Executive summary:

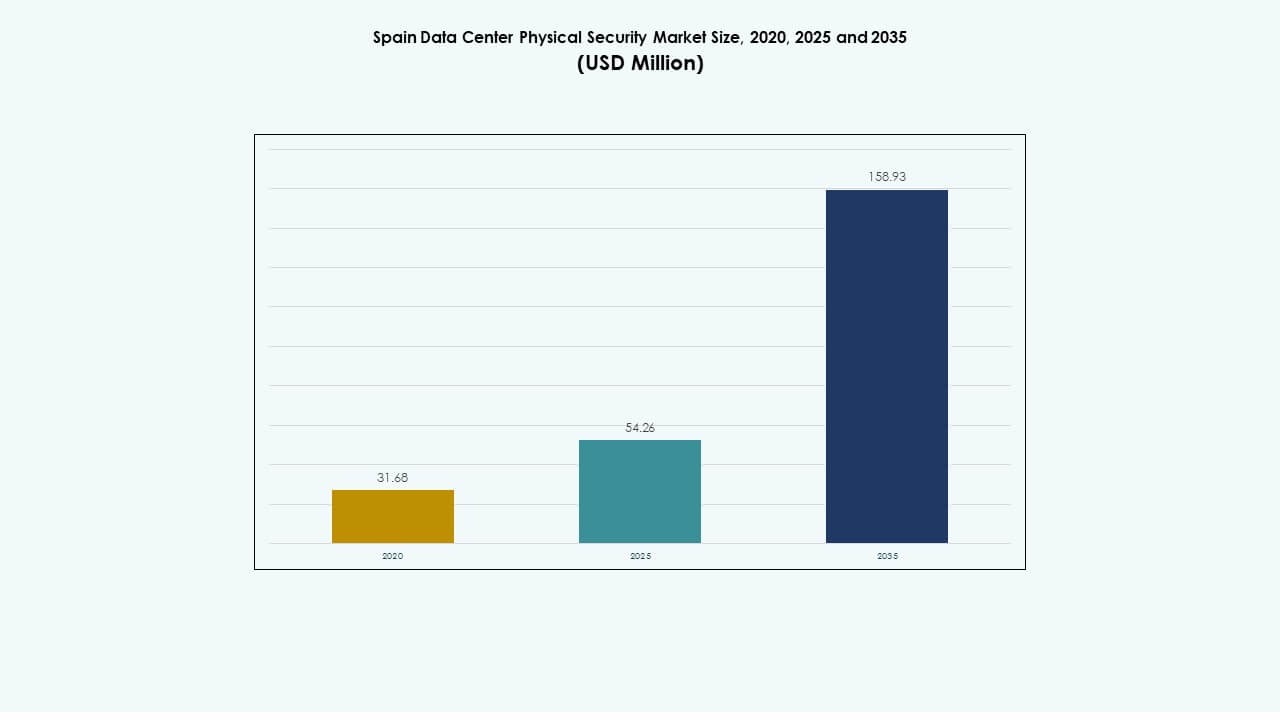

The Spain Data Center Physical Security Market size was valued at USD 31.68 million in 2020, grew to USD 54.26 million in 2025, and is anticipated to reach USD 158.93 million by 2035, at a CAGR of 11.30% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Spain Data Center Physical Security Market Size 2025 |

USD 54.26 Million |

| Spain Data Center Physical Security Market, CAGR |

11.30% |

| Spain Data Center Physical Security Market Size 2035 |

USD 158.93 Million |

Rising deployment of AI-driven video analytics, biometric access control, and IoT-integrated surveillance systems drives the market’s growth. Rapid data center expansion and strict European compliance standards push operators to modernize their physical security infrastructure. Investors view it as a strategic segment that ensures asset protection, operational reliability, and adherence to evolving ESG and data safety norms across digital ecosystems.

Central Spain, particularly Madrid, leads the market due to its high concentration of hyperscale and colocation facilities. Northern regions such as Bilbao and Zaragoza are emerging hubs with sustainable edge data centers supported by renewable energy. Southern areas like Barcelona and Valencia gain traction through growing coastal connectivity and new international cable routes that demand strong physical security measures.

Market Drivers

Market Drivers

Rising Deployment of AI-Powered and Biometric Security Systems Across Critical Data Centers

The Spain Data Center Physical Security Market experiences strong growth with expanding adoption of biometric access, video analytics, and smart perimeter sensors. Operators integrate AI-powered surveillance that identifies unauthorized movement and unusual behavior in real time. This reduces manual supervision and strengthens overall protection layers. Government compliance rules demand advanced monitoring tools to ensure operational transparency. The combination of automation and analytics enhances site reliability. Investors view AI integration as a key differentiator for operational resilience. It fosters innovation and improves customer trust across hyperscale and colocation facilities.

- For instance, Orange España is deploying a private 5G network at the Port of Valencia to connect over 25,000 devices, including surveillance cameras, sensors, and security systems. The network’s dedicated 5G Stand-Alone infrastructure enhances operational safety, supports real-time monitoring, and strengthens the port’s transition toward fully digital and secure logistics operations.

Growing Enterprise Digitization Driving Investment in Physical Security Infrastructure

Expanding digital infrastructure across BFSI, telecom, and manufacturing sectors fuels security system upgrades. Rising deployment of edge and hybrid data centers in Spain increases exposure to threats, prompting higher spending on robust physical protection. Cloud adoption accelerates the construction of new facilities that demand modernized surveillance and access control. Firms deploy AI-based intrusion detection and fire suppression integration to reduce downtime. It attracts global vendors offering modular and scalable protection systems. Businesses view advanced security architecture as essential for compliance with European data safety mandates. This structural evolution enhances Spain’s role in secure data management.

Integration of Smart Building Technologies Enhancing Energy Efficiency and Safety Standards

The growing link between smart building systems and physical security defines a new phase of innovation. Advanced IoT devices enable predictive maintenance, energy optimization, and real-time environmental control. Data center operators integrate environmental sensors with access control and surveillance networks to boost both safety and efficiency. Automation supports 24/7 monitoring with minimal manual intervention. This convergence reduces operating costs while maintaining compliance with sustainability goals. It transforms how companies design future-ready facilities. The market gains a competitive edge through efficient, secure, and energy-conscious infrastructure models.

Regulatory Mandates and ESG Commitments Shaping Investment Decisions

Government rules around GDPR and cybersecurity require facilities to deploy advanced physical defense mechanisms. ESG-focused investors prioritize facilities that follow green building and safety compliance standards. Enhanced reporting transparency drives greater accountability in physical security procurement. Vendors invest in energy-efficient surveillance cameras and digital identity systems. It promotes a sustainable balance between operational resilience and environmental responsibility. Businesses align their risk strategies with these mandates to gain customer confidence. Regulatory-driven modernization continues to guide long-term market stability and capital flow.

- For instance, Spain’s Agency for the Supervision of Artificial Intelligence (AESIA) oversees ethical and regulatory compliance for high-risk AI systems, including those used in security and surveillance. The agency ensures alignment with EU AI Act and GDPR standards, promoting transparency, accountability, and responsible adoption of AI technologies across critical sectors such as data infrastructure.

Market Trends

Market Trends

Rising Integration of AI and Machine Learning in Surveillance and Monitoring Systems

AI and ML algorithms redefine data center protection by enabling faster threat identification and response. Smart analytics detect motion anomalies, tailgating, and behavioral deviations within seconds. These tools minimize human error and enhance site intelligence. The Spain Data Center Physical Security Market benefits from real-time data sharing between subsystems. Predictive alerts reduce downtime and strengthen operational continuity. Cloud-managed systems provide remote visibility across multi-site operations. The trend signals a shift toward proactive and self-learning security ecosystems.

Expansion of Modular and Scalable Physical Security Architectures

Growing demand for flexible infrastructure drives investment in modular protection systems. Operators implement scalable surveillance nodes, access points, and integrated controls adaptable to facility size. This modularity allows faster expansion with lower setup costs. Enterprises prefer plug-and-play models that support future upgrades. It improves return on investment while maintaining compliance. The market experiences a shift toward flexible, easily deployable designs. Vendors that offer hybrid models combining hardware and software layers gain stronger traction.

Adoption of Unified Security Management Platforms Across Large-Scale Data Centers

Operators consolidate multiple security layers under single management platforms for improved coordination. Centralized command centers link access control, video surveillance, and intrusion systems. This integrated visibility enhances decision-making and response speed. The Spain Data Center Physical Security Market shifts toward platforms with automation and analytics built in. Unified dashboards simplify maintenance and reduce integration complexity. Organizations achieve operational synergy between IT and physical security teams. This transition improves scalability and reduces operational silos.

Increasing Focus on Edge Data Center Security and Micro-Site Resilience

Edge computing expansion creates new physical security priorities across smaller, distributed sites. Compact facilities demand cost-effective but advanced surveillance and access management systems. Vendors introduce lightweight AI cameras, digital locks, and low-power monitoring tools. It ensures uniform safety standards across dispersed infrastructures. Edge sites near urban zones gain attention for supporting real-time data processing. The market evolves to protect these mini hubs efficiently. Secure edge nodes strengthen Spain’s overall digital ecosystem and connectivity network.

Market Challenges

High Capital Expenditure and Integration Complexity Across Legacy Systems

Deployment of advanced biometric and AI-enabled systems involves significant upfront costs. Many legacy facilities struggle to integrate modern surveillance and alarm infrastructure within existing frameworks. Compatibility issues delay upgrades and inflate maintenance budgets. The Spain Data Center Physical Security Market faces barriers in scaling due to fragmented architectures. Small operators often lack resources for full automation. Integration across fire, HVAC, and access networks demands expert system design. It slows adoption speed and reduces standardization across facilities.

Data Privacy Concerns and Workforce Skill Gaps Limiting System Optimization

Expanding use of surveillance and biometric data raises compliance challenges under GDPR. Operators must secure sensitive identity records while maintaining transparency. Insufficient training among on-site staff limits the effective use of intelligent tools. Vendors face pressure to design privacy-focused systems with encrypted communication channels. The market experiences slower learning curves in regions with limited technical skill availability. It requires structured partnerships for workforce development. Continuous education programs become essential to ensure proper system operation and compliance alignment.

Market Opportunities

Market Opportunities

Expansion of Green Data Center Development and Sustainable Security Solutions

Spain’s growing renewable energy initiatives support the construction of energy-efficient data centers. Security vendors align products with low-energy IoT devices and smart sensors. The Spain Data Center Physical Security Market benefits from innovations that reduce environmental impact. Solar-powered surveillance and low-voltage access systems enhance ESG credentials. It opens avenues for investment from sustainable infrastructure funds. Vendors developing eco-friendly solutions gain a strong competitive advantage across European projects.

Rising Foreign Investments and Cross-Border Data Infrastructure Projects

Foreign cloud and telecom operators expand in Spain due to strong connectivity and geographic reach. International collaborations create demand for standardized, high-grade physical security protocols. Global companies deploy uniform frameworks for access management and perimeter control. It encourages joint ventures with Spanish integrators and service providers. Enhanced data exchange across European regions supports multi-country security network deployment. These partnerships strengthen Spain’s role as a key security hub in Southern Europe.

Market Segmentation

By Data Center Size

Large data centers dominate the Spain Data Center Physical Security Market due to hyperscale adoption and enterprise cloud expansion. They deploy AI-enabled surveillance, multi-level access control, and advanced perimeter systems. Medium centers show steady demand from regional colocation providers expanding digital capacity. Small facilities focus on cost-efficient modular systems. The shift toward scalable architectures allows smooth technology integration. High security reliability across large sites drives market leadership in this segment.

By Component

The solution segment leads the market due to the growing demand for advanced security systems, including access control and surveillance technologies. Service components gain traction for system integration, consulting, and post-deployment maintenance. It ensures continuous performance and compliance with safety mandates. Vendors offering complete lifecycle services strengthen their competitive position. The balance between hardware and service-based solutions defines the long-term ecosystem.

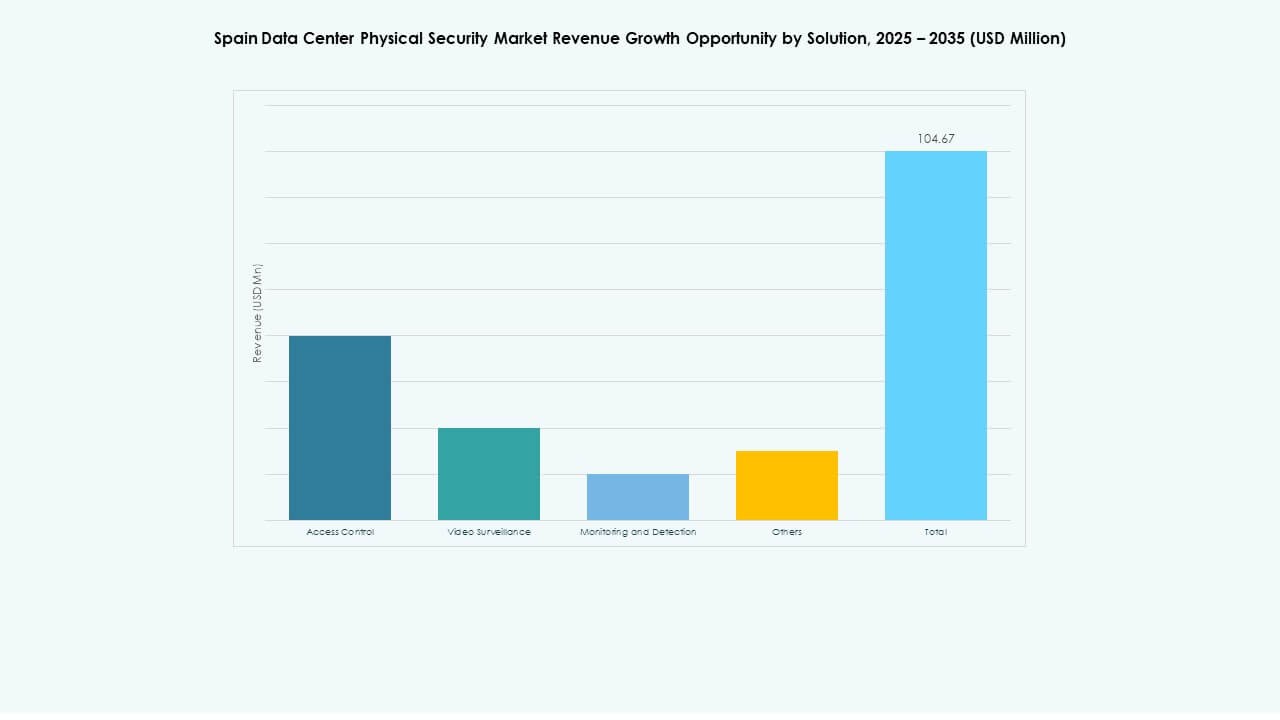

By Solution

Video surveillance dominates due to the integration of AI analytics, motion detection, and thermal monitoring. Access control ranks second with increasing use of biometric identification and multi-factor entry systems. Monitoring and detection solutions expand with IoT sensors and alarm networks enhancing perimeter protection. Other tools such as environmental sensors and fire alarms contribute to overall site safety. It fosters a comprehensive, layered defense structure across Spanish facilities.

By Services

System integration leads the service segment by enabling efficient coordination between hardware and software layers. Consulting services support site assessment and compliance planning. Maintenance and support ensure uptime through preventive system checks. The Spain Data Center Physical Security Market benefits from managed service models reducing operational complexity. Continuous vendor involvement builds client trust and system longevity.

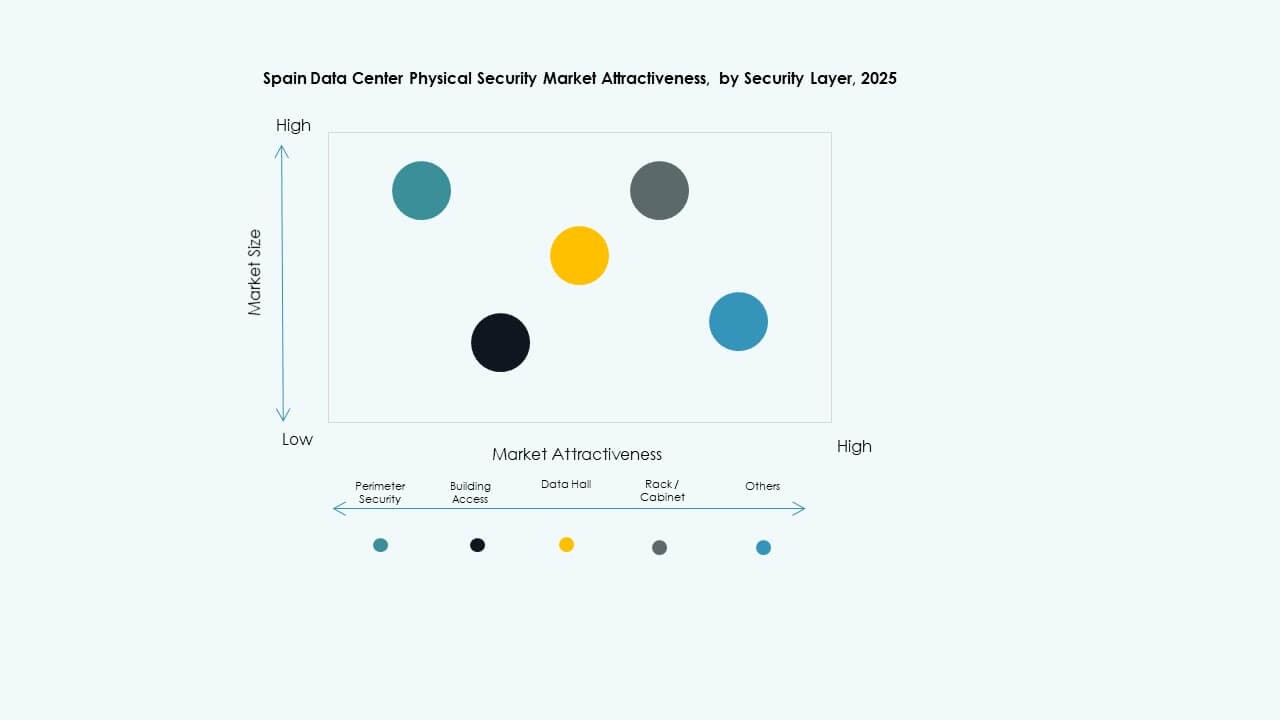

By Security Layer

Building access systems account for the largest share due to strong compliance focus. Perimeter security ranks high with expanding deployment of surveillance cameras and intrusion barriers. Data hall and rack-level protection grow with increased sensitivity of storage zones. Operators use multi-layered security combining both physical and digital measures. It enhances reliability and aligns with Tier III and Tier IV certification requirements.

By Data Center Type

Hyperscale facilities hold the dominant share driven by global cloud providers expanding presence in Spain. Colocation centers grow with rising SME demand for secure hosting. Enterprise and edge data centers follow due to localized data processing requirements. The mix of large and distributed facilities defines the country’s evolving digital landscape. It strengthens Spain’s appeal as a regional technology hub.

By End-user

BFSI leads the market due to high data sensitivity and strict compliance needs. IT and telecom follow with large-scale operational networks requiring continuous uptime. Government, healthcare, and retail sectors show strong adoption for critical service protection. Manufacturing adds gradual demand for industrial automation safety. It highlights a broadening customer base supporting market diversification.

Regional Insights

Western and Central Spain – Established Core of Data Center Security Investments (40% Share)

Madrid and nearby regions host most hyperscale and colocation data centers. Central Spain benefits from robust power infrastructure, fiber networks, and low-risk locations. Global players establish main campuses around these areas to meet enterprise demand. The Spain Data Center Physical Security Market gains strength from proximity to business districts and regulatory centers. It forms the operational backbone of national data protection infrastructure.

- For instance, Equinix’s Madrid data centers implement rigorous security protocols with five security checkpoints, including 24/7 manned security stations, mantraps, and biometric readers. Their infrastructure supports over 600 racks in facilities like MD6 and integrates AI-assisted systems for monitoring.

Northern Spain – Growing Hub for Energy-Efficient and Edge Facilities (35% Share)

Regions like Bilbao and Zaragoza attract new developments for edge computing and renewable-powered data centers. Cooler climate and renewable access support sustainable facility growth. Investors target smaller modular projects with high security standards. Integration of advanced surveillance systems improves regional uptime reliability. It becomes a key zone for balancing national data flow between major cities.

Southern and Eastern Spain – Emerging Zones with Expanding Coastal Connectivity (25% Share)

Barcelona, Valencia, and Malaga witness growing investment driven by strong subsea cable connectivity. The coastal proximity enhances cross-border data transfer with Africa and Western Europe. Emerging players develop mid-sized colocation centers to meet regional service needs. It supports Spain’s broader goal of becoming a Mediterranean connectivity hub. Enhanced perimeter and building access systems secure these high-traffic facilities effectively.

- For instance, Iberdrola and Echelon Data Centres formed a joint venture, Echelon Iberdrola Digital Infra, to develop large-scale data centers in Spain powered by renewable energy. The partnership focuses on energy-efficient infrastructure and sustainable power supply, aligning with Iberdrola’s goal of advancing clean, grid-connected digital facilities across the country.

Competitive Insights:

- Bosch Sicherheitssysteme GmbH

- Securitas AB

- Axis Communications AB

- Honeywell International Inc.

- Johnson Controls

- Schneider Electric SE

- Siemens AG

- ABB Ltd

- Cisco Systems, Inc.

- Genetec

The Spain Data Center Physical Security Market features intense competition among global technology leaders and specialized security integrators. It includes companies with deep portfolios in surveillance, access control, and building automation. Bosch, Axis, and Honeywell strengthen their positions with AI-enabled analytics and integrated monitoring systems. Schneider Electric and Siemens lead through infrastructure automation and smart facility management. Securitas and Johnson Controls deliver comprehensive security-as-a-service models targeting hyperscale and colocation operators. It shows rising collaboration among OEMs and integrators for cloud-managed solutions. Continuous innovation in edge analytics, mobile credentialing, and zero-trust physical access models shapes market leadership.

Recent Developments:

Recent Developments:

- In June 2025, Siemens AG opened a new data center technology hub in Madrid, Spain, with a satellite team in Aragon, to develop sustainable digital infrastructure solutions tailored for data centers across Spain and Portugal, creating 30 jobs over three years.

- In June 2024, Honeywell International Inc. completed the acquisition of Carrier Global Corporation’s Global Access Solutions business for $4.95 billion, enhancing its building automation portfolio with advanced access control solutions like LenelS2, Onity, and Supra, which support security needs in data centers including those in Spain.