Executive summary:

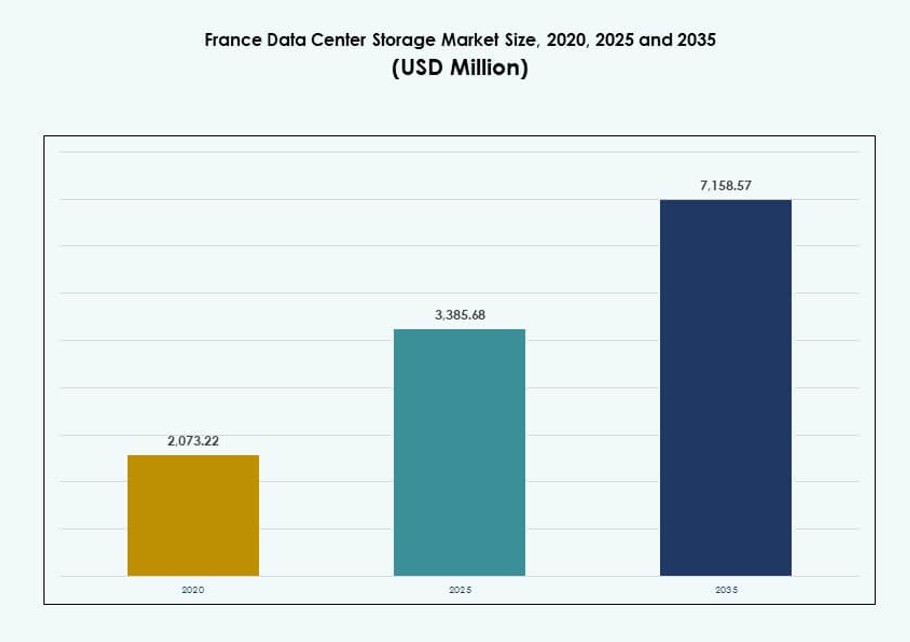

The France Data Center Storage Market size was valued at USD 2,073.22 million in 2020 to USD 3,385.68 million in 2025 and is anticipated to reach USD 7,158.57 million by 2035, at a CAGR of 7.70% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| France Data Center Storage Market Size 2025 |

USD 3,385.68 Million |

| France Data Center Storage Market, CAGR |

7.70% |

| France Data Center Storage Market Size 2035 |

USD 7,158.57 Million |

Rising cloud adoption, virtualization, and AI integration are reshaping storage demands across sectors. Enterprises seek scalable, high-speed, and secure infrastructure to manage growing data volumes. The shift toward hybrid and multi-cloud environments drives investment in flash arrays, software-defined storage, and object-based systems. These technologies enable better performance, lower latency, and improved operational control. Businesses and investors view the market as a foundation for digital transformation, resilience, and competitive edge.

Île-de-France leads the market due to high enterprise density, network infrastructure, and ongoing hyperscale development. Paris and its suburbs host most major data center deployments, attracting both public and private sector demand. Regions like Auvergne-Rhône-Alpes and PACA are emerging, supported by industrial growth, fiber upgrades, and smart city initiatives. These areas show increasing interest in edge deployments and localized data storage models.

Market Dynamics:

Market Drivers

Rising Digitalization Across Industries and the Push for Advanced Storage Modernization

France is experiencing rapid digital transformation across multiple sectors such as healthcare, government, and telecom. Enterprises seek scalable and secure storage solutions to handle growing data loads. The move toward digital services, remote work, and real-time analytics has increased demand for low-latency infrastructure. The France Data Center Storage Market is benefiting from this shift, with public and private institutions expanding capacity. Advanced storage systems like SAN and NAS offer efficient data access and centralized management. Vendors invest in modular systems and flash storage to meet workload-specific needs. Data availability and recovery capabilities have become strategic imperatives. Businesses prioritize systems that enable seamless integration across hybrid environments. Investors see strong returns in this segment due to consistent demand.

- For instance, OVHcloud operates its flagship Gravelines campus in northern France, one of Europe’s largest data center hubs. As of 2026, it supports high-performance object storage and enterprise workloads using NVMe flash and S3-compatible architectures.

Shift Toward Flash-Based Storage for Performance-Critical Enterprise Applications

Organizations are replacing legacy hard disk systems with high-performance SSD-based architecture. The rise in virtualization, AI, and analytics workloads drives this transition. SSDs deliver lower latency and higher throughput, enabling faster access to mission-critical data. This trend fuels growth in all-flash arrays and hybrid storage. The France Data Center Storage Market reflects this evolution, with hyperscalers and enterprises increasing SSD adoption. Strong performance gains and energy efficiency make SSDs attractive despite higher upfront costs. Government-supported digital innovation also encourages this shift. Data center operators focus on reducing energy use while enhancing IOPS. Flash storage aligns with both performance and sustainability goals.

Enterprise Cloud Adoption Fuels Demand for Scalable and Flexible Storage Solutions

Cloud storage is gaining traction across public and hybrid models, driven by demand for flexible resource scaling. Enterprises prefer platforms that support disaster recovery, remote access, and multitenancy. The France Data Center Storage Market benefits from growing reliance on IaaS and SaaS models. Scalable storage underpins migration to virtualized infrastructure. Hybrid deployments increase due to security concerns around fully public models. Data centers integrate software-defined storage for better control and adaptability. Cloud storage reduces capital expenditure and enhances data mobility. France’s favorable regulatory framework supports cloud-centric data practices. Businesses optimize operations by shifting from capex to opex models.

AI, IoT, and 5G Infrastructure Rollouts Necessitate New Storage Architectures

The deployment of 5G networks and edge computing amplifies the demand for decentralized, high-speed storage. AI and IoT workloads generate vast data volumes that require real-time processing and retrieval. Traditional systems are ill-equipped to manage such loads at scale. The France Data Center Storage Market is adapting through edge storage integration and distributed data processing. Use cases in automotive, smart cities, and industrial automation accelerate this trend. Edge-ready flash systems and modular storage enable seamless data aggregation. Companies deploy AI-powered storage for intelligent tiering and load balancing. These shifts make next-gen storage essential for digital infrastructure growth. Storage systems now function as enablers of innovation and agility.

- For instance, Atos deployed HPE GreenLake solutions to support its BullSequana high‑performance computing environments in France, enabling flexible, on‑premises storage consumption models. This integration enhances scalable storage and analytics capabilities for AI and large‑data workloads.

Market Trends

Adoption of Software-Defined Storage (SDS) to Improve Control, Cost Efficiency, and Scalability

SDS decouples storage software from hardware, enabling centralized control and cost optimization. Enterprises seek vendor-agnostic platforms that scale on-demand. SDS enhances automation, performance monitoring, and backup management. The France Data Center Storage Market sees rising SDS uptake for agility and multi-cloud compatibility. IT teams gain better visibility across workloads with policy-driven orchestration. SDS solutions are ideal for distributed environments and private cloud deployment. Open-source platforms also drive cost efficiencies in government and SMB segments. The trend supports digital sovereignty through localized control. France’s IT modernization aligns with this architectural shift.

Increased Use of AI-Based Storage Management for Predictive Insights and Workload Optimization

Artificial intelligence is reshaping storage management by enabling predictive analytics and fault detection. AI-driven tools forecast data traffic, identify anomalies, and automate capacity planning. This increases uptime and efficiency across workloads. The France Data Center Storage Market benefits from growing interest in autonomous IT infrastructure. AI supports intelligent tiering, aligning workloads with optimal storage types. It reduces human intervention and enhances operational reliability. Edge AI in storage systems supports low-latency computing for real-time applications. Telecom and retail sectors see strong use cases. AI integration into storage control layers is becoming standard.

Energy-Efficient Storage Infrastructure Gaining Ground for Sustainable Data Center Operations

Sustainability remains a top priority for hyperscalers and colocation providers. France enforces carbon neutrality goals, which impact data center design. Energy-efficient storage systems reduce power consumption and improve PUE metrics. The France Data Center Storage Market reflects this by shifting toward low-power SSDs and intelligent cooling. Vendors introduce rack-level optimization for better airflow and thermal balance. Storage equipment now factors into ESG reporting and compliance standards. Investors prefer assets that align with green data center strategies. Liquid cooling and AI-enhanced monitoring also support sustainability targets. Efficient storage design supports long-term operational savings.

Expansion of Edge Storage Nodes to Support Real-Time Analytics and Decentralized Processing

Edge storage adoption grows to support real-time use cases in transportation, utilities, and surveillance. Centralized architectures face latency and bandwidth limits, especially with rising data from IoT. Decentralized storage nodes enable faster data capture and analysis. The France Data Center Storage Market is evolving with telcos and enterprises deploying localized storage clusters. These nodes process data closer to end-users, reducing backhaul traffic. Edge setups use ruggedized and compact systems tailored for harsh environments. Integration with 5G and MEC platforms drives further deployment. Industries leverage this model for responsive, autonomous operations. Edge storage supports rapid data turnaround for time-sensitive applications.

Market Challenges

High Capital Expenditure and Legacy System Dependency Restricting Adoption of Modern Storage

Transitioning from legacy infrastructure to modern storage demands significant upfront investment. Many enterprises in France still operate hybrid environments with outdated components. Compatibility issues, cost of migration, and retraining needs slow down adoption. The France Data Center Storage Market faces budget constraints in mid-sized enterprises. These firms often defer upgrades due to perceived risk and ROI uncertainty. Legacy systems limit scalability and security, yet remain critical in operations. Storage transformation requires cross-functional coordination and vendor support. Government incentives only partly offset infrastructure costs. Hesitation persists in industries with regulated IT environments.

Complex Regulatory Landscape and Data Sovereignty Compliance Creating Operational Barriers

Data privacy and residency regulations in France require local data storage and tight access controls. Operators must comply with GDPR, national cybersecurity laws, and sector-specific mandates. This increases cost and complexity in storage architecture planning. The France Data Center Storage Market sees slower rollout of cloud-based and cross-border solutions. Enterprises must ensure encrypted storage, audit trails, and multi-tenant isolation. Hybrid deployments add further complexity in compliance monitoring. Fines and enforcement risks deter flexible storage use. Regulatory audits demand granular visibility into storage activities. These requirements strain resources and limit adoption flexibility.

Market Opportunities

Surge in AI and Analytics Workloads Creating Demand for High-Speed and Intelligent Storage

AI adoption across healthcare, finance, and manufacturing creates new demand for fast, intelligent storage. Real-time inference and model training require low-latency, scalable storage platforms. The France Data Center Storage Market can meet this need with NVMe and AI-driven storage systems. Vendors have opportunities to offer integrated analytics and storage bundles. Investments in GPU infrastructure also trigger growth in supporting storage layers. Enterprises seek solutions with tiered caching and intelligent data placement. High-throughput storage enables faster decisions and innovation cycles.

Growth of Regional Edge Infrastructure Supporting Decentralized Workloads and Compliance Needs

Edge computing is expanding across France’s regional cities and industrial zones. Storage providers can target localized deployments with tailored hardware and software. The France Data Center Storage Market benefits from edge-ready SSDs, ruggedized enclosures, and secure management software. Decentralized storage aligns with national data residency rules and real-time application needs. Edge growth opens opportunities in logistics, retail, and energy sectors. Partnerships with telecom operators and municipal IT networks can drive new contracts.

Market Segmentation

By Storage Type

The France Data Center Storage Market is segmented into traditional storage, all-flash storage, hybrid storage, and others. All-flash storage dominates due to its superior performance, low latency, and space efficiency. Hybrid storage also sees growth by combining flash speed with HDD affordability. Traditional systems remain in use in cost-sensitive workloads. Demand continues shifting toward flash as AI and real-time workloads expand.

By Storage Deployment

Storage deployment includes SAN, NAS, DAS, and others. SAN systems lead the market due to their reliability in handling large-scale enterprise data. NAS systems gain traction among SMBs for ease of use and file-level access. DAS supports high-speed local access in performance-intensive setups. Enterprises increasingly prefer SAN with built-in redundancy and centralization.

By Component

By component, the market is segmented into hardware and software. Hardware dominates with significant demand for SSDs, HDDs, enclosures, and controllers. Software gains traction through SDS platforms and management tools that enhance scalability and automation. Storage software plays a vital role in cost control, orchestration, and visibility.

By Medium

Storage media include HDD, SSD, and tape storage. SSD leads in value share due to speed and reliability in enterprise workloads. HDD remains relevant in archival and low-cost bulk storage. Tape usage declines but persists in long-term backup scenarios due to durability and cost-effectiveness.

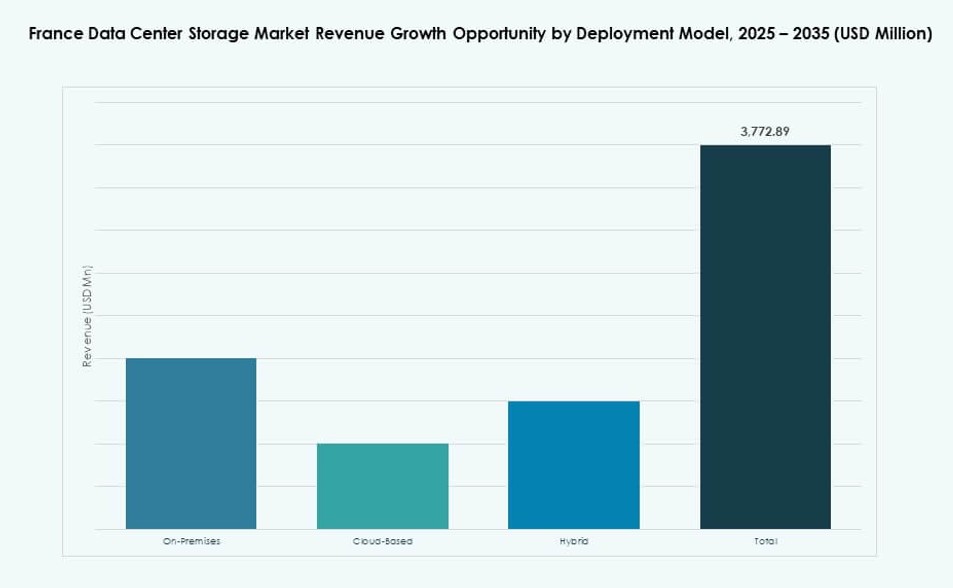

By Deployment Model

Deployment models include on-premises, cloud-based, and hybrid. Hybrid models dominate as organizations seek a balance between control and flexibility. On-premises setups are preferred in regulated sectors, while cloud gains popularity in startups and agile enterprises. Hybrid adoption rises with the use of edge storage and multi-cloud.

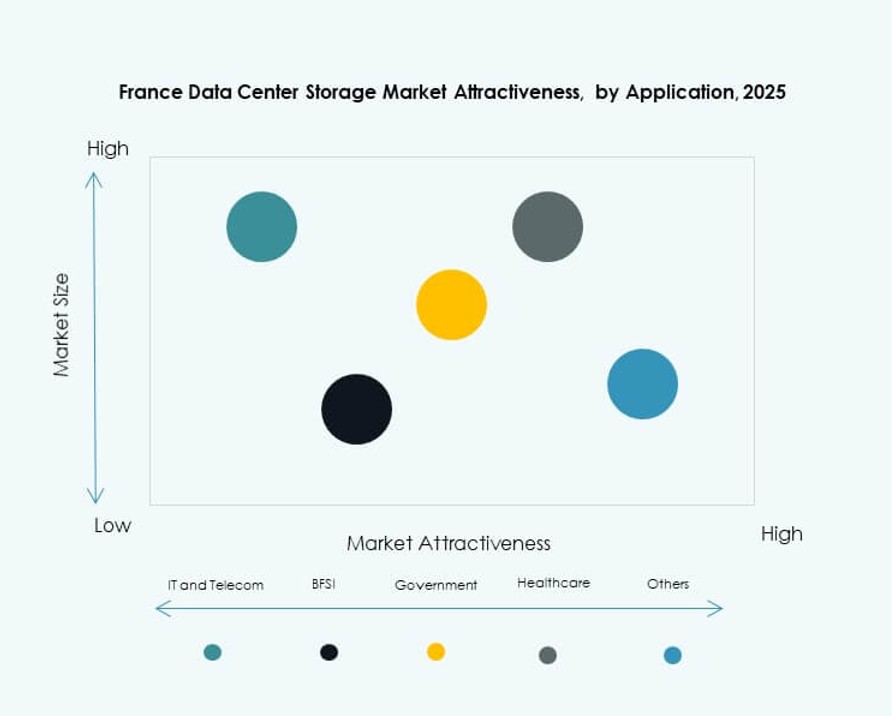

By Application

Key applications are IT and telecommunications, BFSI, government, healthcare, and others. IT and telecom lead due to massive data generation, 5G rollout, and high service demands. BFSI follows, driven by compliance, real-time processing, and high storage security. Government and healthcare see steady growth through digital transformation and e-health initiatives.

Regional Insights

Paris and Île-de-France Lead the National Market with Over 45% Share Due to Dense Enterprise Base

Paris and its surrounding Île-de-France region dominate the France Data Center Storage Market with a market share exceeding 45%. This region hosts the majority of hyperscalers, financial institutions, and enterprise headquarters. Dense connectivity, strong IT infrastructure, and proximity to government bodies make it the primary data center hub. Investment flows into storage upgrades and capacity expansion in this zone. Data localization regulations also drive expansion in local facilities. This region anchors most cloud, AI, and big data operations.

- For instance, Equinix operates the PA10 IBX data center in Saint‑Denis, Île‑de‑France, as part of its Paris campus, supporting enterprise and cloud storage workloads. The facility strengthens Equinix’s local colocation footprint and enables low‑latency access for hyperscale and digital service providers in the region.

Occitanie, Auvergne-Rhône-Alpes, and Provence-Alpes-Côte d’Azur Emerging with Strong Investment Activity

Southern and central regions like Occitanie, Auvergne-Rhône-Alpes, and PACA are emerging as key growth zones. These areas contribute nearly 30% of the market combined. Industrial development, university R&D partnerships, and improved fiber connectivity encourage data center expansion. Edge storage deployments are rising here to support decentralized IT needs. Regional governments back digital infrastructure projects to attract businesses. These areas show strong potential for green data center models and low-latency services.

- For instance, Data4 operates the DC23 facility at its Paris-Saclay campus in Île-de-France, offering around 30 MW of power capacity. The site supports scalable colocation and storage infrastructure for enterprise and cloud workloads.

Hauts-de-France, Grand Est, and Brittany Contribute 20–25% with Emphasis on Edge and Compliance-Driven Storage

Northern and western regions such as Hauts-de-France, Grand Est, and Brittany account for 20–25% of the France Data Center Storage Market. These subregions offer logistical advantages for edge deployments and serve growing industries like logistics, healthcare, and smart agriculture. Proximity to Benelux and Germany enhances cross-border digital connectivity. Demand for compliant, low-energy storage solutions is rising. Infrastructure upgrades and smart city initiatives further support market expansion in these zones.

Competitive Insights:

- OVHcloud

- Atos

- Orange Business Services

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- IBM Corporation

- NetApp

- Seagate Technology

- Huawei Technologies

- Cisco Systems, Inc.

The France Data Center Storage Market is highly competitive, with a mix of global technology providers and domestic players driving innovation and capacity expansion. Leading vendors like Dell Technologies, IBM, and HPE dominate due to extensive storage portfolios and strong local presence. French firms such as OVHcloud and Atos maintain strategic relevance through localized offerings and edge storage initiatives. Players invest in flash storage, SDS, and hybrid models to meet enterprise demand for scalable and energy-efficient systems. Cloud providers and telcos add competitive pressure with bundled infrastructure services. It fosters vendor partnerships, acquisitions, and technology upgrades to maintain market position. The competitive landscape rewards those offering low-latency, secure, and high-performance storage tailored to AI and analytics workloads.

Recent Developments:

- In July 10, 2025, Vesper Infrastructure Partners signed a binding agreement to acquire 100% of Thésée DataCenter from owners including Caisse des Dépôts et Consignations and Groupe IDEC Invest. Thésée operates a facility in Île-de-France with 4.6MW current capacity and 33MW future potential.

- In June 2025, Atos received a confirmatory acquisition offer from the French government for its Advanced Computing division, valued at €410 million. The offer targets high-performance computing and AI segments, reinforcing France’s capabilities in advanced data processing and storage infrastructure.

- In January 2024, DATA4 partnered with OVHcloud to implement liquid cooling solutions at its Marcoussis data center near Paris. The initiative enhances storage infrastructure efficiency to meet rising AI and colocation demands, aligning with sustainable data center strategies.

- In February 2024, NTT DATA announced plans to construct a new data center in Paris with over 84MW IT capacity. The development aims to support growing demand for secure storage and colocation services, positioning NTT DATA among the key players in France’s expanding storage market.