Executive summary:

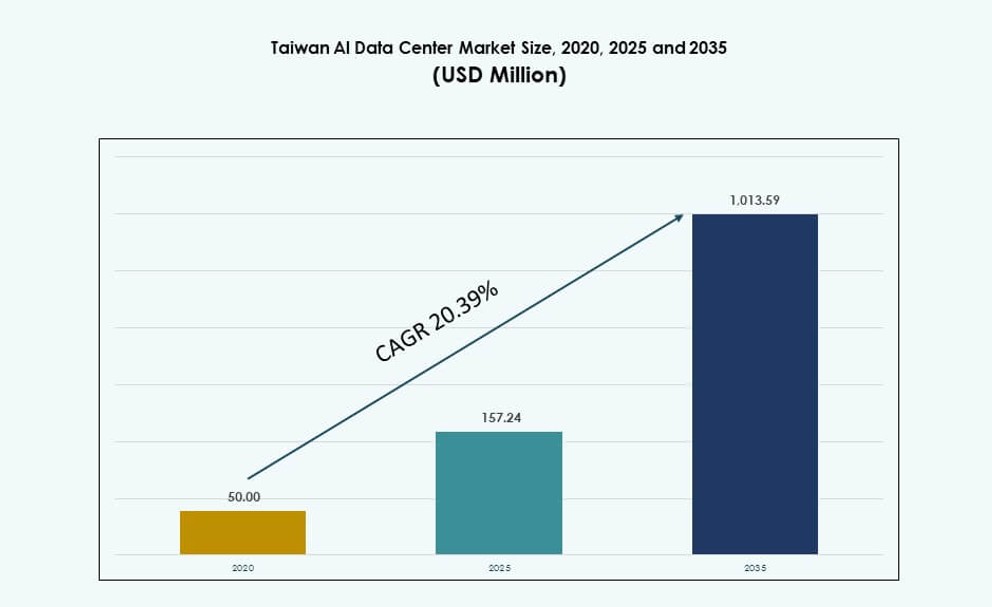

The Taiwan AI Data Center Market size was valued at USD 50.00 million in 2020 to USD 157.24 million in 2025 and is anticipated to reach USD 1,013.59 million by 2035, at a CAGR of 20.39% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Taiwan AI Data Center Market Size 2025 |

USD 157.24 Million |

| Taiwan AI Data Center Market, CAGR |

20.39% |

| Taiwan AI Data Center Market Size 2035 |

USD 1,013.59 Million |

Rapid AI adoption in enterprise and government sectors is driving infrastructure investment across Taiwan. Cloud providers, telecom firms, and chipmakers are investing in AI-ready data centers with liquid cooling and high-density racks. The market is also benefiting from demand for sovereign AI compute and low-latency service delivery. Strong chip design and manufacturing ecosystems enable early access to cutting-edge GPUs and system integration. These developments position the Taiwan AI Data Center Market as a strategic hub for both local innovation and regional AI infrastructure growth.

Northern Taiwan dominates the market due to established R&D clusters, fiber infrastructure, and hyperscale activity in Taipei and Hsinchu. Central Taiwan is gaining traction with manufacturing-led AI edge deployments in Taichung. Southern Taiwan is emerging with renewable-integrated sites near Kaohsiung, offering land availability and export linkage for AI workloads. These regional strengths contribute to a balanced and scalable ecosystem for the Taiwan AI Data Center Market.

Market Dynamics:

Market Drivers

Rising AI Workloads Accelerating Data Infrastructure Investment Across Sectors

The Taiwan AI Data Center Market is growing due to increasing demand for AI-specific workloads. Industries including healthcare, finance, and manufacturing require high-performance computing for real-time analytics and automation. This shift fuels demand for GPU-dense infrastructure and advanced thermal management. Government support for digital transformation further strengthens investment across sectors. Global tech firms are partnering with Taiwanese players to expand capacity. Cloud providers are also scaling up local zones to support AI integration. AI model complexity requires higher compute, power, and network efficiency. Taiwan’s position in the global semiconductor supply chain boosts ecosystem reliability. It plays a central role in regional AI deployment strategies.

- For instance, in November 2024, Taiwan’s government launched a USD 3 billion, three-year plan specifically for AI data centers to support workloads across sectors.

AI Hardware Innovation Driving Rack Density and Energy-Efficient Infrastructure

Demand for AI-optimized hardware is transforming design principles in the Taiwan AI Data Center Market. Integration of NVIDIA H100 and custom AI chips requires support for higher rack power densities. Operators adopt liquid cooling and modular power systems to meet thermal and efficiency requirements. The push for sustainability is leading to greener infrastructure using renewable energy contracts. Enterprises are redesigning data pipelines to support AI model inference at scale. Taiwan’s proximity to chip manufacturing enables early access to next-gen GPUs. Facilities are being designed with 50–100 kW racks for GenAI deployments. Infrastructure shifts align with enterprise AI priorities. The market supports long-term technology resilience.

Strategic National Focus on Digital Sovereignty and Edge Compute Expansion

The government’s focus on digital resilience makes the Taiwan AI Data Center Market strategically vital. National security policies encourage sovereign data storage for critical workloads. This drives local deployment of AI-focused colocation and cloud infrastructure. Demand for edge computing is rising due to latency-sensitive applications. Sectors like autonomous mobility, healthcare imaging, and smart cities prefer AI data centers closer to users. Regional telcos expand fiber backbone to support this edge growth. National AI strategies also support localized innovation in NLP and CV. Taiwan’s strategic location enhances its role in North Asia AI deployments. It supports regional cloud and compute continuity.

- For instance, Taiwan’s 5G rollout drives edge computing demand, with urban centers adding micro-sites for low-latency applications in smart cities and mobility.

Enterprise AI Integration and Cloud Adoption Fueling Market Expansion

Enterprise adoption of AI models in NLP, ML, and CV is fueling cloud migration. Hybrid AI environments are now the standard across medium and large businesses. The Taiwan AI Data Center Market benefits from demand for scalable and elastic compute. System integrators offer orchestration layers to manage multi-cloud and on-premise AI workloads. Enterprises are investing in AI lifecycle tools, requiring secure and high-speed compute access. Cloud-native architectures are optimized for containerized AI model deployment. Enterprise-led demand drives service innovation in AI-as-a-service. It strengthens Taiwan’s relevance for both regional and global AI integration plans.

Market Trends

Rise of Liquid Cooling Technologies in High-Density AI Workloads

The Taiwan AI Data Center Market is witnessing strong adoption of liquid cooling systems. High-performance AI models increase thermal load, making traditional air-cooling inadequate. Operators are investing in cold-plate and immersion cooling to manage heat. These technologies support AI racks exceeding 50 kW capacity. Liquid cooling reduces PUE while supporting dense GPU configurations. Vendors design facilities with modular layouts for cooling retrofits. Demand for sustainability further encourages this shift. Technology innovation focuses on efficient fluid dynamics and heat reuse. Taiwan’s energy-conscious environment accelerates this cooling evolution.

AI-Specific Colocation Services Gaining Market Momentum

AI-focused colocation services are rising in demand from enterprises and research firms. Taiwan colocation providers offer customized rack space for AI servers and accelerators. Services include high-power circuits, low-latency fiber links, and AI-ready thermal management. Enterprises prefer colocation for faster AI model deployment and scaling. It allows direct access to cloud on-ramps and dedicated network routes. Service differentiation includes GPU rental and model orchestration support. Global AI players seek partnerships with local colocation leaders. Taiwan AI Data Center Market benefits from its neutral interconnect ecosystem. This trend reshapes traditional colocation models.

Integration of AI in Data Center Operations for Predictive Efficiency

Data center operators are integrating AI in infrastructure management systems. Predictive analytics help optimize cooling, power, and resource usage. AI-driven DCIM tools forecast hardware failure and manage maintenance schedules. This reduces downtime while improving operational cost efficiency. Machine learning models adjust cooling and power supply based on real-time usage. Taiwan’s tech-savvy ecosystem supports rapid testing of such AI tools. It ensures resilient and responsive infrastructure. Operators adopt autonomous management to scale GenAI environments. Taiwan AI Data Center Market becomes a testing ground for AI-in-AI ops.

Edge AI Data Centers Supporting Low-Latency Workloads in Urban Zones

Edge data centers tailored for AI use cases are emerging across Taiwan’s urban areas. Smart city deployments, autonomous transport, and real-time surveillance require low-latency inference. Edge nodes integrate compact GPU servers with high-speed connectivity. Operators focus on sub-5 ms latency zones for critical applications. AI edge deployments complement centralized training in hyperscale facilities. Telecom firms lead this expansion using distributed micro data centers. Taiwan AI Data Center Market evolves toward hybrid topology with edge and core interlink. Urban density supports fast rollout of edge AI capacity.

Market Challenges

Power Supply Constraints and Grid Stability Issues in High-Density Zones

The Taiwan AI Data Center Market faces challenges in securing stable and scalable power. High-density AI racks increase electricity demand beyond traditional levels. Grid limitations in urban zones slow down new deployments. Permitting delays and power allocation restrictions create capacity bottlenecks. Taiwan’s renewable energy transition poses intermittency risks for AI workloads. Infrastructure upgrades are costly and time-consuming. Data centers must invest in energy storage and backup systems. Regulatory compliance adds complexity to power procurement. It affects deployment timelines and operational cost.

Land Scarcity, Seismic Risks, and Zoning Limitations in Urban Taiwan

Securing suitable land for AI data centers is becoming difficult in major Taiwanese cities. Limited availability drives up costs in Taipei, Taoyuan, and Hsinchu regions. Zoning rules restrict large-scale deployments near residential zones. Taiwan’s seismic activity demands reinforced building codes and advanced resiliency planning. Developers face added costs to meet earthquake-proofing standards. Environmental permitting slows down new project approvals. Coastal locations offer space but raise flood-resilience concerns. These factors impact long-term planning for high-capacity facilities. It makes expansion more complex and capital-intensive.

Market Opportunities

Semiconductor Leadership Creating Edge in AI-Driven Infrastructure Scaling

Taiwan’s global leadership in semiconductor manufacturing enables early access to advanced AI chips. Integration of homegrown and partner silicon enhances system-level optimization. This allows customized AI infrastructure for specific workloads. The Taiwan AI Data Center Market leverages its chip industry to attract global cloud and AI leaders. It positions the country as a critical innovation hub for AI-native data center design.

Cross-Border AI Services and Regional Cloud Zones Driving Export-Led Growth

Global AI firms view Taiwan as a base for serving North Asia and Southeast Asia. Data centers offer sovereign-compliant zones while supporting regional exports. Taiwan supports regulatory alignment with cross-border partners. AI data centers become a service-export tool for advanced model hosting and deployment. This creates growth beyond domestic demand.

Market Segmentation

By Type

Hyperscale facilities lead the Taiwan AI Data Center Market, accounting for the largest share due to rising demand from cloud service providers and tech firms. Colocation and enterprise data centers are growing fast as companies shift from legacy infrastructure. Edge and micro data centers are emerging for latency-sensitive AI use cases in urban and industrial zones.

By Component

Hardware dominates the Taiwan AI Data Center Market, driven by GPU accelerators, high-speed networking, and liquid cooling systems. Software and orchestration tools are gaining traction with enterprises adopting hybrid AI deployments. Services segment is expanding as businesses seek AI infrastructure management, integration, and consulting capabilities.

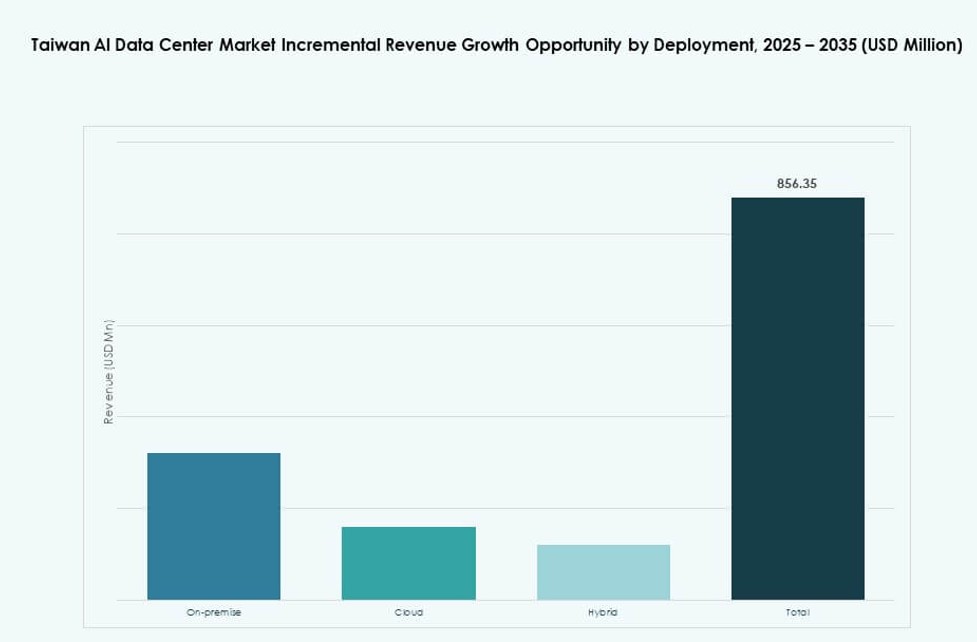

By Deployment

Cloud deployment holds the largest market share due to its scalability and integration with AI platforms. Hybrid models are rapidly expanding as businesses blend on-premise control with cloud agility. On-premise deployments remain relevant in BFSI and government sectors, where data sovereignty and security matter.

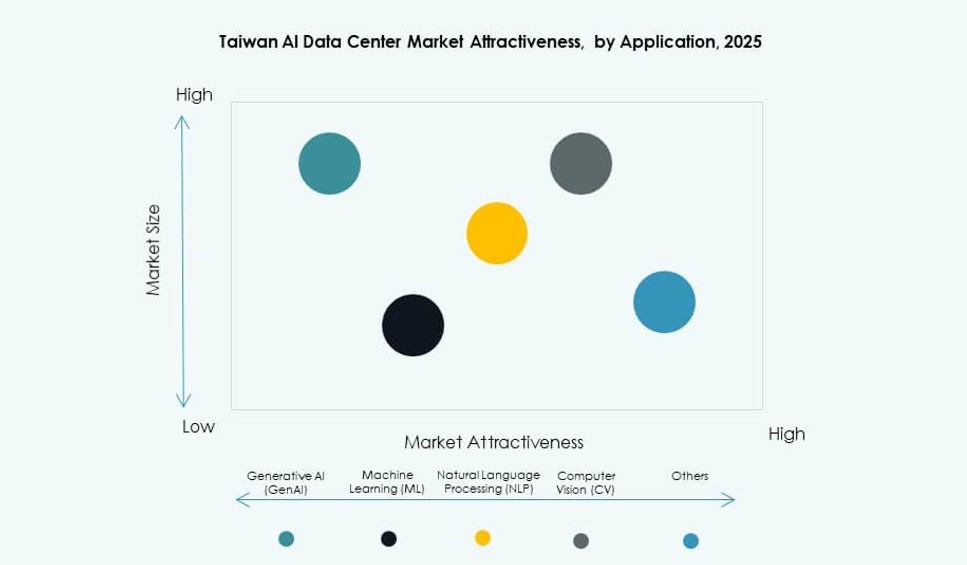

By Application

Machine Learning is the dominant application in the Taiwan AI Data Center Market, widely adopted across financial and industrial sectors. Generative AI is gaining momentum in content creation and virtual services. NLP and Computer Vision follow, driven by chatbots, fraud detection, and smart city surveillance systems.

By Vertical

IT and Telecom lead the Taiwan AI Data Center Market, with AI driving network automation and service innovation. BFSI, Healthcare, and Manufacturing are fast adopters, deploying AI to improve efficiency, compliance, and productivity. Media & Entertainment leverages AI for real-time streaming and personalization. Retail and Automotive are catching up with vision-based AI systems.

Regional Insights

Northern Taiwan Leading Market Share with Hyperscale and R&D Clusters

Northern Taiwan, including Taipei, New Taipei, and Hsinchu, holds over 60% share of the Taiwan AI Data Center Market. The region benefits from proximity to semiconductor R&D centers and strong power-grid infrastructure. Taipei’s enterprise base and government institutions support demand for AI cloud services. Hsinchu houses tech parks that drive AI testing and model deployment.

Central Taiwan Supporting Edge and Manufacturing-Driven AI Use Cases

Central Taiwan accounts for about 25% of the market, led by Taichung and Changhua. The region hosts manufacturing zones requiring AI for smart factory operations. Growing demand for edge compute supports micro data center development in industrial hubs. Its balanced land availability and power resources enable stable AI infrastructure growth.

- For example, Foxconn is deploying Nvidia-powered AI robots and smart workcells in its Taichung factories as part of its 3+3 strategy. In Taiwan, it is also building a $1.4 billion AI supercomputing cluster with Nvidia, set to be fully operational by mid-2026.

Southern Taiwan Emerging with Renewable Energy Integration and Port Connectivity

Southern Taiwan contributes roughly 15% of the Taiwan AI Data Center Market. Cities like Tainan and Kaohsiung offer space, fiber connectivity, and renewable energy access. Large infrastructure projects are underway near port zones to support AI training and model hosting. The region’s strategic location helps serve Southeast Asian clients efficiently.

- For example, TSMC is building three new 2nm fabs in Taiwan’s Southern Science Park to meet rising AI chip demand. These facilities are expected to begin mass production by 2026 as part of TSMC’s advanced node expansion strategy.

Competitive Insights:

- Chief Telecom

- Taiwan Fixed Network Data Centers

- Giga Computing

- Equinix

- Digital Realty Trust

- Microsoft (Azure)

- Amazon Web Services (AWS)

- NVIDIA

- Google Cloud / Alphabet

- Hewlett Packard Enterprise (HPE)

The Taiwan AI Data Center Market is shaped by global hyperscale players, regional telecoms, and hardware innovators. Cloud providers like AWS, Microsoft, and Google dominate through scalable infrastructure and AI-ready zones. Chief Telecom and Taiwan Fixed Network serve local demand with sovereign-compliant facilities. NVIDIA and Giga Computing strengthen the ecosystem with AI-optimized hardware and accelerated servers. Equinix and Digital Realty Trust lead in colocation, targeting enterprise workloads. Competition is driven by differentiation in rack density, energy efficiency, and AI service integration. It supports hybrid cloud adoption, AI model hosting, and vertical-specific deployments. Taiwan’s semiconductor ecosystem gives local firms a unique edge in integrated design.

Recent Developments:

- In January 2026, Empyrion Digital broke ground for its first Taiwan data center (TW1) in Taipei’s Neihu district, featuring 7MW scalable IT load for AI and cloud computing. The facility supports liquid cooling and high-density racks, with service readiness targeted for Q4 2027.

- In July 2025, Foxconn Formed a Strategic Partnership with TECO Electric & Machinery. Foxconn partnered with TECO Electric & Machinery to co‑develop AI data center infrastructure, combining server, cooling, and power expertise to accelerate global deployment beyond Taiwan.

- In June 2025, AWS launched the Asia Pacific (Taipei) cloud region with a $5 billion investment in local data centers, including a Direct Connect location at Chief Telecom’s HD site.