Executive summary:

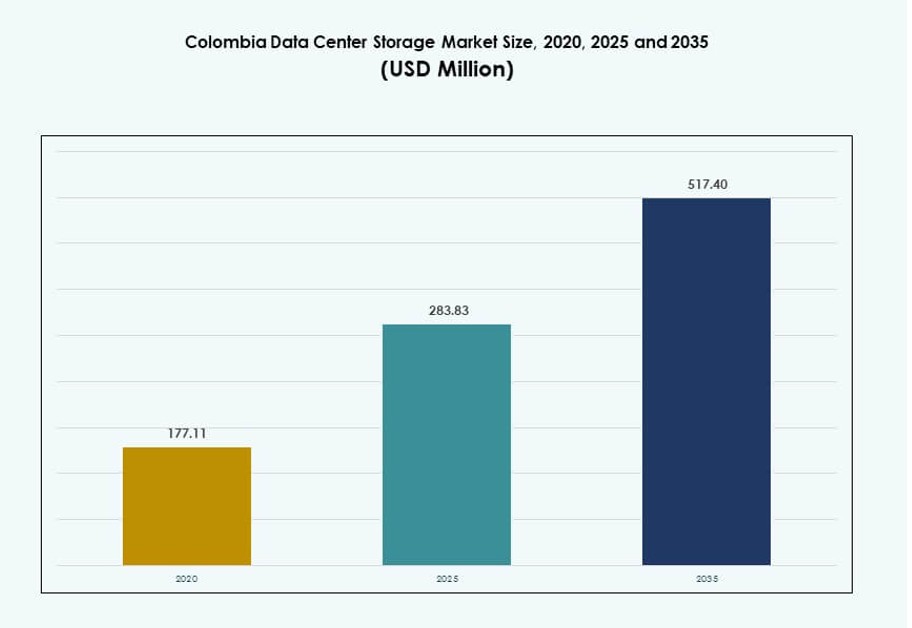

The Colombia Data Center Storage Market size was valued at USD 177.11 million in 2020 to USD 283.83 million in 2025 and is anticipated to reach USD 517.40 million by 2035, at a CAGR of 6.13% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Colombia Data Center Storage Market Size 2025 |

USD 283.83 Million |

| Colombia Data Center Storage Market, CAGR |

6.13% |

| Colombia Data Center Storage Market Size 2035 |

USD 517.40 Million |

The market is driven by digital transformation across financial services, telecom, and public sectors. Enterprises are modernizing storage infrastructure to support hybrid cloud, AI workloads, and compliance with data privacy regulations. Growing use of flash storage, software-defined platforms, and backup solutions is accelerating adoption. Businesses increasingly demand high-availability, scalable systems to support critical workloads. The market plays a vital role in ensuring uptime, performance, and security. Local demand for data localization, analytics, and secure backups is rising. For investors, it represents a stable opportunity in a digitally evolving economy.

Bogotá leads the market with the highest concentration of hyperscale and colocation facilities due to its robust fiber infrastructure and enterprise density. Medellín is emerging with smart city investments and innovation clusters supporting edge deployments. Other cities like Barranquilla and Cali are gaining traction for secondary storage zones and backup hosting. The regional landscape is shaped by infrastructure readiness, digital adoption, and access to power. Urban hubs with scalable energy and low-latency connectivity continue to drive Colombia’s data center storage expansion.

Market Dynamics:

Market Drivers

Rising Cloud Integration and the Push for Scalable Storage Solutions in Enterprise Workloads

Enterprises in Colombia are adopting hybrid and multi-cloud infrastructure to support digital expansion. The need to manage structured and unstructured data across systems has made scalable storage vital. Enterprises require solutions that ensure low latency, high throughput, and seamless data access across locations. This has driven adoption of software-defined storage and storage virtualization technologies. Financial services, telecom, and healthcare sectors have moved fast toward cloud-first strategies. These sectors depend on high-availability storage for analytics, compliance, and disaster recovery. The Colombia Data Center Storage Market benefits from enterprise mandates to modernize aging systems. Legacy platforms cannot handle AI workloads or high-speed data exchange. Organizations are replacing them with intelligent, policy-driven architectures.

Digitalization in Banking, Fintech, and Public Sector Fueling Demand for Secure Storage Infrastructure

The financial and public sectors have accelerated digital transformation to improve service delivery and compliance. Financial institutions face mandates around secure, compliant data storage and data protection. Data localization rules have prompted local banks to build or lease domestic storage infrastructure. The rise in fintech applications and digital wallets has further increased demand for high-availability, encrypted storage. In the public sector, data archival, citizen services, and internal records require structured storage solutions. Government initiatives are investing in digitizing services and modernizing IT systems. These developments make secure and scalable storage critical to operational continuity. The Colombia Data Center Storage Market is benefitting from a combination of compliance pressure and digital service rollout. It supports seamless backend operations for banks and public portals.

AI, IoT, and Edge Computing Shaping Storage Configuration Across Industry Use Cases

The adoption of IoT in logistics, energy, and smart cities is producing massive amounts of edge data. This surge has created a need for decentralized, high-speed storage close to endpoints. AI applications in manufacturing, telecom, and customer service require storage that supports real-time analytics and model training. Data must be transferred, processed, and archived without delay or loss. These use cases are fueling demand for NVMe, all-flash, and object-based storage systems. Cloud-native platforms are expanding their data center presence to handle complex data workflows. Colombia’s growing AI and analytics market is driving integration of intelligent storage infrastructure. The Colombia Data Center Storage Market reflects this shift with vendors bundling AI-ready storage in service portfolios. Enterprises view storage as an enabler of intelligent decision-making.

- For instance, Microsoft’s AI Tour highlighted how organizations in Colombia are embracing cloud and AI solutions to drive business and social impact, with studies showing 59 % of Colombian firms implemented AI within six months and many planning to increase AI budgets.

Colocation and Hyperscale Providers Driving Storage Infrastructure Investments for On-Demand Growth

Colocation demand in Bogotá and Medellín has surged with the expansion of hyperscale and cloud providers. Enterprises prefer leasing space and storage resources instead of investing in costly infrastructure. Storage-as-a-Service (STaaS) offerings allow clients to scale without upfront capital. Global operators like AWS, Azure, and Oracle are expanding local availability zones. This trend is reshaping how businesses access and manage storage. Dynamic workloads from gaming, streaming, and ecommerce require flexible and secure storage layers. Hyperscale players integrate high-speed SSD and NVMe storage to meet service-level agreements. The Colombia Data Center Storage Market is gaining momentum from this shift toward flexible consumption models. It ensures that businesses stay agile without compromising performance or compliance.

- For instance, in February 2024, Cirion Technologies launched its Bare Metal Cloud service at a data center in Bogotá, enabling low-latency, high-performance infrastructure for enterprises deploying hybrid and cloud-connected workloads in Colombia.

Market Trends

Growing Role of Storage Automation, AI-Powered Tiering, and Predictive Management Tools

Data center operators in Colombia are investing in automation to streamline storage lifecycle management. AI-powered tools classify data by access frequency and business value. This allows automated tiering across SSDs, HDDs, and cold storage. Predictive analytics tools help detect faults and optimize storage utilization before issues arise. AI-driven automation reduces manual intervention, lowers operational costs, and improves uptime. It also ensures regulatory data is archived correctly and accessed securely. Storage platforms now integrate machine learning to support autonomous optimization. The Colombia Data Center Storage Market is evolving with this trend. Operators gain visibility and control across large-scale, complex environments.

Shift Toward High-Density Storage Systems to Reduce Space and Energy Footprint

Space optimization has become a major trend in Colombian data centers, especially in urban hubs. Storage density is being improved through the adoption of compact all-flash and blade-based storage units. These systems deliver high IOPS per rack while consuming less power. High-density infrastructure aligns with ESG goals by reducing carbon footprint and lowering cooling costs. Operators are retrofitting legacy racks with denser media to free up real estate. It allows deployment of more compute and storage within the same physical footprint. Flash-based platforms with deduplication and compression features further optimize storage use. The Colombia Data Center Storage Market reflects this trend in design and procurement preferences. It enables operators to meet both capacity and sustainability targets.

Integration of Cyber-Resilient Storage Architectures to Support Business Continuity

With increasing ransomware and data breach incidents, cyber-resilient storage has gained traction. Data center operators are adopting immutable backups, air-gapped storage, and built-in encryption. These security layers safeguard critical business data from cyber threats. Secure storage is especially important in regulated sectors like healthcare, BFSI, and government. Storage solutions now come with real-time anomaly detection and automatic recovery features. Compliance frameworks demand storage that supports auditing and traceability. Cyber resilience is becoming a differentiator in competitive bids and public procurements. The Colombia Data Center Storage Market is shifting toward resilience-focused architectures. Operators integrate these features to enhance trust and reduce recovery costs.

Emergence of Industry-Specific Storage Solutions Optimized for Vertical Applications

Vendors are tailoring storage solutions to match the needs of key verticals. Telecom providers seek scalable object storage for 5G, video, and voice applications. Banks deploy low-latency flash arrays for real-time transaction processing. Healthcare facilities require archival and image-based storage optimized for PACS and EMRs. Government agencies use policy-based storage to automate retention and classification. Education platforms use hybrid storage for LMS data, media content, and backups. Vertical-specific needs are shaping procurement criteria and technical specifications. It improves performance and operational efficiency across industry workflows. The Colombia Data Center Storage Market is expanding with these differentiated storage models that align with sector-specific IT demands.

Market Challenges

High Power Costs, Limited Local Manufacturing, and Supply Chain Constraints Hindering Infrastructure Scaling

Electricity pricing in Colombia affects long-term cost planning for data center operators. High energy costs raise total cost of ownership for storage-heavy applications. Local manufacturing of storage hardware is minimal, forcing dependency on imports. This creates vulnerability to currency fluctuations and customs delays. Supply chain disruptions increase procurement lead time for SSDs, storage blades, and backup systems. Operators face delays when upgrading capacity or deploying new racks. Limited availability of certified engineers also slows down complex storage integration. The Colombia Data Center Storage Market struggles with these operational and supply-side inefficiencies. It hampers rapid scaling in response to demand spikes.

Fragmented Policy Framework and Urban Zoning Barriers Limiting Hyperscale and Modular Storage Expansion

Land acquisition for large-scale facilities is difficult in urban centers due to zoning constraints. Regulatory approvals for energy, environment, and construction are often delayed. National and regional authorities apply different guidelines on digital infrastructure. This fragmentation causes uncertainty in hyperscale investments and expansion planning. Modular deployments also face delays due to inconsistent licensing. Some regions lack dedicated digital infrastructure incentives. Cross-border data compliance adds complexity for multi-tenant storage providers. The Colombia Data Center Storage Market faces structural hurdles that impact growth velocity. These factors discourage new entrants and slow down time-to-market for local players.

Market Opportunities

Expansion of Regional Edge Storage to Support Smart Cities, IoT, and Decentralized Applications

Cities outside Bogotá are deploying smart grids, surveillance systems, and transport sensors. These applications generate high-volume, real-time data requiring localized storage. Edge data centers with integrated storage are being set up in regional hubs. This opens opportunities for vendors offering compact, rugged storage systems. Healthcare, logistics, and energy operators prefer edge storage to reduce latency. The Colombia Data Center Storage Market can capture growth through these decentralized rollouts. It improves data control and system responsiveness at local levels.

Rising Demand for STaaS and Subscription-Based Models from Mid-Sized Enterprises

Small and medium businesses are adopting pay-as-you-go models to manage costs. Storage-as-a-Service allows clients to scale usage without capital lock-in. Vendors offering tiered pricing and SLA-backed services are gaining traction. Managed storage solutions for compliance, backup, and disaster recovery are also growing. The Colombia Data Center Storage Market supports agile IT procurement for mid-market firms. It provides financial flexibility while ensuring performance.

Market Segmentation

By Storage Type

All-flash storage dominates due to its speed, reliability, and suitability for mission-critical applications. It holds the highest share among storage types, replacing traditional systems in financial and telecom sectors. Hybrid storage also sees adoption where cost-performance balance is needed. Traditional storage remains in legacy use cases but is phasing out. The Colombia Data Center Storage Market is shifting toward flash and hybrid systems for agility and responsiveness.

By Storage Deployment

Storage Area Network (SAN) systems lead in large-scale deployments, driven by demand in banking and telecom data centers. SAN offers high-speed block-level access, ideal for transaction-heavy workloads. NAS systems follow, mainly adopted in media, education, and research applications for file-based access. Direct-attached storage (DAS) finds use in edge setups and smaller deployments. The Colombia Data Center Storage Market shows strong preference for SAN in mission-critical environments.

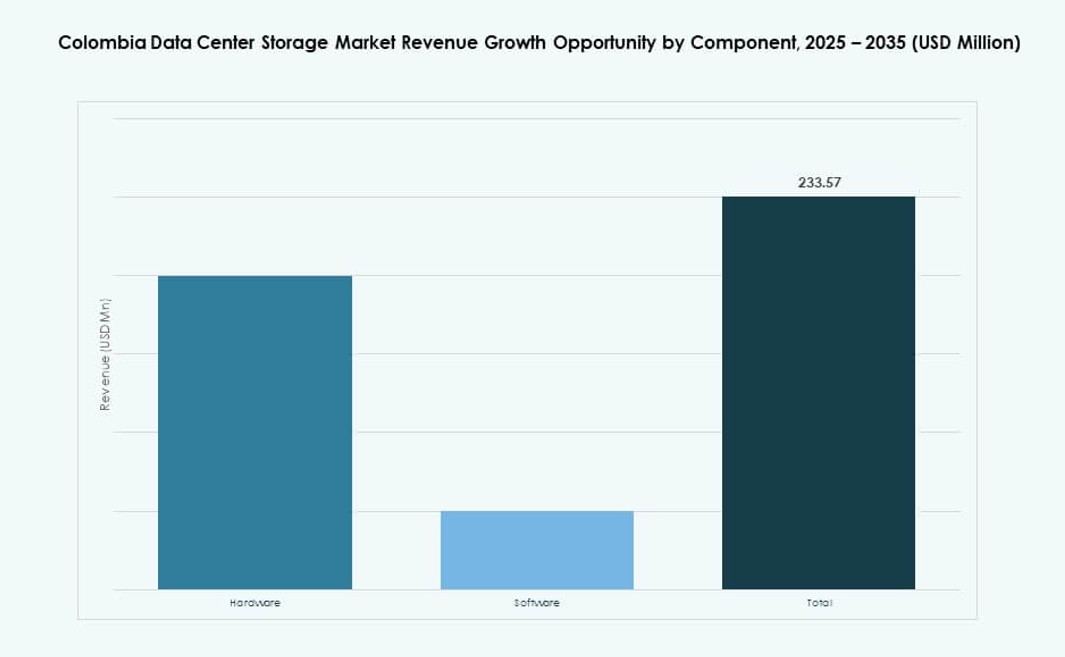

By Component

Hardware holds the larger share of the market, driven by investments in SSDs, servers, and backup infrastructure. Equipment upgrades to support cloud and AI workloads have increased spending on physical components. Software, including storage management and virtualization tools, is gaining traction with hybrid setups. Vendors bundle software with hardware to offer integrated solutions. The Colombia Data Center Storage Market continues to favor hardware-led solutions for capacity and speed.

By Medium

Solid-State Drives (SSD) account for the largest share, owing to faster performance, lower latency, and higher durability. SSD adoption has grown in financial, telecom, and cloud segments. Hard Disk Drives (HDD) are used in backup and archival tasks. Tape storage maintains niche relevance for long-term government and healthcare data. The Colombia Data Center Storage Market reflects this media diversification, with SSDs becoming standard in new deployments.

By Deployment Model

Cloud-based deployments lead due to growing adoption of SaaS, PaaS, and IaaS solutions. Enterprises prioritize cloud-native architectures for flexibility and scalability. On-premises models remain in regulated industries requiring full control. Hybrid models are increasing in popularity for balancing privacy, latency, and scalability. The Colombia Data Center Storage Market supports all three models with rising cloud preference.

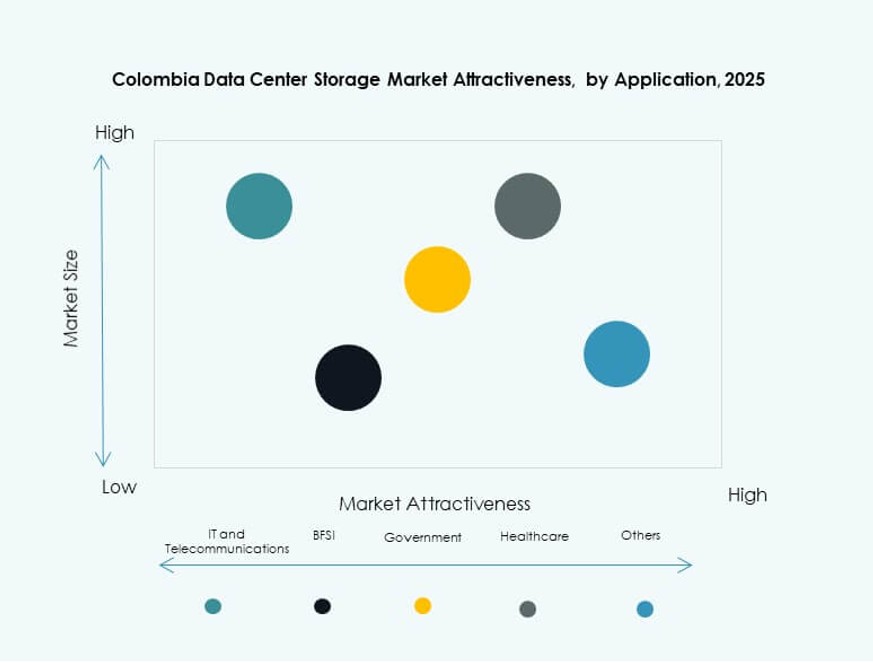

By Application

IT and telecommunications dominate storage usage, driven by data-intensive applications and 5G expansion. BFSI follows, requiring fast, secure, and compliant storage solutions. Government deployments are rising due to digital services and citizen data platforms. Healthcare applications include EMRs, imaging, and backup systems. Other segments include education, retail, and logistics. The Colombia Data Center Storage Market reflects strong demand diversity across verticals.

Regional Insights

Bogotá Metropolitan Region Leads with Over 60% Market Share Due to Infrastructure and Connectivity

Bogotá remains the digital core of Colombia, holding over 60% of the market share. Its high fiber penetration, power stability, and enterprise density support advanced data center operations. Most hyperscale and colocation providers are based here, targeting financial services, telecom, and public agencies. The region hosts the largest data center clusters and availability zones. It offers low-latency connectivity and access to cloud exchange hubs. The Colombia Data Center Storage Market concentrates heavily in Bogotá due to these strategic advantages.

- For instance, Ascenty’s Bogotá 1 data center offers 10 MW of installed power and about 9,500 m² of space in Colombia, providing carrier‑neutral colocation and connectivity services that support scalable enterprise and cloud workloads.

Medellín Emerging with 20% Market Share as Innovation and Smart City Initiatives Take Hold

Medellín accounts for around 20% of the market, supported by its innovation district and tech initiatives. It has invested in digital infrastructure for smart mobility, public data platforms, and education networks. Edge data centers are being deployed to meet regional demand. The city’s business-friendly ecosystem attracts startups and mid-sized enterprises. Public-private partnerships support expansion in digital services. The Colombia Data Center Storage Market benefits from Medellín’s strategic push for tech-driven development.

Barranquilla, Cali, and Bucaramanga Jointly Hold 15–20% Market Share with Growing Edge Deployments

These cities together account for 15–20% of the market and are seeing growing edge deployment activity. Barranquilla and Cali are investing in smart surveillance, e-health, and digital commerce. Bucaramanga supports education, government, and utility applications. Regional demand comes from latency-sensitive services and decentralized applications. Local operators deploy micro data centers to meet near-edge needs. The Colombia Data Center Storage Market is diversifying beyond capital cities through such investments.

- For instance, KIO Networks’ BOG1 facility in Bogotá encompasses roughly 5,000 m² (about 53,820 sq ft) of built space with two data halls and 6 MW of power capacity to support mission‑critical colocation and connectivity services.

Competitive Insights:

- Cirion Technologies

- ETB Data Centers

- IFX Networks

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- Cisco Systems, Inc.

- Lenovo Group

- IBM Corporation

- NetApp

- Huawei Technologies Co., Ltd.

The Colombia Data Center Storage Market features a competitive mix of global hardware providers, regional service operators, and cloud infrastructure players. Cirion Technologies, IFX Networks, and ETB dominate in local infrastructure and colocation services, offering direct storage hosting for enterprises. Global vendors such as Dell, HPE, and Cisco provide high-performance hardware, all-flash arrays, and SDS platforms. IBM and NetApp focus on hybrid storage and enterprise backup solutions, while Huawei and Lenovo push AI-integrated infrastructure. Partnerships between local operators and global OEMs shape procurement decisions and service offerings. It supports segment-specific deployments across BFSI, telecom, and healthcare sectors. Vendors are differentiating through energy-efficient systems, cyber-resilient architecture, and service scalability. The Colombia Data Center Storage Market remains fragmented, but large players continue expanding footprint via regional alliances and managed storage services.

Recent Developments:

- In October 2025, Vertivannounced a distribution agreement with DACAS Peru to enhance its channel reach across Latin America, including Colombia. The collaboration focuses on supplying critical infrastructure components, including power and cooling systems that support storage and data center reliability for high-density AI and enterprise workloads in the region.

- In October 2025, GTD partnered with Peru’s Grupo Romero, through its InfraCorp arm, to jointly develop its data center business across Chile, Peru, and Colombia. Infracorp acquired a 49% stake in Gtdata Holdco, GTD’s data center subsidiary, for US$118 million, enabling the operation of 11 interconnected, Tier III-certified data centers across the three countries.