Executive summary:

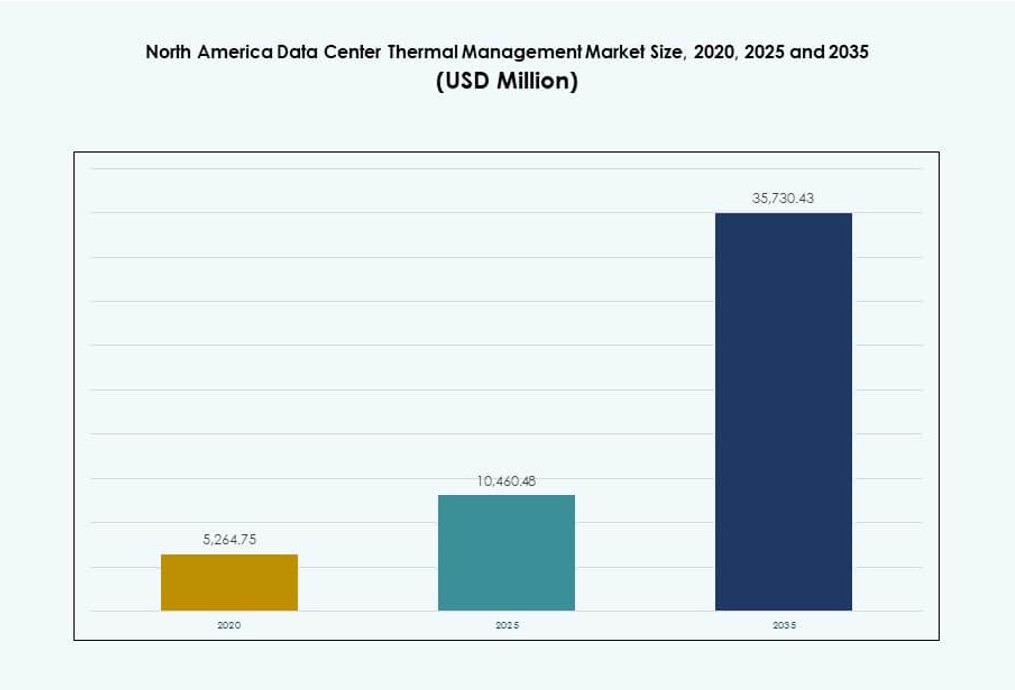

The North America Data Center Thermal Management Market size was valued at USD 5,264.75 million in 2020 to USD 10,460.48 million in 2025 and is anticipated to reach USD 35,730.43 million by 2035, at a CAGR of 13.00% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| North America Data Center Thermal Management Market Size 2025 |

USD 1,282.37 Million |

| North America Data Center Thermal Management Market, CAGR |

11.98% |

| North America Data Center Thermal Management Market Size 2035 |

USD 4,000.51 Million |

Thermal management has become a critical enabler of next-generation data center infrastructure across North America. Operators are rapidly adopting liquid cooling, AI-optimized airflow, and modular containment systems to support rising rack power densities and AI workloads. Sustainability mandates and energy efficiency goals push innovation across all segments. Businesses view thermal optimization as essential for operational stability, while investors consider it a high-growth area tied directly to AI, HPC, and hyperscale demand expansion.

The United States leads the regional market with widespread hyperscale development and strong cloud ecosystem presence. Canada emerges as a strategic growth hub due to renewable power, cold climate, and growing AI infrastructure in provinces like Québec and Ontario. Mexico sees increasing investment in edge and colocation facilities, driven by regional enterprise digitization and demand for compact, scalable cooling solutions. These dynamics reflect a broad, multi-tiered opportunity landscape across North America.

Market Dynamics:

Market Drivers

Rising Power Density in AI and HPC Infrastructure Requiring Advanced Cooling Adaptation

Data centers in North America are deploying AI and HPC workloads with rack densities exceeding 40 kW. This power increase requires direct-to-chip liquid cooling and immersion systems. Traditional air-cooling setups cannot manage the heat output effectively in such environments. Operators are retrofitting legacy sites to align with modern thermal demands. The North America Data Center Thermal Management Market benefits from early technology testing by hyperscalers. It drives innovation in cooling distribution units, controls, and heat reuse. Thermal failure risks also make uptime-critical cooling a high-investment area. Businesses and investors prioritize this segment to secure energy savings and operational resilience.

- For instance, Supermicro’s liquid-cooled 8x NVIDIA H100 GPU systems maintain GPU temperatures at 46–54°C, a 9–17°C reduction compared to air-cooled setups at 55–71°C.

Shift Toward Sustainable Infrastructure Driving Water and Energy Efficient Cooling Design

Cloud and colocation providers target sustainable growth by adopting efficient cooling systems. Cooling contributes up to 40% of total facility energy consumption, prompting redesigns across North America. Closed-loop liquid cooling, refrigerant-free systems, and modular solutions support LEED, Energy Star, and carbon neutrality goals. Water usage effectiveness is becoming a competitive differentiator. The North America Data Center Thermal Management Market sees demand from tech firms aiming to reduce environmental footprint. Governments also issue mandates around energy reporting and water usage. Efficient thermal designs help meet ESG compliance. Investors gain long-term value from lower OpEx and enhanced facility lifespan.

Growing Edge and Modular Deployments Accelerating the Use of Compact, Scalable Cooling Solutions

Edge computing and prefabricated modular data centers grow rapidly across the U.S. and Canada. These formats demand thermal management solutions that are scalable, fast to deploy, and space-optimized. Rear door heat exchangers, rack-based cooling, and hybrid liquid-air technologies dominate such applications. The North America Data Center Thermal Management Market captures value from edge rollouts in telecom, manufacturing, and retail. It supports latency reduction and localized compute needs. Vendors focus on plug-and-play cooling units tailored for containerized infrastructure. Businesses invest in modular systems to reduce risk and simplify future expansions. Compact cooling becomes a key differentiator in edge-based growth models.

- For instance, NVIDIA HGX H100 SXM5 8-GPU boards support direct liquid cooling with configurable thermal design power up to 700W per GPU.

Increased Reliability Requirements Driving Adoption of Predictive and AI-Driven Thermal Control

Downtime risk from overheating leads operators to adopt AI-powered thermal control systems. These platforms predict heat loads, optimize fan speeds, and manage chilled water loops in real time. Data Center Infrastructure Management (DCIM) tools with thermal mapping enhance operational accuracy. The North America Data Center Thermal Management Market evolves to offer intelligent automation for heat resilience. It supports Tier III and Tier IV designs where thermal failure is unacceptable. Predictive insights lower energy usage without compromising uptime. Businesses leverage analytics for performance tracking and compliance audits. This capability makes thermal management not just a cost center but a strategic control layer.

Market Trends

Integration of Liquid Cooling into Mainstream Deployments Beyond Niche HPC and AI Use Cases

Liquid cooling is transitioning from niche to mainstream within enterprise and colocation segments. Direct-to-chip and rear-door liquid heat exchangers are now used in standard deployments. These systems manage rising densities while reducing floor space usage. Vendors provide retrofittable kits to simplify integration. The North America Data Center Thermal Management Market incorporates these systems into newly designed and upgraded facilities. Liquid cooling offers reduced power draw and better thermal control. Operators prioritize these solutions for GPU-intensive workloads. Their adoption marks a shift in baseline expectations for next-gen facilities.

Data Center Heat Reuse Gaining Traction for Sustainability and Utility Partnerships

Heat reuse projects in North America are gaining visibility due to rising energy costs and ESG goals. Operators now use waste heat to warm nearby buildings or greenhouses. It allows data centers to offset environmental impact while creating secondary revenue. The North America Data Center Thermal Management Market reflects growing partnerships with utilities and municipalities. Successful examples exist in colder regions like Canada and northern U.S. states. Vendors develop compatible equipment such as heat pumps and reclaim exchangers. Reuse planning becomes part of thermal design strategies. These systems drive long-term sustainability goals without heavy infrastructure change.

AI-Based Thermal Monitoring and Predictive Maintenance Becoming Standard in Facility Design

AI is being embedded into Building Management Systems (BMS) and DCIM platforms. These tools manage cooling performance, fan speed, and chiller loads with minimal manual oversight. The North America Data Center Thermal Management Market sees this as an enabler for OPEX control and uptime assurance. Operators gain visibility into thermal zones and identify risks early. AI reduces overcooling and minimizes false alarms. Machine learning adapts settings based on historical loads and seasonal shifts. It improves SLA adherence and equipment lifecycle. Such technologies now appear in RFPs for large-scale expansions.

Demand for Liquid Cooling-Compatible IT and Infrastructure Equipment Across Vendors

OEMs and cooling vendors increasingly collaborate to offer liquid-ready infrastructure. Servers, racks, and enclosures now support integrated cold plates or immersion formats. The North America Data Center Thermal Management Market benefits from this convergence. Compatibility ensures smoother deployments and avoids complex retrofits. Tech firms prefer standardized platforms for quicker rollout across regions. Vendors that enable open-loop and closed-loop systems gain wider adoption. Thermal management decisions now influence IT hardware selection. The alignment between IT and facilities creates new ecosystem dynamics in the market.

Market Challenges

Complexity and Cost of Upgrading Legacy Facilities to Support Next-Gen Thermal Architectures

Retrofitting legacy sites to handle AI and high-density workloads presents significant challenges. Many data centers in North America were built for 5–10 kW rack densities. New workloads often require 30–60 kW, forcing redesign of cooling paths, floor layouts, and electrical support. The North America Data Center Thermal Management Market faces high upfront costs in liquid cooling retrofits. Incompatibility with older IT gear also raises deployment barriers. Operational disruptions during retrofits reduce revenue uptime. Many operators postpone upgrades or limit them to small sections. This delays the adoption of efficient cooling across older assets.

Shortage of Skilled Labor and Standardized Design Knowledge in Emerging Thermal Systems

Thermal systems now involve liquid circuits, heat reuse, and AI-based controls. Engineers need specialized training for design, installation, and maintenance. The North America Data Center Thermal Management Market sees a shortage of such technical talent. Vendors vary in design standards, which slows deployments and raises risk. Smaller operators face longer project cycles due to knowledge gaps. Education programs lag behind the technology pace. Businesses struggle to scale advanced cooling in multiple sites. Labor constraints limit the speed of sustainable infrastructure expansion.

Market Opportunities

Growth in Hyperscale and AI Infrastructure Driving Long-Term Demand for Advanced Cooling

AI models and cloud applications require high-density compute environments. Hyperscalers build massive facilities with cooling loads reaching hundreds of megawatts. The North America Data Center Thermal Management Market will gain sustained momentum from this trend. It supports long-term investments in liquid cooling, automation, and thermal energy reuse. Companies offering scalable solutions will capture large multi-site deals.

Policy Support for Green Cooling and Smart Infrastructure Creating Incentive-Driven Markets

Government incentives encourage green energy, water conservation, and efficient infrastructure. These policies create funding pipelines for cooling modernization. The North America Data Center Thermal Management Market benefits from such initiatives. Vendors offering low-water and energy-efficient systems will win more public-private partnerships. Regulatory alignment creates clear growth pathways across the U.S. and Canada.

Market Segmentation

By Data Center Size

Large data centers dominate the North America Data Center Thermal Management Market due to widespread hyperscale expansion. They demand high-capacity cooling systems tailored for 40–60 kW racks. Medium data centers grow steadily with colocation adoption among enterprises. Small facilities find relevance in edge deployments requiring compact cooling units. Each segment tailors its solution to space, density, and uptime needs.

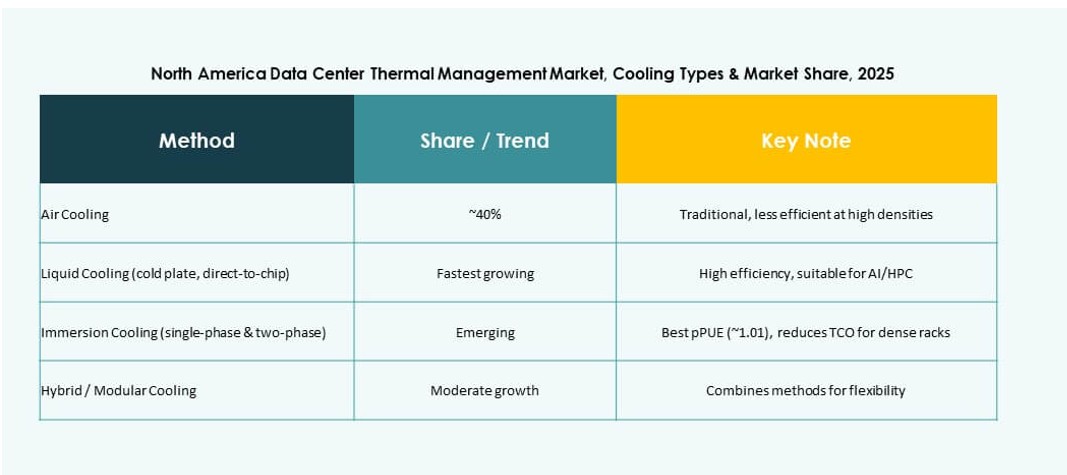

By Cooling Technology

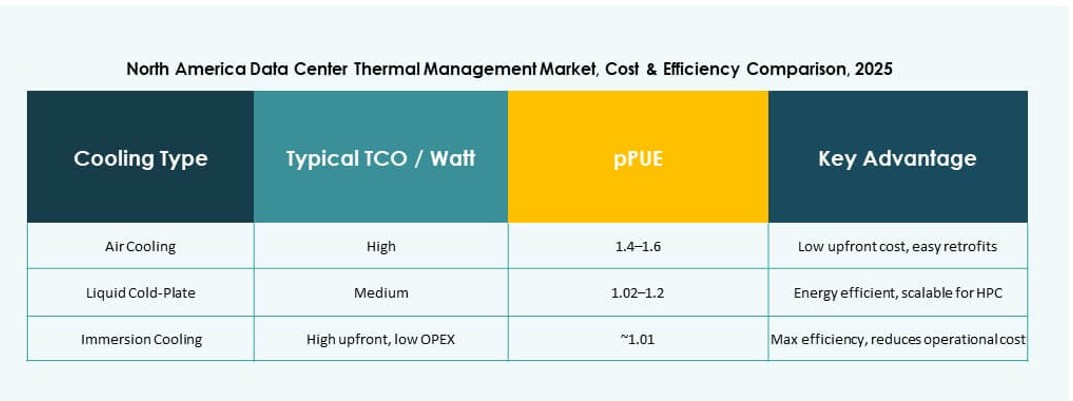

Air-based cooling, including hot/cold aisle containment and rear door exchangers, holds the largest share in existing facilities. Liquid-based technologies like direct-to-chip and immersion rapidly gain traction due to high-density loads. Hybrid solutions combine both for flexibility in mixed rack environments. Thermoelectric and phase-change remain niche but attract interest in compact setups.

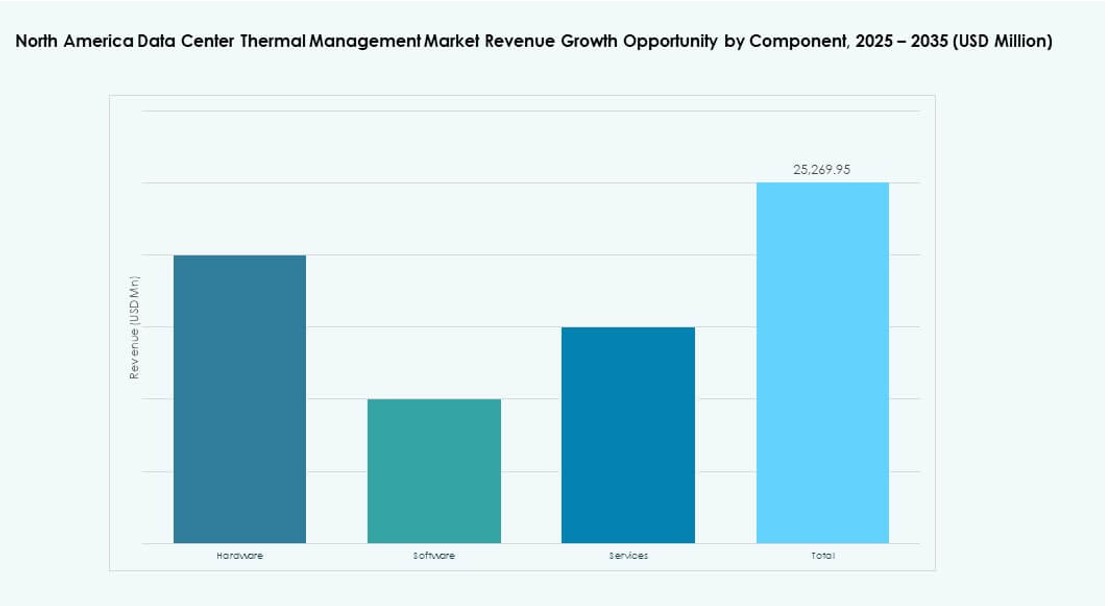

By Component

Hardware accounts for the highest share, driven by chillers, fans, and distribution systems. Software components are expanding, with AI-based optimization and thermal modeling tools. Services segment adds value through installations, retrofits, and maintenance support. The North America Data Center Thermal Management Market favors integrated component strategies for long-term resilience.

By Hardware

Cooling units and chillers form the largest hardware share due to their core function in thermal exchange. Piping, heat sinks, and airflow devices support fluid and air transport across racks. Each sub-segment addresses different thermal profiles, with flexibility and redundancy built into designs. Demand is high in both greenfield and retrofit projects.

By Software

DCIM dashboards and BMS modules lead in adoption, enabling centralized monitoring. AI optimization tools gain usage for dynamic workload-based cooling. CFD simulation supports facility planning and thermal zoning. Software platforms help lower energy costs and improve decision-making across operations.

By Services

Installation and commissioning dominate the services segment. Preventive maintenance and monitoring services ensure long-term reliability. Retrofits and upgrades gain momentum with AI adoption and liquid cooling retrofits. “Monitoring as a Service” grows as operators outsource analytics for efficiency. Each service aligns with the market’s shift toward intelligent infrastructure.

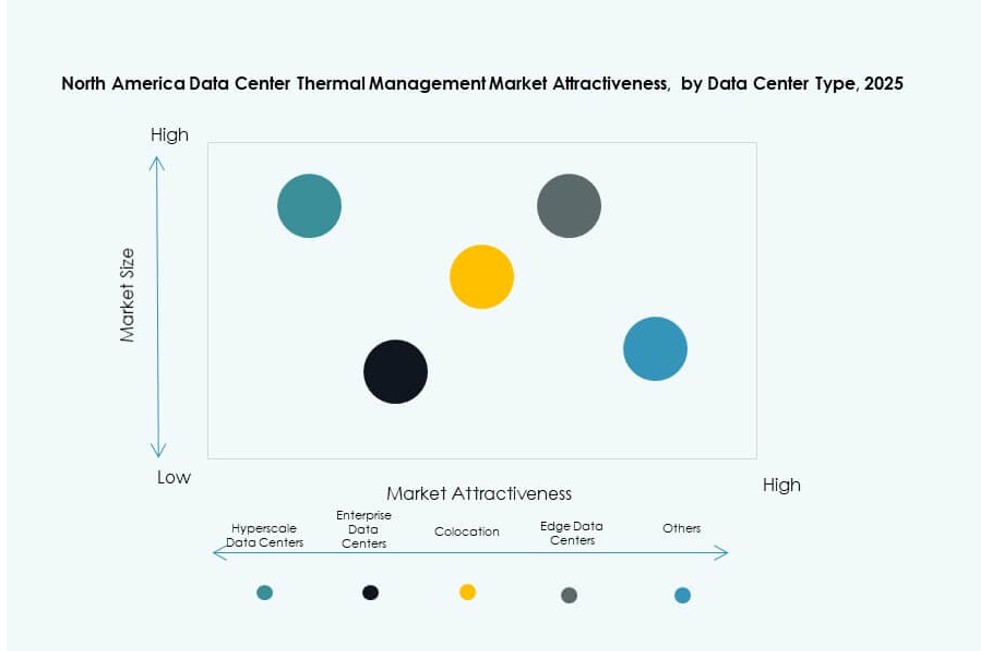

By Data Center Type

Hyperscale centers hold the largest share due to high compute loads and investment volumes. Enterprise deployments follow, requiring scalable but secure thermal systems. Colocation/cloud sites adopt modular cooling designs. Edge/micro centers use rack-based or compact liquid systems. Each segment pursues thermal efficiency aligned with business models.

By Structure

Room-based cooling remains dominant in older data centers. Row-based and rack-based systems grow fastest, especially in modular deployments. Rack-level cooling enables density above 30 kW with minimal footprint. The shift favors rack-integrated solutions that reduce floor-based cooling inefficiencies.

Regional Insights

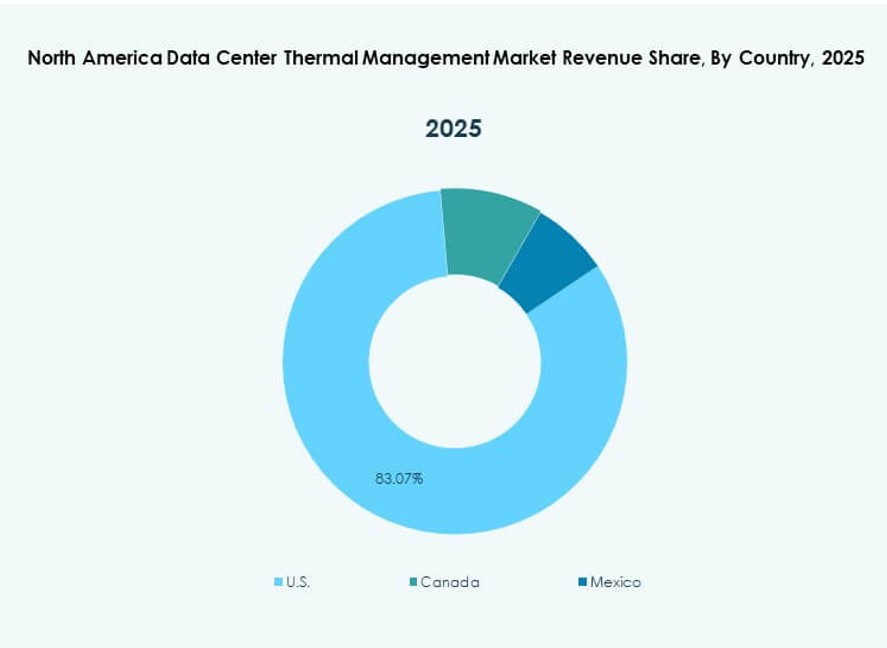

United States Leading with Over 75% Market Share Due to Hyperscale Concentration and Investment Scale

The United States commands the largest share of the North America Data Center Thermal Management Market. Its dominance stems from major hyperscale activity in Virginia, Texas, California, and Oregon. Large campuses drive demand for liquid cooling and predictive thermal automation. U.S.-based cloud providers like Amazon, Microsoft, and Google lead deployments. Investments target both greenfield and retrofit projects. State-level incentives for energy-efficient infrastructure strengthen market momentum.

Canada Emerging with 15% Market Share Supported by Renewable Energy and AI Infrastructure

Canada follows with growing adoption across provinces like Québec, Ontario, and British Columbia. Its data centers benefit from hydroelectric power and cold climate, enabling free cooling and low PUE targets. The North America Data Center Thermal Management Market expands here with AI-focused infrastructure in Montréal and Toronto. Canadian operators focus on sustainable design, using hybrid cooling systems and river-cooled setups. Public policies favor digital infrastructure resilience.

- For instance, Stack Infrastructure’s TOR01 campus in Toronto offers up to 56 MW capacity, serving hyperscale and enterprise clients in a high-demand metro. The facility is designed for high efficiency, leveraging the local climate to support sustainable cooling strategies.

Mexico Accounting for Around 10% Market Share with Demand Rising in Edge and Colocation Segments

Mexico holds a smaller yet expanding portion of the North America Data Center Thermal Management Market. Growth concentrates in Querétaro, Guadalajara, and Monterrey due to proximity to enterprise hubs. Edge and modular deployments need compact and resilient cooling. Operators adopt hybrid solutions in high-temperature zones. Colocation demand from financial and retail firms fuels new facilities. Government interest in digital infrastructure adds support for thermal upgrades.

- For instance, Equinix’s MX2 data center in Querétaro, Mexico supports enterprise and cloud workloads with standardized air‑cooled CRAC/CRAH cooling infrastructure. The facility is built with redundancy and capacity planning to meet high uptime requirements.

Competitive Insights:

- Vertiv Group Corp.

- Schneider Electric

- Stulz GmbH

- Trane Technologies plc

- Daikin Industries Ltd.

- Delta Electronics, Inc.

- Johnson Controls International plc

- Eaton Corporation

- Huawei Technologies Co., Ltd.

- Munters Group AB

The North America Data Center Thermal Management Market remains highly competitive with a mix of global powerhouses and regional specialists. Vertiv, Schneider Electric, and Stulz lead in thermal innovation, offering scalable and efficient cooling systems for hyperscale and enterprise data centers. Trane and Daikin focus on HVAC-integrated solutions, catering to both room-based and modular setups. Delta Electronics and Huawei invest heavily in liquid cooling for AI workloads. Eaton and Johnson Controls emphasize energy-efficient control systems and predictive maintenance tools. Market competition intensifies with rising demand for liquid cooling, AI-driven automation, and hybrid systems. It continues to evolve through mergers, product launches, and strategic partnerships that improve energy efficiency, thermal visibility, and deployment speed.

Recent Developments:

- In November 2025, Johnson Controls launched a new product for scalable cooling. The company introduced the Silent-Aire Coolant Distribution platform, offering capacities from 500kW to over 10MW for high-density data centers

- In March 2025, Delta launched advanced thermal management innovations like In-Rack CDUs handling up to 250kW for AI GPUs and servers, supporting hybrid liquid-air cooling in high-density data centers. These solutions emphasize energy efficiency for NVIDIA-enabled HPC environments.

- In February 2025, Airedale by Modine announced major orders for high-capacity, purpose-built cooling equipment tailored for scalable, sustainable AI data centers. This deal highlights the company’s strategic position in thermal management amid rising demand for high-performance computing clusters.