This zoning model also supports infrastructure compliance for sensitive AI deployments in healthcare and banking. Providers integrate AI dashboard monitoring with containerized orchestration. These zones help standardize AI workload delivery across verticals.

Interconnect Density, AI Exchange Points, and Metro Fiber Loops Improve Data Throughput for AI Pipelines

The market advances toward AI-specific interconnect infrastructure that supports distributed training and inference across metro zones. The Switzerland AI Data Center Market integrates high-bandwidth fiber loops linking Zurich, Geneva, and Bern. AI exchange points emerge to reduce hop latency for collaborative compute between universities, enterprises, and cloud nodes. Enterprises adopt direct cloud on-ramps for AI pipeline optimization. New partnerships with telcos deliver AI-grade interconnect solutions near academic clusters. Cross-connect options allow model developers to share datasets and inference loads across hybrid deployments. Network operators develop SLAs specific to AI latency and throughput needs. Interconnect evolution plays a key role in sustaining AI innovation.

AI Infrastructure-as-a-Service (AI-IaaS) and GPU Leasing Models Expand Enterprise Access to AI Compute

Emerging infrastructure-as-a-service models give enterprises flexible access to AI-optimized capacity without full capital investment. The Switzerland AI Data Center Market supports GPU leasing options, short-term cluster rental, and reserved AI pod deployment. AI startups and mid-sized firms prefer opex-based infrastructure use over capex-heavy builds. Facility operators partner with cloud firms and hardware vendors to offer bundled AI stacks. Dynamic allocation of AI resources through orchestration platforms becomes standard. Clients demand access to container-ready environments with pre-configured AI models. AI-IaaS improves infrastructure utilization and expands market participation. These models reshape ownership structures across next-generation facilities.

Market Challenges

High Energy Costs, Renewable Dependency, and Grid Stability Pressure Power Planning and Sustainability Metrics

Energy-intensive AI workloads strain Switzerland’s already expensive electricity market, especially during winter. The Switzerland AI Data Center Market faces pressure to secure long-term green energy contracts to align with sustainability goals. Operators must rely on hydropower and solar procurement, which may fluctuate seasonally. Grid congestion risks rise with the addition of high-density GPU clusters requiring stable multi-MW loads. Backup power planning adds cost and complexity. Achieving Tier IV reliability while maintaining low carbon intensity presents a challenge. Regulatory pressure demands strict ESG disclosures on energy and emissions. These constraints make energy planning a critical factor in site selection and investor confidence.

Talent Gaps in AI Infrastructure Design, Liquid Cooling Integration, and Orchestration Tools Limit Market Speed

The market struggles with a shortage of professionals trained in AI infrastructure planning and advanced thermal system deployment. The Switzerland AI Data Center Market requires engineers skilled in integrating liquid cooling, GPU racks, and orchestration platforms. Local labor pipelines lag behind demand from rapid AI facility rollout. Integrators face delays due to limited availability of certified cooling specialists. Complex DCIM and AI workload schedulers require specialized software training. Enterprises expanding from traditional IT face learning curves in infrastructure orchestration. Upskilling programs remain limited and localized. Talent gaps extend build cycles and increase deployment risk for advanced facilities.

Market Opportunities

Growing Demand for Sovereign AI Infrastructure and Privacy-Focused Compute Supports Investment Inflows

Investors gain from rising enterprise demand for privacy-respecting AI infrastructure tailored to Switzerland’s regulatory environment. The Switzerland AI Data Center Market supports sovereign cloud and edge compute tailored to GDPR and national privacy laws. Global firms deploy secure AI workloads in the region to meet compliance. National AI initiatives support local LLM training and medical research. Market incentives align with investor expectations for stable returns in sovereign compute growth.

Emergence of Vertical-Specific AI Infrastructure in Finance, Healthcare, and Manufacturing Increases Monetization Potential

Sector-focused deployments drive future opportunities for AI-optimized facilities tailored to specific industry needs. The Switzerland AI Data Center Market enables GPU infrastructure aligned with medical diagnostics, fraud detection, or precision engineering. AI service providers co-locate near industry clusters to reduce latency. This alignment allows operators to monetize compute in high-value verticals and expand service portfolios for enterprise AI use.

Market Segmentation

By Type

Hyperscale facilities dominate the Switzerland AI Data Center Market, driven by demand for large-scale AI model training and sovereign cloud deployments. They hold the highest share due to scalability, multi-MW capacity, and global operator investments. Colocation and enterprise data centers follow, serving medium-sized AI workloads and industry-specific deployments. Edge and micro data centers remain niche but are gaining traction in urban zones for inference and real-time AI.

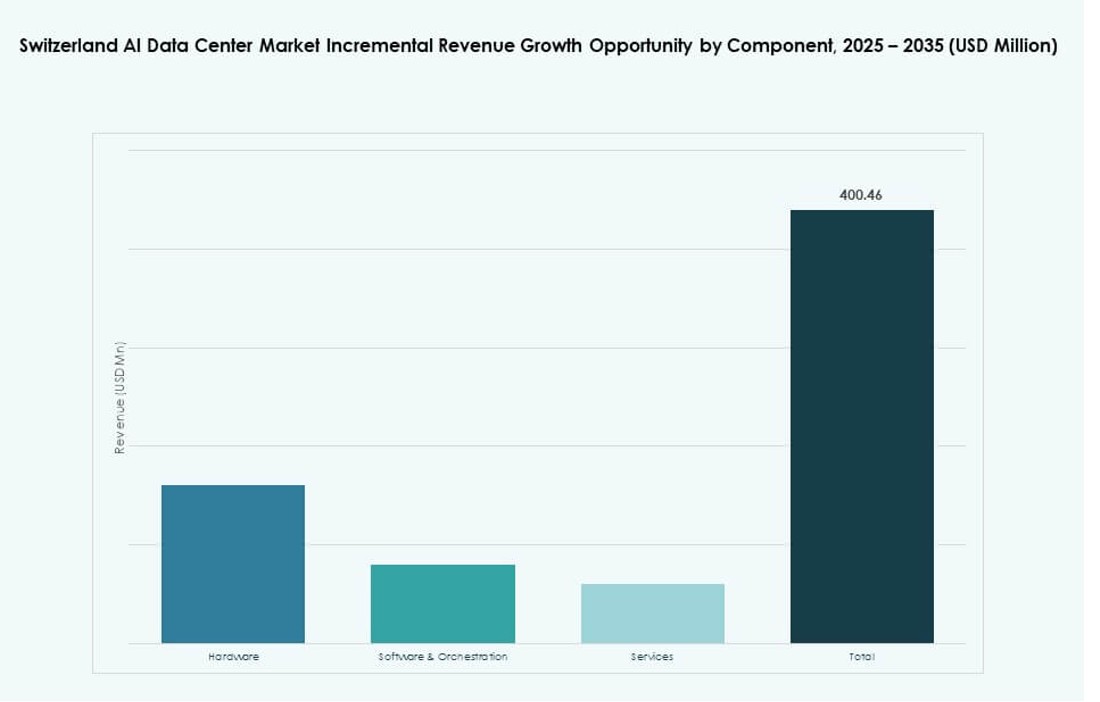

By Component

Hardware holds the leading share in the Switzerland AI Data Center Market, supported by investments in GPU servers, liquid-cooled racks, and high-density power systems. Software and orchestration platforms see rapid growth as AI workload management becomes complex. Services, including integration, monitoring, and lifecycle support, contribute to value-added offerings and long-term client retention, especially in colocation and hybrid setups.

By Deployment

Hybrid deployments dominate due to enterprise demand for flexible AI compute spanning on-premise and cloud environments. The Switzerland AI Data Center Market sees rising adoption of hybrid models in healthcare and BFSI sectors. Cloud-only deployments are growing fast among AI startups and research entities. On-premise remains relevant for high-security workloads and controlled data environments in regulated industries.

By Application

Machine Learning (ML) accounts for the largest application share, powering predictive analytics and automation use cases. Generative AI (GenAI) gains momentum for content creation, LLM training, and synthetic data modeling. Natural Language Processing (NLP) supports multilingual AI development, especially in enterprise AI chatbots. Computer Vision (CV) enables industrial automation and medical imaging use. Others include robotics and forecasting models.

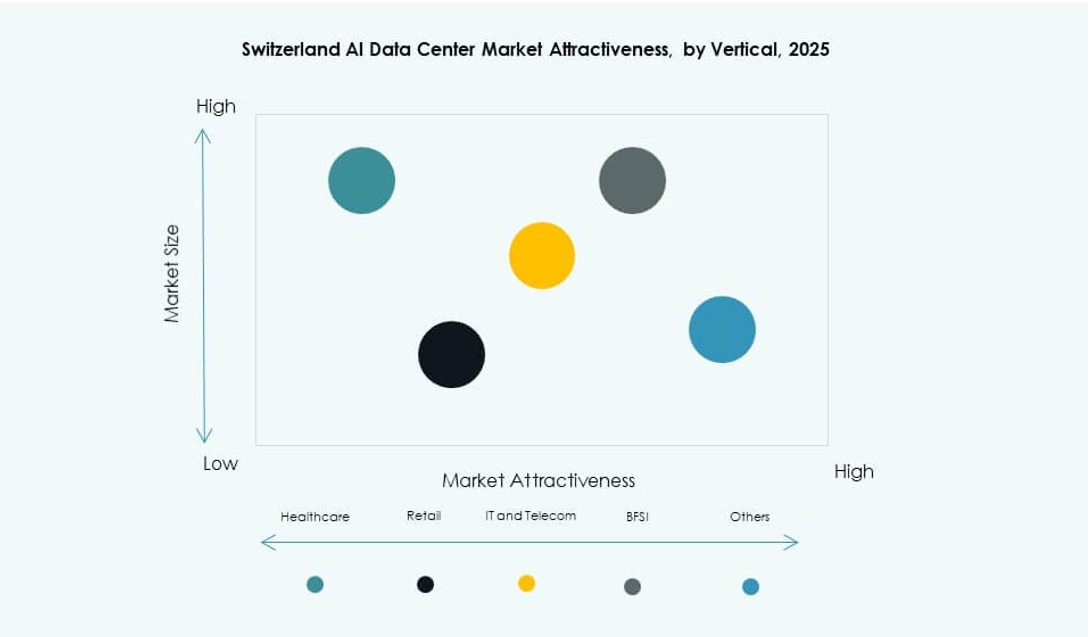

By Vertical

The BFSI vertical leads the Switzerland AI Data Center Market, driven by fraud detection, algorithmic trading, and customer analytics. Healthcare follows closely due to AI-driven diagnostics and secure data processing needs. IT and Telecom support AI-native application delivery and cloud orchestration. Retail, manufacturing, and media sectors adopt AI for personalization, quality control, and immersive content experiences. Automotive and others contribute niche but rising demand.

Regional Insights

Zurich Leads the Market with Over 55% Share Due to Hyperscale Presence and AI Ecosystem Integration

Zurich dominates the Switzerland AI Data Center Market with over 55% share, supported by its role as a financial and tech hub. The region hosts hyperscale facilities backed by global and regional cloud providers. Its proximity to major enterprises and academic AI research labs accelerates workload migration. AI deployments in fintech and insurance create demand for local compute. Zurich offers robust fiber infrastructure, power availability, and regulatory stability. These conditions make it the preferred region for AI-first infrastructure development.

- For instance, Microsoft announced in June 2025 a $400 million investment to upgrade its four existing datacenters near Zurich and Geneva with advanced GPUs for AI infrastructure, serving over 50,000 customers including regulated sectors like finance and healthcare.

Geneva Region Holds Over 25% Share Due to Cross-Border Connectivity and Sovereign Cloud Activity

The Geneva region holds over 25% market share, driven by diplomatic, healthcare, and research sectors requiring AI-ready infrastructure. Cross-border connectivity to France and proximity to multinational institutions enable hybrid AI deployments. Geneva’s energy reliability and skilled workforce support medium-sized facilities with GPU clusters. Healthcare-focused AI models and multilingual NLP applications anchor demand. Several regional operators target Geneva for sovereign AI deployments due to legal neutrality. The region’s appeal continues to grow for AI-regulated workloads.

Bern and Other Regions Contribute Around 20% Share with Emerging Growth in Edge AI and Research Infrastructure

Bern and surrounding areas contribute roughly 20% share of the Switzerland AI Data Center Market. Regional governments support edge AI research, educational AI clusters, and industrial AI use. Universities and applied research labs drive compute needs tied to smart infrastructure and digital twin modeling. The region attracts niche colocation operators deploying modular pods. High-altitude sites offer energy-efficient cooling potential. These conditions foster gradual but steady AI infrastructure expansion beyond traditional metro zones.

- For instance, NorthC Group operates a data center in Biel (Bern region) with 4.0 MW of power capacity, serving as a key communications hub interconnected with its Zurich and Basel sites. The company’s newest AI-ready project a 4.5 MW facility is planned at The Hive campus in Geneva, targeting scientific research and AI workloads near CERN.

Competitive Insights:

- Green Datacenter

- Safe Host

- Exoscale

- Microsoft (Azure)

- Amazon Web Services (AWS)

- Equinix

- Digital Realty Trust

- Google Cloud / Alphabet

- NVIDIA

- Dell Technologies

The Switzerland AI Data Center Market features a mix of global hyperscalers, regional colocation providers, and infrastructure leaders competing across deployment, performance, and regulatory capabilities. It remains highly fragmented with Microsoft, AWS, and Google Cloud driving demand for hyperscale AI clusters in Zurich and Geneva. Green Datacenter and Safe Host serve enterprise and sovereign clients through compliant colocation models. NVIDIA and Dell Technologies support AI hardware integration with advanced GPU stacks and liquid-cooled systems. Equinix and Digital Realty focus on interconnect density and hybrid AI deployments. Providers invest in smart infrastructure, sustainable energy sourcing, and AI-optimized designs to attract vertical-specific AI clients. Competitive pressure encourages innovation across rack density, cooling, orchestration, and modular configurations to meet evolving AI workloads in Switzerland.

Recent Developments:

- In October 2025 ABB and NVIDIA partnered to develop next‑generation power solutions for future AI data centers. ABB announced a collaboration with NVIDIA focusing on scalable power distribution technologies for high‑efficiency AI workloads. The work supports designs for gigawatt‑scale facilities and advanced power architecture tailored to AI infrastructure needs.

- In June 2025, Switzerland‑based ABB introduced new AI‑ready power architectures aimed at data centers, designed specifically to support the higher power density, reliability, and efficiency requirements of AI workloads. In launching these solutions, the company targeted global data center operators that are scaling GPU‑rich infrastructure, reinforcing Switzerland’s role as a technology base for advanced AI data center power systems.

- In June 2025 Microsoft announced a major investment to deepen its cloud and AI infrastructure in Switzerland. Microsoft pledged USD 400 million to upgrade and expand its data centers near Zurich and Geneva, boosting AI service capacity and advanced GPU support. This investment strengthens Switzerland’s role in enterprise AI deployments and cloud-native innovation