Executive summary:

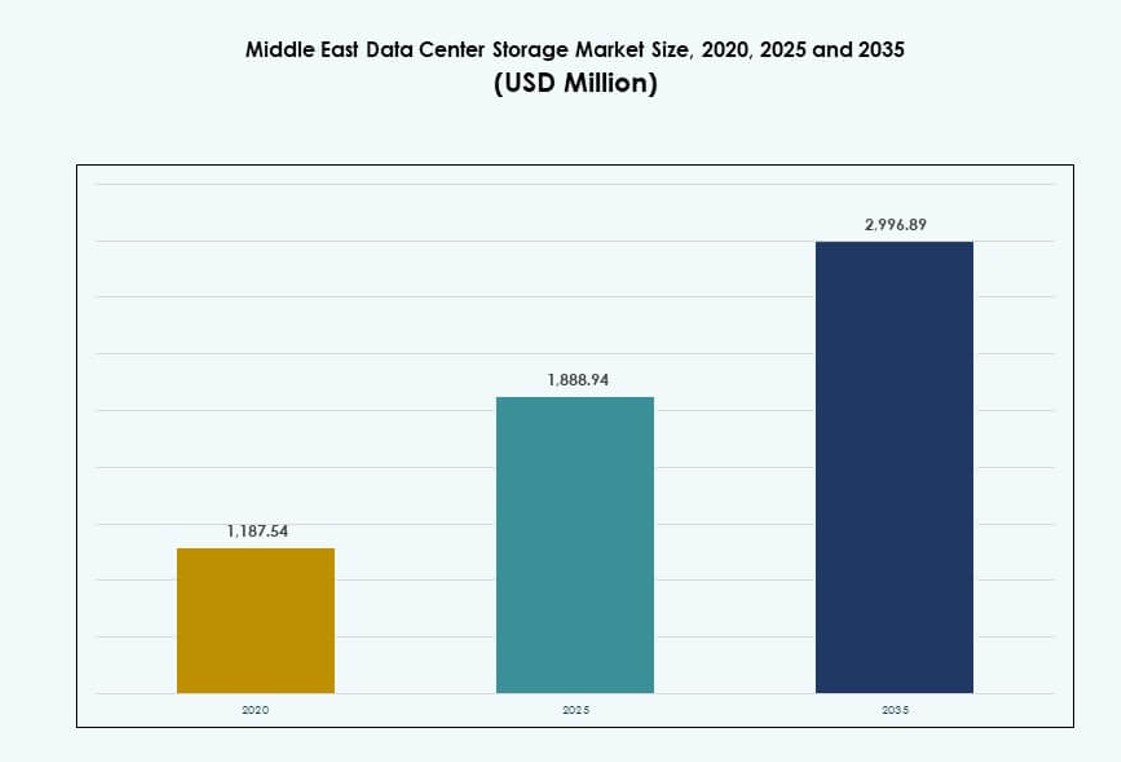

The Middle East Data Center Storage Market size was valued at USD 1,187.54 million in 2020 to USD 1,888.94 million in 2025 and is anticipated to reach USD 2,996.89 million by 2035, at a CAGR of 4.58% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Middle East Data Center Storage Market Size 2025 |

USD 1,888.94 Million |

| Middle East Data Center Storage Market, CAGR |

4.58% |

| Middle East Data Center Storage Market Size 2035 |

USD 2,996.89 Million |

The market is gaining momentum due to strong demand for AI-ready infrastructure, data localization laws, and enterprise cloud adoption. Organizations across BFSI, telecom, and government are investing in scalable storage systems to support real-time analytics, regulatory compliance, and multi-cloud environments. Technologies like software-defined storage and NVMe are transforming performance benchmarks. Businesses view storage infrastructure as vital to long-term digital competitiveness. Investors are also targeting the segment due to its role in enabling national strategies and smart city projects.

The GCC region leads the market with the UAE and Saudi Arabia driving hyperscale developments and regulatory-led hosting demand. Countries like Qatar and Israel are expanding cloud footprints, while emerging markets such as Oman and Jordan show rising investments in edge and secondary data centers. Regional growth reflects diverse digital maturity levels, with each country aligning infrastructure with national transformation agendas. This drives sustained demand across core and frontier markets.

Market Dynamics:

Digital Transformation Across Government and Private Sectors Accelerates Data Storage Demand

The Middle East Data Center Storage Market is being driven by the digitalization efforts of both governments and private entities. National programs in the UAE, Saudi Arabia, and Qatar aim to build digital economies, which increase the need for robust data storage systems. Entities across banking, telecom, and public administration are shifting from legacy systems to modern, software-defined storage. This structural shift supports real-time analytics, citizen services, and secure data retention. It also expands the use of private and hybrid clouds, creating demand for scalable storage platforms. AI-driven governance and automation tools need reliable backend infrastructure to function seamlessly. Businesses investing in storage infrastructure benefit from improved service delivery and compliance readiness. The market acts as a foundational layer for all digital operations and transformation programs in the region.

- For instance, e& (Etisalat) UAE signed a US$1 billion+ agreement with AWS in 2024 to deliver core cloud services including storage and computing across the Middle East, training 60,000 individuals in cloud technologies.

Hyperscale Expansion and Cloud Adoption Fuel Infrastructure Upgrades

Large-scale cloud deployments and hyperscale data centers are fueling investments in high-capacity, low-latency storage solutions. Regional cloud zones launched by AWS, Microsoft Azure, and Oracle are encouraging enterprises to migrate workloads from on-premise setups. This trend is pushing demand for NVMe, all-flash arrays, and software-defined storage with advanced data deduplication and backup features. Governments have mandated local hosting for critical data, driving hyperscalers to build in-region capabilities. Enterprises in telecom and banking seek higher throughput and fault tolerance. It has encouraged vendors to offer modular, energy-efficient, and compliance-ready storage systems. The Middle East Data Center Storage Market supports these infrastructure shifts, offering the scalability required to manage multi-cloud and containerized workloads.

AI and Advanced Workloads Necessitate Storage Innovation and Performance Gains

AI, machine learning, and big data analytics require faster read/write cycles and high-bandwidth connections. Businesses deploying AI for surveillance, financial modeling, or automation prefer NVMe-based all-flash storage for low-latency operations. The rise of real-time IoT analytics in industrial and oil & gas applications further boosts high-performance storage demand. The market favors platforms capable of managing structured and unstructured data across hybrid environments. Startups and research entities also rely on these storage systems to train models and handle simulations. Investors see value in performance-optimized infrastructure due to the exponential rise in enterprise data volumes. The Middle East Data Center Storage Market plays a strategic role in enabling these workloads with minimal lag and high resiliency.

- For instance, Saudi Aramco has expanded its data storage and AI processing infrastructure to support seismic and operational data analytics, leveraging high‑performance computing resources to accelerate data‑driven insights across its exploration and production operations.

Data Sovereignty, Regulatory Compliance, and Cybersecurity Drive Secure Storage Investments

Data residency laws in the Middle East require critical sectors to store and process data locally. Saudi Arabia and the UAE enforce compliance for financial institutions, telecom operators, and public cloud providers. Secure storage infrastructure with encryption, access control, and zero-trust architectures becomes a compliance asset. Cybersecurity mandates have pushed interest in backup storage and disaster recovery-as-a-service. Enterprises value storage platforms with automated threat detection and anomaly tracking. Government initiatives like smart cities, health digitization, and e-governance elevate the need for secure storage zones. The Middle East Data Center Storage Market supports this demand through tiered and compliant infrastructure models that safeguard sensitive data.

Market Trends

Adoption of Liquid-Cooled and Heat-Efficient Storage Systems for Sustainability Goals

Energy-efficient storage infrastructure is gaining traction as data center operators in the Middle East face sustainability regulations. Liquid-cooled racks and low-power flash storage systems reduce energy usage and improve thermal efficiency. Operators use AI to monitor workloads and shift inactive data to cold storage. Countries such as the UAE and Saudi Arabia offer green building incentives that encourage adoption of sustainable systems. Hyperscale facilities incorporate renewable energy alongside high-density storage to limit carbon footprint. Liquid cooling also helps improve reliability in harsh climate zones. The Middle East Data Center Storage Market sees this trend accelerating, especially among facilities targeting LEED certifications and net-zero goals.

Convergence of Storage with Edge Computing Architectures in Remote and Industrial Zones

Industries in oil, gas, and mining are deploying edge storage systems to manage data generated from remote IoT devices. These setups support localized computing and storage without needing constant internet backhaul. Edge storage is used for real-time processing of sensor data, video feeds, and equipment telemetry. Operators adopt ruggedized storage arrays optimized for harsh environments. This architecture enables data triage and sync with central data centers later. It also supports predictive maintenance and autonomous operations. The Middle East Data Center Storage Market supports edge deployments for industrial resilience and decentralized data operations across non-urban regions.

Rise of Storage-as-a-Service (STaaS) and Subscription-Based Procurement Models

Enterprises prefer flexible, consumption-based storage models to manage operational costs and avoid upfront capital investments. STaaS models allow scaling up or down based on workload demands. Managed service providers offer end-to-end storage, from provisioning to compliance monitoring. These services come with SLAs for uptime, latency, and data integrity. It helps smaller businesses adopt enterprise-grade infrastructure without infrastructure ownership. Financial and healthcare sectors lead in STaaS adoption to meet variable data needs. The Middle East Data Center Storage Market is shifting toward OPEX-led models, enabling better resource utilization and predictable IT spend.

Integration of Blockchain and Immutable Storage for Legal and Financial Archiving

Enterprises increasingly adopt blockchain-based storage mechanisms to maintain immutable records. It helps meet legal, regulatory, and audit requirements. Financial institutions and public registries deploy storage systems with tamper-proof logging and time-stamping. These solutions offer transparent change histories, improving accountability. Some use cases include transaction ledgers, land records, and patient archives. Integration with blockchain ensures data origin can be verified, reducing fraud risk. The Middle East Data Center Storage Market sees this trend in sectors handling sensitive documentation with long retention cycles.

Market Challenges

High Cost of Advanced Storage Systems and Operational Complexity for Resource-Constrained Players

Deploying modern storage infrastructure involves significant capital investment, especially in flash-based and NVMe platforms. Many enterprises struggle to match performance goals within budget limits. Mid-sized organizations and public sector bodies face difficulty adopting high-availability and multi-redundant systems. Storage system integration with legacy applications adds to complexity. A lack of in-region manufacturing leads to dependency on imports, which increases lead times. It puts stress on supply chains and limits quick deployments. The Middle East Data Center Storage Market must overcome these cost and compatibility hurdles to enable broader adoption across different verticals.

Limited Availability of Skilled Workforce and Storage Specialists Hinders Adoption of Modern Architectures

Talent shortages in data center operations extend to storage configuration, optimization, and security. While hyperscale players maintain in-house teams, smaller firms rely on limited external resources. Complexities in managing hybrid and multi-cloud storage add to the challenge. Storage cybersecurity, compliance mapping, and backup verification demand specialized skills. A lack of standardization across deployment models causes inconsistencies in service delivery. Language barriers and certification gaps also reduce effectiveness in regional training. It limits the Middle East Data Center Storage Market from scaling high-performance deployments beyond tier-1 cities.

Market Opportunities

Government Mandates and Smart Nation Programs Driving Demand for Sovereign Storage

National digital agendas across Saudi Arabia, UAE, and Qatar aim to store sensitive data within borders. Local cloud zones and national data banks seek high-capacity, secure, and compliance-ready storage platforms. These mandates create opportunities for vendors providing audit-compliant infrastructure. The Middle East Data Center Storage Market will benefit from projects requiring regional data residency and multi-tier access controls.

Healthcare, Fintech, and Surveillance Use Cases Enabling Vertical-Specific Growth Paths

Each vertical brings unique workloads, driving demand for customized storage platforms. Healthcare generates large imaging data sets, fintech requires encrypted real-time access, and surveillance needs scalable archival storage. Vendors offering tailored solutions see higher adoption. The Middle East Data Center Storage Market can tap into this segmentation to deliver vertical-centric offerings with specialized performance, availability, and retention features.

Market Segmentation

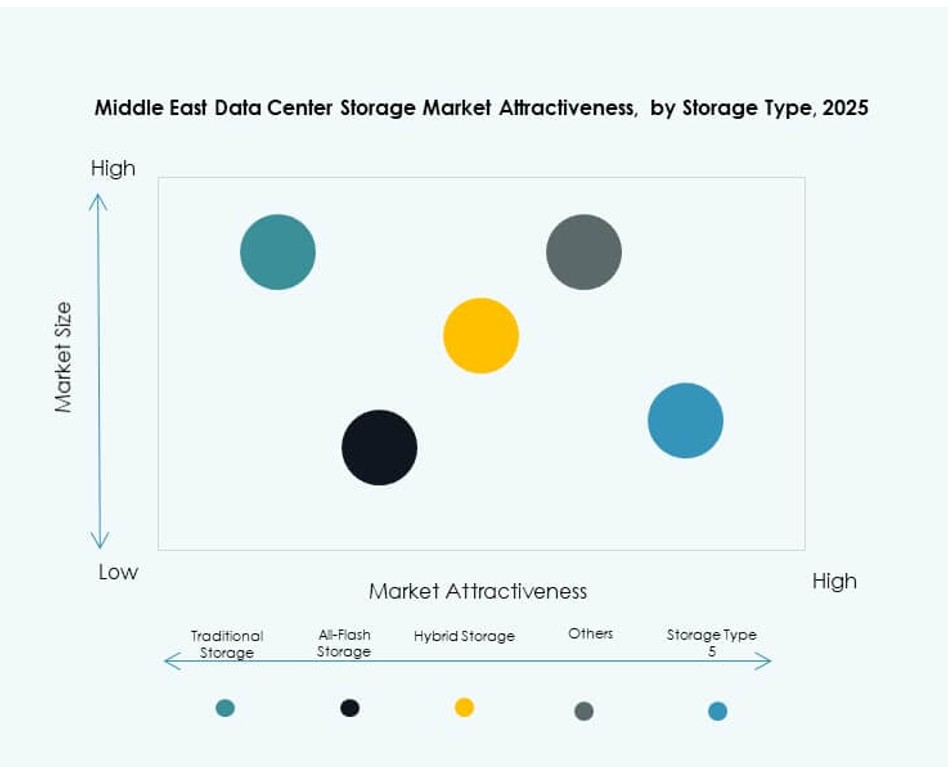

By Storage Type

Traditional storage continues to hold a significant portion of the Middle East Data Center Storage Market due to its maturity and affordability. However, all-flash storage is gaining fast adoption, particularly in BFSI and telecom segments, due to its performance benefits. Hybrid storage remains popular among enterprises seeking a balance between cost and performance. The shift toward virtualization and AI workloads drives demand for faster, scalable storage platforms across sectors.

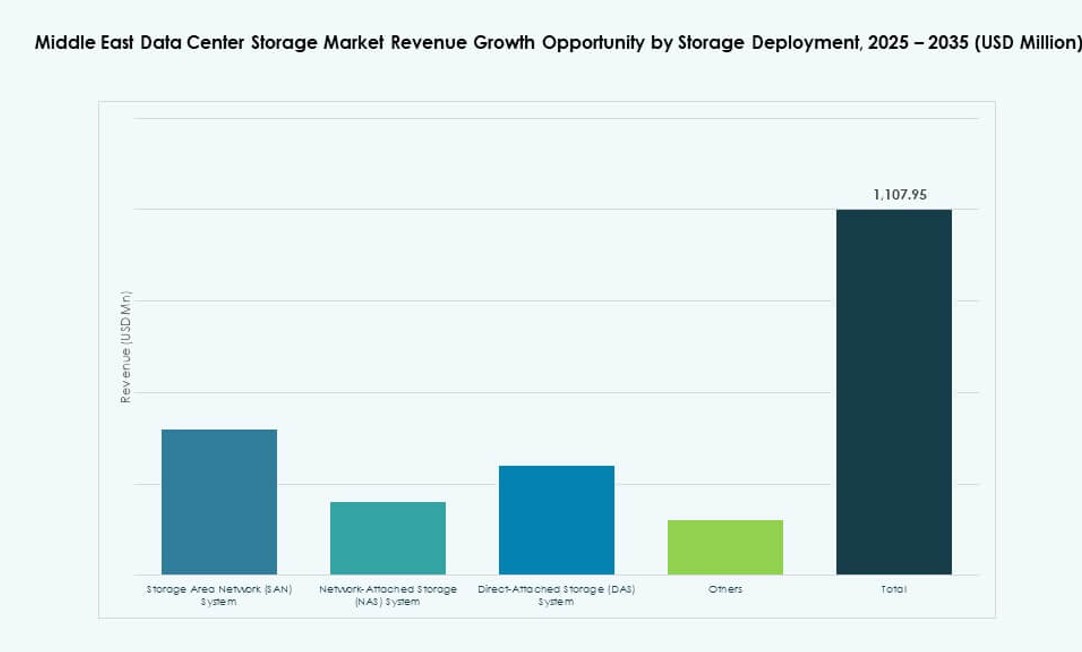

By Storage Deployment

Storage Area Network (SAN) systems dominate the market with their high-speed, block-level access capabilities. SAN is preferred in mission-critical environments such as banking, telecom, and cloud hosting. Network-attached Storage (NAS) systems are growing among SMEs and content platforms for file-level storage. Direct-attached Storage (DAS) systems serve niche applications like edge and local server setups. The Middle East Data Center Storage Market is seeing SAN and NAS integration in hybrid environments.

By Component

Hardware accounts for a major share of the market due to continued investments in physical storage infrastructure, including flash drives, enclosures, and rack systems. Software is gaining traction due to the rise in virtualized, software-defined, and AI-driven storage solutions. Features like backup orchestration, data lifecycle automation, and replication are increasingly software-led. The Middle East Data Center Storage Market is seeing growth in integrated platforms combining hardware resilience with software flexibility.

By Medium

Solid-State Drives (SSD) dominate the high-performance segment due to faster data access, lower latency, and better power efficiency. Hard Disk Drives (HDD) continue to hold market share for archival and backup purposes where capacity matters more than speed. Tape storage is still used for deep archive and compliance-related workloads in specific government and research sectors. The Middle East Data Center Storage Market is moving toward SSD adoption in all active workloads.

By Deployment Model

Cloud-based deployment models are gaining preference among mid-sized firms and digital startups for their agility, scalability, and cost efficiency. On-premises models remain strong in highly regulated sectors like defense, finance, and government. Hybrid deployments are rising across the region, supporting data localization needs while leveraging cloud flexibility. The Middle East Data Center Storage Market reflects this diverse mix of deployment choices based on compliance, cost, and operational control.

By Application

IT and telecommunications lead the market with large-scale storage requirements across multiple operations. BFSI is the second largest segment, driven by compliance-heavy workloads and transaction-intensive services. Government applications are growing due to e-governance initiatives and national digitization programs. Healthcare and education are emerging contributors with demand for secure and long-term storage. The Middle East Data Center Storage Market supports varied sectoral requirements through purpose-built solutions.

Regional Insights

GCC Region Leads with Over 65% Share Due to Cloud Expansion and Government Initiatives

The Gulf Cooperation Council (GCC) region, led by the UAE and Saudi Arabia, dominates the Middle East Data Center Storage Market with over 65% share. Its leadership comes from rapid digitalization, strong investments in hyperscale infrastructure, and national strategies like Saudi Vision 2030 and UAE Digital Economy Strategy. GCC countries have also attracted global cloud providers and telecom operators. Storage needs are growing across fintech, smart cities, and health platforms. It offers a favorable environment with incentives for green data centers and sovereign hosting.

- For example, Khazna Data Centers announced a 30MW hyperscale facility in Abu Dhabi (AUH7) in May 2024, set for operation by mid-2026, featuring carrier-neutral design with 7,500 sqm whitespace across Tier 3 modules.

Levant Region Accounts for Around 20% of the Market, Driven by Telecom and Public Sector Demand

The Levant subregion, including countries like Jordan and Lebanon, holds approximately 20% of the regional market. Telecom-led modernization and government digitization programs are major demand drivers. Local hosting and compliance are gaining relevance due to data protection regulations. Education and financial services also contribute to storage infrastructure growth. While infrastructure is smaller compared to GCC, efforts are ongoing to improve regional capacity. The Middle East Data Center Storage Market sees the Levant as an evolving but stable contributor.

Emerging Markets in North Africa Represent 15% Share with Strong Growth Potential

North African countries such as Egypt and Morocco account for nearly 15% of the Middle East Data Center Storage Market. Egypt’s ICT sector growth and Morocco’s push for digital inclusion fuel demand for data centers and modern storage systems. Investment zones and free economic areas create favorable conditions. Government and private sector initiatives are laying groundwork for cross-border digital services. While capacity is still building, the region holds strong future potential for investors targeting frontier markets.

- For instance, Dell EMC’s PowerScale storage platform, built on a scalable cluster architecture, enables enterprises to unify vast unstructured data into a single shared resource and support cloud migration, analytics, and modern workloads with flexible performance characteristics validated by global deployments.

Competitive Insights:

- Khazna Data Centers

- STC Solutions

- Gulf Data Hub

- Huawei Technologies Co., Ltd.

- Dell Technologies

- Hewlett Packard Enterprise Development LP (HPE)

- Lenovo Group

- IBM Corporation

- Seagate Technology

- Veeam Software

The Middle East Data Center Storage Market features a strong mix of global OEMs, regional operators, and vertically integrated cloud players. Global leaders like Dell, HPE, and Huawei deliver high-density and software-defined storage for hyperscale and enterprise environments. Regional players such as Khazna Data Centers and STC Solutions focus on sovereign hosting and hybrid deployments across BFSI and public sectors. Partnerships between telecom operators and global tech vendors are common for meeting compliance and latency requirements. The market favors companies offering scalable, encrypted, and workload-aware storage systems. It remains highly competitive as providers seek to capture demand across smart cities, financial services, and AI workloads.

Recent Developments:

- In December 2025, Khazna Data Centers acquired 225,000 sqm of land in Dammam, Saudi Arabia, for a 200 MW AI-ready data center campus, expanding regional storage capacity amid MENA market growth projected to double by 2030.

- In November 2025, Microsoft announced a partnership to expand data center capacity in the UAE. In this development, the company deepened its Middle East commitment through collaboration aimed at enhancing storage and computing infrastructure to meet rising regional demand.

- In October 2025, Alibaba Cloud launched its second data center in Dubai. This expansion supports broader cloud services and AI adoption in the Middle East, including partnerships with local entities like W Bank to accelerate digital infrastructure growth.

- In August 2024, Hewlett Packard Enterprise (HPE) partnered with Khazna Data Centers to launch the UAE’s first managed data center hosting service featuring direct liquid cooling for AI workloads, optimizing storage and compute efficiency to support national AI strategies.