Executive summary:

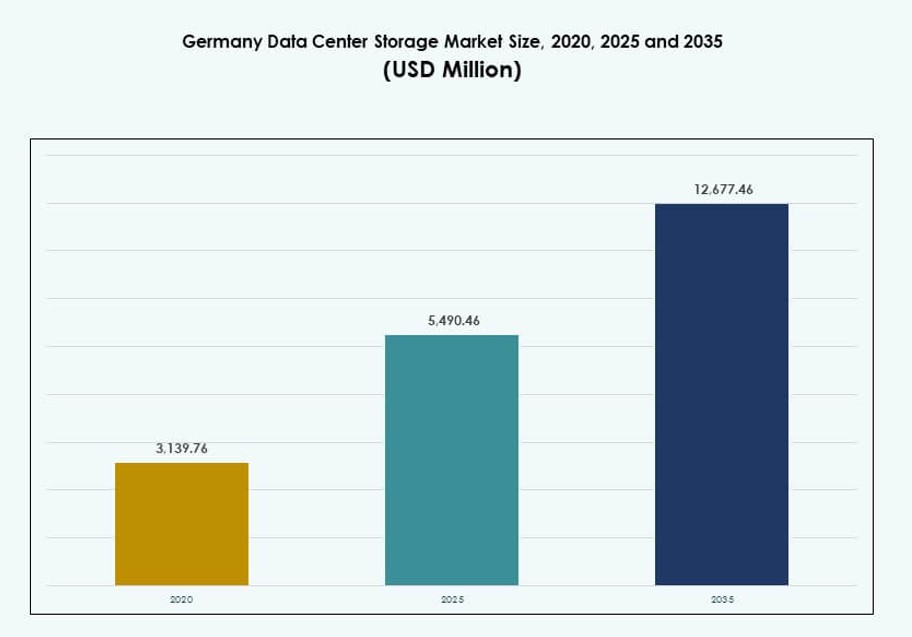

The Germany Data Center Storage Market size was valued at USD 3,139.76 million in 2020 to USD 5,490.46 million in 2025 and is anticipated to reach USD 12,677.46 million by 2035, at a CAGR of 8.64% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Germany Data Center Storage Market Size 2025 |

USD 5,490.46 Million |

| Germany Data Center Storage Market, CAGR |

8.64% |

| Germany Data Center Storage Market Size 2035 |

USD 12,677.46 Million |

Rapid digital transformation across industries is driving strong demand for scalable and secure storage solutions. Enterprises are shifting to cloud-based and hybrid models, adopting flash arrays, NVMe systems, and SDS platforms. Rising AI, IoT, and big data workloads require low-latency and high-throughput performance. Compliance with GDPR and sovereign cloud mandates adds urgency for localized storage infrastructure. The market’s role is central to Germany’s digital economy, offering long-term value for investors and infrastructure players.

Frankfurt leads due to its hyperscale footprint, dense interconnection, and strategic positioning as a European digital hub. Berlin and Munich are emerging as strong secondary centers with rising demand from tech startups and industrial players. Other cities like Hamburg and Düsseldorf support regional hosting, edge deployment, and disaster recovery needs. This distributed growth reflects Germany’s push for nationwide digital coverage and localized data processing.

Market Dynamics:

Market Drivers

Surging Enterprise Data Volumes Necessitate Scalable and High-Performance Storage Solutions

Germany is witnessing exponential growth in enterprise data due to digitization across industries. Enterprises are replacing legacy storage systems with scalable, low-latency infrastructure to manage unstructured and structured data. The adoption of customer analytics, AI, and IoT accelerates this shift. High-capacity all-flash arrays and NVMe systems are gaining traction for real-time access. Storage modernization ensures business continuity, disaster recovery, and performance optimization. It supports Germany’s position as a digital leader in Europe. The Germany Data Center Storage Market benefits from strong cloud-native transformation and application modernization. Enterprises are prioritizing storage efficiency to remain competitive.

Accelerating Cloud and Hybrid IT Infrastructure Driving Demand for Flexible Storage Architectures

Cloud adoption is reshaping storage demand across enterprises, service providers, and government. On-premises systems are increasingly integrated with cloud-native platforms to enable workload portability. Storage providers are launching hybrid and software-defined storage models tailored for complex IT environments. Dynamic scaling and automated tiering are essential for cost control and agility. AI-optimized storage frameworks are emerging to support real-time cloud workloads. The shift to microservices and containerized environments demands persistent and decentralized storage. The Germany Data Center Storage Market is witnessing demand for open, vendor-neutral platforms. This evolution makes storage a core pillar of digital business strategies.

Digital Sovereignty and Data Localization Regulations Fuel Investment in National Data Centers

The introduction of the EU General Data Protection Regulation (GDPR) has made localized data storage a top priority. Germany enforces strict data residency mandates for financial, healthcare, and government sectors. Enterprises seek in-country data centers with certified storage infrastructure. This regulatory framework increases demand for compliant, resilient, and auditable storage systems. Domestic and international providers are scaling up regional storage capacity to meet legal requirements. The Germany Data Center Storage Market gains strategic relevance for companies operating in highly regulated sectors. Sovereign cloud deployments also drive demand for storage encryption and backup compliance. Regulations elevate the need for secure storage design.

- For instance, Bechtle signed partnership agreements with Deutsche Telekom and Arvato Systems to expand its GDPR‑compliant multi‑cloud portfolio hosted in German data centers, strengthening secure local data infrastructure for regulated industries.

AI and HPC Workload Growth Promoting Demand for High-Density and Energy-Efficient Storage

The rise of AI, high-performance computing (HPC), and big data analytics creates intense storage performance demands. These workloads require ultra-low-latency access, high throughput, and petabyte-scale capacity. All-flash and NVMe-based architectures dominate deployments in AI-focused data centers. Edge AI deployments further stimulate localized high-speed storage requirements. Enterprises are optimizing rack density and power usage effectiveness (PUE) with advanced storage cooling integration. The Germany Data Center Storage Market gains importance in supporting AI data pipelines. It serves as a foundation for model training, inferencing, and autonomous systems. Advanced storage also enhances scientific research and industrial automation projects.

- For instance, SuperMUC‑NG at the Leibniz Supercomputing Centre (LRZ) uses a BeeGFS parallel filesystem with multi‑petabyte capacity and aggregated high throughput to support demanding HPC and AI research workloads, including projects for German research institutions.

Market Trends

Growth of Software-Defined Storage (SDS) Enabling Agility and Cost Efficiency Across Enterprises

SDS adoption is growing across Germany’s enterprise landscape to decouple storage software from hardware. Organizations deploy SDS to reduce vendor lock-in, optimize resource use, and enable centralized control. SDS simplifies management across hybrid and multi-cloud environments. It also enhances resilience through automated provisioning and policy-based tiering. Enterprises are deploying SDS for flexibility in data protection, backup, and archival tasks. Open-source SDS platforms are gaining acceptance for customization. The Germany Data Center Storage Market sees SDS as a tool for reducing CAPEX while enabling dynamic scaling. This trend aligns with cloud-native transformation goals.

AI-Based Predictive Storage Management Enhancing Performance and Preventive Maintenance

AI integration in storage solutions is reshaping system efficiency and uptime. Predictive analytics tools help detect anomalies and optimize storage resource allocation in real-time. Enterprises use AI to forecast workload demands and automate backup or replication. Intelligent tiering ensures cold and hot data are stored optimally. AI-enabled platforms offer storage recommendations based on usage trends. Vendors also embed AI in storage security to identify unusual access behavior. The Germany Data Center Storage Market is incorporating AI to streamline infrastructure operations. These solutions minimize downtime and improve TCO across enterprise deployments.

Edge Data Center Deployments Stimulating Localized Storage Expansion for Latency-Sensitive Workloads

Edge computing expansion across manufacturing, retail, and smart cities is fueling demand for distributed storage. Applications at the edge require high-speed local storage for real-time decision-making. German enterprises are deploying micro data centers with integrated flash or hybrid storage systems. These facilities handle tasks like computer vision, industrial IoT, and remote monitoring. Compact, rugged storage platforms are deployed in space-constrained environments. Edge storage also reduces backhaul traffic and data transfer costs. The Germany Data Center Storage Market supports edge growth by delivering high-performance localized systems. It addresses needs where latency tolerance is minimal.

Sustainability Trends Boosting Demand for Energy-Efficient Storage Technologies and Cooling Integration

Green IT strategies in Germany push data centers to adopt sustainable storage practices. Enterprises adopt SSDs over HDDs for lower power consumption and faster data access. Vendors are designing modular storage with lower carbon footprints and recyclable materials. Storage systems are increasingly integrated with smart cooling and thermal control systems. Government incentives and ESG goals drive demand for efficient designs. Liquid cooling compatibility and renewable energy integration are also rising in importance. The Germany Data Center Storage Market incorporates eco-friendly storage into long-term capacity planning. Sustainability compliance is becoming a key procurement criterion.

Market Challenges

Legacy Infrastructure and Budget Constraints Restricting Storage Modernization for Mid-Sized Enterprises

Despite rising digital needs, many German mid-sized enterprises struggle with aging on-premise storage systems. Upgrading to modern storage often involves high upfront costs and complex integration. Legacy systems lack scalability and efficiency for today’s data volumes and workloads. Security and compliance risks increase when outdated systems are used. Smaller firms may hesitate to shift to hybrid or cloud-based storage due to data sensitivity and skills gaps. Lack of skilled IT staff for SDS and virtualization further limits adoption. The Germany Data Center Storage Market faces resistance from conservative IT buyers. Market growth depends on vendor efforts to simplify deployment and reduce TCO.

Cybersecurity Concerns and Ransomware Threats Challenge Storage Strategy Across Critical Sectors

Germany’s industrial and public sectors are frequent targets of cyberattacks. Storage environments become vulnerable points for ransomware and data exfiltration. Enterprises demand immutable backups, zero-trust access controls, and encryption at rest. Managing security across hybrid cloud and on-premise platforms is complex. Real-time threat detection and response need integration into storage systems. Compliance with GDPR adds complexity in handling breach response and reporting. The Germany Data Center Storage Market must address growing demand for hardened and resilient storage. Regulatory fines and reputation loss raise the stakes for storage reliability.

Market Opportunities

Rising AI and HPC Investments Offering Scope for Tiered, Low-Latency, and High-Density Storage

Germany’s investments in AI infrastructure, including research labs and industrial automation, expand demand for performance-driven storage. HPC centers across academia and enterprise require high-speed storage solutions with rapid IOPS delivery. Growth in machine learning workloads encourages NVMe and GPU-integrated storage. Vendors have an opportunity to offer tiered systems for cold, warm, and hot data layers. The Germany Data Center Storage Market can capitalize on AI adoption with scalable and energy-efficient designs. Growth accelerates through national strategies like GAIA-X and European cloud initiatives.

Expanding Cloud and Colocation Ecosystem Creates Demand for Customizable and As-a-Service Storage Models

Cloud growth across Frankfurt, Berlin, and Munich boosts demand for elastic storage. Colocation providers are expanding white-label storage offerings with API-based access and metered usage. Enterprises prefer opex-based models to reduce financial risk. Vendors offering storage-as-a-service and pay-per-use plans are well-positioned. The Germany Data Center Storage Market gains traction by supporting workload portability and API integration. Modular storage racks, remote provisioning, and vendor-neutral interfaces will drive adoption.

Market Segmentation

By Storage Type

All-flash storage leads adoption in performance-critical deployments, replacing traditional spinning disk drives. Hybrid storage systems remain popular in cost-sensitive environments balancing speed and capacity. Traditional storage is declining but still used for legacy workloads. The Germany Data Center Storage Market is shifting toward flash-based architecture due to faster access times and lower power use. Vendors offering flexible configurations dominate.

By Storage Deployment

Storage Area Network (SAN) systems dominate large-scale enterprise deployments due to high availability and centralized control. Network-Attached Storage (NAS) is common in media and content-heavy applications. Direct-Attached Storage (DAS) is preferred for small-scale setups or edge sites. The Germany Data Center Storage Market sees SAN as the primary deployment type for mission-critical operations. Growth in NAS adoption is tied to file-sharing and distributed teams.

By Component

Hardware accounts for the largest market share due to the physical infrastructure demands of expanding data centers. Software is growing in importance with the rise of SDS and virtualization. The Germany Data Center Storage Market is seeing strong interest in software-led automation tools. Integration of storage management, backup, and orchestration platforms drives software uptake.

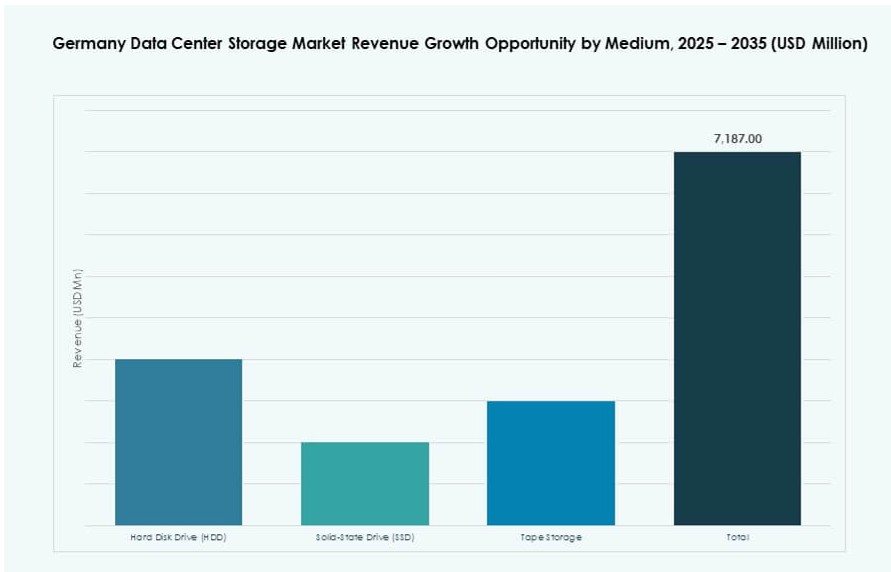

By Medium

Solid-State Drives (SSDs) dominate due to higher speed, reliability, and energy efficiency. Hard Disk Drives (HDDs) remain relevant for archival and large-volume storage needs. Tape storage is limited to long-term backup and cold storage cases. The Germany Data Center Storage Market prioritizes SSD adoption in active workloads. Enterprises shift from HDDs to SSDs to improve latency and performance.

By Deployment Model

Cloud-based storage is gaining momentum across digital-first enterprises. On-premise remains essential for regulated sectors and latency-sensitive applications. Hybrid models are growing due to their ability to combine control with scalability. The Germany Data Center Storage Market leans toward hybrid deployments to support flexible infrastructure goals. Enterprises look for seamless migration paths and vendor interoperability.

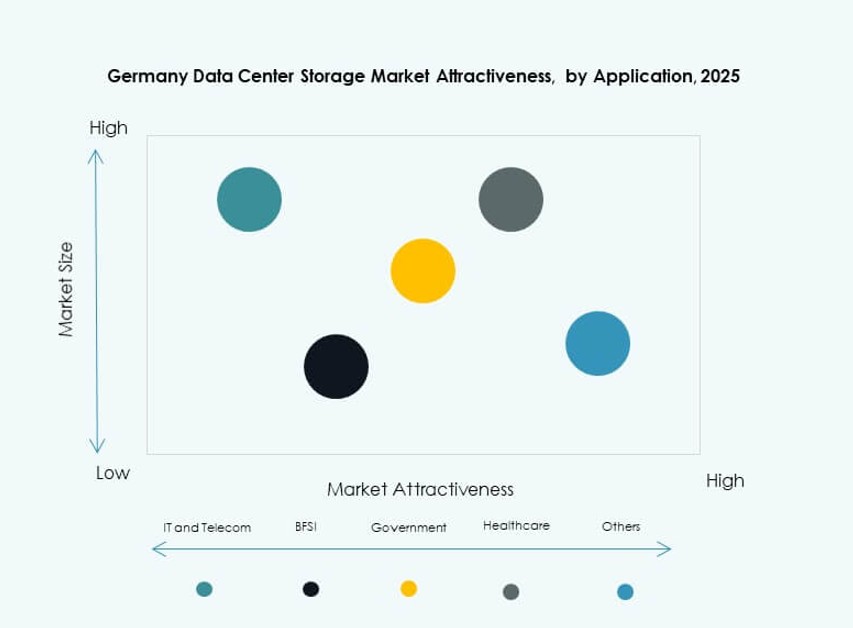

By Application

IT and telecommunications lead demand with constant storage upgrades for network operations and service delivery. BFSI requires secure and compliant storage for financial records and transactions. Government and healthcare sectors prioritize data residency, compliance, and availability. The Germany Data Center Storage Market supports all verticals, with BFSI and IT as the top adopters. Others include retail and manufacturing investing in digital infrastructure.

Regional Insights

Frankfurt Leads with Over 35% Share Due to Its Role as Europe’s Data Exchange Hub

Frankfurt is Germany’s primary data center cluster, hosting key cloud providers, IXPs, and hyperscale facilities. Its dense fiber connectivity and regulatory stability attract international and domestic enterprises. The city’s power availability and network resilience support high-density storage infrastructure. The Germany Data Center Storage Market sees Frankfurt as its anchor zone. Providers expand modular and AI-optimized storage capacity in this region to support growth.

- For instance, Digital Realty began construction on FRA20, delivering 16MW of AI-ready IT capacity across 8,100 square meters.

Berlin and Munich Emerging with 20% and 15% Market Share Respectively Due to Tech Ecosystems

Berlin’s tech startup ecosystem and government presence drive demand for scalable, cost-effective storage. Colocation and edge storage facilities support hybrid deployments across sectors like media, fintech, and AI. Munich hosts industrial and automotive giants investing in secure on-premise and cloud-integrated storage. The Germany Data Center Storage Market sees balanced growth across these zones. AI and HPC workloads further strengthen demand in Munich.

- For instance, Colt DCS expanded German capacity by 117MW total, including Berlin sites supporting 130kW per rack for AI workloads.

Other Regions Including Hamburg, Düsseldorf, and Stuttgart Share 30% Combined Due to Regional Hosting Needs

Secondary cities are expanding colocation and enterprise IT footprints for regional access and disaster recovery. Hamburg’s port logistics, Düsseldorf’s financial institutions, and Stuttgart’s manufacturing sector fuel localized storage needs. These cities host edge facilities that integrate storage with compute for latency-sensitive tasks. The Germany Data Center Storage Market spreads across regions for resilience and compliance. Tier II and Tier III cities support decentralization strategies.

Competitive Insights:

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- IBM Corporation

- NetApp

- Huawei Technologies

- Fujitsu Limited

- Lenovo Group

- Cisco Systems, Inc.

- Veeam Software

- Bechtle

The Germany Data Center Storage Market features a balanced mix of global technology vendors and local IT infrastructure providers. Dell Technologies, HPE, and IBM lead in enterprise-scale deployments with end-to-end storage portfolios. NetApp and Veeam gain ground in data protection and hybrid storage environments. Huawei and Fujitsu provide performance-centric systems aligned with European standards. Local firms like Bechtle support integration and services across Tier II cities. Competition is driven by flash storage innovation, software-defined platforms, and regulatory compliance support. Vendors compete on scalability, cost efficiency, sustainability, and service reliability. The market rewards providers that offer secure, modular, and high-performance solutions built for cloud-native and AI-driven workloads.

Recent Developments:

- In December 2025, Bechtle signed partnership agreements with Deutsche Telekom and Arvato Systems to expand its multi-cloud portfolio, incorporating GDPR-compliant infrastructure from German data centers to enhance digital sovereignty.

- In September 2025, Dell Technologies expanded its partnership with Nutanix introducing PowerStore integrated with Nutanix Cloud Platform for enhanced enterprise storage in data centers, generally available in spring 2026.

- In January 2025, Lenovo Group announced the acquisition of Infinidat to strengthen its high-end enterprise storage portfolio for modern data centers, emphasizing cyber-resilient and scalable solutions