Executive summary:

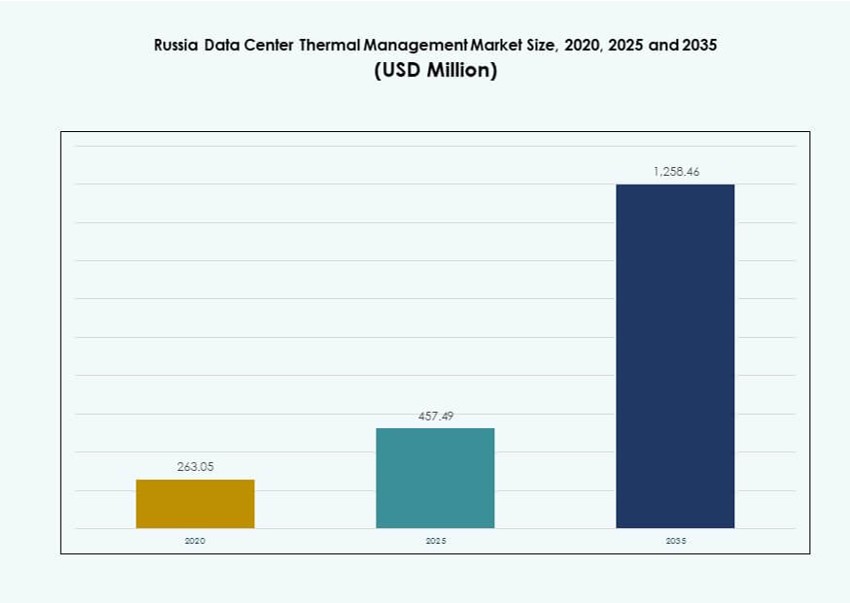

The Russia Data Center Thermal Management Market size was valued at USD 263.05 million in 2020, rising to USD 457.49 million in 2025, and is anticipated to reach USD 1,258.46 million by 2035, at a CAGR of 10.59% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Russia Data Center Thermal Management Market Size 2025 |

USD 457.49 Million |

| Russia Data Center Thermal Netherlands Market, CAGR |

10.59% |

| Russia Data Center Thermal Management Market Size 2035 |

USD 1,258.46 Million |

Rising demand for high-performance computing, data localization policies, and liquid cooling adoption are driving market growth. Operators are deploying AI-optimized thermal systems, shifting from traditional air-based methods to hybrid and liquid-based cooling. The expansion of hyperscale, colocation, and edge facilities boosts investment in efficient and scalable thermal infrastructure. Innovation in cooling hardware, software, and services improves energy use and system reliability. These factors position the Russia Data Center Thermal Management Market as a strategic space for investors, tech vendors, and infrastructure developers targeting long-term digital growth.

Central Russia, including Moscow and its surrounding areas, leads the market due to hyperscale concentration and strong enterprise demand. Northwestern Russia, particularly St. Petersburg, follows with growing colocation hubs and favorable cooling conditions. Emerging clusters in regions like Kazan, Yekaterinburg, and Novosibirsk show rising interest driven by industrial digitization and smart city projects. Cold climates in several zones support energy-efficient designs and waste heat reuse opportunities. This regional diversity shapes deployment strategies across the market.

Market Dynamics:

Market Drivers

Rising High-Density Workloads Across Major Cities Demands Advanced Cooling Solutions

Russia’s growing use of high-performance computing, AI clusters, and GPU-intensive workloads drives demand for precision thermal systems. Cities like Moscow and St. Petersburg host data centers operating at higher rack densities, often exceeding 20 kW per rack. These loads require liquid cooling systems and advanced airflow control to maintain reliability. Operators deploy direct-to-chip and rear door heat exchangers to prevent thermal spikes. Demand for rack-level cooling is pushing upgrades in legacy centers. The Russia Data Center Thermal Management Market benefits from the shift to modular, high-efficiency systems. Investors view thermal infrastructure upgrades as necessary for uptime assurance. Adoption of new cooling tech directly ties to data center expansion and modernization.

Domestic Data Localization Policies Support Infrastructure Growth and Cooling Investments

Data sovereignty laws require companies to store and process citizen data within Russian borders. This has led to strong domestic data center expansion, creating demand for thermal systems. Government regulations have accelerated construction of local facilities, boosting demand for efficient cooling equipment. Operators are scaling infrastructure across secondary cities, increasing regional cooling needs. Growth in edge data centers also supports small-scale cooling deployments. Russia Data Center Thermal Management Market growth ties closely to these regulatory drivers. Hardware and service vendors gain from localized infrastructure mandates. Strategic data hosting compliance fuels continuous demand for cooling upgrades.

- For instance, Rostelecom’s Moscow-IV data center is a Tier IV facility under development in Moscow with a planned capacity of 17 MW. It features redundant infrastructure and advanced cooling systems designed to support enterprise colocation and high availability.

Shift Toward Energy Efficiency and Lower PUE in Harsh Operating Conditions

Operators aim to reduce power usage effectiveness (PUE) and improve energy efficiency in colder regions. Though ambient air can support free cooling, thermal design must adapt to seasonal variations. Many facilities now use hybrid systems combining liquid and air cooling to balance energy use. Cold climates also require frost control and humidity balancing, which adds thermal complexity. The Russia Data Center Thermal Management Market benefits from energy-efficiency mandates tied to ESG goals. Investors seek infrastructure that can meet environmental targets without compromising uptime. Thermal innovations are now critical for both economic and regulatory compliance. Local vendors compete by offering region-specific cooling modules.

Edge Deployments and IoT Integration Accelerate Need for Scalable Thermal Infrastructure

The rollout of smart cities, 5G networks, and IoT devices increases edge computing deployments. These distributed nodes require compact and scalable cooling units. Micro data centers must operate in varying environments, demanding rugged and flexible thermal designs. Liquid-based and passive cooling technologies support edge growth in remote areas. Software-driven optimization enhances temperature control across distributed systems. Russia Data Center Thermal Management Market players are investing in edge-ready cooling portfolios. These trends create new opportunities for modular, easy-to-deploy thermal units. Edge expansion supports demand beyond large hubs and into secondary cities and industrial zones.

- For instance, Vertiv deployed Liebert AFC adiabatic free‑cooling chillers and Liebert PDX systems with EconoPhase at IXcellerate’s Moscow One campus, significantly cutting cooling energy use and enabling partial PUE levels as low as 1.05 in high‑density data halls.

Market Trends

Liquid Cooling Technologies See Rising Adoption Across Hyperscale and Colocation Data Centers

Direct-to-chip and immersion cooling technologies are gaining momentum across hyperscale facilities in Russia. Operators targeting densities above 30 kW per rack adopt liquid cooling to improve heat removal. Immersion cooling finds use in AI and crypto mining setups, where thermal loads are intense. Rear door heat exchangers using liquid circulation improve energy transfer without raising fan loads. Russia Data Center Thermal Management Market trends show steady migration from legacy air-cooled systems to liquid-based designs. Vendors now offer integrated systems with built-in pumps, manifolds, and heat exchangers. Adoption remains strongest among new builds, though retrofits are increasing.

Software Optimization and Predictive Analytics Reshape Thermal Operations Management

Vendors embed AI-powered modules into cooling infrastructure to enable real-time thermal analytics. Data center operators use machine learning models to predict heat zones and optimize airflow. Software-defined thermal management reduces response time to load changes and improves efficiency. DCIM platforms integrate thermal dashboards for visibility and automation. The Russia Data Center Thermal Management Market benefits from growing adoption of intelligent cooling controls. CFD simulations are used in design planning to minimize hotspots. Predictive control helps lower mechanical cooling needs, saving operational energy. Software is now a core part of holistic thermal management solutions.

High Investment in Modular Cooling Systems to Support Scalable Deployments

Modular cooling units gain popularity due to faster setup time and ease of scalability. These prefabricated systems support rapid expansion without disrupting operations. Row-based and rack-based units allow precise temperature control in isolated zones. Operators prefer modular units for edge and enterprise deployments. Russia Data Center Thermal Management Market trends indicate rising use of containerized cooling pods. These systems reduce installation time and capital expenses. Vendors now offer modular kits including airflow devices, sensors, and smart controls. Scalable thermal infrastructure is key to managing dynamic workloads.

District Heating and Heat Recovery Technologies Gain Strategic Interest

Operators explore opportunities to reuse waste heat from data centers in nearby residential or industrial heating networks. Russia’s cold climate offers strong potential for heat recovery through water-based loops. Urban data centers consider integration with municipal district heating grids. Some providers offer modular systems with heat exchangers that capture thermal output. Russia Data Center Thermal Management Market stakeholders recognize long-term economic and environmental gains from heat reuse. Projects in Moscow and Kazan are exploring pilot-scale heat transfer systems. These efforts align with sustainability targets and improve public-private collaboration.

Market Challenges

Harsh Climatic Conditions and Infrastructure Limitations Impact Cooling System Design

Russia’s vast geography brings extreme cold in northern areas and heat in southern zones, complicating system design. Seasonal variation challenges stable temperature control, especially for facilities using outside air for free cooling. Equipment must endure rapid weather changes without compromising internal temperature ranges. Humidity and frost risk require extra insulation and defrosting features. Russia Data Center Thermal Management Market stakeholders must design systems resilient to wide thermal swings. Infrastructure in remote areas lacks stable power and connectivity, limiting adoption of advanced systems. Harsh climates increase maintenance costs and reduce equipment lifespan.

Supply Chain Constraints and Import Dependency Affect Thermal Equipment Availability

Sanctions and trade restrictions limit access to global vendors, affecting delivery timelines and pricing. Many components used in high-performance cooling systems rely on international suppliers. Delays in shipments or limited availability create integration risks for operators. Domestic manufacturing capacity for advanced cooling components remains limited. The Russia Data Center Thermal Management Market faces higher costs and longer deployment cycles due to import dependency. Local vendors struggle to meet rising demand for precision-engineered systems. This limits the pace of modernization and affects competitiveness against global benchmarks.

Market Opportunities

Expansion of Edge and Modular Data Centers Unlocks New Cooling Applications

Edge and micro data center growth in rural and industrial areas creates demand for flexible thermal systems. Compact liquid and hybrid cooling units support limited-space environments. These applications need low-power and maintenance-friendly solutions. Russia Data Center Thermal Management Market players can benefit from offering localized and rugged thermal solutions. Prefabricated kits designed for plug-and-play use offer strong commercial value. Vendors focusing on rural digitization and IoT rollouts find new revenue channels.

Sustainability Goals and ESG Reporting Fuel Demand for Green Cooling Solutions

Operators must align with energy-efficiency goals and reduce emissions. This drives investment in low-PUE systems and alternative cooling approaches. Russia Data Center Thermal Management Market sees interest in systems with natural refrigerants, heat reuse, and AI-driven controls. Sustainable cooling adds long-term asset value and improves investor appeal. Providers offering measurable energy-saving solutions gain market edge. ESG-driven procurement favors vendors with proven sustainability performance.

Market Segmentation

By Data Center Size

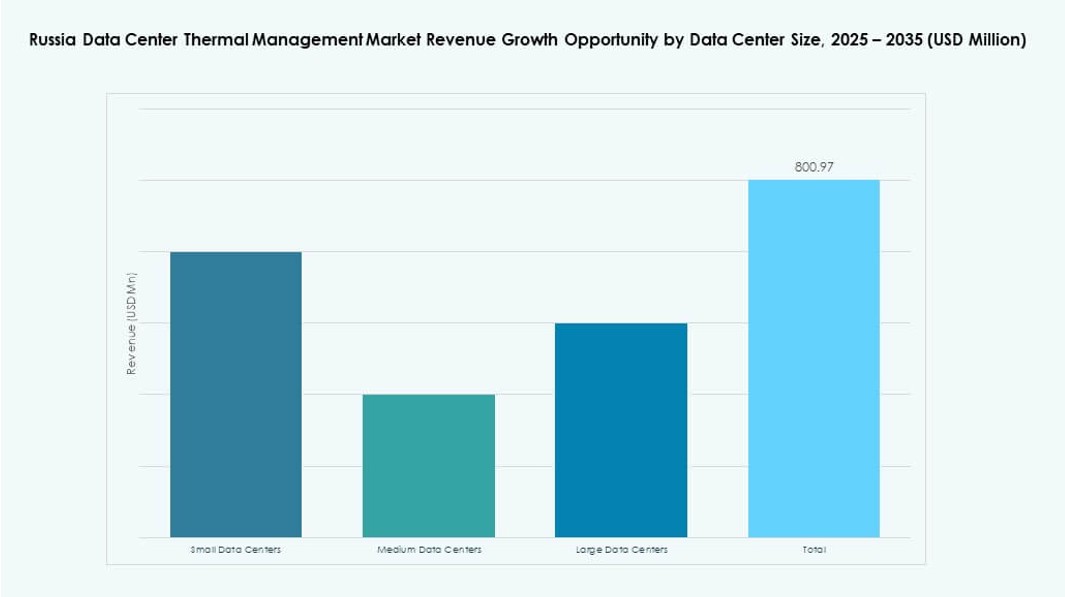

Large data centers dominate the Russia Data Center Thermal Management Market due to hyperscale and colocation growth in Moscow and St. Petersburg. Medium data centers follow, supporting enterprise workloads across Tier II cities. Small centers are growing with edge and IoT expansion. Large facilities drive demand for scalable and high-capacity cooling systems, including liquid and hybrid models.

By Cooling Technology

Air-based cooling remains widely used, especially direct air and hot/cold aisle containment methods in mid-sized facilities. However, liquid-based cooling—particularly direct-to-chip and immersion—is growing among high-density centers. Hybrid systems combining both are seeing increasing adoption for balancing efficiency and cost. Thermoelectric and phase-change technologies remain niche but may grow in specialized applications.

By Component

Hardware forms the core of thermal investments, with dominant share in chillers, heat exchangers, and airflow devices. Software adoption grows due to AI optimization and DCIM integration. Services such as retrofits and remote monitoring gain traction, especially among older facilities upgrading to modern standards.

By Hardware

Cooling units and chillers hold the largest share due to high capital allocation for core cooling. Heat exchangers and airflow devices support rack-level temperature control. Piping and distribution remain crucial for liquid setups. Other components such as thermal sensors and bypass valves add system-level efficiency.

By Software

DCIM dashboards and AI optimization tools are widely adopted for real-time cooling control. BMS modules are used in integration with facility systems. CFD simulation tools gain popularity in new builds and retrofits. Software helps reduce overcooling, optimizing airflow and energy consumption.

By Services

Installation and commissioning dominate due to steady new data center deployment. Preventive maintenance ensures cooling reliability and reduces unplanned downtime. Retrofits and upgrades attract investments from aging facilities. Monitoring-as-a-service is emerging in remote operations.

By Data Center Type

Hyperscale and colocation/cloud centers lead thermal management spending due to their scale and density. Enterprise centers remain steady but slower in adopting newer cooling. Edge/micro centers are fastest-growing, demanding compact and rugged solutions for decentralized computing.

By Structure

Room-based cooling remains in use for legacy centers, but rack- and row-based structures dominate new deployments. Rack-based cooling supports high-density IT loads, while row-based designs offer efficient aisle containment. Modular setups enhance scalability and airflow control.

Regional Insights

Central Russia Leads Market Activity with Over 55% Share Driven by Hyperscale Expansion

Moscow and its surrounding areas account for more than half of the Russia Data Center Thermal Management Market. This region hosts most hyperscale and enterprise data centers, backed by strong IT infrastructure and cloud service demand. Operators deploy advanced cooling systems, including hybrid and liquid solutions. Regional regulatory clarity also supports steady data center construction. The concentration of business, finance, and tech industries fuels market dominance. Thermal investments here focus on uptime assurance and energy optimization.

- For example, Moscow hosts Rostelecom’s Moscow-III data center, which spans 3,500 square meters with capacity for 900 racks and 10 MW of power. This Tier III facility includes state-of-the-art cooling systems alongside redundant power supplies for high uptime reliability.

Northwestern Russia Holds 20% Market Share Driven by Colocation Growth in St. Petersburg

St. Petersburg serves as the second-largest hub with growing colocation and cloud facility presence. Cold climate conditions allow operators to leverage free cooling and heat reuse methods. Thermal system providers deploy custom solutions to suit architectural constraints in historic zones. Regional universities and R&D hubs also drive edge computing and localized data hosting. The Russia Data Center Thermal Management Market benefits from diversified demand and strong tech ecosystem in this subregion.

- For example, IXcellerate’s Moscow-One data center (relevant to regional operations) features a flexible cooling system combining chilled water and DX units with N+1 redundancy, expandable to 13.7 MW capacity. It supports 185 standard racks across 600 square meters of data halls with a design PUE of 1.4 at full load.

Volga, Ural, and Siberian Regions Share Remaining 25% as Emerging Clusters Rise

Cities like Kazan, Yekaterinburg, and Novosibirsk show rising activity with local government support and industrial digitization. These regions demand mid-sized and edge data centers, often with modular cooling setups. Cold weather zones enable natural cooling, reducing energy consumption. Thermal investments here focus on rugged and scalable systems. Market growth remains slower than central regions but shows strong future potential. Vendors expanding to these areas gain first-mover advantage.

Competitive Insights:

- Vertiv Group Corp.

- Daikin Industries Ltd.

- Delta Electronics, Inc.

- Johnson Controls International plc

- Airedale International Air Conditioning Ltd.

- Rittal

- Asetek, Inc.

- Black Box Corporation

- Mitsubishi Electric Corporation

- Huawei Technologies Co., Ltd.

The competitive landscape shows strong presence from global HVAC and thermal solution leaders and local engineering firms. Vertiv Group Corp. competes through comprehensive power and cooling portfolios that match large data center needs. Daikin and Delta focus on energy-efficient chillers and modular systems that fit both hyperscale and colocation facilities. Johnson Controls and Airedale emphasize integrated building systems that lower operational costs. Rittal and Asetek drive niche cooling solutions for high-density racks. Black Box and Huawei combine infrastructure services with thermal products to meet enterprise demand. Mitsubishi Electric and other players target customized deployments for edge and remote facilities. In this market, innovation, local support, and total cost of ownership remain key factors in vendor differentiation and long-term contracts.

Recent Developments:

- In November 2025, Rittal LLC announced its showcase of integrated IT infrastructure and AI-ready liquid cooling solutions at SC25 (November 16–21), targeting high-density data center workloads.

- In November 2025, Delta partnered with Siemens on prefabricated modular data center power solutions, combining Delta’s UPS, battery, and cooling with Siemens’ distribution to cut deployment time by up to half in fast-growing markets.

- In August 2025, Daikin acquired DDC Solutions, a leader in rack-level air conditioning for AI data centers, to integrate with its commercial cooling portfolio and expand globally starting in North America.