Executive summary:

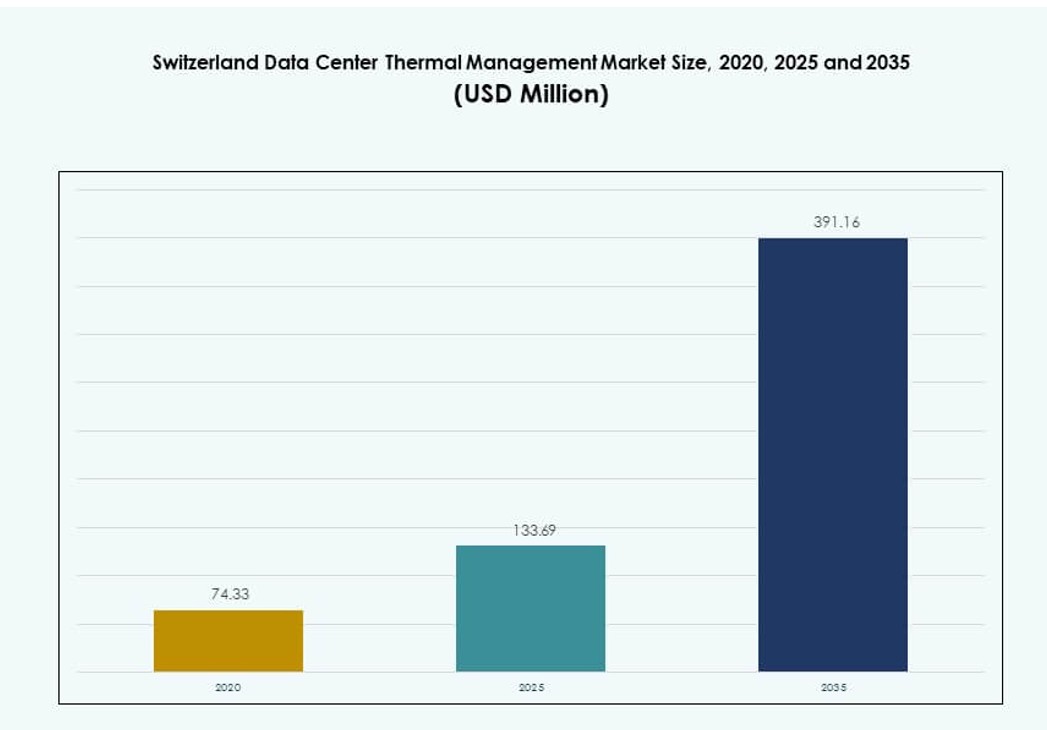

The Switzerland Data Center Thermal Management Market size was valued at USD 74.33 million in 2020, grew to USD 133.69 million in 2025, and is anticipated to reach USD 391.16 million by 2035, at a CAGR of 11.27% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Switzerland Data Center Thermal Management Market Size 2025 |

USD 133.69Million |

| Switzerland Data Center Thermal Netherlands Market, CAGR |

11.27% |

| Switzerland Data Center Thermal Management Market Size 2035 |

USD 391.16 Million |

Rising AI, big data, and HPC workloads are reshaping cooling demands, driving adoption of liquid-based and AI-optimized systems. Companies are investing in scalable and modular cooling to improve energy efficiency and meet ESG standards. Smart cooling, free cooling, and thermally intelligent infrastructure are becoming essential to reduce operating costs and carbon footprints. The market holds strategic importance for investors, with operators aligning thermal planning with long-term digital infrastructure expansion across enterprise and hyperscale environments.

Zurich leads the Switzerland Data Center Thermal Management Market due to its hyperscale density, financial sector demand, and low-latency connectivity. Geneva is emerging, supported by international organizations and a strong push for sustainability-led data center design. Basel, Lausanne, and Bern are developing edge and disaster recovery facilities. These secondary cities attract localized workloads, contributing to distributed infrastructure growth and reinforcing thermal system innovation across varied deployment scales.

Market Dynamics:

Market Drivers

Rapid Increase in High-Density Computing Workloads Necessitates Advanced Cooling Technologies

High-density workloads from AI, machine learning, and HPC environments strain existing cooling setups. Traditional air-based cooling systems are reaching efficiency limits in handling such heat loads. Operators are adopting liquid cooling, rear door heat exchangers, and chip-level thermal solutions. These technologies help ensure operational stability and lower failure risks in compact rack environments. Businesses prioritize thermal management to protect expensive servers from thermal throttling. The Switzerland Data Center Thermal Management Market benefits from this technological shift. Liquid-to-chip solutions gain traction among hyperscale and colocation operators. Efficient thermal systems extend server life and reduce energy costs. This development attracts strong capital flow toward next-gen cooling infrastructure.

- For instance, Supermicro’s liquid-cooled NVIDIA GB200 NVL72 SuperCluster supports 250 kW cooling capacity per rack with integrated coolant distribution units for 72 Blackwell GPUs. These technologies help ensure operational stability and lower failure risks in compact rack environments.

Surging Demand for Energy-Efficient Systems to Meet National and Corporate Sustainability Goals

Swiss enterprises aim to meet stringent energy regulations and corporate ESG commitments. Efficient cooling contributes heavily to Power Usage Effectiveness (PUE) targets. The market sees increased use of free cooling, evaporative systems, and AI-optimized thermal controls. Operators integrate renewable power sources with smart cooling management. These efforts enhance environmental performance and lower operational costs. Data center owners view thermal management upgrades as a strategic investment. It improves compliance while supporting green certifications. The Switzerland Data Center Thermal Management Market is central to sustainable infrastructure growth. Energy-aware cooling design drives long-term operational and branding benefits.

- For instance, Vertiv’s Liebert XDU 1450 kW coolant distribution unit delivers up to 1450 kW cooling capacity at a 5°C approach temperature for high-density racks in European data centers. Operators integrate renewable power sources with smart cooling management.

AI-Driven Automation and Software Integration Driving Smart Thermal Infrastructure

Software-defined infrastructure supports real-time thermal tracking and adaptive cooling. AI tools help monitor load fluctuations, heat distribution, and equipment performance. Intelligent systems automatically adjust airflow, fan speed, and coolant levels. Operators avoid overheating risks while reducing power draw and maintenance cycles. The Switzerland Data Center Thermal Management Market benefits from DCIM dashboards and CFD-based simulation models. These software modules offer predictive analytics and cost modeling. Enterprises value automation for its precision and control. Data center operators gain operational transparency and reduce human error. AI-enabled cooling ecosystems align with smart infrastructure strategies.

Strategic Investments in Hyperscale and Colocation Buildouts Elevate Thermal Infrastructure Needs

Hyperscale operators expand Swiss campuses to serve global and regional cloud demand. Colocation providers scale capacity to meet enterprise and content delivery workloads. Thermal design becomes integral during early construction and retrofit phases. Cold aisle containment, modular chillers, and scalable cooling units form the core design. These investments create sustained demand for thermal hardware and integrated services. The Switzerland Data Center Thermal Management Market aligns with the rapid growth of digital infrastructure. Investors fund thermal solutions as part of long-term value creation. Stakeholders prioritize thermal readiness for workload flexibility and uptime assurance.

Market Trends

Growth of Liquid-Based Cooling Adoption for Performance-Intensive Applications Across Data Centers

Liquid cooling gains adoption due to its superior thermal transfer and space-saving design. Direct-to-chip and immersion methods see uptake in AI, crypto, and research centers. Rear-door liquid systems balance cost and effectiveness for existing builds. It supports thermal management where traditional air cooling is no longer viable. The Switzerland Data Center Thermal Management Market sees a shift to modular liquid platforms. Vendors offer preconfigured units with scalable capacity. Energy savings and performance stability drive their preference. Liquid cooling also aligns with PUE and carbon goals in modern deployments. The technology sees strong support from both hyperscale and HPC operators.

Modular and Scalable Thermal Solutions Supporting Rapid Deployment and Edge Facility Growth

Operators prefer modular cooling designs to match dynamic capacity needs. Pre-integrated units reduce deployment time and minimize site disruption. Edge and micro data centers use compact cooling technologies with integrated control systems. Modular fans, chilled water units, and heat exchangers simplify infrastructure rollouts. The Switzerland Data Center Thermal Management Market supports such scalability demands. Developers value flexibility during capacity planning and site expansion. Modular solutions also enhance serviceability and reduce operational complexity. Edge deployment trends further strengthen this shift. Scalable thermal frameworks support speed-to-market for digital services.

Integration of AI Optimization Engines with Thermal Management Platforms for Intelligent Control

AI-driven platforms offer predictive temperature management and real-time adjustments. These tools reduce energy waste and optimize cooling based on workloads. CFD simulations improve airflow modeling and capacity planning. Integration with BMS systems enhances centralized control and remote monitoring. The Switzerland Data Center Thermal Management Market sees widespread use of AI in thermal dashboards. This software layer reduces technician burden and supports proactive failure mitigation. Intelligent engines enhance cooling ROI and asset longevity. AI adoption aligns with the industry’s push for autonomous data center operations. These platforms transform thermal infrastructure into intelligent ecosystems.

Rise in Demand for Sustainable Cooling Solutions Using Free Cooling and Renewable Integration

Swiss climate and altitude support ambient air cooling and indirect free cooling. Operators leverage environmental conditions to lower energy use. Some facilities use lake water or geothermal resources to manage heat. Hybrid cooling systems combine mechanical and natural methods for better efficiency. The Switzerland Data Center Thermal Management Market integrates sustainability into system design. Thermal management forms part of long-term green strategies. Clean cooling solutions attract ESG-focused investors and data-driven clients. Operators benefit from regulatory incentives and brand differentiation. Green thermal infrastructure becomes a competitive advantage.

Market Challenges

Infrastructure Compatibility and Retrofitting Complexity in Existing Data Centers

Legacy data centers were designed around traditional air-cooled architectures. Retrofitting advanced cooling systems in such facilities poses structural and operational risks. Space constraints limit the deployment of liquid-based systems and modular chillers. Downtime for installation disrupts service-level commitments, raising concerns for operators. The Switzerland Data Center Thermal Management Market faces challenges in older enterprise builds. System integration with existing BMS and power layouts adds further complexity. Cost concerns delay upgrades even when energy savings are evident. Operators must balance modernization goals with risk management. Gradual retrofits and hybrid solutions offer partial relief but extend timelines.

High Capital Cost of Advanced Thermal Management Technologies for Emerging Operators

Adoption of cutting-edge thermal technologies involves significant upfront investment. Liquid cooling, AI-powered systems, and modular platforms carry higher procurement and deployment costs. Smaller data centers and new entrants struggle to justify such capital outlays. While operational savings exist, long ROI periods hinder quick adoption. The Switzerland Data Center Thermal Management Market sees entry barriers for smaller players. Without subsidies or leasing models, financial constraints slow market penetration. High cost of imported thermal components adds to the challenge. Financial flexibility becomes a decisive factor in tech selection. This limits market democratization and innovation scaling.

Market Opportunities

Growing Role of AI, Big Data, and HPC Workloads Creating Demand for Specialized Cooling Systems

AI, analytics, and high-performance computing create intense thermal loads per rack. These environments require advanced cooling systems with real-time thermal tuning. Liquid cooling and direct-to-chip designs address these demands. The Switzerland Data Center Thermal Management Market supports such workloads with robust infrastructure. Data centers designed for AI workflows present a long-term opportunity for thermal system providers. Vendors offering precision-focused systems stand to gain from this demand cycle.

Sustainability-Focused Infrastructure Investments Unlock New Thermal Innovation and Deployment Models

Green data center design creates scope for sustainable thermal solutions. Free cooling, lake water systems, and low-GWP refrigerants gain traction. Operators seek thermal management that supports ESG benchmarks. The Switzerland Data Center Thermal Management Market aligns with Switzerland’s strong renewable energy commitments. Innovation in thermoelectric and phase-change systems could tap this shift. Energy-efficient cooling becomes a lever for both regulatory compliance and investor interest.

Market Segmentation

By Data Center Size

Large data centers dominate the Switzerland Data Center Thermal Management Market due to hyperscale and colocation growth. These facilities require high-capacity and scalable cooling systems. Medium-sized centers follow with moderate adoption of intelligent cooling. Small data centers use basic air cooling, often lacking advanced features. The market focuses on large centers for ROI and energy efficiency. Most innovation occurs in this segment due to workload intensity and heat density.

By Cooling Technology

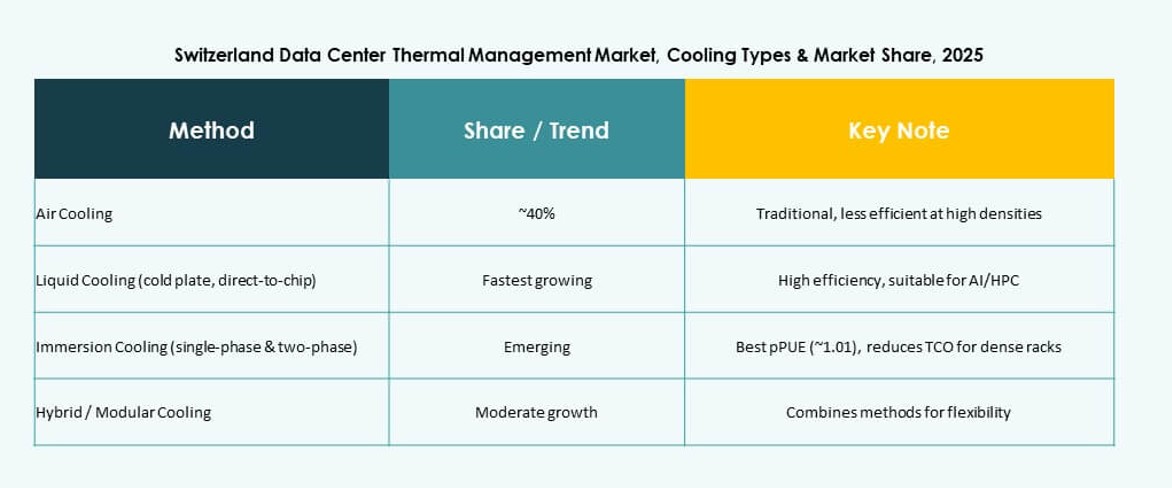

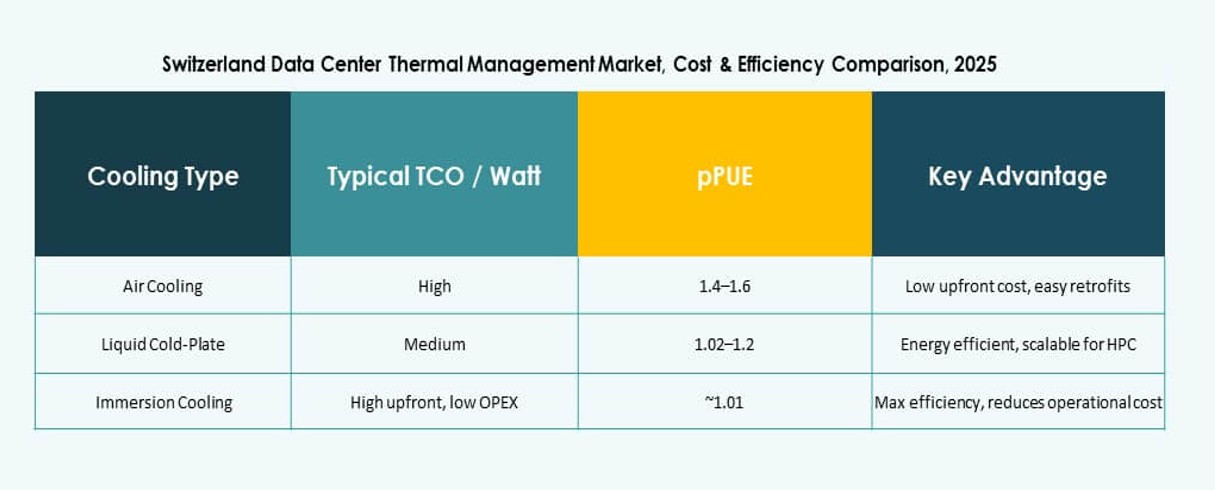

Air-based cooling holds a strong presence due to simplicity and cost-effectiveness. Hot/cold aisle containment and rear-door heat exchangers see broad use. Liquid-based cooling grows rapidly for AI and HPC applications. Direct-to-chip and immersion cooling attract high-density deployments. Hybrid systems offer balanced performance for mixed workloads. The Switzerland Data Center Thermal Management Market shows strong growth in hybrid adoption due to flexibility and modularity.

By Component

Hardware dominates the market by revenue due to demand for chillers, fans, and exchangers. Software grows in importance with AI, DCIM, and CFD models gaining ground. Services are essential for system integration, maintenance, and upgrades. The market shows strong bundling trends with end-to-end offerings. Vendors often combine hardware with AI dashboards or managed service contracts. This integrated approach improves efficiency and customer retention.

By Hardware

Cooling units and chillers lead the segment with high usage across all data center sizes. Piping, airflow devices, and exchangers support custom cooling topologies. Rear-door heat sinks and smart fans gain share in retrofitting projects. High-performance cooling units feature in hyperscale deployments. The Switzerland Data Center Thermal Management Market prioritizes energy efficiency and heat removal in hardware procurement. System lifespan and modularity influence purchasing decisions.

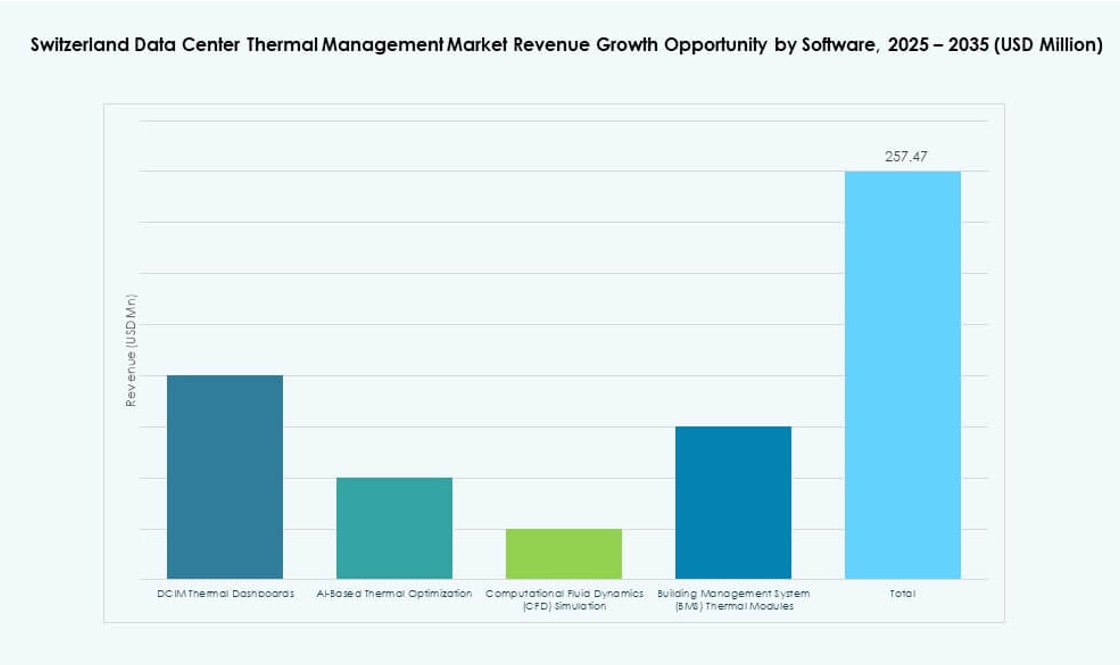

By Software

AI optimization software shows the fastest growth in thermal management platforms. DCIM dashboards provide visual tracking and alerts. CFD simulation tools aid layout design and airflow modeling. BMS modules link thermal performance with broader facility management. The market sees growing demand for integrated thermal monitoring across all scales. Predictive controls help lower PUE and manage performance under variable workloads.

By Services

Installation and commissioning remain critical, especially in new greenfield projects. Preventive maintenance ensures uptime and thermal efficiency. Monitoring-as-a-service and remote diagnostics gain momentum with AI integration. Retrofit and upgrade services support legacy system transitions. The Switzerland Data Center Thermal Management Market emphasizes service flexibility and performance contracts. Vendors who offer rapid response and predictive maintenance gain customer preference.

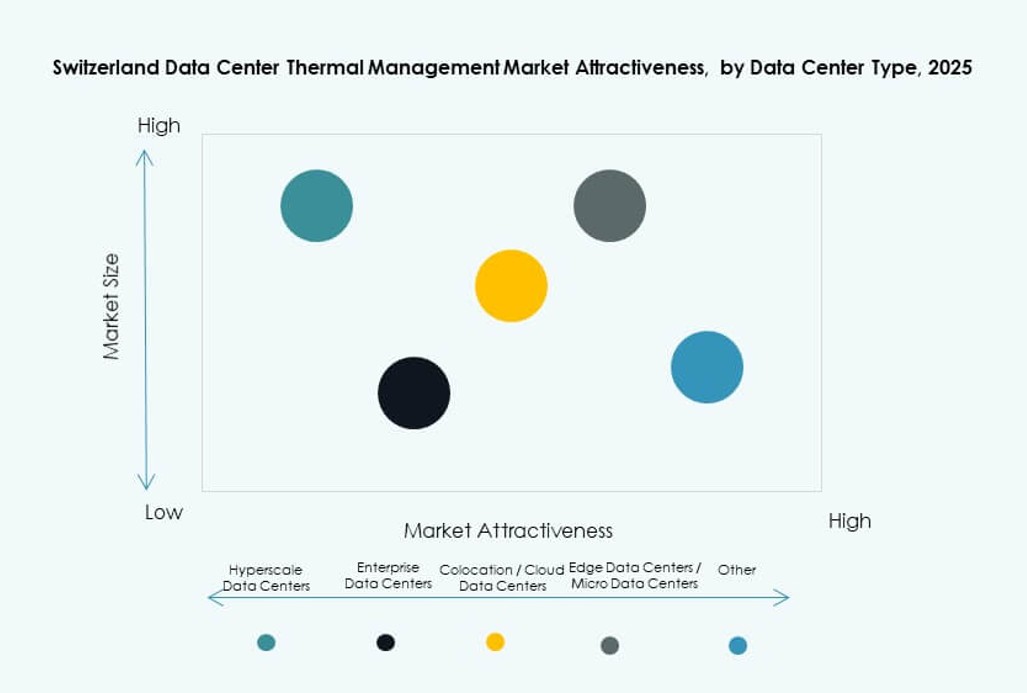

By Data Center Type

Hyperscale data centers dominate due to large-scale deployments from global cloud providers. Colocation and cloud facilities follow with tailored cooling requirements. Edge and micro data centers adopt compact systems for regional workloads. Enterprise deployments include hybrid cooling with IT infrastructure modernization. The market focuses on hyperscale and cloud segments due to investment inflow and workload diversity. Scalability and energy efficiency drive vendor selection.

By Structure

Room-based systems are common in older facilities but see declining share. Row- and rack-based cooling gain share with modular and dense workloads. Row-based systems support flexible deployment across expanding footprints. Rack-based cooling aligns with liquid and direct-to-chip setups. The Switzerland Data Center Thermal Management Market trends toward rack-based solutions for AI and high-density servers. Space optimization and thermal precision drive structural preference.

Regional Insights

Zurich Region Leads with Largest Market Share Due to Hyperscale and Financial Sector Growth

Zurich accounts for over 45% of the Switzerland Data Center Thermal Management Market. Hyperscale campuses, banking infrastructure, and cloud deployments fuel growth in this region. Global firms prefer Zurich for regulatory stability and connectivity. The city supports strong colocation activity with low-latency network hubs. Investors back thermal infrastructure to support long-term operational performance. Efficient cooling remains essential due to space limitations and dense rack configurations.

- For instance, Green Datacenter’s Zurich West campus features redundant cooling systems achieving a PUE of 1.19 across 10,000 m² of data center space with up to 25 kW per rack. Global firms prefer Zurich for regulatory stability and connectivity.

Geneva Region Emerges as a Key Secondary Market with International Organization Presence

Geneva contributes around 25% of the market, driven by global institutions and intergovernmental data needs. Its bilingual culture and proximity to France enhance regional digital activity. International NGOs and enterprises invest in green, secure facilities. The region supports renewable cooling strategies and integration with lakewater systems. Geneva’s growth reinforces decentralized infrastructure deployment. The thermal systems market responds with modular and sustainable designs.

- For instance, Infomaniak’s D4 data center in Geneva reuses waste heat for district heating with sustainable operations emphasizing zero water consumption in cooling. International NGOs and enterprises invest in green, secure facilities.

Basel, Lausanne, and Bern Contribute Remaining Share with Edge and Enterprise Deployments

The combined share of these regions stands at around 30%. Basel leads among them due to pharmaceutical and research-driven IT demands. Lausanne supports edge deployments due to academic and startup ecosystems. Bern hosts government digital infrastructure and enterprise builds. The Switzerland Data Center Thermal Management Market benefits from region-specific workloads and zoning flexibility. These areas gain importance in edge computing and disaster recovery planning. Thermal innovation follows distributed infrastructure trends.

Competitive Insights:

- Vertiv Group Corp.

- Mitsubishi Electric Corporation

- Daikin Industries Ltd.

- Johnson Controls International plc

- Delta Electronics, Inc.

- Trane Technologies plc

- Airedale International Air Conditioning Ltd.

- Asetek, Inc.

- Eaton Corporation

- Huawei Technologies Co., Ltd.

The competitive landscape of the Switzerland Data Center Thermal Management Market shows a mix of global HVAC leaders and specialized thermal technology vendors. Vertiv and Mitsubishi Electric hold strong positions through broad portfolios and deep service networks. Daikin and Johnson Controls drive adoption with energy-efficient chillers and controls. Delta Electronics and Trane deliver integrated power and cooling solutions. Asetek and Airedale focus on high-performance liquid cooling for dense workloads. Eaton and Huawei strengthen offerings with infrastructure components and digital management tools. Companies compete on energy efficiency, reliability, and service support. Partnerships and localized service hubs help firms meet stringent Swiss performance and sustainability norms. Competitive differentiation stems from innovation, rapid deployment, and tailored thermal solutions for hyperscale, colocation, and enterprise data centers.

Recent Developments:

- In December 2025, Trane Technologies plc entered a definitive agreement to acquire Stellar Energy Digital, a provider of turnkey liquid-to-chip cooling solutions for data centers. The acquisition strengthens Trane’s position in high-efficiency thermal management for mission-critical environments.

- In November 2025, NorthC Data Centers (Switzerland) AG and Legrand Switzerland AG announced a collaboration involving the deployment of advanced cooling solutions at NorthC’s AI-enabled data center infrastructure in Münchenstein, Switzerland.

- In May 2025, Nortek Air Solutions, LLC unveiled StatePoint 2025, a hybrid cooling plant integrating pumps, cooling towers, dry coolers, and heat exchangers for large-scale data centers. This update reduces total cost of ownership and simplifies deployment on a smaller footprint, supporting AI workloads with scalability.

- In March 2025, R&M (Reichle & De-Massari) officially announced the expansion of its infrastructure partner program to include a global collaboration with STULZ GmbH.

- In January 2025, Mitsubishi Electric Corporation acquired Crystal Air Holdings Limited via its European subsidiary to bolster IT cooling services for data centers across Europe. The deal enhances one-stop solutions including air-conditioning sales, installation, operation, and maintenance amid rising demand from AI and IoT growth.