Executive summary:

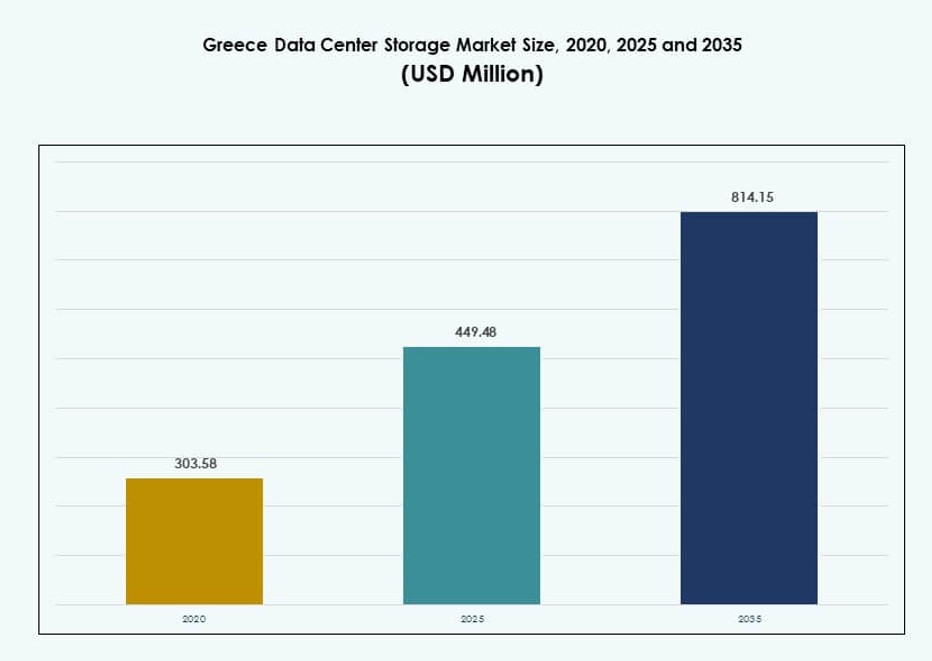

The Greece Data Center Storage Market size was valued at USD 303.58 million in 2020 to USD 449.48 million in 2025 and is anticipated to reach USD 814.15 million by 2035, at a CAGR of 6.07% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Greece Data Center Storage Market Size 2025 |

USD 449.48 Million |

| Greece Data Center Storage Market, CAGR |

6.07% |

| Greece Data Center Storage Market Size 2035 |

USD 814.15 Million |

The market is driven by increasing cloud adoption, digital public services, and enterprise IT modernization. Businesses across telecom, BFSI, and government sectors are adopting scalable, low-latency storage solutions to support AI, IoT, and analytics workloads. Hybrid cloud models and software-defined storage are becoming standard as demand for flexibility and compliance grows. These shifts create strong incentives for vendors and investors to enhance infrastructure across key verticals.

Attica leads the market with strong data center presence, supported by subsea cable landings and hyperscale investments. Athens acts as a digital gateway between Europe and nearby regions, enabling cross-border data exchange. Crete is emerging due to new facilities and enhanced interconnection options. Northern and Central Greece show steady progress, driven by regional expansion of smart services and enterprise IT.

Market Dynamics:

Market Drivers

Rising Digital Transformation Initiatives from Public and Private Sectors

Greece is undergoing rapid digital transformation supported by public funding and enterprise-led modernization. Government programs like “Digital Transformation Bible” and EU-backed RRF initiatives are boosting cloud, edge, and AI readiness. These drive adoption of advanced storage infrastructure in line with smart services. Enterprises seek scalable storage to manage data-heavy workloads including analytics, automation, and video. Demand is shifting toward hyperconverged and software-defined storage. This aligns with Greece’s goal of building secure, sovereign data ecosystems. The Greece Data Center Storage Market is responding with hybrid deployments and local hyperscale investments. Cloud providers and colocation firms are tapping these trends to expand storage capacity.

- For instance, the existing Athens campus (ATH1 and ATH2) supports over 1,000 racks as part of 22MW total capacity expansion plans supporting cloud and edge workloads.

Growing Data Localization Demand and Regulatory Compliance Requirements

Data sovereignty laws and regulatory frameworks now demand localized data processing and secure storage practices. Enterprises across BFSI, healthcare, and government verticals are investing in certified storage systems with backup and disaster recovery. GDPR compliance and sector-specific mandates drive the need for structured storage solutions. Cloud service providers offer region-specific zones to comply with these regulations. Investments in local colocation facilities with secure SAN and NAS deployments are growing. This fuels storage hardware and software upgrades. Hybrid cloud models enable flexibility while ensuring control. The Greece Data Center Storage Market benefits from storage innovation tailored to legal frameworks.

- For instance, Eurobank uses NetApp technology to manage critical data across its BFSI operations in Greece. NetApp’s ONTAP software provides high availability and supports GDPR compliance for secure and resilient storage environments.

Subsea Cable Projects and Strategic Geographic Position Boosting Data Exchange

Greece’s location at the intersection of Europe, Asia, and Africa offers strong digital interconnection opportunities. New subsea cable landings such as BlueMed and Quantum Cable enhance international connectivity. These drive demand for edge and backbone storage in Athens and other coastal hubs. Telecom operators upgrade storage backbones to support high-throughput and low-latency routing. Global platforms see Greece as a new transit and storage hub for regional cloud services. It opens opportunities for data-rich industries like gaming, content delivery, and AI. The Greece Data Center Storage Market is expanding to support this rising intercontinental data traffic.

Enterprise Cloud Migration and Storage Modernization Across Sectors

Greek enterprises are shifting from legacy storage models to cloud-integrated systems. Digital-first strategies across sectors like retail, telecom, and logistics rely on rapid storage access. Organizations deploy all-flash arrays and object-based storage for speed and scale. Virtualization, DevOps, and container-based applications reshape workload behavior. This triggers upgrades from on-prem SAN/NAS to cloud-native storage solutions. Managed services and infrastructure-as-a-service (IaaS) models are accelerating adoption. The Greece Data Center Storage Market reflects this with rising traction for flexible, consumption-based storage delivery models. Businesses prioritize performance, scalability, and compliance while maintaining cost efficiency.

Market Trends

Shift Toward All-Flash and NVMe Storage for High-Performance Workloads

High-speed storage is becoming essential as enterprises run latency-sensitive workloads like AI, ML, and real-time analytics. NVMe and all-flash arrays are replacing traditional hard drives in both core and edge deployments. Vendors promote energy-efficient SSDs to reduce power use and maximize throughput. This trend is notable across fintech, telecom, and public cloud players. Colocation providers design high-density rack layouts to host flash-based systems. Tiered storage models gain attention to balance performance and cost. The Greece Data Center Storage Market shows strong movement toward flash-based storage to support demanding applications.

Integration of AI and Machine Learning for Predictive Storage Management

AI-powered storage management platforms improve data tiering, failure prediction, and workload balancing. Vendors integrate intelligent tools into storage arrays and controllers to automate operations. Predictive analytics optimize capacity usage and reduce unplanned outages. These features appeal to data-heavy industries like media, public sector, and logistics. IT teams use ML models to monitor utilization trends across hybrid environments. This improves resource efficiency and aligns storage provisioning with business demand. The Greece Data Center Storage Market embraces smart storage software that enhances reliability and operational agility.

Emergence of Edge Data Centers Driving Decentralized Storage Infrastructure

Edge computing adoption expands across cities and islands in Greece, spurred by IoT and 5G rollout. Small-scale edge data centers require localized, compact storage systems. Edge colocation models enable real-time analytics for applications like smart grids, maritime tech, and mobility platforms. Modular storage deployments become critical in remote and semi-urban zones. Telecom operators and ISPs build micro-data centers with secure DAS and NAS systems. This decentralization reduces latency and improves content delivery. The Greece Data Center Storage Market supports this shift with edge-ready storage hardware and software offerings.

Adoption of Object-Based Storage for Cloud-Native and Archival Applications

Object storage is gaining popularity for its scalability and compatibility with cloud-native tools. Enterprises rely on it to store unstructured data like media files, logs, and backups. Public sector bodies use object-based systems for compliance-driven archiving. It supports S3 API compatibility and ensures seamless cloud integration. Tiered storage models place object storage at the cold layer for long-term retention. Service providers offer managed object storage solutions bundled with cloud platforms. The Greece Data Center Storage Market adopts object models to manage explosive data growth while maintaining cost control.

Market Challenges

High Energy Costs and Limited Green Power Access for Storage Operations

Energy remains one of the most critical barriers to efficient data center storage expansion in Greece. Power tariffs are high and renewable penetration is uneven, impacting operational costs. Cooling needs for high-density storage arrays increase power draw. Small and mid-tier data centers struggle to adopt energy-efficient infrastructure. Regulatory hurdles and slow permitting limit the pace of solar or wind integration. Most storage providers rely on grid energy without consistent green power purchase agreements. The Greece Data Center Storage Market feels pressure to align with EU green goals but faces infrastructural constraints in doing so.

Limited Skilled Workforce and Delayed Infrastructure Modernization in Secondary Regions

There is a shortage of trained professionals for advanced storage systems across the Greek IT sector. System integration, security configuration, and multi-cloud storage management require upskilling. Public universities lag in offering updated training on cloud-native and AI-enabled storage tools. Data centers in secondary cities lack infrastructure for high-speed connectivity and modern racks. These gaps hinder balanced regional development of storage services. Enterprises in non-metro regions face delays in infrastructure deployment and access to advanced storage features. The Greece Data Center Storage Market encounters disparities in talent and infrastructure, slowing consistent nationwide growth.

Market Opportunities

Foreign Investment and Hyperscale Entry Offering Acceleration Potential

Greece is attracting foreign investment through digital infrastructure funds and EU-backed programs. New hyperscale entrants explore the country as a southern European base. Investment accelerates deployment of next-gen storage solutions including NVMe, cloud-native arrays, and software-defined platforms. The Greece Data Center Storage Market gains from capital inflow and strategic partnerships that build scalable, future-proof ecosystems.

5G and IoT Expansion Creating Demand for Real-Time and Mobile Storage Applications

The rollout of 5G and smart device networks drives need for low-latency, mobile-compatible storage. Use cases in shipping, transport, and public utilities call for rugged, scalable solutions. Vendors tailor edge deployments to serve connected ecosystems across urban and rural areas. The Greece Data Center Storage Market benefits from innovation that supports dynamic, distributed storage environments.

Market Segmentation

By Storage Type

Traditional storage holds a declining share, while all-flash and hybrid systems gain traction for performance and scalability. All-flash storage leads among large enterprises due to demand for low-latency data handling. Hybrid storage remains dominant in public sector deployments. The Greece Data Center Storage Market favors hybrid models for balancing cost and speed, supported by growing SSD integration.

By Storage Deployment

Network-attached storage (NAS) dominates due to flexibility and multi-user access. Storage Area Network (SAN) adoption is strong among telecoms and financial firms for high-speed performance. Direct-attached storage (DAS) continues in small-scale and edge setups. The Greece Data Center Storage Market benefits from modular deployments suited to mixed infrastructure environments and scale-out demands.

By Component

Hardware constitutes the larger share, driven by high investment in SSDs, enclosures, and networking gear. Software is growing steadily with demand for storage management, virtualization, and automation platforms. Vendors bundle software with hyperconverged systems for simplicity. The Greece Data Center Storage Market continues to shift toward integrated software-defined storage solutions.

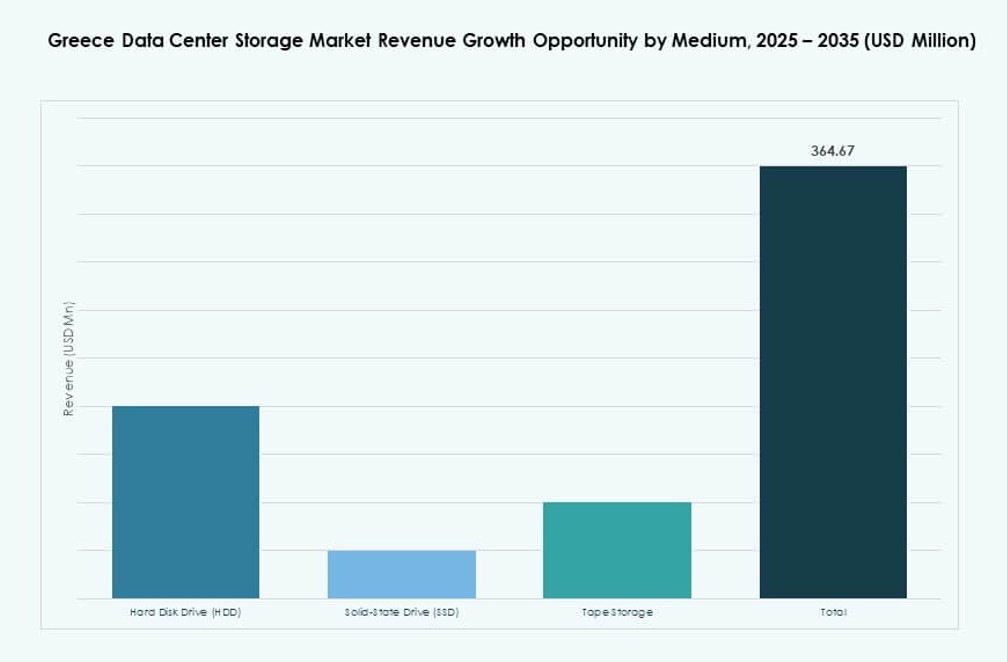

By Medium

Solid-state drives (SSDs) are overtaking hard disk drives (HDDs) in critical workloads due to performance and energy savings. HDDs still dominate archival and cold storage layers. Tape storage sees limited use, mostly in legacy systems. The Greece Data Center Storage Market supports mixed media adoption based on workload, cost, and durability preferences.

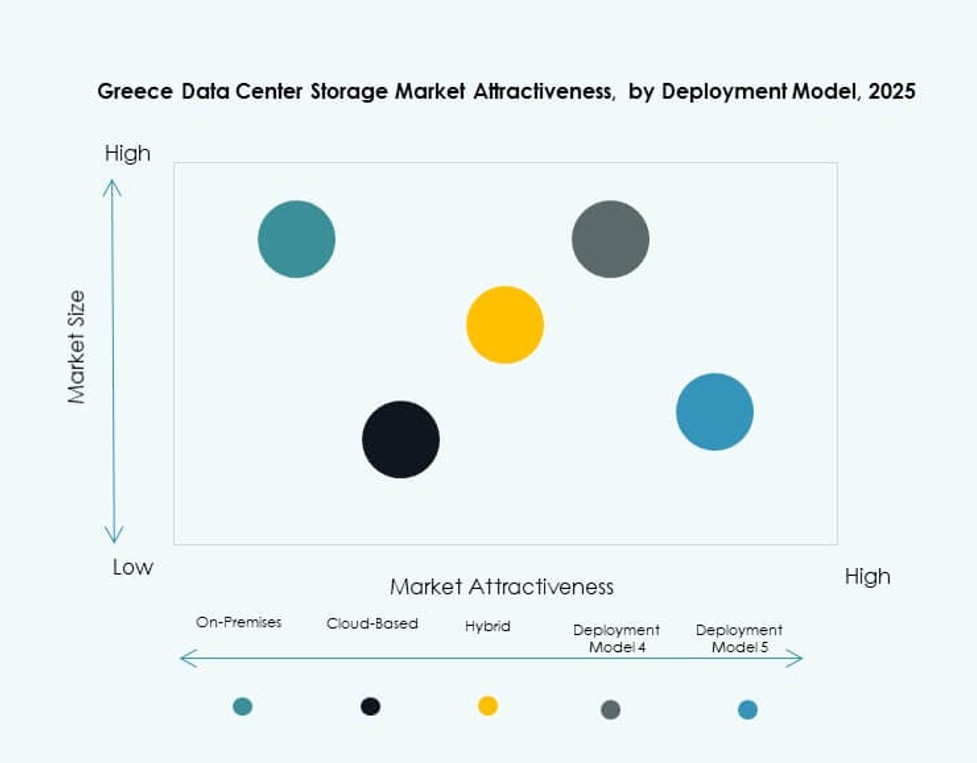

By Deployment Model

Cloud-based storage leads, especially among SMEs and digital-native firms. On-premises remains common in healthcare and public administration. Hybrid deployment models are accelerating, driven by the need for security, control, and scalability. The Greece Data Center Storage Market shows increasing hybrid adoption, aligning with evolving enterprise workload distribution patterns.

By Application

IT and telecom dominate usage, followed by BFSI and public sector. Healthcare storage is growing with medical imaging and patient record digitization. Other segments like education and logistics show moderate growth. The Greece Data Center Storage Market supports data-driven transformation across sectors with tailored storage solutions.

Regional Insights

Attica region dominates the Greece Data Center Storage Market with over 60% share. Athens remains the central hub due to dense network infrastructure and subsea cable access. It hosts major data centers, telecom providers, and hyperscale edge deployments. Its proximity to international routes strengthens its role in regional data exchange.

- For instance, Data4 has announced plans to develop a large-scale data center campus near Athens, Greece, as part of its Southern Europe expansion strategy. The project aims to support hyperscale and AI workloads with a focus on energy efficiency and digital infrastructure resilience.

Central and Northern Greece together account for around 25% of the market. Thessaloniki leads among emerging urban zones with investments in smart city and 5G rollout projects. The region is attracting tech startups and logistics firms. Infrastructure upgrades and incentives support new data centers with hybrid cloud capabilities.

Southern Greece and island regions hold about 15% of the market, primarily driven by tourism, local governance, and maritime sectors. These zones rely on modular edge data centers to support IoT and mobile applications. Connectivity improvements and renewable energy adoption will unlock further storage capacity in these geographies. The Greece Data Center Storage Market balances urban and regional expansion through edge-focused strategies.

- For instance, Vodafone Greece has outlined long‑term investments to expand 5G network coverage across the country, including island regions. This expansion supports broader connectivity needs for low‑latency services and digital applications.

Competitive Insights:

- Intracom Telecom

- Space Hellas

- OTE Group

- Uni Systems

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- IBM Corporation

- NetApp

- Huawei Technologies

- Cisco Systems

The Greece Data Center Storage Market features a balanced mix of local integrators and global storage vendors. Intracom Telecom, Space Hellas, and OTE Group lead domestic infrastructure deployment, especially in telecom and public sector segments. Global players like Dell, HPE, and IBM hold strong positions through hardware and software storage solutions tailored for hybrid and cloud environments. Cisco and Huawei enhance competitive intensity by offering scalable network-attached and SAN systems. NetApp and Uni Systems focus on enterprise and BFSI clients through data management and flash storage services. It fosters innovation in NVMe, SDS, and disaggregated systems as demand for modernization grows. Strategic alliances, acquisitions, and integrated service models shape vendor strategies across regions and verticals.

Recent Developments:

- In April 2025, Space Hellas and Digital Realty launched a new Point of Presence (PoP) at the HER1 data center in Heraklion, Crete. The collaboration enhances interconnection and access to secure data center storage services across southeastern Greece, improving regional enterprise connectivity.

- In April 2025, Digital Realty, through its subsidiary Lamda Hellix, inaugurated its first data center in Crete, Greece. The facility delivers carrier-neutral storage and cloud services, supporting high-capacity data workloads. This expansion reinforces Greece’s strategic role in regional data storage infrastructure amid growing AI and cloud demand.

- In December 2024, EDGNEX Data Centers by DAMAC and PPC Group revealed a joint venture to form Data In Scale SA, launching a large-scale data center in Spata, East Attica. The first phase involves €150 million in investment for a 12.5MW facility, with expansion plans up to 25MW. This project targets scalable data storage and cloud computing needs, strengthening Greece’s role as a digital hub linking Europe, Asia, and Africa.

- In November 2024, Intracom Telecom announced the development of a new state-of-the-art manufacturing facility in Western Macedonia, Greece. This strategic move is aimed at boosting its production capabilities, which may support the country’s growing demand for localized data center infrastructure and storage equipment.