Executive summary:

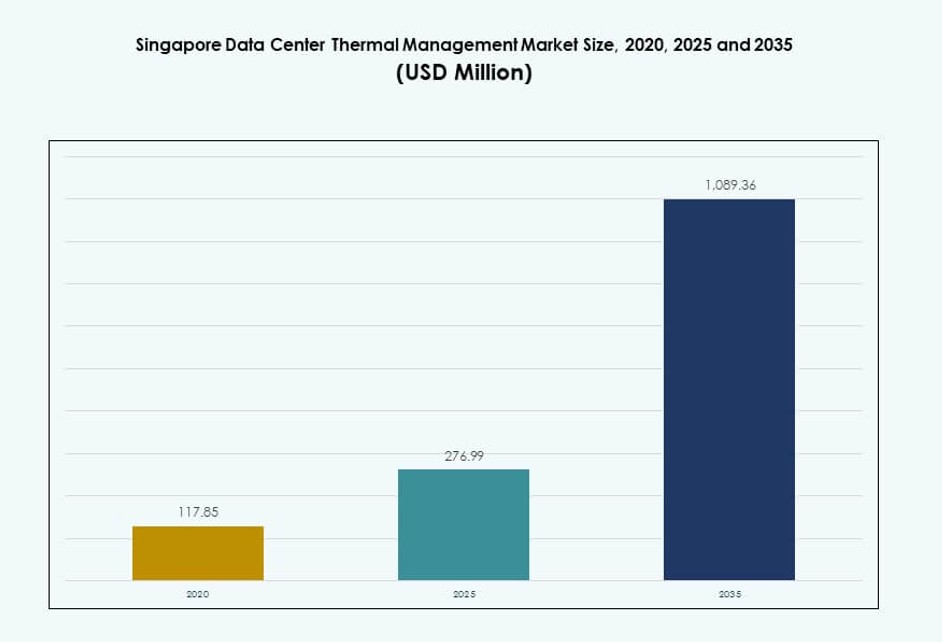

The Singapore Data Center Thermal Management Market size was valued at USD 117.85 million in 2020, grew to USD 276.99 million in 2025, and is anticipated to reach USD 1,089.36 million by 2035, at a CAGR of 14.57% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Singapore Data Center Thermal Management Market Size 2025 |

USD 276.99 Million |

| Singapore Data Center Thermal Netherlands Market, CAGR |

14.57% |

| Singapore Data Center Thermal Management Market Size 2035 |

USD 1,089.36 Million |

Growth in Singapore’s market is driven by rising AI, cloud, and hyperscale deployments that demand high-density server cooling. Companies are rapidly adopting liquid cooling, AI-driven automation, and smart building integrations to improve energy efficiency and sustainability. Regulatory mandates and digital economy policies are pushing for next-gen thermal systems, making innovation essential. The market holds strategic importance for global and regional investors seeking stable, high-return infrastructure assets. Businesses increasingly view efficient thermal management as key to uptime, ESG compliance, and future-readiness.

Central Singapore leads due to dense data center clusters in zones like Jurong and Changi, supported by top-tier connectivity and real estate. These zones attract hyperscale operators and multinational cloud providers, making them dominant. Peripheral areas such as Woodlands and Tuas are emerging, favored for land availability and industrial zoning. New developments in edge computing and urban micro data centers are also shaping localized thermal infrastructure growth.

Market Dynamics:

Market Drivers

Rising AI and GPU Workloads Driving Liquid Cooling and Dense Rack Thermal Efficiency Solutions

Singapore’s data center market is rapidly adapting to AI-driven workloads requiring dense server racks and high heat output. Thermal management systems must address cooling for racks exceeding 20–30 kW, especially for GPU-intensive computing. Traditional air-based systems no longer meet the efficiency standards, leading to demand for direct-to-chip and immersion cooling. The Singapore Data Center Thermal Management Market benefits from this shift, as operators prioritize efficiency and uptime. Regulatory frameworks supporting sustainability also encourage investment in low-PUE systems. Liquid cooling systems reduce energy waste and improve performance per square meter. Operators align cooling strategies with AI-readiness and ESG targets. Strategic investors treat thermal management as a key infrastructure layer for scaling AI and machine learning platforms.

- For instance, Digital Realty partnered with CoolestDC, a spin-off from the National University of Singapore, to pilot liquid cooling at its SIN11 facility. The trial demonstrated up to 29% reduction in power consumption compared to traditional air-cooled systems.

Sustainability Mandates and Green Data Center Policies Creating New Demand for Efficient Thermal Technologies

Singapore enforces stringent sustainability benchmarks, including Green Mark certifications and carbon neutrality goals for digital infrastructure. These policies push thermal management upgrades across legacy and new facilities. Operators must deploy systems with low water and energy usage, including evaporative cooling and closed-loop liquid systems. It strengthens the role of energy-efficient cooling in the Singapore Data Center Thermal Management Market. Enterprises and hyperscalers seek modular and retrofit-ready systems to meet ESG compliance. The market rewards technologies that deliver lower Power Usage Effectiveness (PUE) and support predictive maintenance. Smart controls and automation platforms are critical to meeting these expectations. Facility owners align thermal investments with long-term regulatory trajectories. Investors recognize thermal efficiency as a cost-control and branding advantage in Singapore’s competitive digital economy.

- For instance, a Singapore colocation provider retrofitted 114 CRAC units with Vertiv EC fans and Liebert iCOM controllers, extending unit lifespan by 7 years while achieving significant energy savings.

Government-Backed Infrastructure and Smart City Development Fuels High-Density Urban Edge Data Centers

Singapore’s Smart Nation initiative integrates digital infrastructure into city planning, creating a demand for compact, high-density edge facilities. These sites require highly localized thermal management due to limited space and urban heat. It drives adoption of row-based and rack-based cooling formats that reduce footprint and optimize airflow in tight server environments. The Singapore Data Center Thermal Management Market benefits from integration with national digital priorities. Government-backed projects, including 5G and AI clusters, create targeted demand for cooling innovation. Tier-3 and Tier-4 facilities prioritize cooling redundancy and fault-tolerant designs to meet service level agreements. Efficient heat dissipation enables urban hosting of latency-sensitive applications. Private-public collaboration strengthens demand for resilient cooling infrastructure aligned with national digital goals.

Private Cloud and Financial Sector Digitalization Expanding Enterprise Data Center Thermal Upgrades

Financial institutions and enterprises in Singapore are investing in private cloud environments, demanding advanced cooling for security and regulatory compliance. These workloads often run in secure, custom-built data centers that prioritize uptime and fault-tolerant infrastructure. It drives upgrades in thermal management systems to ensure resilience, efficiency, and performance. The Singapore Data Center Thermal Management Market sees strong momentum from BFSI and telecom sectors. These segments require cooling systems that support high IOPS, encryption, and transaction throughput. Upgrades include chilled water systems, airflow containment, and BMS integration. Cybersecurity and compliance pressures push firms to house sensitive data locally, creating stable demand for thermal infrastructure. Enterprise consolidation projects also drive retrofits with modern, energy-efficient thermal solutions.

Market Trends

Shift Toward AI-Driven Thermal Management Optimization Using Predictive Analytics and Smart Controls

Operators are integrating AI-based monitoring tools to regulate thermal systems in real time. These solutions analyze temperature fluctuations, rack load, and humidity to optimize airflow and fluid dynamics. Machine learning platforms enhance control systems, reducing overcooling and energy waste. The Singapore Data Center Thermal Management Market sees this trend as critical for uptime and sustainability. Predictive maintenance powered by AI prevents cooling system failures before they occur. Smart dashboards enable faster response during load spikes. Adaptive control logic adjusts fans and pumps based on actual IT usage rather than preset limits. Vendors offering embedded AI functions in cooling systems gain traction. AI-readiness becomes a differentiator in vendor selection.

Integration of Liquid Cooling Solutions in Rack and Row Systems for High-Density Compute Zones

Rack- and row-based cooling formats are increasingly integrating liquid systems to address localized heat zones. These formats offer efficient and compact cooling for high-performance racks, especially those supporting AI and advanced analytics. The Singapore Data Center Thermal Management Market shows rising adoption of rear-door heat exchangers and direct-to-chip cooling. Operators blend air and liquid strategies for hybrid environments. Row-based cooling improves response time in dynamic server deployments. Data centers use liquid-cooled racks to increase power density per square meter. Liquid solutions extend hardware lifespan and reduce thermal throttling. Retrofits enable liquid cooling adoption without major structural overhaul. Liquid-capable racks emerge as a standard in new facilities.

Surge in Demand for Retrofits and Modular Cooling Systems in Legacy Facilities

Many older facilities are upgrading to modern thermal technologies without complete overhauls. Modular cooling units allow integration with existing layouts and airflow paths. The Singapore Data Center Thermal Management Market captures this trend by offering scalable plug-and-play cooling systems. Operators replace outdated units with hot aisle containment and precision cooling. Retrofit demand is strong in enterprise and colocation segments. Modular systems reduce deployment time and upfront cost. Facility managers seek minimum downtime during installation. Scalable cooling systems match workload growth without over-provisioning. Flexibility becomes a key factor in buying decisions for thermal infrastructure.

Growth of CFD Simulation Tools and Digital Twins to Optimize Cooling Design in New Builds

New data center projects in Singapore incorporate advanced modeling tools to simulate cooling dynamics before construction. CFD (computational fluid dynamics) software helps identify airflow inefficiencies, hotspots, and thermal bottlenecks. The Singapore Data Center Thermal Management Market adopts digital twins to reduce trial-and-error in physical setups. Virtual models accelerate commissioning and design validation. Operators use simulations to select between hot-aisle, rear-door, or immersion configurations. Digital twins enable real-time adjustments post-launch. Design engineers collaborate with cooling vendors during early blueprint stages. Accurate modeling reduces cost overruns and improves thermal performance from day one. CFD-backed decisions also align cooling capacity with sustainability goals.

Market Challenges

Land Constraints and High Real Estate Costs Limit Large-Scale Cooling Infrastructure Deployment

Singapore’s limited land availability creates challenges in designing large-scale data centers with extensive cooling systems. High-density construction requires compact and efficient thermal solutions that fit within strict spatial limitations. The Singapore Data Center Thermal Management Market must balance performance with footprint. High real estate costs drive operators toward vertical cooling strategies and dense rack configurations. Cooling solutions must minimize noise and environmental footprint due to proximity to urban areas. Engineering complexity rises with hybrid and modular setups. System upgrades often require custom retrofits to adapt to small footprints. Overhead and raised floor space constraints further complicate airflow planning. Developers prioritize energy-efficient equipment that meets both spatial and functional constraints.

Water Usage Restrictions and Sustainability Regulations Limit Cooling Technology Choices

Singapore’s water conservation policies impact data centers using evaporative or water-cooled systems. Facilities must comply with environmental benchmarks and usage caps. The Singapore Data Center Thermal Management Market sees restrictions shaping cooling choices. Operators avoid water-heavy designs in favor of closed-loop systems. Liquid cooling adoption must align with water recycling and discharge controls. Regulatory pressure narrows the choice of thermal designs, especially in hyperscale projects. Some vendors face delays in approvals due to compliance concerns. Operators must invest in monitoring tools to report on water consumption. Balancing thermal efficiency with environmental goals remains a constant challenge in Singapore’s tightly regulated market.

Market Opportunities

Emergence of Liquid Cooling-as-a-Service and Vendor Partnerships for AI Infrastructure Support

Vendors offer managed thermal solutions that include deployment, monitoring, and lifecycle upgrades. These services reduce capex for operators and support AI-scale infrastructure. The Singapore Data Center Thermal Management Market sees this model as a growth engine. Strategic partnerships allow data centers to adopt complex cooling systems without managing them internally. This model also supports experimentation with immersion and chip-level cooling. Managed cooling services appeal to cloud, telecom, and edge facility owners.

New Government Incentives and Green Finance for Sustainable Cooling Infrastructure

Singapore’s green finance frameworks and tax benefits support investments in sustainable cooling. Operators pursuing Green Mark or BCA certifications gain access to financing. The Singapore Data Center Thermal Management Market benefits from policies that link performance with financial incentives. Cooling projects aligned with ESG targets attract private and institutional capital. This creates new investment channels for innovative thermal startups and suppliers.

Market Segmentation

By Data Center Size

Large data centers dominate the Singapore Data Center Thermal Management Market due to hyperscale deployments and high-density compute needs. Their scale demands advanced cooling systems such as liquid cooling and containment designs. Medium-sized data centers follow, often retrofitting with modular solutions. Small centers remain niche, focusing on specific applications like retail or edge computing.

By Cooling Technology

Air-based cooling, especially direct air and hot/cold aisle configurations, holds a large market share due to its long-standing use. Liquid-based cooling is growing rapidly, especially with direct-to-chip and immersion systems gaining popularity. Hybrid solutions that combine air and liquid methods are becoming preferred in high-density zones. Phase-change and thermoelectric remain niche technologies.

By Component

Hardware accounts for the largest share in the Singapore Data Center Thermal Management Market. Key investments go into chillers, heat exchangers, and fans. Software is rising with the adoption of AI optimization and BMS integration. Services like retrofitting, monitoring, and maintenance are growing due to facility expansion and ESG requirements.

By Hardware

Cooling units and chillers form the backbone of thermal infrastructure. Heat exchangers and airflow devices support both air and liquid systems. Piping and other components are essential in new builds and retrofits. Demand for high-efficiency units is driven by ESG benchmarks and space limitations in urban facilities.

By Software

AI optimization and CFD simulations lead the software segment. DCIM dashboards and BMS modules are crucial for integrated facility management. These tools support predictive analytics and energy efficiency tracking. Their use is critical in Tier-3 and Tier-4 data centers requiring high uptime and compliance.

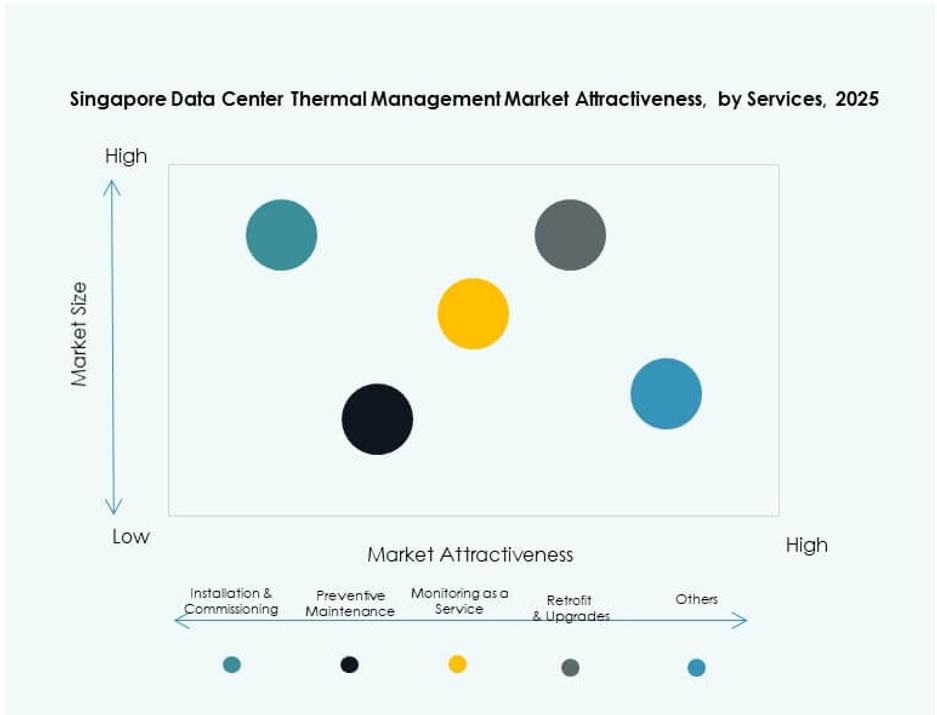

By Services

Preventive maintenance and retrofitting hold a dominant position, especially in enterprise and colocation facilities. Monitoring as a service is gaining adoption due to rising demand for performance visibility. Installation and commissioning services remain strong for greenfield and expansion projects.

By Data Center Type

Hyperscale and colocation/cloud data centers lead in thermal management demand. Enterprise data centers are investing in modernization and hybrid cooling systems. Edge and micro data centers are emerging, pushing compact and localized cooling innovations.

By Structure

Room-based cooling is widely deployed in traditional setups. However, rack-based and row-based structures are gaining share due to high-density demands and modular builds. Rack-based cooling is preferred in space-constrained environments, including edge deployments and AI data zones.

Regional Insights

Urban Core Zones Holding Largest Market Share with Over 55% Due to Density and Digital Economy Presence

Central Singapore, including Marina Bay, Jurong, and Changi zones, dominates with over 55% of the Singapore Data Center Thermal Management Market. These areas host major enterprise and hyperscale data centers. Their advanced digital infrastructure and connectivity attract global players. Urban zones require compact, low-noise thermal systems that meet sustainability standards. Real estate pressure leads to vertical cooling strategies and modular systems. This subregion shows consistent investment in AI and cloud-ready cooling facilities.

- For instance, ST Telemedia Global Data Centres (STT GDC) reported an 11.2% improvement in PUE across its portfolio since 2020, driven by air-cooling optimizations in tropical environments like Singapore. The company highlights its focus on efficient infrastructure tailored to high-humidity climates in regional operational reports.

Industrial and Periphery Areas Contributing Around 30% Share Driven by Emerging Hyperscale Clusters

Western and northern parts of Singapore, including Tuas and Woodlands, represent about 30% of the market. These locations offer lower land costs and power availability, attracting hyperscale investments. Facilities here adopt advanced thermal technologies like immersion and direct-to-chip cooling. The market sees strong government support for developing these zones into smart industrial hubs. Infrastructure upgrades support efficient cooling deployments at scale.

- For instance, Equinix’s SG3 data center in Tuas is a large-scale facility supporting high-density deployments and uses chilled water cooling systems. The site is engineered for energy efficiency and is certified under Singapore’s Green Mark program.

Edge and Emerging Micro Data Center Sites Account for 15% Market Share with Steady Growth

Edge and distributed computing zones across business parks and telecom exchanges form the remaining 15%. These locations support latency-sensitive applications and urban compute nodes. Growth is driven by demand for localized, compact, and smart-cooled systems. Vendors offer custom rack-based solutions and liquid-ready systems. The trend supports real-time applications in financial services, AI, and smart city deployments. This subregion will gain share as Singapore expands its digital urban infrastructure.

Competitive Insights:

- Schneider Electric

- Vertiv Group Corp.

- Daikin Industries Ltd.

- Delta Electronics, Inc.

- Trane Technologies plc

- Johnson Controls International plc

- Fujitsu Limited

- Airedale International Air Conditioning Ltd.

- Mitsubishi Electric Corporation

- ST Telemedia Global Data Centres

The Singapore Data Center Thermal Management Market features intense competition led by global players and regional infrastructure providers. It favors companies offering energy-efficient, compact, and AI-integrated solutions. Schneider Electric and Vertiv lead with diverse cooling portfolios covering air, liquid, and hybrid technologies. Daikin, Delta Electronics, and Trane Technologies maintain strong footholds through HVAC innovations and localized service networks. Fujitsu and Mitsubishi Electric bring advanced control systems and predictive maintenance capabilities. ST Telemedia and Keppel act as end-user innovators, integrating thermal systems across large-scale hyperscale and colocation builds. It rewards vendors that deliver low-PUE systems, modular scalability, and compliance with Singapore’s Green Mark standards. Partnerships, digital twin deployment, and immersion cooling projects remain key competitive differentiators.

Recent Developments:

- In October 2025, Johnson Controls launched its Silent-Aire Coolant Distribution platform, expanding thermal management solutions for high-density data centers, at Data Centre World Asia 2025 in Singapore.

- In October 2025, Carrier debuted its QuantumLeap thermal management suite, including liquid cooling and predictive services via the Abound platform, at a Singapore event.

- In October 2025, Ecolab Inc. introduced 3D TRASAR Technology for direct-to-chip liquid cooling in the Southeast Asia market, spotlighted in Singapore during Data Center World Asia.