Executive summary:

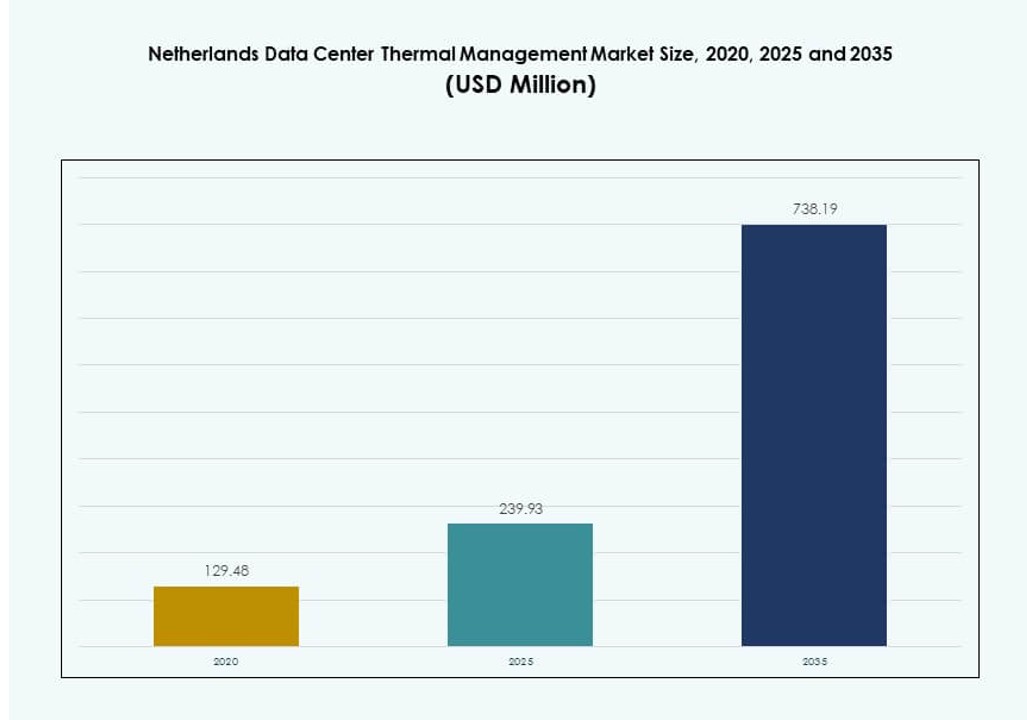

The Netherlands Data Center Thermal Management Market size was valued at USD 129.48 million in 2020 to USD 239.93 million in 2025 and is anticipated to reach USD 738.19 million by 2035, at a CAGR of 11.83% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Netherlands Data Center Thermal Management Market Size 2025 |

USD 239.93 Million |

| Netherlands Data Center Thermal Netherlands Market, CAGR |

11.83% |

| Europe Data Center Thermal Management Market Size 2035 |

USD 738.19 Million |

Market growth is driven by rising rack density, AI workloads, and strict energy efficiency targets. Operators adopt liquid cooling, advanced airflow control, and smart thermal software to manage heat loads. Innovation focuses on hybrid cooling and heat reuse systems. The market holds strategic value for businesses and investors by enabling lower operating costs, regulatory compliance, and long-term asset resilience in high-demand digital infrastructure.

Geographically, the Randstad region leads due to its concentration of hyperscale and colocation data centers. Amsterdam acts as the core connectivity and cloud hub. Emerging regions such as North Brabant and Groningen gain attention due to land availability and grid access. These areas support decentralization strategies and future expansion while maintaining national network performance and reliability.

Market Dynamics:

Market Drivers

Rise of High-Density Computing and AI Workloads Requiring Advanced Cooling Infrastructure

The rise in high-density server environments, driven by AI, machine learning, and HPC applications, is reshaping cooling demands. Traditional systems struggle to manage rack loads above 20 kW, pushing adoption of liquid cooling and hybrid systems. The Netherlands Data Center Thermal Management Market responds with direct-to-chip and immersion cooling. These technologies enable reduced energy usage and enhance thermal control at rack level. Operators adopt innovative systems to prevent hotspots and improve server uptime. Hyperscalers prefer thermal management that supports GPU-heavy deployments. Advanced cooling becomes essential to maximize performance within regulatory energy limits. Businesses view this as a critical enabler for future scalability.

Government Pressure to Lower PUE and Achieve Carbon-Neutral Data Infrastructure

Stringent energy-efficiency regulations in the Netherlands target data centers with high power usage. Authorities enforce low PUE thresholds, encouraging operators to replace legacy air systems with sustainable alternatives. The Netherlands Data Center Thermal Management Market aligns with national carbon targets, accelerating green cooling innovation. Data centers reduce their environmental footprint through heat reuse and renewable cooling sources. Regulatory frameworks such as energy labeling and building performance standards guide procurement. Investors consider sustainability credentials essential for project approval. Efficient thermal systems directly impact ESG compliance and long-term asset value. This creates strong demand across both new builds and retrofits.

- For example, Microsoft’s Netherlands data centers achieved a PUE of 1.14 and WUE of 0.04 L/kWh through direct evaporative cooling used less than 5% of the year.

Strategic Location of the Netherlands as a Connectivity Hub Demands Efficient Cooling

The Netherlands acts as a digital gateway to Europe, with Amsterdam hosting over 70% of the country’s data capacity. Its location attracts hyperscale and interconnection providers operating at high intensity. This density requires highly efficient thermal management to maintain operational reliability. The Netherlands Data Center Thermal Management Market benefits from this cluster effect, driving system upgrades and service innovation. Proximity to undersea cables and financial institutions increases uptime expectations. Efficient cooling reduces operational disruptions and supports competitive SLAs. Businesses prioritize thermal strategies in tender processes. This makes advanced cooling a differentiator in high-value colocation and cloud bids.

- For example, Amsterdam hosts over 70% of Netherlands data capacity, driving dense operations where operators like Microsoft maintain low PUE via efficient air-based cooling.

Retrofit Opportunities in Aging Data Centers Accelerating Hybrid Cooling Deployment

Many legacy data centers in the Netherlands operate below modern efficiency standards, presenting significant retrofit potential. Operators focus on hybrid cooling solutions to balance cost and performance. The Netherlands Data Center Thermal Management Market sees growing interest in modular, rack-based systems for retrofitting without downtime. Solutions like rear-door heat exchangers and in-row cooling support gradual upgrades. The demand for smart cooling retrofits includes DCIM integration and AI-based thermal optimization. Retrofits offer quick wins in sustainability scoring and energy bill reduction. Investors support brownfield upgrades for faster ROI. Retrofit-focused services open growth for OEMs and local system integrators.

Market Trends

Adoption of Smart Thermal Management Systems for Predictive and Autonomous Cooling

Operators are integrating AI-powered controls to manage cooling dynamically based on real-time workload demands. These systems predict thermal spikes and optimize energy use across cooling units. The Netherlands Data Center Thermal Management Market reflects this with growing use of machine learning models for airflow control. DCIM and BMS modules integrate temperature, humidity, and power data to automate responses. Predictive maintenance is enabled by thermal analytics and sensor fusion. These capabilities minimize human intervention and prevent failure risks. Businesses rely on smart systems to improve uptime and reduce service costs. The transition supports the move toward autonomous data center operations.

Expansion of Liquid Cooling Adoption in GPU and HPC-Dense Environments

The adoption of liquid cooling technologies is growing rapidly in AI and HPC deployments. Direct-to-chip and immersion cooling enable efficient heat removal for racks exceeding 30 kW. The Netherlands Data Center Thermal Management Market aligns with this shift as hyperscale demand rises. Operators focus on liquid-cooled pods and modular deployments to handle dense server loads. Liquid solutions improve PUE and reduce mechanical system stress. Cooling distribution units are now common in new builds. Vendors offer prefabricated liquid systems for faster rollouts. This trend supports lower TCO and aligns with sustainability benchmarks.

Integration of Thermal Management with District Heating and Circular Energy Models

Thermal systems are being integrated into district heating networks to reuse excess heat. Operators feed waste heat into municipal grids, reducing cooling costs and supporting sustainability goals. The Netherlands Data Center Thermal Management Market is a key part of this circular energy approach. Projects in Amsterdam and Rotterdam export recovered heat to thousands of homes. This trend promotes collaboration between utilities, municipalities, and data centers. Energy efficiency incentives encourage participation. The integration supports zero-waste cooling strategies. It positions thermal management as a revenue-generating function in green data infrastructure.

Growth in Modular and Scalable Cooling Infrastructure for Edge and Regional Expansion

Edge deployments and regional data centers require modular, compact cooling solutions with easy scalability. The Netherlands Data Center Thermal Management Market adapts with containerized and row-based cooling setups. Vendors design units with flexible deployment for suburban or micro data centers. These systems offer plug-and-play installation, remote management, and low setup costs. This trend supports latency-sensitive services like IoT, 5G, and media streaming. Operators focus on agility and low-risk investment models. Modular thermal solutions meet demand without large CAPEX. It reflects the shift to distributed infrastructure across the country.

Market Challenges

Land and Power Constraints Impact Cooling System Deployment and Scalability

Urban data center zones face land scarcity and power limitations that constrain large-scale cooling infrastructure. These constraints affect the design of thermal management systems and limit choices for high-capacity cooling. The Netherlands Data Center Thermal Management Market must adapt to smaller footprints and power budgets. Operators balance thermal efficiency with space optimization. High-density rack zones require tailored cooling distribution. Grid congestion delays the deployment of liquid cooling and district heat export systems. These issues raise project timelines and reduce operational flexibility. Strategic planning and advanced modeling are required to overcome these site-specific challenges.

High Upfront Costs and Technical Complexity of Next-Gen Cooling Technologies

New cooling solutions, particularly liquid-based and AI-optimized systems, involve significant capital investment. Operators hesitate to upgrade without guaranteed ROI or regulatory pressure. The Netherlands Data Center Thermal Management Market contends with adoption barriers for complex thermal designs. These systems require skilled technicians, advanced sensors, and custom integration. Cooling retrofits also involve risk to uptime and airflow disruptions. Some colocation providers delay upgrades due to client sensitivity. Market adoption depends on education, incentives, and service partnerships. Vendors must demonstrate efficiency gains clearly to drive faster transition.

Market Opportunities

Surging Demand for Immersion and Direct-to-Chip Cooling in AI Data Workloads

AI expansion drives adoption of immersion and direct-to-chip cooling, especially in HPC and GPU-heavy facilities. These technologies reduce mechanical load and support compact, energy-efficient designs. The Netherlands Data Center Thermal Management Market sees rapid traction for such solutions among hyperscale operators. Vendors offer high-performance liquid solutions tailored for regional rack densities. Data centers seek differentiation through cooling performance. This niche offers strong growth for OEMs and fluid manufacturers.

Retrofit-Focused Services and Thermal Software Solutions Unlock New Revenue Streams

The retrofit market opens recurring revenue for service providers offering thermal monitoring, DCIM software, and predictive diagnostics. The Netherlands Data Center Thermal Management Market evolves toward software-defined cooling. Operators integrate CFD and AI-based insights to manage legacy airflow. System integrators and retrofit specialists gain long-term contracts. These opportunities support both brownfield and mixed-tier sites.

Market Segmentation

By Data Center Size

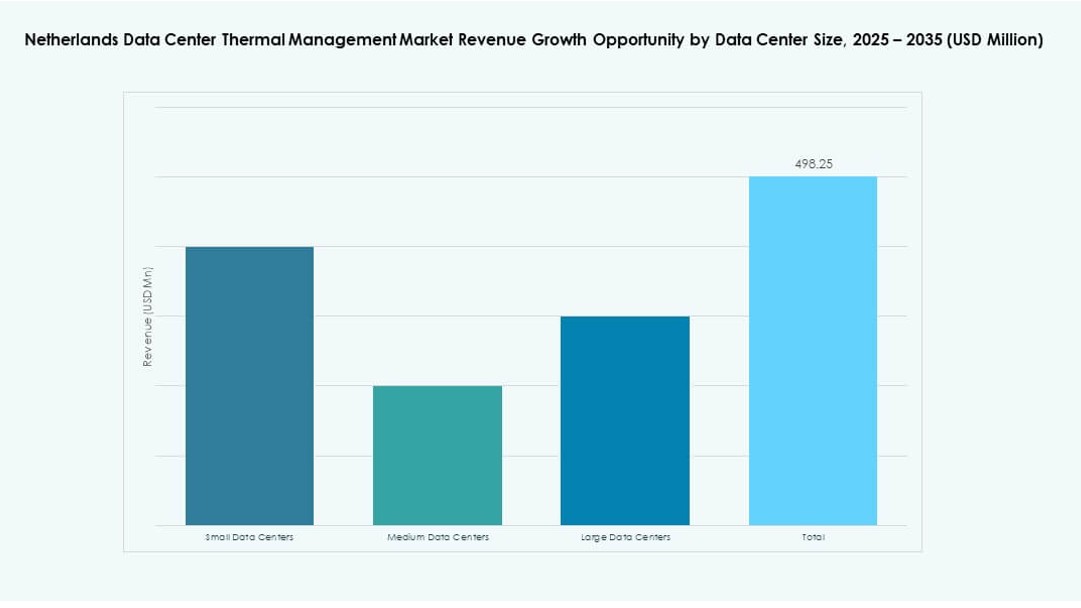

Large data centers dominate the Netherlands Data Center Thermal Management Market due to high processing loads from cloud and hyperscale firms. These facilities demand robust and efficient thermal infrastructure. Medium-sized data centers are growing steadily, driven by enterprise and government workloads. Small data centers focus on modular and edge-friendly cooling systems. Vendors offer tailored solutions to each size tier.

By Cooling Technology

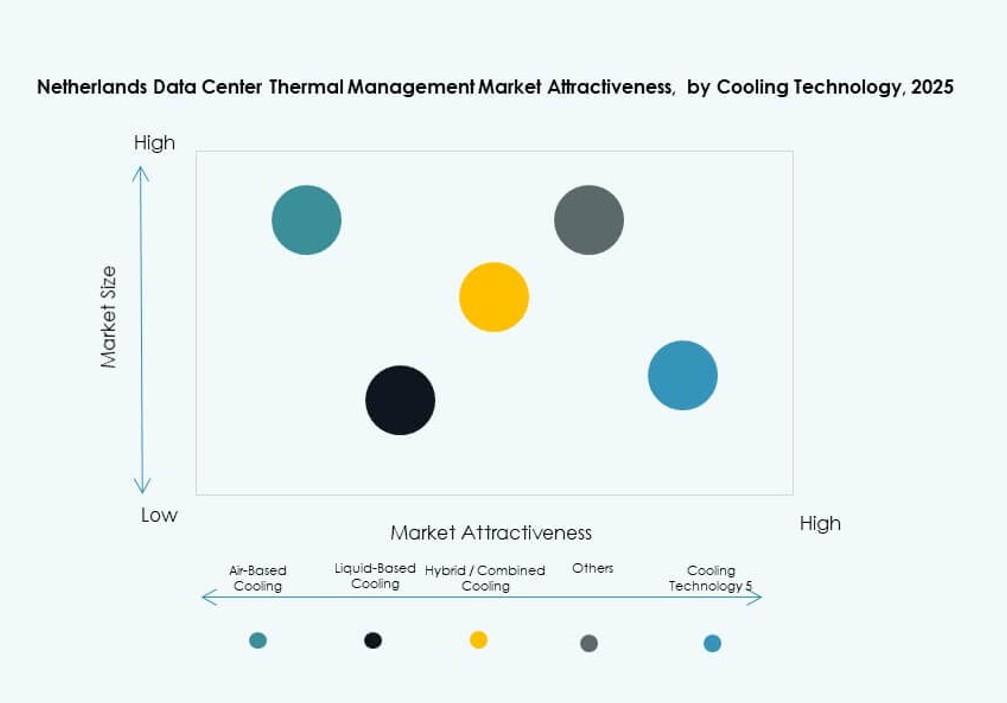

Air-based cooling remains widely used, particularly hot/cold aisle containment and rear door heat exchangers. However, liquid-based cooling is gaining market share, especially direct-to-chip and immersion setups for high-density zones. Hybrid systems combining air and liquid cooling are preferred in retrofits. Thermoelectric and phase-change technologies remain niche but grow in specialized applications. The Netherlands Data Center Thermal Management Market reflects this diverse technology landscape.

By Component

Hardware remains the largest component segment, accounting for bulk of thermal system investment. It includes chillers, heat exchangers, and airflow units. Software is rapidly growing with DCIM and AI optimization tools enabling smart thermal control. Services such as retrofits, monitoring, and preventive maintenance ensure long-term system performance. These components form an integrated thermal ecosystem in modern data centers.

By Hardware

Cooling units and chillers hold a major share, followed by fans, heat exchangers, and airflow devices. High-efficiency fans and advanced piping systems are in demand to reduce energy loss. Rear door and in-rack systems support high-density cooling needs. OEMs offer component-level upgrades to meet PUE goals. The Netherlands Data Center Thermal Management Market benefits from advanced hardware design.

By Software

DCIM dashboards and AI optimization tools dominate the software segment. These systems provide real-time cooling analytics, performance benchmarking, and predictive modeling. CFD simulations help design efficient airflow layouts. BMS modules integrate cooling with facility-level systems. Software enables automation and regulatory compliance, driving higher adoption across the Netherlands Data Center Thermal Management Market.

By Services

Preventive maintenance and retrofits lead the services segment due to ongoing energy efficiency upgrades. Installation and commissioning services remain important for new builds. Monitoring-as-a-Service offers scalable thermal oversight. Vendors offer bundled services for lifecycle cooling management. The Netherlands Data Center Thermal Management Market grows through recurring service engagement.

By Data Center Type

Colocation and cloud data centers dominate due to multi-tenant facilities in Amsterdam and other urban hubs. Hyperscale facilities drive innovation in thermal efficiency. Enterprise and edge data centers focus on modular systems. Each data center type drives demand for tailored cooling strategies. The Netherlands Data Center Thermal Management Market adapts its offerings by deployment model.

By Structure

Room-based cooling is common in legacy and large-scale deployments. Row- and rack-based systems gain share due to their modularity and space efficiency. Row-based systems support scalable retrofits and dense computing. Operators invest in flexible structures to manage thermal zones precisely. This diversity supports optimal cooling alignment across workloads.

Regional Insights

Randstad Region Leads Market Share Due to Dense Data Infrastructure and Hyperscale Activity

The Randstad region, comprising Amsterdam, Rotterdam, Utrecht, and The Hague, holds over 70% of the Netherlands Data Center Thermal Management Market. It hosts the largest colocation, cloud, and interconnection hubs in the country. Amsterdam alone accounts for the majority of new deployments and upgrades. Operators in this zone implement advanced cooling to meet strict energy efficiency rules. Proximity to subsea cables and financial institutions makes thermal resilience critical. It remains the epicenter of demand for innovative cooling solutions.

Emerging Regions Like North Brabant and Groningen Support Market Decentralization

North Brabant and Groningen are gaining market share, contributing around 15% to the Netherlands Data Center Thermal Management Market. These regions benefit from available land, grid capacity, and government incentives. Developers expand regional data centers to reduce dependence on Amsterdam. Edge facilities in these areas require modular cooling infrastructure. Local authorities promote sustainable design through planning regulations. These regions provide stable environments for distributed workloads and backup services.

- For instance, NorthC’s GR1 leverages groundwater cooling (ATES) systems, achieving PUE below 1.2 while supporting up to 10 MW IT load in a sustainable design.

Other Regions Witness Gradual Adoption Driven by Edge, 5G, and Media Workloads

Smaller subregions such as Limburg, Gelderland, and Overijssel represent the remaining 15% market share. Their growth is slower but steady, driven by emerging edge deployments, CDN services, and digital transformation projects. Cooling solutions in these zones focus on compact, scalable designs. Operators prefer low-maintenance and remote-controlled systems. These areas enable national coverage with localized latency and resilience. The Netherlands Data Center Thermal Management Market grows through this geographic diversification.

- For instance, Eurofiber’s Netherlands data centers use N+1 redundant cooling systems, including free cooling and chillers, to ensure energy-efficient and reliable thermal performance across regional colocation sites. These facilities are designed with high availability and sustainable infrastructure in mind.

Competitive Insights:

- Vertiv Group Corp.

- Schneider Electric SE

- Trane Technologies plc

- Airedale International Air Conditioning Ltd.

- Daikin Industries Ltd.

- Johnson Controls International plc

- Huawei Technologies Co., Ltd.

- Delta Electronics, Inc.

- Mitsubishi Electric Corporation

- Asetek, Inc.

The Netherlands Data Center Thermal Management Market remains highly competitive, with a mix of global OEMs, thermal specialists, and local integrators. Vertiv and Schneider Electric lead in high-density, AI-ready cooling systems tailored for hyperscale and colocation environments. Trane, Johnson Controls, and Daikin hold strong positions in precision HVAC and building-level integration. Airedale and Asetek differentiate through immersion and direct-to-chip liquid cooling. Huawei and Delta Electronics drive adoption through power-thermal convergence. Local firms like Royal HaskoningDHV and Dataplace focus on retrofit projects and modular deployments. It favors vendors offering scalable, low-PUE, and retrofit-friendly solutions. Strategic partnerships, smart software integration, and energy-efficient designs define competitive positioning. Product localization, service support, and green compliance are key decision factors among Dutch operators.

Recent Developments:

- In September 2024, power technology company Infinity Turbine launched and promoted its Cluster Mesh Power Generation System specifically targeting Dutch AI data centers to address rising thermal and energy demands

- In July 2024, European colocation provider Penta Infra and heating company Polderwarmte signed a letter of intent (LOI) to reuse residual heat from Penta’s AMS01 data center in Haarlem.