Executive summary:

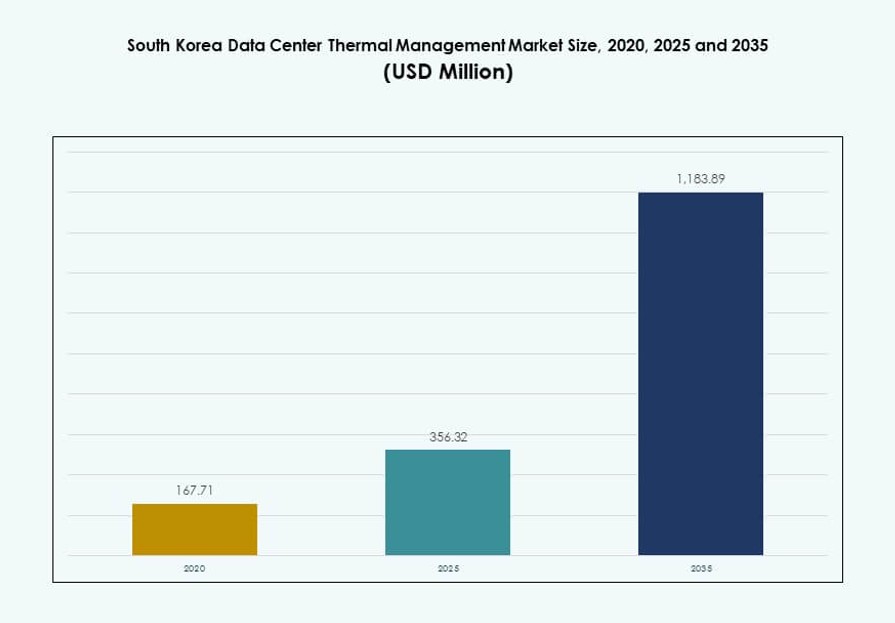

The South Korea Data Center Thermal Management Market size was valued at USD 167.71 million in 2020, increased to USD 356.32 million in 2025, and is anticipated to reach USD 1,183.89 million by 2035, at a CAGR of 12.67% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| South Korea Data Center Thermal Management Market Size 2025 |

USD 356.32 Million |

| South Korea Data Center Thermal Management Market, CAGR |

12.67% |

| South Korea Data Center Thermal Management Market Size 2035 |

USD 1,183.89 Million |

The market is driven by rising deployment of high-density AI and cloud workloads, which demand efficient and scalable thermal solutions. Operators are shifting toward liquid-based cooling, immersion systems, and AI-integrated control platforms to meet performance and energy goals. Innovation in predictive maintenance, digital twins, and thermal orchestration enhances system reliability. The South Korea Data Center Thermal Management Market plays a vital role in national digital infrastructure, offering long-term value for data-driven industries and infrastructure investors.

Seoul and Gyeonggi-do dominate the market due to hyperscale data center concentration, network connectivity, and favorable infrastructure. Busan and Gwangju are emerging as strategic hubs with large-scale data parks supported by industrial AI applications. Regions like Daejeon and Jeju show rising demand for edge cooling driven by smart cities and government IT needs. This geographic diversification strengthens resilience and boosts localized thermal solution deployments across the country.

Market Dynamics:

Market Drivers

Surging High-Density Workloads Requiring Advanced Cooling Integration Across Hyperscale and AI Data Centers

Rapid growth in AI, machine learning, and high-performance computing drives demand for high-density server environments. Hyperscale players like Naver and KT Cloud are expanding facilities with 30–60 kW per rack densities. These deployments require advanced thermal solutions beyond traditional CRAC/CRAH setups. Direct-to-chip liquid cooling, immersion, and hybrid heat rejection are becoming essential. The South Korea Data Center Thermal Management Market benefits from this shift, driven by strategic national digitalization plans. Businesses investing in AI workloads are prioritizing efficiency and thermal resilience. It encourages rapid adoption of energy-optimized thermal systems. Strong technology upgrades enhance cooling performance while reducing energy footprints.

- For instance, Naver’s GAK Chuncheon data center uses NAMU natural airflow cooling, requiring artificial cooling on only about 35 days per year. The system leverages ambient temperatures to maximize free cooling and minimize energy use.

Strategic Emphasis On Energy Efficiency, Sustainability, And Water Usage Optimization In Thermal Systems

Operators prioritize low PUE and WUE metrics to comply with ESG mandates and global reporting standards. Domestic players and global entrants are investing in closed-loop systems, adiabatic coolers, and evaporative-free alternatives. These systems minimize water consumption and energy usage while supporting rising thermal loads. It strengthens the South Korea Data Center Thermal Management Market as sustainability becomes a key differentiator for operators. Demand for software-integrated optimization tools is rising among eco-conscious facilities. Integration with renewable energy and carbon offset frameworks enhances infrastructure compliance. Energy-efficient thermal solutions offer long-term savings and investor appeal. This encourages infrastructure investment and upgrades across hyperscale and enterprise deployments.

National Investments In AI And Digital Infrastructure Fueling Large-Scale Greenfield Data Center Projects

South Korea’s government supports AI infrastructure and edge expansion through incentives, land allotments, and permitting support. New zones in Saemangeum, Busan, and Gwangju are earmarked for hyperscale data parks. These facilities are built with future-ready cooling frameworks from inception. The South Korea Data Center Thermal Management Market gains from integrated planning of thermal flows, automation, and energy controls. Vendors introducing smart cooling hardware gain early-mover advantages in project specifications. Cloud, fintech, and gaming sectors rely on data centers with thermal reliability. Strategic site selection emphasizes cooling system performance in high-humidity or coastal areas. Infrastructure developers view cooling innovation as a value creation tool.

- For instance, Samsung SDS’s Chuncheon disaster recovery facility features a modular design with a PUE of 1.2 and a gross floor area of 18,542 m². The rounded Y‑shaped exterior promotes natural airflow to support efficient cooling in the facility.

Digital Transformation In Healthcare, Finance, And Retail Driving Distributed And Modular Cooling Systems

Edge and micro data centers are expanding rapidly to support real-time computing needs in smart hospitals, autonomous transport, and e-commerce. These decentralized setups require scalable, rack-level thermal management with minimal space and water footprint. Compact cooling systems and modular liquid loop deployments are gaining adoption. The South Korea Data Center Thermal Management Market supports localized infrastructure with thermal agility. Growing workloads in Seoul’s tech corridors and regional Tier II cities diversify cooling needs. Businesses deploying edge nodes need efficient and easy-to-maintain thermal systems. Long-term contracts for modular thermal equipment are gaining traction. It strengthens vendor relationships and enhances return on investment.

Market Trends

Adoption Of Immersion Cooling Systems For AI-Driven Server Loads Across Tier I And Hyperscale Facilities

Immersion cooling is expanding in pilot and production phases, supporting ultra-high-density server clusters above 50 kW per rack. Korean operators view it as a viable strategy for AI models requiring high thermal envelopes. Cloud providers test single-phase and two-phase systems to evaluate footprint and operational savings. The South Korea Data Center Thermal Management Market sees strong OEM engagement in custom immersion tanks and dielectric fluids. Immersion enables better thermal stability, lower power usage, and reduced maintenance needs. Operators validate PUE improvements while aligning with green building standards. It allows flexible infrastructure design with minimal airflow restrictions. Long-term adoption depends on capex optimization and ecosystem readiness.

Widespread Use Of AI-Driven Thermal Management Software For Real-Time Cooling Optimization

AI-powered thermal software enables predictive load balancing, automated fan control, and fluid temperature tuning. Korean data centers deploy DCIM platforms with machine learning algorithms to reduce power draw and improve uptime. The South Korea Data Center Thermal Management Market benefits from digital twins and simulation tools driving operational insights. AI-driven platforms enable real-time alerts on airflow inefficiencies and thermal hotspots. It helps operators fine-tune cooling strategies with minimal human intervention. Software integration across BMS and DCIM allows centralized control and reporting. Developers and colocation providers adopt AI tools to maximize tenant satisfaction. Adoption accelerates for high-density AI and GPU-heavy environments.

Demand Surge For Rack-Based Cooling Units Supporting Dense IT Loads In Limited Floor Space

Rack-based thermal management is growing in compact facilities such as edge nodes and enterprise deployments. Operators select integrated rear-door cooling units, cold plate systems, and micro chillers for higher load per cabinet. The South Korea Data Center Thermal Management Market sees growth in custom-configured rack cooling tailored to specific workload types. Enterprises value solutions that provide thermal isolation without altering room-wide infrastructure. It enables targeted cooling, energy control, and faster deployment. Rack systems support greenfield and retrofit use cases with ease. Growth in high-frequency trading, genomics, and streaming accelerates demand. Vendors innovate to enhance serviceability and remote operability of these units.

Deployment Of Sustainable Heat Reuse Systems For District Heating And Circular Energy Integration

Operators explore heat reuse for external building heating, agriculture, and industrial applications. Heat exchangers and energy recovery units capture excess thermal output from servers. In the South Korea Data Center Thermal Management Market, players partner with local municipalities and real estate developers. It supports national carbon goals and reduces community heating costs. Smart campuses and eco-parks integrate data centers into circular heating ecosystems. Modular heat recovery units are being installed in new data center campuses. It provides additional revenue channels for operators. Sustainability-conscious hyperscale firms integrate these technologies in environmental strategies.

Market Challenges

High Capital Investment Requirements And Complex Regulatory Landscape For Advanced Cooling Deployments

Thermal technologies such as liquid cooling and AI-driven systems require significant upfront investment. Many local operators face challenges justifying ROI due to limited scale or legacy integration hurdles. The South Korea Data Center Thermal Management Market experiences delays in project approvals due to evolving zoning and environmental norms. Permitting complexities around water usage, emission limits, and grid interconnections affect deployment timelines. Thermal system retrofits in existing sites add to cost burdens. Smaller operators lack expertise in liquid loop designs or hybrid cooling. Financing institutions seek predictable thermal system KPIs before releasing funds. This slows market penetration for advanced technologies.

Talent Shortage And Infrastructure Gaps Restricting Adoption Of Liquid And Modular Cooling Technologies

There is a shortage of skilled thermal engineers and field technicians trained in liquid loop maintenance, immersion systems, or AI-based cooling. The South Korea Data Center Thermal Management Market suffers from limited availability of service providers outside Seoul. Edge deployments struggle to access reliable thermal support teams. Equipment localization remains a barrier, with many key components imported. Logistical issues in mountain or coastal zones further challenge delivery and serviceability. It creates reliance on a narrow pool of vendors and drives service costs higher. Knowledge gaps at enterprise client side also limit demand. These issues slow down ecosystem maturity and local manufacturing.

Market Opportunities

Edge Data Center Growth Across Logistics, Healthcare, And Smart Cities Fueling Compact Cooling Solutions

Edge computing investments are growing in regional logistics hubs, smart hospital campuses, and urban AI centers. Compact thermal systems that offer high-density cooling with minimal maintenance are in high demand. Vendors offering modular, easy-to-integrate cooling gain traction. The South Korea Data Center Thermal Management Market supports these deployments with rack-level systems. It enables faster rollouts for time-sensitive applications. Regional governments promote edge zones to decentralize capacity. Strategic investors seek asset-light cooling solutions for fast ROI.

Partnerships With Utility Providers And Real Estate Developers Enable Heat Reuse And Green Campus Models

Operators form strategic alliances with district heating companies and mixed-use real estate projects. It allows reuse of thermal waste from data centers for community heating or agricultural use. The South Korea Data Center Thermal Management Market benefits from smart campus planning. Thermal systems become part of integrated sustainability zones. It opens opportunities for innovation funding, brand visibility, and regulatory credits.

Market Segmentation

By Data Center Size

Large data centers dominate the South Korea Data Center Thermal Management Market, holding over 60% market share. Hyperscale and colocation players drive demand for high-capacity, multi-MW cooling infrastructure. Medium-sized centers follow, driven by finance, media, and healthcare IT workloads. Small facilities are growing in edge and enterprise segments but contribute a lower share due to scale limitations.

By Cooling Technology

Air-based cooling, especially hot/cold aisle and rear-door heat exchangers, remains dominant due to established infrastructure. Liquid-based cooling is the fastest-growing category, led by direct-to-chip and immersion systems in AI workloads. Hybrid cooling systems are emerging in new hyperscale projects. Thermoelectric and phase-change options remain niche, suited for micro data center use cases.

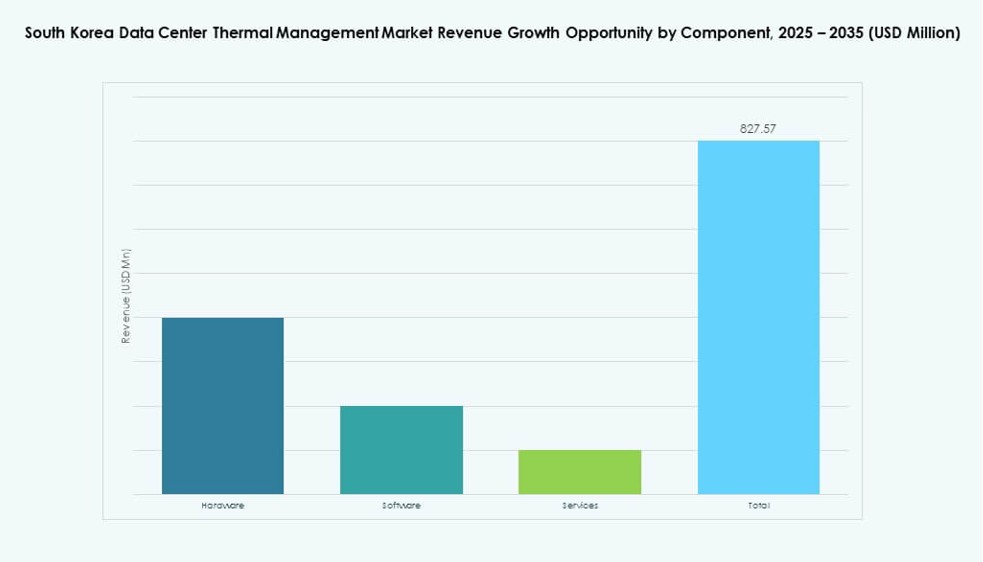

By Component

Hardware holds the largest share in the South Korea Data Center Thermal Management Market due to its capital-intensive nature. Services are gaining importance with increasing retrofits and remote monitoring needs. Software adoption is growing rapidly, especially in AI-optimized and BMS-integrated deployments that improve efficiency and reduce manual intervention.

By Hardware

Cooling units/chillers and heat exchangers dominate this category. Rear-door heat exchangers and direct liquid-cooled plates see rising deployment in new AI-heavy zones. Piping and distribution systems are crucial for supporting liquid infrastructure. Airflow devices are still important in room-based cooling setups. Other components include modular pump systems and thermal sensors.

By Software

AI optimization tools and CFD simulation software are growing fast, especially in new AI-driven and sustainable facilities. DCIM dashboards remain common across all data center sizes. BMS modules are essential for integration with facility-level controls. It helps achieve centralized management of thermal infrastructure with better operational efficiency.

By Services

Installation and commissioning services hold a leading share in greenfield projects. Preventive maintenance and retrofitting gain relevance in aging infrastructure. Monitoring-as-a-service offerings are gaining traction, especially for edge deployments. Thermal audit and design services are also growing among enterprise clients upgrading cooling systems.

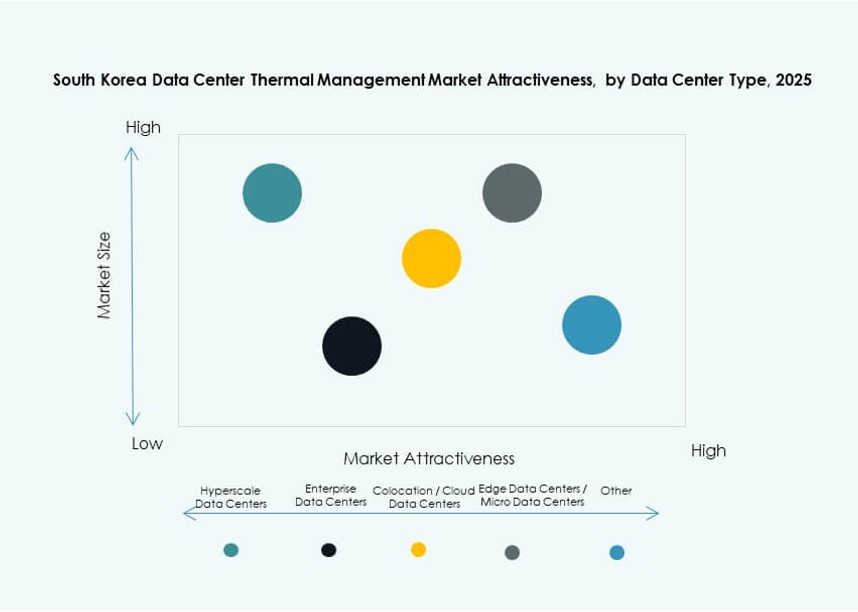

By Data Center Type

Hyperscale facilities dominate due to AI and cloud demand from firms like KT Cloud and Naver. Colocation/cloud facilities follow, serving small and mid-size enterprises. Edge/micro data centers are growing rapidly with logistics and healthcare applications. Enterprise data centers continue to hold steady demand for medium-scale thermal systems.

By Structure

Row-based and room-based setups dominate traditional deployments. Rack-based structures are growing quickly in edge and high-density zones. It enables modular cooling with compact footprint. Rack-level systems offer scalability for dynamic workloads, driving their adoption in new AI and HPC infrastructure across urban zones.

Regional Insights

Seoul Capital Region Leads With Over 65% Market Share Backed By Hyperscale Expansion And Digital Hubs

Seoul and Gyeonggi-do dominate the South Korea Data Center Thermal Management Market. The region houses the majority of hyperscale campuses, enterprise IT parks, and government-hosted infrastructure. High demand for AI and cloud services attracts both local and global thermal solution providers. It enables strong demand for air-based and liquid-cooled infrastructure. Regulatory alignment and grid availability favor further growth. It remains the innovation and investment core of the market.

- For instance, DCI commissioned its SEL01 data center in Seoul’s Gasan-dong district as a 20 MW facility. It marks the company’s first operational site in South Korea, supporting hyperscale and cloud clients.

Southern Industrial Belt Including Busan, Gwangju, And Ulsan Emerges As Strategic Secondary Zone

Busan and surrounding regions account for over 20% market share, supported by logistics and industrial AI applications. Land availability, coastal cooling advantages, and local government incentives drive growth. The South Korea Data Center Thermal Management Market benefits from rising hyperscale developments in Saemangeum. These zones are suitable for liquid and hybrid cooling models due to water and space access. It attracts greenfield investment and diversification away from Seoul.

- For instance, Hyundai E&C completed the Pacific Sunny Data Center in Yongin’s Jukjeon district, a large‑scale facility on a 99,125 m² site with a 64 MW IT load capacity and carrier‑neutral design. The center features high‑efficiency cooling and pre‑cooling systems that help achieve strong energy performance and operational stability.

Tier II Cities Like Daejeon, Daegu, And Jeju Account For Nearly 15% And Support Decentralized Edge Growth

Daejeon and Jeju are positioning themselves as digital infrastructure hubs. Data centers here serve smart healthcare, disaster recovery, and government cloud needs. The South Korea Data Center Thermal Management Market supports edge-oriented thermal innovation in these cities. Their geographical spread helps optimize latency for end-users. Investment-friendly policies and R&D collaborations foster cooling system pilots. It makes these regions attractive for edge-focused cooling vendors.

Competitive Insights:

- Mitsubishi Electric Corporation

- Daikin Industries Ltd.

- Delta Electronics, Inc.

- LG Electronics

- Samsung SDS

- Vertiv Group Corp.

- Schneider Electric

- Fujitsu Limited

- Johnson Controls International plc

- NTT Facilities

The competitive landscape in the South Korea Data Center Thermal Management Market shows strong presence of both global and domestic players competing on technology, service breadth, and integration capabilities. Leading firms focus on advanced liquid cooling, AI-driven thermal controls, and energy optimization features to win large hyperscale and enterprise contracts. Domestic brands leverage local partnerships and deep market knowledge to tailor solutions for regional data center needs. International vendors bring global best practices and robust R&D investments to support high-density cooling and sustainability goals. It drives price competition and accelerates product upgrades. Service portfolios that include predictive maintenance and remote thermal monitoring gain traction with large operators. Strategic alliances and localized manufacturing help companies secure long-term engagements. Competitive differentiation hinges on efficiency, reliability, and rapid deployment support.

Recent Developments:

- In November 2025, Mitsubishi Electric Corporation signed a memorandum of understanding (MoU) with Hon Hai Precision Industry (Foxconn) to form a global alliance supplying AI data center solutions, including thermal management systems.

- In September 2025, LG Electronicsand SK Innovation signed a memorandum of understanding (MOU) at the SK Seorin Building in Seoul to co-develop integrated energy and cooling solutions for AI data centers.