Executive summary:

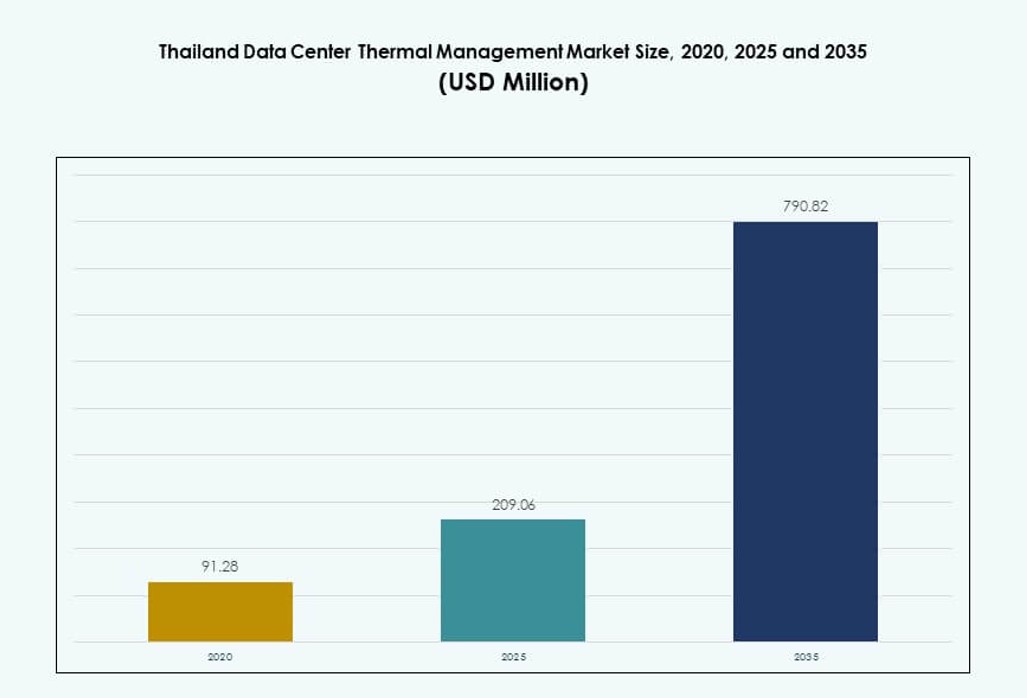

The Thailand Data Center Thermal Management Market size was valued at USD 91.28 million in 2020 to USD 209.06 million in 2025 and is anticipated to reach USD 790.82 million by 2035, at a CAGR of 14.13% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Thailand Data Center Thermal Management Market Size 2025 |

USD 209.06 Million |

| Thailand Data Center Thermal Netherlands Market, CAGR |

14.13% |

| Thailand Data Center Thermal Management Market Size 2035 |

USD 790.82 Million |

Rising digital transformation, growing hyperscale deployments, and increasing AI computing loads are reshaping cooling demands in Thailand’s data centers. Operators are shifting toward liquid-based and hybrid cooling technologies to manage higher rack densities. Adoption of AI-powered DCIM tools and smart thermal analytics is improving operational efficiency. Businesses prioritize sustainability, leading to demand for energy-efficient systems with low PUE. Strategic investment in modular and scalable cooling designs supports long-term growth. The market holds strong potential for vendors offering innovative, high-performance thermal systems. For investors, it provides exposure to Thailand’s digital infrastructure expansion and energy optimization strategies.

Bangkok leads the market due to its dense concentration of hyperscale, enterprise, and colocation facilities. Strong connectivity, power availability, and government-backed infrastructure drive investment in the capital region. The Eastern Economic Corridor is emerging as a secondary hub, supported by land availability and digital economy incentives. Northern and outlying regions are witnessing growth in edge data centers driven by enterprise and telecom demand. This regional spread reflects Thailand’s broader push for digital decentralization and infrastructure resilience.

Market Dynamics:

Market Drivers

Rising Digitalization and Cloud Growth Driving Demand for Advanced Thermal Systems

Thailand’s digital economy is growing rapidly with rising demand for cloud, AI, and digital services. This is triggering high-density server deployments and larger data center footprints across metro areas. The Thailand Data Center Thermal Management Market is evolving to support this shift with scalable, energy-efficient cooling technologies. Businesses seek modular cooling units and automation-driven systems to ensure reliability and cost-efficiency. Demand for low-latency infrastructure is pushing hyperscalers to expand within the country. New facility launches are increasingly designed with thermal optimization at their core. Efficient thermal management reduces power consumption and improves uptime. Investors view this market as a critical enabler of digital infrastructure readiness. The long-term outlook remains strong for vendors offering scalable and smart cooling solutions.

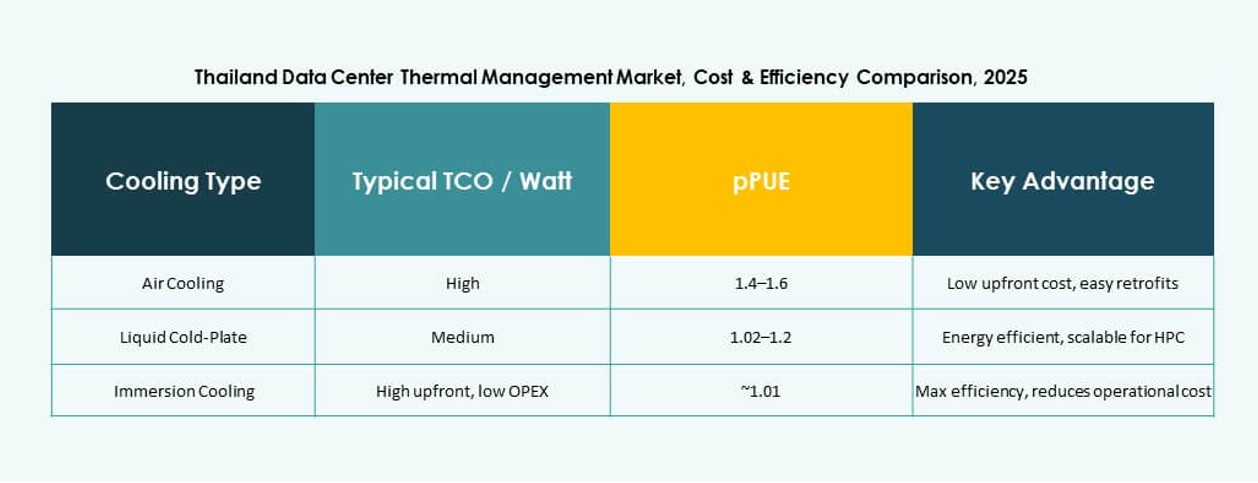

Increased Adoption of Liquid and Hybrid Cooling Technologies for AI and HPC Loads

AI workloads and high-performance computing are placing greater thermal stress on racks and GPUs. Air cooling no longer supports the thermal requirements of dense, high-power setups. It drives the adoption of liquid-based and hybrid cooling technologies across newer data centers. Liquid-to-chip and immersion cooling are gaining traction among operators running AI models. The Thailand Data Center Thermal Management Market benefits from this shift in cooling approach. Data center operators require systems that maintain low power usage effectiveness (PUE) while supporting rack densities above 40 kW. Vendors offering integration with existing infrastructure gain an edge. Enterprises are now prioritizing systems that align with ESG goals. This technological shift creates long-term growth opportunities for specialized cooling providers.

- For instance, Vertiv’s Liebert XDU1350 liquid cooling system delivers 1,350 kW of heat removal using a liquid-to-liquid heat exchanger, supporting rack densities exceeding 60 kW and deployed by hyperscalers and colocation providers in AI and HPC clusters across Asia to retrofit air-cooled halls without major structural changes.

Regulatory Focus on Energy Efficiency and Environmental Impact Promoting Thermal Innovation

Thailand is aligning with global environmental standards by tightening efficiency norms for power and cooling. New energy codes and PUE thresholds are emerging for commercial data centers. The Thailand Data Center Thermal Management Market must adapt to stricter mandates on sustainability and water usage. Cooling vendors are investing in eco-friendly refrigerants, closed-loop cooling, and free cooling where feasible. Businesses are tracking WUE and PUE as core metrics tied to compliance. These norms shape procurement decisions and guide capital investment. Smart monitoring systems using AI and DCIM platforms are being deployed to ensure real-time performance tracking. Regulators and utilities are working to incentivize low-impact cooling upgrades. This makes thermal efficiency a strategic factor for facility planning and retrofitting.

- For instance, Google’s data centers reported a global average PUE of 1.10 in 2023, achieved through AI-optimized air and liquid cooling systems, including closed-loop designs that reduce water usage in several Asia-Pacific facilities.

Strategic Location and Infrastructure Readiness Making Thailand a Regional Digital Hub

Thailand’s geographic position, robust fiber backbone, and reliable power infrastructure attract hyperscalers and colocation players. New submarine cable projects and regional interconnectivity improve its appeal for global digital infrastructure. The Thailand Data Center Thermal Management Market gains from the rise in domestic and international investments. Bangkok and Eastern Economic Corridor (EEC) zones are becoming hotspots for greenfield data centers. Operators view thermal management not only as an operational concern but also as a differentiator in service-level agreements. This creates demand for high-efficiency chillers, smart airflow control, and adaptive AI modules. These developments boost investor confidence and trigger long-term infrastructure commitments. The market is evolving into a key enabler for digital transformation and regional cloud expansion.

Market Trends

Shift Toward AI-Optimized Thermal Management Through Predictive Monitoring and Control

The adoption of AI-based cooling control systems is becoming central to reducing energy waste. Smart cooling platforms are being deployed to optimize temperatures based on live IT loads. The Thailand Data Center Thermal Management Market is shifting toward predictive models that learn from thermal patterns. These platforms enable operators to respond faster to workload fluctuations and avoid hot spots. Vendors are integrating AI modules into BMS and DCIM platforms to improve visibility. Demand for cooling automation is rising in Tier III and IV facilities. Predictive analytics improve operational uptime and reduce maintenance needs. Companies deploying AI-based cooling see measurable improvements in PUE. This trend is setting new standards for intelligent data center management.

Deployment of Rack-Based and Row-Based Thermal Management in Edge and Modular Builds

Modular and edge data center designs require localized and efficient thermal systems. Rack-based and row-based cooling units are gaining traction in smaller footprints and micro-edge deployments. The Thailand Data Center Thermal Management Market is witnessing a design shift toward compact, scalable solutions. Operators are integrating cooling directly into racks to cut latency and energy waste. Row-based systems help control airflow precisely in modular zones. These technologies reduce space consumption and improve cooling redundancy. Growth in IoT and remote work applications increases demand for edge sites with efficient cooling. Vendors focusing on plug-and-play solutions see strong adoption in emerging use cases. This trend supports a lean and distributed digital infrastructure strategy.

Increasing Adoption of Direct-to-Chip and Immersion Cooling in AI-Heavy Deployments

With GPU-based processing loads rising, direct-to-chip and immersion cooling are becoming more practical. High-density environments now demand these approaches to keep hardware within thermal limits. The Thailand Data Center Thermal Management Market is adapting to accommodate cooling solutions capable of 50–70 kW per rack. Direct-to-chip systems enable targeted thermal removal at chip level with high precision. Immersion cooling provides superior performance for extreme-density deployments. Operators deploying AI, analytics, and blockchain workloads adopt these technologies for long-term efficiency. Facilities retrofitting legacy systems are also evaluating these options for improved sustainability. These methods reduce the need for external chillers and air handlers. Adoption of liquid cooling continues to redefine thermal design standards.

Emergence of CFD-Driven Cooling Layouts for Enhanced Heat Distribution Optimization

Computational Fluid Dynamics (CFD) modeling is reshaping how thermal layouts are designed and validated. Data center operators are simulating airflow paths and heat zones before physical buildouts. The Thailand Data Center Thermal Management Market benefits from widespread use of CFD tools in new and retrofit projects. These models optimize equipment placement, airflow direction, and containment structures. Vendors offering simulation-backed design consulting see greater market traction. CFD use reduces trial-and-error during commissioning and speeds up ROI. It also improves compliance with PUE and green building certifications. Data centers now use CFD to plan future expansion without compromising thermal performance. This trend reflects the growing demand for data-driven infrastructure planning.

Market Challenges

High Capital Expenditure for Liquid and Hybrid Cooling Technologies Across Legacy Sites

Adoption of advanced thermal systems demands significant upfront investment, especially for older facilities. Retrofitting legacy rooms to support liquid or hybrid cooling often involves structural and electrical upgrades. The Thailand Data Center Thermal Management Market faces barriers due to cost-intensive installation requirements. Many small and medium operators are hesitant to adopt newer systems due to long payback periods. Return on investment depends heavily on workload density and energy prices. High-end cooling systems also require skilled maintenance teams and specialized training. Without robust incentives or government support, penetration of next-gen cooling remains limited in certain segments. Cost sensitivity across enterprise and colocation providers restricts rapid modernization. This challenge slows down industry-wide transition to low-PUE designs.

Limited Local Supply Chain and Technical Workforce for High-End Thermal Systems

The market suffers from a shortage of domestic manufacturers and thermal technology providers. Most liquid and hybrid cooling solutions depend on imports and integration partners. The Thailand Data Center Thermal Management Market is impacted by delays in parts procurement and limited local expertise. Skilled engineers capable of deploying and maintaining advanced systems are in short supply. High-performance liquid cooling setups require advanced knowledge in fluid dynamics, electronics, and redundancy planning. Training gaps among facility teams hinder system performance and risk uptime. OEMs and global vendors face logistical and installation delays, especially in remote areas. This supply gap restricts widespread adoption of cutting-edge solutions and affects rollout timelines.

Market Opportunities

Rising Demand from Hyperscale and AI-Focused Data Centers Expanding Regional Presence

Global hyperscale and AI-focused companies are expanding into Thailand to build next-gen facilities. It creates strong demand for high-performance thermal systems that meet large-scale IT loads. The Thailand Data Center Thermal Management Market will benefit from hyperscalers needing sustainable, scalable cooling. Opportunity lies in offering modular, liquid-based, and hybrid systems customized for Tier III and IV designs. Service providers offering installation, retrofits, and maintenance for high-density workloads will also see long-term growth.

Public and Private Sector Push for Energy-Efficient Infrastructure Driving Green Thermal Adoption

The Thai government is encouraging efficient energy usage and sustainability in digital infrastructure. It opens opportunities for vendors offering cooling solutions that reduce water and power usage. The Thailand Data Center Thermal Management Market will benefit from policies supporting renewable-backed and green-certified facilities. Local players adopting eco-friendly systems can also attract investment from ESG-focused funds and partners.

Market Segmentation

By Data Center Size

Large data centers dominate the Thailand Data Center Thermal Management Market, supported by hyperscale and colocation growth. Their extensive rack count and higher IT loads require efficient thermal control systems. Medium facilities are gaining share as enterprise demand increases. Small data centers, often at the edge or within campuses, see adoption of compact, modular cooling units. Growth across all sizes is driving demand for flexible and scalable cooling solutions.

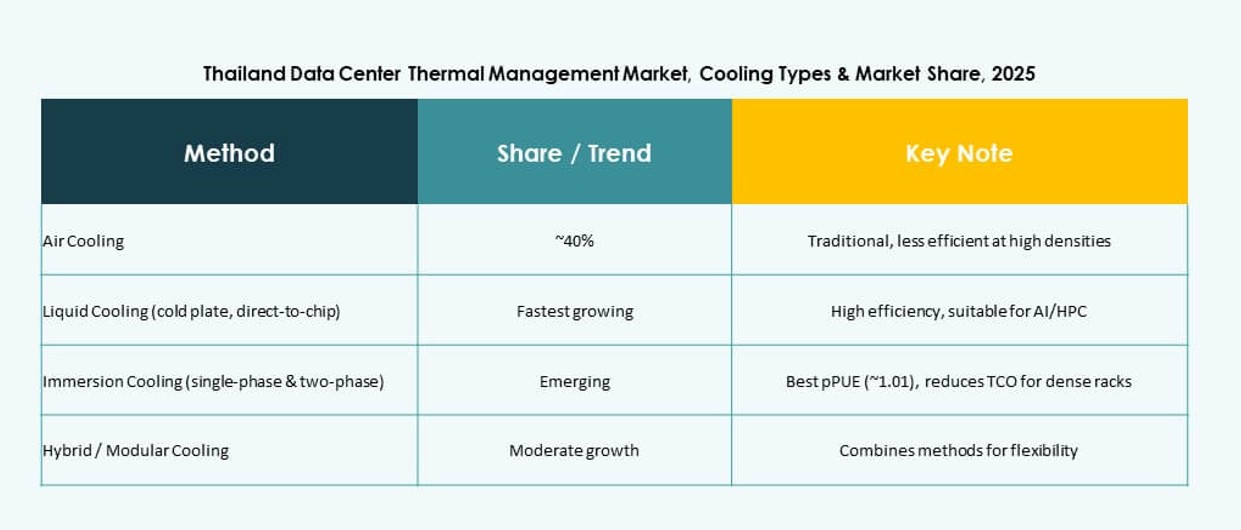

By Cooling Technology

Air-based cooling continues to hold a large share, particularly using hot/cold aisle configurations. However, liquid-based cooling—especially direct-to-chip and immersion—has gained traction for AI-heavy deployments. Hybrid systems are emerging as a preferred solution in mixed-load environments. Rear door liquid and air exchangers are also used in dense rack setups. The Thailand Data Center Thermal Management Market is evolving to support this multi-tech ecosystem.

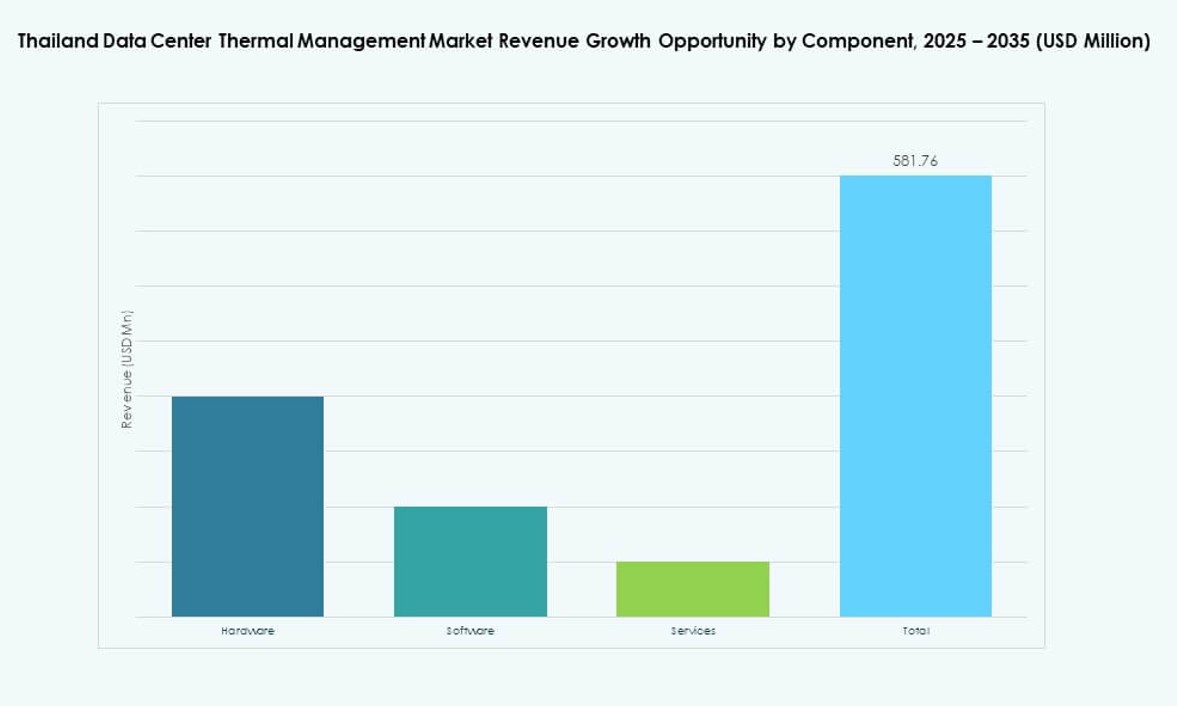

By Component

Hardware leads in revenue contribution with high demand for chillers, airflow systems, and heat exchangers. Software is gaining share with growing use of DCIM, AI, and CFD tools. Services are crucial for lifecycle management, especially for retrofits, predictive maintenance, and monitoring. Vendors offering integrated service + hardware models are well-positioned in the Thailand Data Center Thermal Management Market.

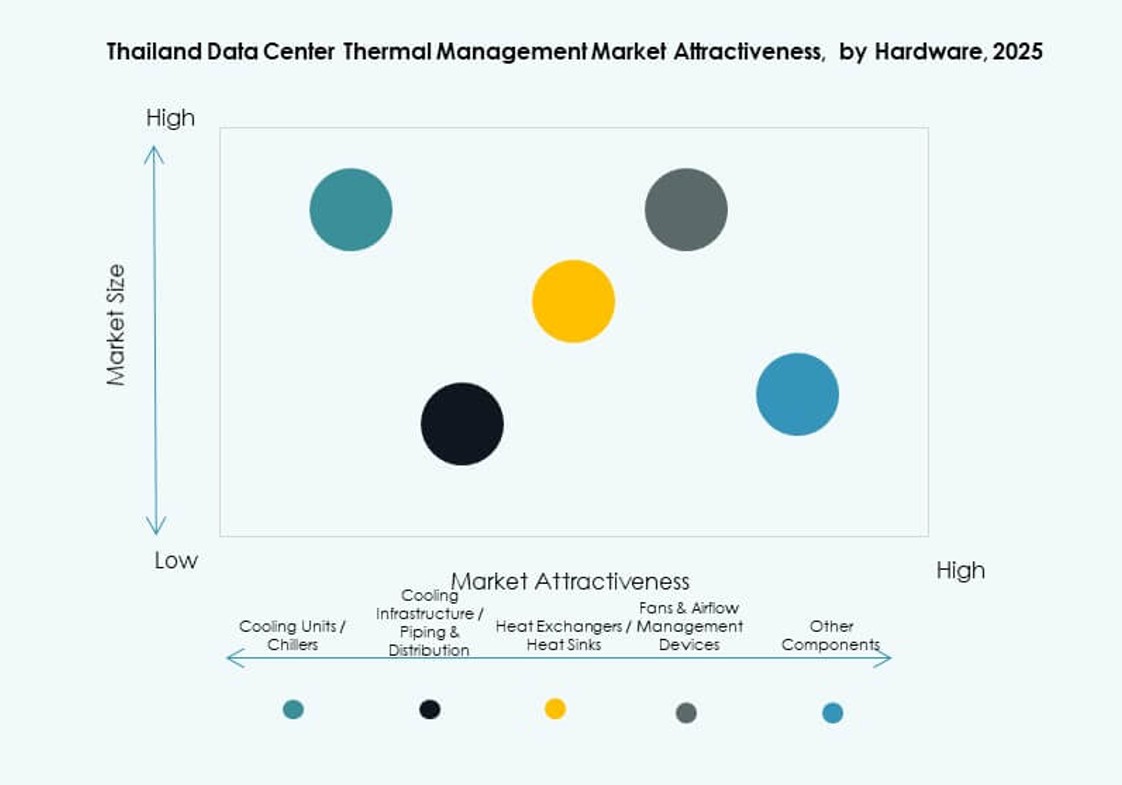

By Hardware

Cooling units and chillers form the core of capital investment. Heat exchangers and airflow devices are critical in managing dense server zones. Rear-door and in-rack fans support high-density setups. Piping and thermal distribution systems are essential in liquid deployments. The Thailand Data Center Thermal Management Market sees innovation in compact, high-efficiency hardware components.

By Software

AI optimization tools and CFD simulation software are expanding market share, supporting performance-based design and automation. BMS and DCIM dashboards enable real-time monitoring and data-driven control. Software plays a key role in reducing PUE and energy costs. Vendors bundling hardware with smart modules see growing preference in the Thailand Data Center Thermal Management Market.

By Services

Installation and commissioning dominate initial deployments, especially in large greenfield builds. Retrofits and predictive maintenance services see high demand among legacy centers. Monitoring-as-a-service is gaining traction in edge and remote setups. The Thailand Data Center Thermal Management Market values integrated service offerings for performance assurance and cost control.

By Data Center Type

Hyperscale facilities lead due to massive AI, cloud, and enterprise deployments. Colocation and cloud providers contribute a major share by hosting mixed workloads. Edge and micro data centers are growing fast, requiring tailored cooling solutions. Enterprise facilities adopt a mix of traditional and new cooling systems. The Thailand Data Center Thermal Management Market reflects this diversity in design and thermal needs.

By Structure

Rack-based and row-based cooling are rising in adoption across modular and scalable deployments. Room-based systems remain in legacy setups but are being replaced gradually. The Thailand Data Center Thermal Management Market trends favor localized thermal management at rack and row level for better efficiency and control.

Regional Insights

Bangkok Metropolitan Region Holds the Largest Share Driven by High Facility Concentration

Bangkok accounts for nearly 63% of the Thailand Data Center Thermal Management Market due to its concentration of hyperscale and enterprise facilities. Strong connectivity, power infrastructure, and demand density make it the country’s primary hub. Most new greenfield projects and international investments target this area. Thermal systems deployed here include large-scale chillers, liquid units, and smart automation. It remains the most advanced region for thermal innovation and deployment scale.

- For instance, True IDC’s North Muangthong data center in Bangkok is Tier III certified by the Uptime Institute and operates with hot/cold aisle containment and N+1 cooling redundancy, supporting enterprise-grade SLAs and high-density compute environments.

Eastern Economic Corridor Emerges as Second-Largest Market with 22% Share

The EEC region is growing into a digital and logistics hub, attracting hyperscale and cloud providers. It accounts for around 22% of the Thailand Data Center Thermal Management Market, supported by land availability and planned submarine cable landings. Operators in this region favor energy-efficient and scalable thermal systems. Government support for smart cities and tech zones drives new data center construction. Vendors are partnering with industrial developers to offer integrated cooling solutions.

Northern and Other Regions Represent 15% Share with High Potential for Edge Growth

Northern Thailand and other emerging zones hold about 15% market share. These regions are seeing rising demand for edge and regional data centers. The Thailand Data Center Thermal Management Market in these areas is driven by telecom providers, education networks, and distributed enterprise systems. Compact cooling, modular deployment, and localized thermal control are in focus. These zones are expected to grow faster due to regional digitization initiatives and low latency requirements.

- For instance, AIS operates a data center in Chiang Mai supporting regional business connectivity with carrier‑grade design and robust networking services.

Competitive Insights:

- Vertiv Group Corp.

- Schneider Electric

- Delta Electronics, Inc.

- Daikin Industries Ltd.

- Trane Technologies plc

- Johnson Controls International plc

- Fujitsu Limited

- Asetek, Inc.

- Samsung SDS

- SUPERNAP Thailand

The Thailand Data Center Thermal Management Market features intense competition driven by global OEMs and regional infrastructure leaders. Vertiv, Schneider Electric, and Delta Electronics lead with broad portfolios in air-based, liquid, and hybrid cooling systems. Local players like SUPERNAP Thailand and True IDC focus on operational integration and site-specific efficiency. Companies invest in AI-enabled thermal software, liquid cooling units, and predictive maintenance services to gain edge. Global firms leverage partnerships and modular product launches tailored for high-density AI workloads. The market rewards vendors offering scalable, energy-efficient solutions suited for hyperscale, colocation, and edge data centers. It continues to shift toward integrated hardware-software platforms optimized for cost, uptime, and sustainability.

Recent Developments:

- In August 2025, Daikin Industries Ltd. bolstered its data center cooling capabilities with the acquisition of Dynamic Data Centers Solutions, Inc. (DDC Solutions), a specialist in AI-compatible server rack cooling. The deal integrates DDC’s technologies into Daikin’s HVAC portfolio to target high-density AI environments globally.

- In June 5, 2025, B.Grimm Technology partnered with Siemens on data center solutions, including thermal management innovations for efficiency and sustainability in Thailand’s market. This collaboration was highlighted at the Siemens Data Center Conference.

- In March 2025, China Mobile officially completed the acquisition of SUPERNAP Thailand, marking a full shift in ownership for the Chonburi data center facility.

- In November 2024, Delta Electronics, Inc. and Siemens Smart Infrastructure formalized a global strategic partnership at a signing ceremony in Bangkok to deliver prefabricated, modular data center power and cooling infrastructure.