Executive summary:

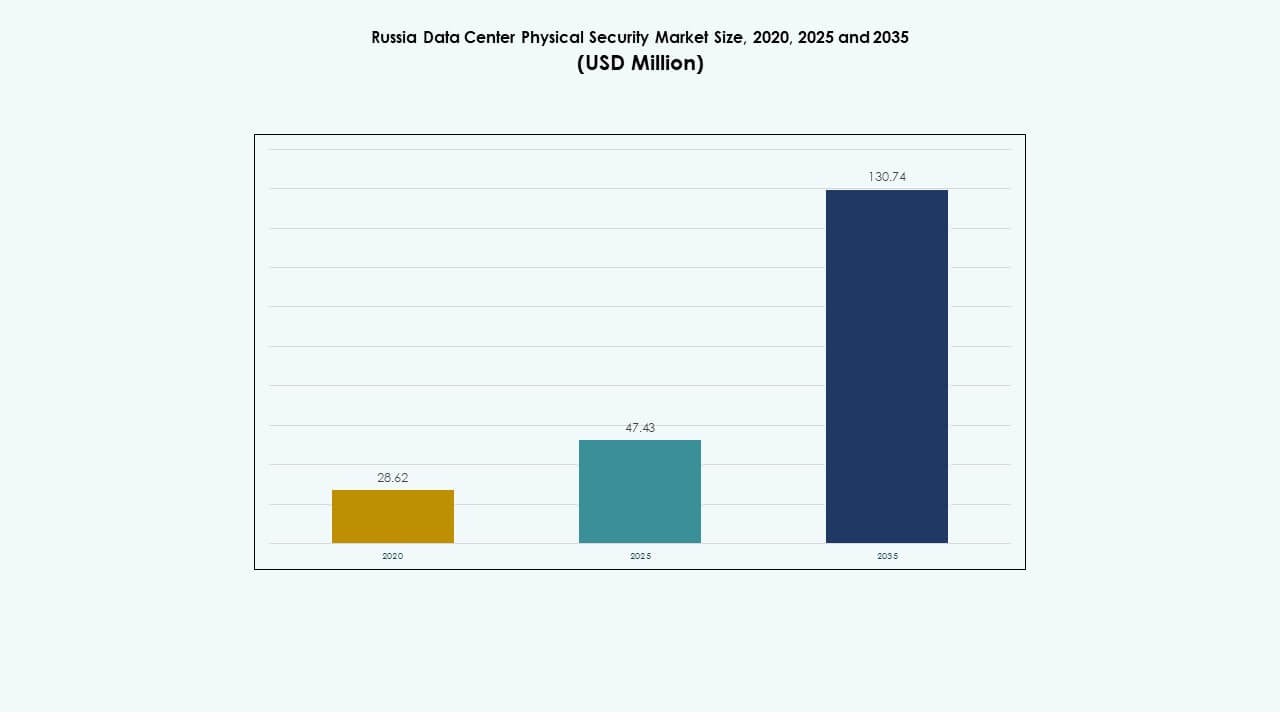

The Russia Data Center Physical Security Market size was valued at USD 28.62 million in 2020, reached USD 47.43 million in 2025, and is anticipated to reach USD 130.74 million by 2035, at a CAGR of 10.63% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Russia Data Center Physical Security Market Size 2025 |

USD 47.43 Million |

| Russia Data Center Physical Security Market, CAGR |

10.63% |

| Russia Data Center Physical Security Market Size 2035 |

USD 130.74 Million |

Strong growth in Russia’s data center ecosystem drives rising investments in multi-layered physical security systems. The adoption of advanced technologies such as AI-enabled video analytics, biometric access control, and IoT-integrated surveillance reshapes operational standards. It has become strategically important for investors and operators seeking compliance with national cybersecurity laws, while enhancing resilience against intrusion and infrastructure failures. Continuous upgrades in access control and monitoring systems reinforce confidence among enterprises and government sectors.

Western Russia, led by Moscow and Saint Petersburg, dominates the market due to its high concentration of hyperscale and colocation facilities. Emerging activity is seen in Yekaterinburg, Kazan, and Novosibirsk, where telecom and IT providers are expanding capacity. These regions attract new projects due to growing demand for data localization and secure cloud infrastructure. The regional spread reflects Russia’s effort to decentralize its data network while maintaining high standards of physical protection and operational reliability.

Market Drivers

Market Drivers

Growing Emphasis on Integrated Security Architecture and Data Sovereignty

The Russia Data Center Physical Security Market benefits from increasing focus on unified security systems combining video surveillance, biometric access control, and intrusion detection. Local enterprises emphasize domestic data storage due to geopolitical conditions and cybersecurity laws, driving investment in physical protection systems. It benefits from policies ensuring sovereign control over digital assets and critical infrastructure. Government-backed projects enhance spending on access management and facility monitoring. It continues to evolve as companies adopt integrated command platforms for threat visibility. Rising awareness about data integrity influences procurement strategies. It strengthens investor confidence in long-term security compliance and operational continuity.

Adoption of AI and IoT-Driven Physical Security Systems Across Facilities

Integration of artificial intelligence, IoT sensors, and advanced analytics transforms how Russian data centers secure perimeters and assets. The adoption of facial recognition, motion detection, and predictive maintenance technologies strengthens operational resilience. It benefits from automation that minimizes human intervention and improves incident response times. Security vendors develop localized AI models tailored to Russian regulations. Data centers employ edge analytics to process large surveillance datasets in real time. Growing 5G connectivity enhances data throughput for distributed monitoring systems. It attracts technology investors seeking scalable innovation in critical infrastructure. Continuous upgrades reflect a shift toward intelligent, adaptive protection ecosystem.

- For instance, added: Johnson Controls unveiled AI-integrated physical security solutions at the Global Security Exchange (GSX) 2024, including models for facial recognition, motion detection, and predictive monitoring. Their platforms leverage IoT sensors and edge analytics to improve incident response, enhancing security automation while complying with regional regulations.

Rising Investment in Hyperscale and Colocation Facilities Drives Market Expansion

Russia’s growing hyperscale and colocation projects demand advanced physical security solutions to manage access and environmental monitoring. Increasing foreign participation under joint ventures supports infrastructure development. It accelerates the deployment of multi-layered access systems, perimeter fencing, and automated visitor tracking. Vendors focus on modular designs for scalability and efficiency. Large players adopt redundant surveillance networks integrated with data management platforms. The growth in enterprise IT load encourages facility operators to prioritize asset protection. Rising capital flows from telecom and cloud providers expand market depth. It remains strategically vital for ensuring trust and uptime in mission-critical environments.

- For instance, Huawei continues to expand its global data center infrastructure through investments in modular, energy-efficient, and AI-ready facilities. In 2024, the company advanced its data center solutions with integrated power, cooling, and lifecycle management systems designed to enhance reliability and scalability across large-scale deployments.

Regulatory Reinforcement and Local Vendor Development Strengthen Market Stability

Compliance with Russia’s data protection and cybersecurity laws reinforces demand for localized security hardware and software. Domestic manufacturers gain momentum by aligning with state security frameworks. The market supports certified technologies meeting Federal Service for Technical and Export Control (FSTEC) standards. It experiences growth as enterprises aim to reduce foreign dependency in physical protection solutions. Increasing audits drive modernization of aging surveillance infrastructure. Government incentives boost adoption of domestic biometric systems. It strengthens the supply chain for sustainable security innovation. The alignment between regulation and investment continues to anchor the sector’s competitive edge.

Market Trends

Market Trends

Shift Toward Smart Command Centers and Real-Time Security Intelligence

Data centers across Russia implement centralized control hubs integrating access, alarms, and video feeds for unified management. AI-driven analytics deliver situational awareness through automated threat detection. It leads to faster response cycles and lower operational costs. Enterprises use digital twins for risk visualization and performance optimization. Smart dashboards display live perimeter integrity metrics to improve compliance reporting. Integration with cloud-native platforms simplifies cross-site monitoring. Vendors introduce adaptive software layers for better interoperability. The trend reflects a move toward predictive and connected facility management.

Increasing Use of Biometric and Multi-Factor Access Controls Across Facilities

Demand for stronger identity verification tools accelerates deployment of fingerprint, facial, and iris scanners. Multi-factor authentication now supports physical and digital asset protection. It ensures secure access while aligning with evolving compliance standards. Facilities integrate AI to monitor abnormal behavioral patterns in real time. Remote management tools expand to support 24/7 operational oversight. Vendors enhance anti-spoofing accuracy using AI-based image processing. Integration with personnel databases improves audit trails. The trend reflects a clear transition toward human-centric, automated verification environments.

Emergence of Edge Security Deployment in Distributed Infrastructure Models

Edge computing growth drives deployment of physical security systems closer to localized data nodes. Operators adopt lightweight monitoring systems supporting autonomous operation. It ensures resilience and faster incident containment without relying on central servers. Vendors design compact access control systems with remote diagnostic features. Edge-enabled video analytics provide low-latency situational insights. Integration with AI enables self-learning surveillance across dispersed environments. Regional operators view these deployments as cost-efficient and scalable. The trend reshapes how distributed infrastructures maintain consistent security standards.

Sustainability-Linked Security Investments and Energy-Efficient Designs

Rising operational costs push data center owners to adopt energy-conscious security systems. Smart cameras and access units use low-power chips to reduce environmental load. It enhances facility sustainability while supporting national green transition goals. Vendors integrate renewable energy compatibility in new infrastructure designs. Efficient hardware extends system uptime during outages. Security devices now support remote firmware updates for longer lifecycle use. The approach appeals to investors focusing on ESG-linked assets. It positions security modernization as part of Russia’s sustainable infrastructure strategy.

Market Challenges

Market Challenges

Dependence on Imported Technology and Integration Barriers

The Russia Data Center Physical Security Market faces challenges due to reliance on imported sensors, cameras, and analytics platforms. Limited access to advanced semiconductor components slows innovation in domestic manufacturing. It creates integration issues when aligning foreign hardware with local compliance standards. Operators often struggle with interoperability between legacy and new systems. Vendors face cost pressure amid currency volatility and logistical constraints. Market fragmentation limits standardization of equipment. Regulatory restrictions complicate partnerships with Western suppliers. The supply chain disruption continues to hinder smooth technology adaptation across facilities.

Complex Compliance Landscape and Rising Cyber-Physical Threat Convergence

Frequent regulatory changes add complexity to physical infrastructure planning. It forces operators to redesign access systems for compliance alignment. The growing overlap of cyber and physical threats increases vulnerability points. Security teams need advanced training to handle blended attack scenarios. High initial investment costs deter smaller facilities from upgrading outdated systems. Legacy data centers remain prone to unauthorized entry and power disruptions. Insurance firms demand stricter risk assessments before coverage approvals. This environment challenges both established operators and new market entrants in maintaining consistent security performance.

Market Opportunities

Expansion of Regional Data Centers and Domestic Cloud Providers

Russia’s regional data center expansion offers growth potential for vendors offering scalable protection systems. Emerging cloud providers invest in facility resilience to meet government hosting regulations. It encourages the development of localized biometric, surveillance, and access technologies. Domestic production incentives create space for innovation and competitive pricing. Partnerships between telecom and IT firms accelerate adoption of integrated systems. The trend supports diversification across regional hubs and tier-2 cities. Investors recognize strong returns from physical infrastructure enhancement. The sector’s growth aligns with long-term digital transformation programs.

Growing Export Potential for Locally Developed Security Technologies

Government support for technological independence boosts export capabilities of Russian security firms. It leads to innovation in smart cameras, AI analytics, and embedded sensors suitable for international markets. Regional collaborations enhance brand presence across Eastern Europe and Central Asia. Vendors target cross-border colocation projects requiring customized compliance modules. It strengthens trade relations while diversifying revenue streams. Rising confidence in homegrown expertise increases global competitiveness. The opportunity fosters a resilient ecosystem of local innovators. Partnerships with state programs ensure sustained international outreach.

Market Segmentation

By Data Center Size

Small and medium data centers dominate the Russia Data Center Physical Security Market due to increasing regional demand for compact and energy-efficient infrastructure. Large data centers, including hyperscale facilities, follow with higher investments in integrated systems. Growth in smaller sites reflects the spread of digital transformation into secondary cities. Vendors focus on modular and scalable solutions suitable for limited space environments.

By Component

Solutions lead the component segment, representing the bulk of spending due to continuous demand for video surveillance and access control tools. Services grow rapidly as integration and maintenance become key for lifecycle management. It benefits from consulting and remote diagnostic support enhancing system uptime. Market players emphasize turnkey delivery and long-term support agreements.

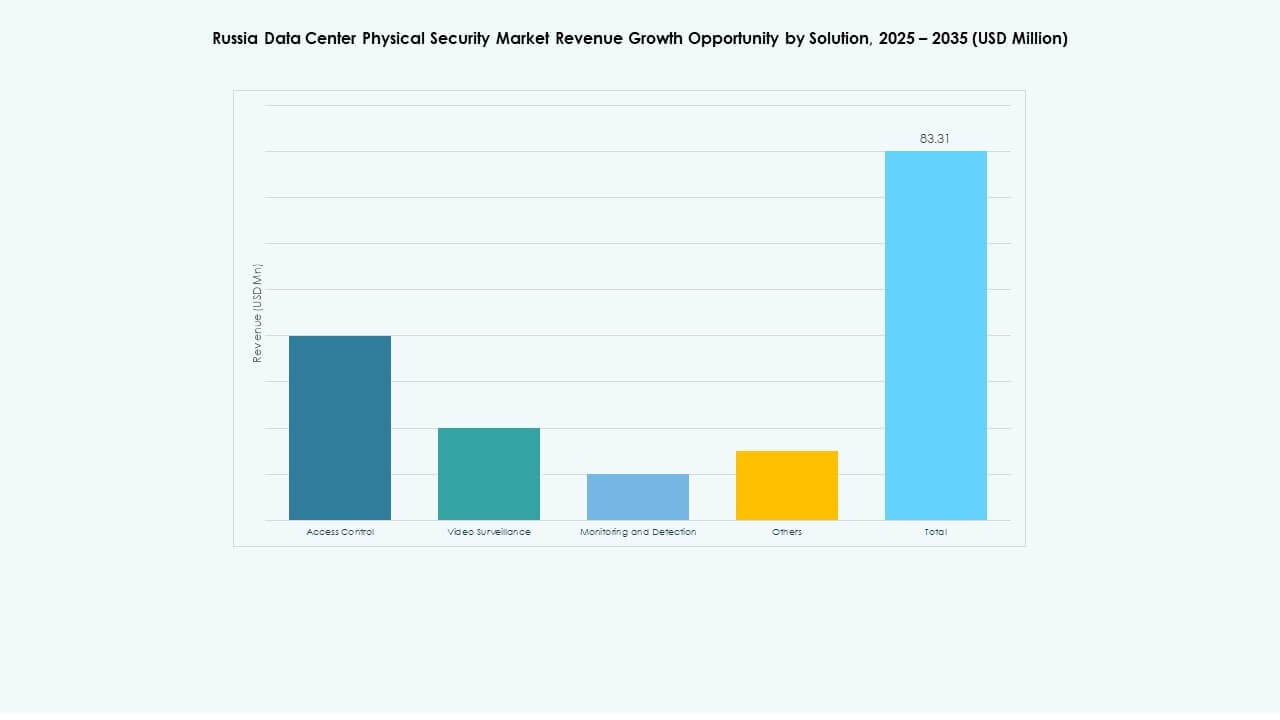

By Solution

Video surveillance holds the largest share driven by demand for AI-based analytics and perimeter monitoring. Access control follows with rapid adoption across government and commercial data centers. Monitoring and detection technologies expand as facilities aim for real-time incident awareness. Vendors integrate these categories under unified command platforms for improved coordination.

By Services

System integration dominates the services segment as enterprises deploy multi-vendor systems requiring seamless interoperability. Consulting services expand through compliance-driven projects. Maintenance and support ensure consistent operational stability across distributed data centers. Service providers emphasize predictive maintenance using IoT sensors for continuous system health evaluation.

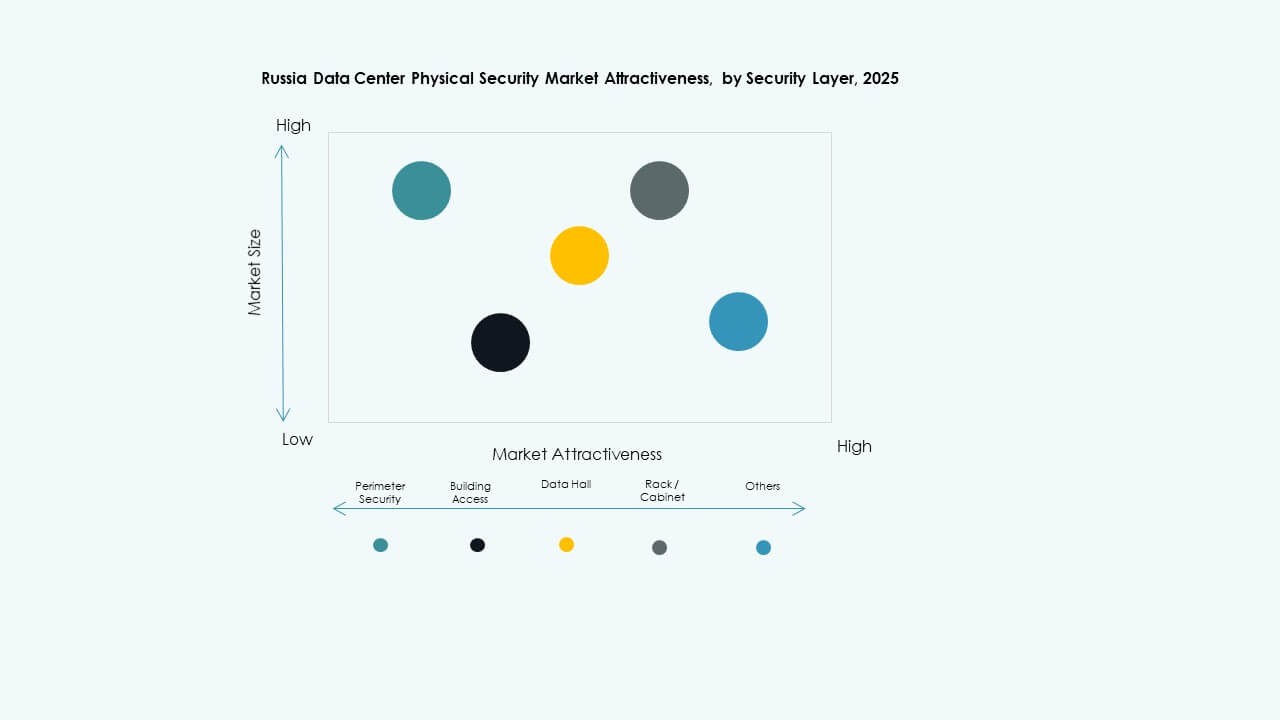

By Security Layer

Building access and data hall layers account for major shares, reflecting core operational security needs. Perimeter security gains importance in hyperscale facilities handling high traffic. Rack-level protection emerges among colocation operators offering shared environments. Vendors focus on layered frameworks balancing coverage depth with cost efficiency.

By Data Center Type

Colocation facilities lead due to the surge in shared infrastructure adoption. Enterprise and edge data centers record strong growth, driven by decentralized computing demand. Hyperscale centers follow as foreign and local cloud firms expand infrastructure footprints. It strengthens multi-tier investment appeal across the Russian data ecosystem.

By End-user

IT & telecom lead end-user adoption due to extensive infrastructure networks and regulatory demands. BFSI and government sectors follow with strict compliance standards for data protection. Healthcare and e-commerce players adopt modern systems to ensure patient and transaction security. Manufacturers integrate smart surveillance to prevent industrial theft.

Regional Insights

Western Russia (Moscow and Saint Petersburg)

Western Russia commands over 60% of the Russia Data Center Physical Security Market, led by high data center density and enterprise concentration. Moscow hosts major hyperscale and colocation facilities, drawing substantial security investments. Saint Petersburg follows with growing fintech and telecom infrastructure. It serves as the technological hub for integrated surveillance and access control solutions. Local authorities emphasize compliance-driven upgrades, ensuring operational resilience in urban centers.

- For instance, DataPro Moscow II features over 150 CCTV cameras with motion detectors for 24/7 security surveillance, alongside 1,600 racks capacity and 11 MW power supply with dual independent inlets, pursuing Uptime Institute Tier IV Design & Facility certification.

Central and Volga Regions

Central and Volga regions hold nearly 25% of market share, supported by emerging industrial and logistics corridors. Government and energy enterprises dominate investment in secure infrastructure. It gains traction through modernization programs and new data storage hubs in Kazan and Nizhny Novgorod. Expanding cloud facilities drive local demand for monitoring and detection systems. Regional initiatives support adoption of Russian-made security products. These areas form a growing mid-tier ecosystem linking western and eastern markets.

- For example, Rostelecom’s subsidiary RTK‑TsOD launched a data center in Nizhny Novgorod in June 2025. The facility spans 3,539 sqm, features 401 racks and delivers 5 MW IT capacity, supporting regional infrastructure growth.

Siberia and Far East

Siberia and the Far East together contribute around 15% of total market value. Infrastructure development in Novosibirsk and Vladivostok drives gradual adoption of access control and video systems. It benefits from favorable land and energy costs for large-scale data center operations. The regions attract new colocation and edge projects serving Asia-Pacific connectivity. Harsh environmental conditions encourage deployment of ruggedized security hardware. These territories are emerging as strategic extensions of Russia’s digital backbone.

Competitive Insights:

Competitive Insights:

- ABB Ltd

- Siemens AG

- Cisco Systems, Inc.

- Bosch Sicherheitssysteme GmbH

- Honeywell International Inc.

- Schneider Electric SE

- Axis Communications AB

- Genetec Inc.

- Fortinet, Inc.

- Palo Alto Networks, Inc.

In the Russia Data Center Physical Security Market, these players maintain competitive positions by blending global experience with tailored solutions for local requirements. ABB and Siemens supply large-scale infrastructure controls and access management systems that appeal to enterprise customers. Bosch, Axis, and Genetec lead with advanced video analytics and surveillance tools. Cisco, Fortinet, and Palo Alto Networks push the boundary between cyber and physical security, offering integrated protection suites. Honeywell and Schneider provide comprehensive building automation combined with security. Competition drives innovation in modular design, compliance adherence, and bundled service offerings. Firms compete on reliability, compliance track record, and ability to integrate security with data-center operations.

Recent Developments:

- In October 2025, ASSA ABLOY acquired Kentix GmbH, a German company specializing in monitoring and access control products designed for data centers, enhancing their capabilities in physical security for this sector.

- In July 2025, Russia’s Megafon launched new data centers in Yekaterinburg and Tver, each offering 1MW of capacity, reinforcing the company’s physical security infrastructure in these regions. This expansion is part of a broader trend where Russian IT firms are investing in increasing data center capacities to address growing demand amid a capacity crunch in the Central Federal District.

- In June 2024, Honeywell International Inc. completed the acquisition of Carrier Global Corporation’s Global Access Solutions business for $4.95 billion, enhancing its building automation portfolio with advanced access control solutions like LenelS2, Onity, and Supra, which support security needs in data centers including those in Spain.

- In December 2024, Bosch Sicherheitssysteme GmbH sold its security and communications technology product business to the European investment firm Triton. The transaction included three business units Video, Access and Intrusion, and Communication as Bosch aims to focus more on systems integration business.