Executive summary:

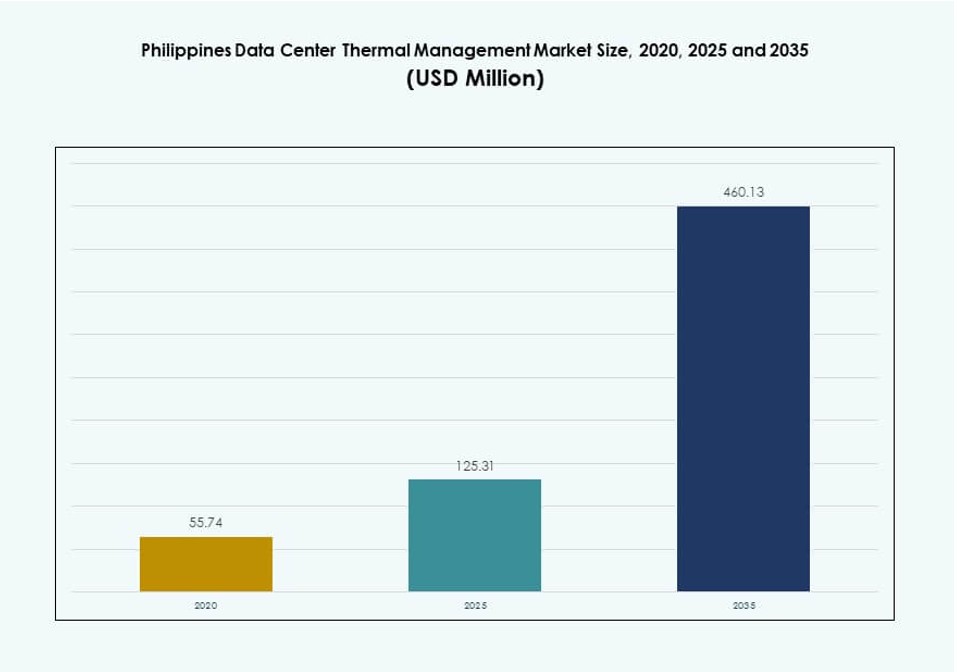

The Philippines Data Center Thermal Management Market size was valued at USD 55.74 million in 2020, increased to USD 125.31 million in 2025, and is anticipated to reach USD 460.13 million by 2035, at a CAGR of 13.80% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Philippines Data Center Thermal Management Market Size 2025 |

USD 125.31 Million |

| Philippines Data Center Thermal Netherlands Market, CAGR |

13.80% |

| Philippines Data Center Thermal Management Market Size 2035 |

USD 460.13 Million |

Growth is driven by expanding hyperscale and colocation facilities, alongside rising AI and cloud adoption. Businesses are deploying high-density server infrastructure, pushing demand for efficient cooling systems. Liquid-based cooling, AI-driven DCIM platforms, and modular thermal systems are gaining traction. Operators aim for energy efficiency and regulatory compliance while ensuring uptime. Thermal systems are now seen as strategic investments to support compute-intensive operations. Innovation in hybrid and immersion cooling technologies continues to redefine infrastructure planning. Investors view this market as critical for supporting digital transformation and sustainability goals.

Metro Manila leads due to its high data center concentration, strong fiber connectivity, and enterprise presence. Clark and Cebu are emerging regions supported by government incentives and infrastructure investments. These areas offer suitable land, power availability, and latency advantages for regional hubs. Secondary cities across Visayas and Mindanao show early-stage activity through edge deployments. Location decisions increasingly consider renewable energy access and climate adaptability. Geographic expansion reflects the need for broader digital infrastructure coverage across the country.

Market Dynamics:

Market Drivers

Digital Transformation and Increased Cloud Investments Driving Thermal System Demand

Digital transformation across industries is pushing demand for high-performance and energy-efficient thermal systems. Enterprises are deploying cloud-based applications, AI workloads, and big data systems, all of which increase server density. The Philippines Data Center Thermal Management Market benefits from increased rack heat loads that demand precise thermal control. Liquid cooling and hybrid systems see higher uptake to maintain uptime and prevent overheating. The rise of financial services, e-commerce, and telecom workloads accelerates this need. Thermal solutions ensure server stability while supporting faster deployment cycles. Energy efficiency regulations also encourage sustainable cooling choices. Businesses and investors consider this a strategic area due to rising compute needs and carbon reduction mandates.

Colocation and Hyperscale Growth Prompting Infrastructure Upgrades

The expansion of colocation and hyperscale data centers drives demand for advanced thermal infrastructure. Operators like ePLDT, Beeinfotech, and Digital Edge are building new high-density sites. These facilities often host AI accelerators and GPUs that generate extreme heat loads. Thermal systems need to match this density while reducing power usage. The Philippines Data Center Thermal Management Market sees strong vendor partnerships for chillers, containment systems, and DCIM tools. Energy use effectiveness (PUE) metrics are closely monitored by global clients. New builds aim for low PUE using AI-optimized airflow and liquid cooling. Thermal system investment now plays a key role in winning enterprise and hyperscale deals. This fuels investor interest in scalable and modular cooling models.

- For instance, in May 2023, STT GDC Philippines announced its 124 MW STT Fairview data center campus in Quezon City, Manila, designed to support high-density workloads with infrastructure readiness for advanced liquid cooling systems.

Rising Power Costs and Renewable Energy Adoption Reinforcing Efficient Cooling

With power rates rising and grid strain increasing, data centers seek thermal solutions that lower energy intensity. Liquid-based cooling and containment-driven airflow strategies support this goal. Renewable energy integration, especially solar, requires thermal systems that can handle fluctuating loads. The Philippines Data Center Thermal Management Market benefits from DCIM and BMS modules that regulate thermal performance in real-time. Efficient thermal systems extend equipment life and reduce failure risk. Industry players adopt intelligent chillers and predictive cooling analytics. The drive to reduce carbon footprint further elevates energy-efficient cooling as a competitive differentiator. Sustainable thermal management becomes a core pillar for infrastructure resilience and regulatory compliance.

Edge Data Center Expansion Creating Need for Scalable Thermal Technologies

Edge and micro data center deployments across second-tier cities are rising, fueled by content delivery and telecom requirements. These facilities have constrained footprints and limited cooling headroom. The Philippines Data Center Thermal Management Market responds with modular, scalable thermal systems suited for remote operation. Row-based and rack-integrated cooling systems gain popularity in such setups. Equipment must offer high thermal efficiency with low maintenance demands. Telecom firms integrate remote monitoring and AI-driven controls for thermal fault detection. These edge sites support 5G base stations and IoT data aggregation, requiring continuous operation. Thermal stability becomes critical in distributed, latency-sensitive applications. Investors back technologies that offer cooling agility across varied environments.

- For instance, STT GDC’s Southeast Asia data centers, including Philippines sites, support higher-density powered racks from 10 to 150kW designed for AI-ready thermal management in edge-like deployments.

Market Trends

AI and HPC Workloads Pushing Shift Toward Liquid-Based Cooling Integration

AI and high-performance computing applications are growing in the Philippines data center space. These workloads require more power and generate greater heat, beyond the limits of traditional air cooling. Liquid-based cooling, including direct-to-chip and immersion, is gaining adoption. The Philippines Data Center Thermal Management Market integrates these systems in GPU-heavy deployments. Vendors report increasing trials of immersion cooling in fintech and research facilities. Thermal designs now support heat reuse and closed-loop liquid systems. Enterprises evaluate ROI based on energy cost savings and footprint efficiency. This trend redefines facility design, influencing floor plans and rack configurations.

AI-Driven DCIM and Thermal Monitoring Enhancing Operational Intelligence

Operators prioritize automation of cooling control systems to minimize manual intervention. AI-enhanced data center infrastructure management (DCIM) tools optimize airflow, fan speeds, and temperature regulation dynamically. The Philippines Data Center Thermal Management Market adopts thermal analytics dashboards to detect inefficiencies in real time. Predictive alerts help prevent thermal runaway and downtime. Smart sensors and IoT modules provide granular insights into rack-level heat. These systems allow seamless integration with building management systems (BMS). Cloud-based thermal control platforms are increasingly used in multi-site operations. The trend strengthens operational efficiency while supporting SLA adherence in mission-critical environments.

Demand for Sustainability Metrics and Heat Recovery System Deployment

Clients now demand sustainability metrics from colocation and cloud providers. Energy usage, cooling water consumption, and carbon reduction play a growing role in contracts. The Philippines Data Center Thermal Management Market sees rising deployment of heat recovery systems. These systems capture waste heat for reuse in neighboring industrial or residential applications. Cooling system vendors now include lifecycle carbon output in product specs. Circular cooling concepts are being tested in eco-zones and green campuses. Energy-conscious buyers favor operators using free-air cooling or low-GWP refrigerants. This trend drives suppliers to innovate sustainable product designs and eco-certifications.

Hybrid Cooling Systems Supporting Diverse IT Load Profiles and Climate Challenges

Philippine data centers operate under tropical climate stress, making hybrid cooling a necessity. Combining air and liquid systems helps balance load conditions and environmental variables. The Philippines Data Center Thermal Management Market integrates hybrid systems for both legacy and new sites. These solutions support hot aisle containment with supplemental liquid circuits. Facilities facing frequent grid fluctuations opt for passive cooling backups. Hybrid configurations reduce reliance on energy-intensive chillers during low load periods. Operators use CFD simulation software to model airflow behavior and heat zones. This trend enables better planning and cost optimization across varied site geographies.

Market Challenges

High Energy Intensity of Cooling Systems and Limited Grid Capacity Affecting Deployment

Thermal systems consume significant power, often 30–40% of total data center energy use. In the Philippines, where electricity prices are high and grid reliability varies, this creates cost and uptime risks. The Philippines Data Center Thermal Management Market faces constraints in deploying energy-intensive solutions. Many regional grids lack resilience to support cooling loads for hyperscale facilities. Liquid-based cooling requires water treatment infrastructure, which adds complexity. Air cooling, while simpler, struggles with high-density racks in tropical zones. Investment in cooling upgrades competes with spending on security, redundancy, and connectivity. This delays modernization for many mid-size operators. Scaling sustainable cooling under local constraints requires creative engineering and policy alignment.

Limited Technical Expertise and High System Integration Costs Slowing Adoption

Advanced thermal management systems demand specialized installation and integration. The Philippines Data Center Thermal Management Market experiences a shortage of certified engineers for liquid cooling, CFD modeling, and thermal software deployment. Most cooling vendors operate via offshore teams, causing delays. System complexity adds to operational risks without trained staff. Small data centers avoid hybrid systems due to integration costs and monitoring requirements. Software modules for DCIM and BMS often require customization to local equipment. The learning curve for AI-based thermal optimization tools remains steep. Without local ecosystem maturity, adoption of next-gen thermal systems remains limited outside top-tier operators.

Market Opportunities

Hyperscale and AI Facility Pipeline Creating Strong Upside for Liquid and AI-Driven Cooling

Major operators have announced new hyperscale and AI-ready campuses in the Philippines. These facilities require cutting-edge thermal systems that support 30–50 kW rack densities. The Philippines Data Center Thermal Management Market sees high interest in liquid-cooled and AI-optimized solutions. Vendors that offer scalable platforms, AI-based dashboards, and modular systems stand to gain. Foreign investments support quick tech deployment in these high-value projects. This pipeline strengthens the business case for advanced cooling technologies.

Government Incentives and Renewable Energy Integration Favoring Energy-Efficient Cooling Vendors

The government supports data center zones and renewable-powered facilities through tax incentives and zoning benefits. Operators are under pressure to reduce PUE and carbon footprint. The Philippines Data Center Thermal Management Market benefits vendors offering low-energy and sustainable cooling. Technologies such as passive systems, immersion cooling, and AI-managed fans gain traction. This policy support creates favorable ground for international thermal infrastructure providers.

Market Segmentation

By Data Center Size

Large data centers dominate the Philippines Data Center Thermal Management Market due to rapid hyperscale and cloud growth. These facilities require advanced thermal systems for high-density workloads and 24/7 operations. Medium-sized data centers also show strong adoption, especially among telecom and financial service providers. Small data centers rely on simpler, cost-effective air-based cooling but face increasing pressure to upgrade. Large facilities lead the segment due to scale economies and vendor partnerships.

By Cooling Technology

Air-based cooling holds a major share due to cost efficiency and ease of maintenance. Hot/cold aisle containment and direct air systems remain preferred in retrofit projects. However, liquid-based cooling is gaining traction, especially in GPU-heavy environments. Direct-to-chip and immersion cooling are being piloted in AI data centers. Hybrid systems combining air and liquid technologies address diverse thermal needs. Emerging technologies like phase-change cooling are under evaluation. Liquid-based solutions are expected to grow rapidly due to rising heat densities.

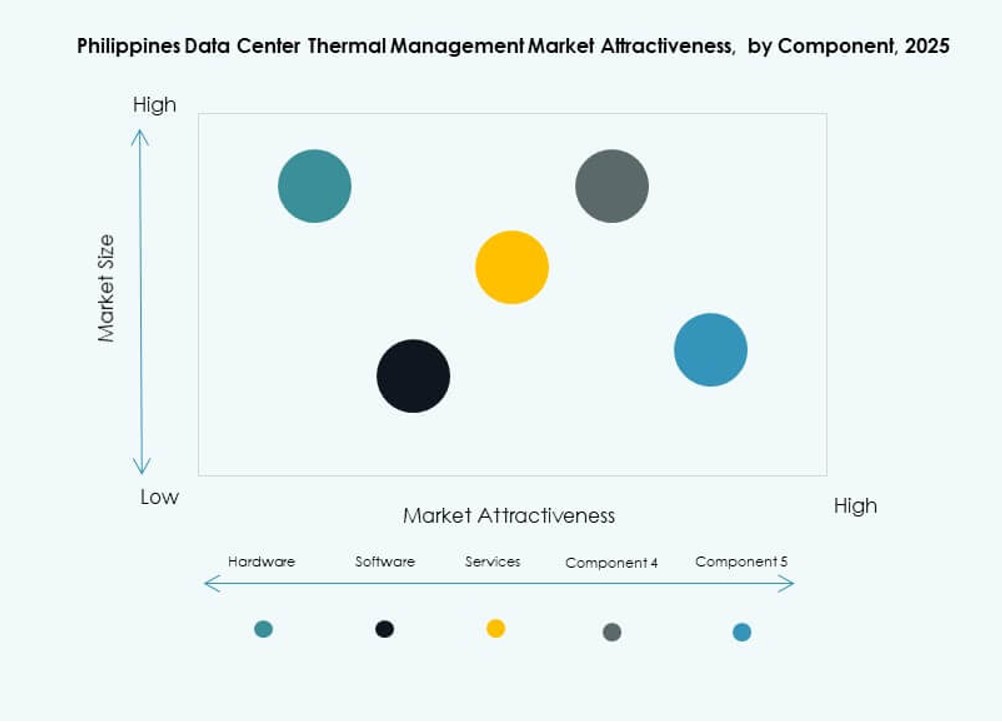

By Component

Hardware leads the segment due to high initial investment in chillers, heat exchangers, and airflow devices. Software is gaining importance with increased use of DCIM, AI modules, and simulation tools. Services including installation, retrofits, and remote monitoring are growing due to demand for uptime assurance. The Philippines Data Center Thermal Management Market sees a shift toward software and services integration for lifecycle performance optimization.

By Hardware

Cooling units and chillers dominate the hardware subsegment with high replacement cycles and capital investment. Heat exchangers and sinks gain importance in liquid cooling setups. Piping and distribution systems are crucial for closed-loop operations. Fans and airflow devices remain essential for air-based systems and containment zones. Other components like thermal interface materials support system efficiency.

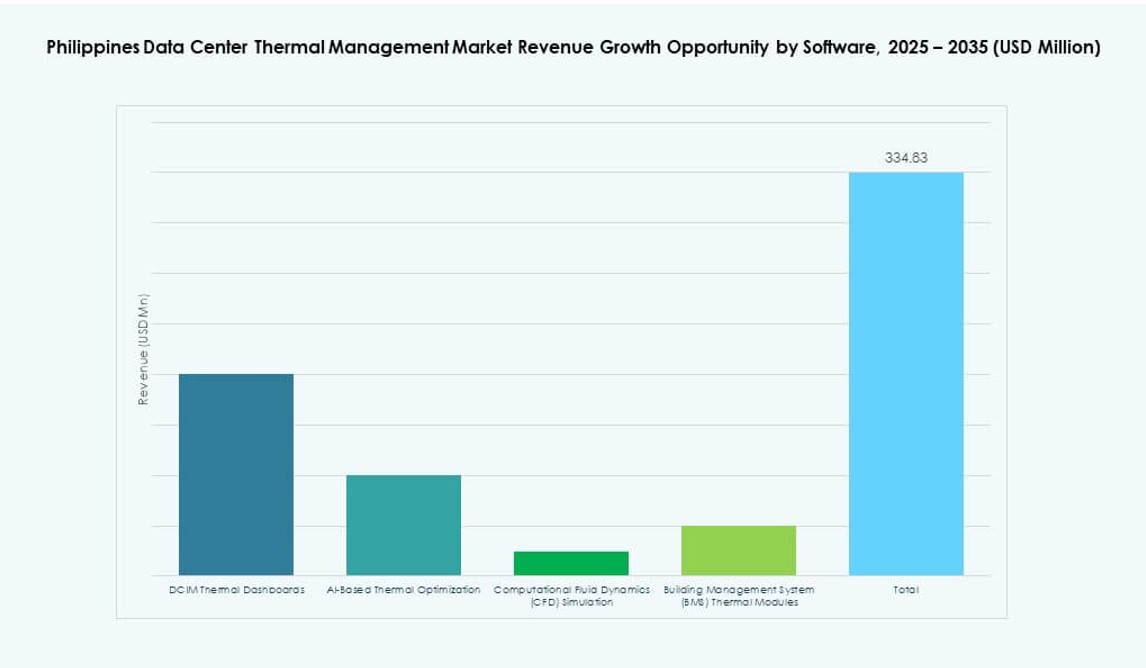

By Software

DCIM dashboards lead the software segment, offering centralized control across sites. AI optimization tools are seeing wider adoption for predictive cooling. CFD simulation software helps design airflow layouts and model thermal behavior. BMS modules integrate building-level controls with IT systems for unified management. The software segment enables efficiency and scalability for thermal operations.

By Services

Preventive maintenance holds the largest share due to its role in uptime and reliability. Installation and commissioning follow closely, especially in greenfield projects. Monitoring-as-a-service grows among small and edge data centers. Retrofit and upgrade services are in demand due to energy savings targets. The services segment enhances long-term system performance and compliance.

By Data Center Type

Colocation and cloud data centers lead the segment, driven by digital outsourcing trends. Hyperscale facilities are emerging with strong investor focus. Enterprise data centers adopt hybrid cooling strategies for legacy IT. Edge and micro data centers need compact, efficient cooling for remote locations. Colocation maintains dominance due to large footprint and uptime SLAs.

By Structure

Room-based cooling remains common in legacy facilities. Row-based systems are growing in mid-tier setups, offering better efficiency. Rack-based cooling is gaining ground in high-density deployments. The Philippines Data Center Thermal Management Market shows a shift toward rack-level control to manage GPU and AI loads. Rack-based setups are expected to grow fastest due to their scalability and energy savings.

Regional Insights

Metro Manila Leads the Market with Over 65% Share Due to Facility Concentration and Connectivity

Metro Manila is the central hub for data center activity in the Philippines. It accounts for more than 65% of the Philippines Data Center Thermal Management Market due to dense facility concentration and enterprise demand. Most hyperscale and colocation providers operate their flagship sites here. Strong fiber networks and reliable power supply make it ideal for thermal technology adoption. Vendors prioritize this region for launching advanced cooling systems. The climate challenges in Manila also drive interest in hybrid cooling setups.

- For instance, Digital Edge’s NARRA1 facility deployed Nortek’s StatePoint liquid cooling technology across its 10 MW IT capacity, achieving an annualized PUE of 1.193 and WUE of 1.355.

Clark and Cebu Emerging as Secondary Hubs with Government and Telecom Support

Clark and Cebu are emerging regions with 20% combined market share. Government incentives and PEZA support have made Clark a preferred location for new data center investments. Cebu sees growth from telecom operators and regional enterprises. Both regions benefit from available land, renewable power sources, and low latency to population centers. These cities attract mid-size data centers and edge deployments. Thermal vendors focus on modular and scalable cooling for these growth zones.

Other Provincial Cities Show Early-Stage Activity with Edge and Micro Deployments

Other cities across Visayas and Mindanao account for the remaining 15% market share. These regions witness growth from edge computing and micro data center needs. Use cases include telecom hubs, content caching, and smart city deployments. Thermal solutions in these areas emphasize compact footprint, remote monitoring, and energy efficiency. Local constraints like power quality and maintenance access influence product selection. These areas present long-term opportunity for low-cost, intelligent thermal systems.

- For instance, ePLDT’s VITRO Data Centers deployed N+1 redundant cooling systems with chillers and fan walls supporting up to 5 kVA per cabinet across multiple sites to ensure high uptime and thermal stability for critical workloads.

Competitive Insights:

- Vertiv Group Corp.

- Schneider Electric

- Daikin Industries Ltd.

- Delta Electronics, Inc.

- Johnson Controls International plc

- Mitsubishi Electric Corporation

- Airedale International Air Conditioning Ltd.

- Eaton Corporation

- Munters Group AB

- Rittal GmbH & Co. KG

The competitive landscape shows strong activity from global and regional players investing in advanced thermal solutions for the Philippines Data Center Thermal Management Market. Vertiv and Schneider Electric lead with comprehensive portfolios spanning hardware, software, and services that support hyperscale and colocation facilities. Daikin and Mitsubishi Electric focus on energy-efficient chillers and HVAC systems. Delta and Johnson Controls bring strong automation and controls capabilities that improve thermal performance. Eaton and Rittal provide reliable power-thermal integration solutions. Airedale and Munters deliver precision cooling for high-density racks. Vendors compete on energy efficiency, reliability, and lifecycle support. Partnerships with local operators and system integrators strengthen go-to-market reach. Competitive differentiation lies in modular solutions, remote monitoring tools, and strong service networks that help clients optimize cooling costs and uptime.

Recent Developments:

- In March 2025, STT GDC Philippines, in partnership with Vertiv and Novare Technologies, launched a facility to showcase liquid cooling technology benefits and use cases for local enterprises handling higher power densities.

- In March 2025, Vertiv Group Corp. collaborated with STT GDC Philippines and Novare Technologies to launch the Philippines’ first liquid cooling showroom featuring Vertiv’s Liebert XDU100 coolant distribution units for AI workloads in data centers.

- In February 2025, Schneider Electric acquired a controlling interest in Motivair enhancing its liquid cooling portfolio for high-density data centers with CDUs, chillers, and software, as announced globally.