Executive summary:

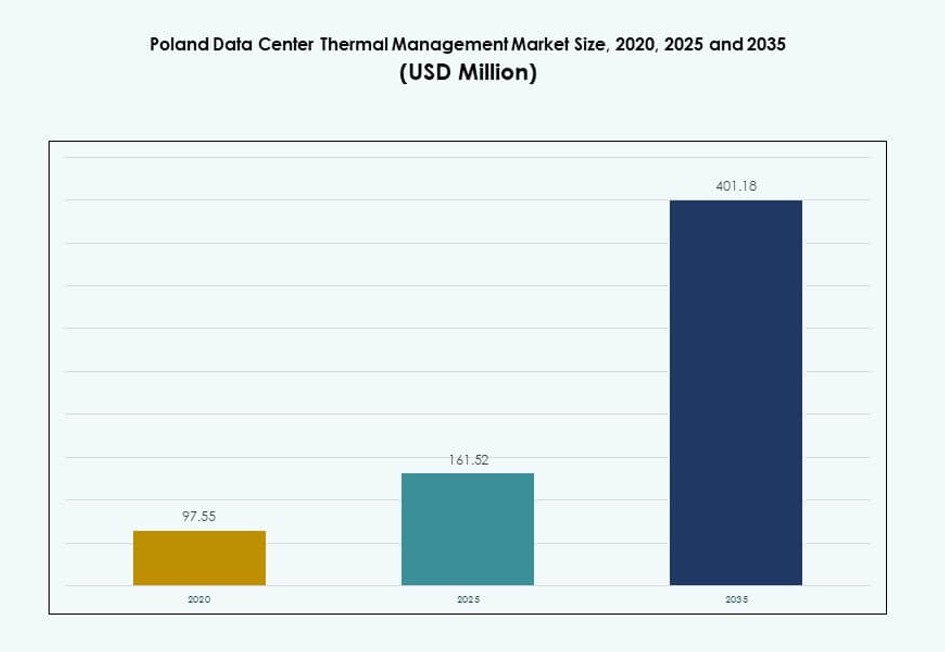

The Poland Data Center Thermal Management Market size was valued at USD 97.55 million in 2020 to USD 161.52 million in 2025 and is anticipated to reach USD 401.18 million by 2035, at a CAGR of 9.46% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Poland Data Center Thermal Management Market Size 2025 |

USD 161.52 Million |

| Poland Data Center Thermal Netherlands Market, CAGR |

9.46% |

| Poland Data Center Thermal Management Market Size 2035 |

USD 401.18 Million |

The market is gaining momentum as data centers deploy high-density computing systems that require advanced thermal solutions. Rapid AI adoption, IoT expansion, and cloud growth are pushing infrastructure to optimize cooling for performance and energy efficiency. Companies are shifting to liquid cooling, AI-driven thermal automation, and modular cooling units. Innovation is key to managing power usage and reducing downtime. Investors prioritize efficient thermal systems to meet ESG goals and support long-term asset performance. Businesses depend on optimized cooling to maintain uptime and protect equipment longevity. It plays a critical role in enabling future-ready digital infrastructure.

Western Poland leads due to strong industrial presence, connectivity to Germany, and active hyperscale projects. Central Poland, including Warsaw, shows high demand from enterprise data centers and national IT initiatives. Northern and eastern regions are emerging with investments in edge infrastructure, driven by smart city programs and telecom expansion. Regional distribution reflects digital infrastructure maturity, power availability, and proximity to user demand. It supports balanced market development across multiple zones.

Market Dynamics:

Market Drivers

Rising High-Density Workloads Accelerate Demand for Advanced Thermal Infrastructure

The Poland Data Center Thermal Management Market is expanding due to a sharp rise in high-density workloads. AI, machine learning, and big data applications require efficient heat dissipation systems. Traditional cooling setups fail to meet the thermal demands of dense server environments. This shift drives investment in precision air and liquid cooling technologies. Data centers with 20-30 kW per rack increasingly depend on rear-door heat exchangers and liquid cooling. Hardware optimization and modular designs reduce energy consumption while improving reliability. Businesses prioritize thermal management to avoid downtime and increase server lifespan. The need for scalable cooling infrastructure positions Poland as a key investment hub.

- For instance, Equinix’s Warsaw IBX® data centers deliver highly connected colocation infrastructure with robust cooling redundancy and industry energy certifications to support mission‑critical operations. These facilities use advanced design practices to maintain efficient temperatures and enable high‑performance workloads within dense server environments.

Strategic Enterprise Expansion and Rising Colocation Investments Boost Infrastructure Modernization

Growing digital transformation among enterprises and cloud service providers pushes demand for efficient cooling systems. Colocation operators expand capacity to attract hyperscale clients. Efficient thermal infrastructure becomes a key differentiator in service-level agreements. Poland offers favorable energy pricing, location proximity, and regulatory clarity, making it a prime data center destination. Thermal management systems form the backbone of uptime guarantees. Enterprises migrating legacy workloads depend on integrated cooling to maintain SLA compliance. Retrofit projects increase, focusing on energy-efficient upgrades. Investors are drawn to stable returns driven by digital infrastructure growth.

Stringent Energy Efficiency Regulations Encourage Sustainable Cooling Innovations

Energy usage regulations in the EU push operators to improve power usage effectiveness. Poland follows EU standards, encouraging the adoption of sustainable thermal systems. Operators explore alternatives like liquid immersion, free-air cooling, and AI-optimized airflow. The Poland Data Center Thermal Management Market evolves with this policy pressure. Government subsidies support green infrastructure upgrades. Heat recovery systems reduce environmental impact and operating costs. Energy audits make efficient cooling a compliance necessity. It boosts investor confidence and long-term infrastructure funding.

Surging AI and IoT Integration Forces Shift Toward Adaptive and Modular Cooling Models

Integration of AI, IoT, and edge computing drives changes in thermal architecture. Distributed computing nodes require local, efficient cooling setups. Edge data centers in Poland depend on rack-based solutions to manage space and thermal loads. Modular cooling systems allow fast deployment and easy scaling. Adaptive cooling technologies ensure temperature optimization across variable workloads. Smart DCIM software enables predictive failure detection and airflow control. The Poland Data Center Thermal Management Market aligns with this decentralized computing model. It attracts attention from smart city developers and telecom operators seeking thermal resilience.

- For instance, Vantage Data Centers’ Warsaw campus spans a 12‑acre site with two data centers delivering a combined 48 MW of critical IT capacity and features efficient cooling systems designed for high performance and sustainability.

Market Trends

Adoption of Liquid Cooling Solutions Gains Ground Across Hyperscale and AI Workloads

Hyperscale facilities in Poland increasingly adopt liquid-based cooling technologies. These systems support high-density servers used in AI and GPU-based tasks. Direct-to-chip and immersion cooling reduce reliance on airflow and increase thermal efficiency. Hyperscale players favor this transition for its sustainability benefits. Data centers achieve lower PUE levels and reduce water usage. The Poland Data Center Thermal Management Market supports this trend through regional deployments. Manufacturers partner with hyperscale clients for tailored solutions. Liquid cooling becomes central to meeting rising thermal density benchmarks.

Integration of Smart Thermal Management Platforms Driven by Software Intelligence

Operators deploy advanced thermal monitoring and control systems to improve efficiency. Smart DCIM dashboards and AI-driven platforms track real-time thermal conditions. These tools optimize airflow, manage rack heat zones, and minimize hotspots. It ensures thermal consistency and reduces energy waste. CFD simulation helps visualize cooling distribution before implementation. The Poland Data Center Thermal Management Market supports this digitization of infrastructure. Software integration improves performance and speeds up incident response. Vendors increasingly bundle software modules with hardware for end-to-end solutions.

Use of Renewable Cooling Sources Like Groundwater and Airside Economizers Increases

Green data centers in Poland are integrating renewable thermal solutions. Use of groundwater loops and airside economizers improves efficiency and sustainability. These systems lower dependency on mechanical refrigeration. Facilities near lakes or cooler regions benefit from low-cost natural resources. It aligns with ESG goals and national decarbonization policies. The Poland Data Center Thermal Management Market includes operators redesigning older sites to support such methods. Lower carbon footprints attract institutional investors focused on sustainability metrics. Future data centers are planned with natural cooling as a design baseline.

Shift Toward Modular and Prefabricated Cooling Units for Fast Deployment

Operators adopt modular thermal systems to speed up deployment cycles. Prefabricated cooling modules integrate seamlessly with rack and row-based designs. They help reduce on-site construction timelines and enable faster scaling. It becomes critical for hyperscale and edge site rollouts. Modular chillers, heat exchangers, and airflow systems increase operational agility. The Poland Data Center Thermal Management Market benefits from this trend due to rising infrastructure rollouts. Prefab units ensure predictable performance and lower project costs. Vendors localize production to meet delivery speed expectations.

Market Challenges

Infrastructure Legacy Limits Compatibility with Next-Gen Cooling Technologies

Many data centers in Poland operate with aging cooling setups that lack flexibility. Legacy air-based systems can’t manage the thermal load from AI or GPU-intensive tasks. Retrofitting these facilities requires downtime, high costs, and structural redesign. Operators face challenges in integrating liquid cooling in old room-based layouts. It reduces readiness for high-density deployment. The Poland Data Center Thermal Management Market sees delays in upgrade decisions. Resistance to early adoption limits innovation cycles. Businesses face tough choices between maintaining uptime or upgrading infrastructure.

Rising Energy Prices and Regulatory Pressure Impact Cooling Operating Budgets

Thermal systems account for a large share of a data center’s energy usage. Rising electricity costs in Poland directly impact operational budgets. Operators must optimize cooling performance without compromising uptime. Regulatory limits on PUE and carbon emissions further increase pressure. Inefficient cooling setups face higher compliance risks. The Poland Data Center Thermal Management Market depends on balancing cost and regulation. Capital expenditure on modern systems creates short-term strain. Smaller operators delay investments, widening the technology adoption gap.

Market Opportunities

Expansion of Hyperscale and Cloud Zones Creates Demand for High-Efficiency Cooling

Poland’s rise as a regional data center hub brings large-scale cooling demand. Hyperscale expansions by global players require low-PUE systems from the start. Developers seek vendors with proven track records in high-density thermal design. The Poland Data Center Thermal Management Market gains from these long-term infrastructure commitments. It supports steady growth in cooling hardware and software demand. Energy-efficient thermal designs become key project enablers.

Edge Deployments and Smart Infrastructure Boost Opportunities in Compact Cooling Solutions

Edge computing growth fuels demand for rack-based and modular cooling units. Telecom and IoT deployments in regional towns create micro-data center needs. These sites need compact, low-power thermal setups with remote monitoring. It enables vendors to introduce lightweight and scalable cooling innovations. The Poland Data Center Thermal Management Market welcomes flexible systems that serve distributed infrastructure. Long-term opportunities arise in mobile, energy-aware thermal units.

Market Segmentation

By Data Center Size

Large data centers dominate due to hyperscale cloud deployment and government-backed digital infrastructure. These sites adopt advanced thermal systems for high-capacity workloads. Medium data centers show fast growth, supporting enterprise clients. Small facilities cater to edge workloads and remote access hubs. The Poland Data Center Thermal Management Market benefits from this diverse size-based demand.

By Cooling Technology

Air-based cooling leads in deployment due to cost efficiency, but liquid-based cooling grows fast. Direct-to-chip and immersion cooling gain traction in AI-based workloads. Hybrid systems balance performance and efficiency. Thermoelectric and phase-change methods find niche applications in high-performance racks. The market shifts toward flexible integration across workload types.

By Component

Hardware accounts for the largest share due to physical infrastructure investments. Cooling units, fans, heat exchangers, and piping remain essential. Software sees strong demand for smart optimization and monitoring. Services grow as operators seek upgrades, remote monitoring, and performance audits. The Poland Data Center Thermal Management Market shows growing reliance on integrated solutions.

By Hardware

Cooling units and chillers dominate hardware spending, driven by high-capacity rack demand. Fans and airflow devices remain vital for room-based layouts. Heat exchangers and rear-door units rise with liquid cooling adoption. Efficient piping systems support precise thermal delivery. The segment sees innovation in modularity and energy efficiency.

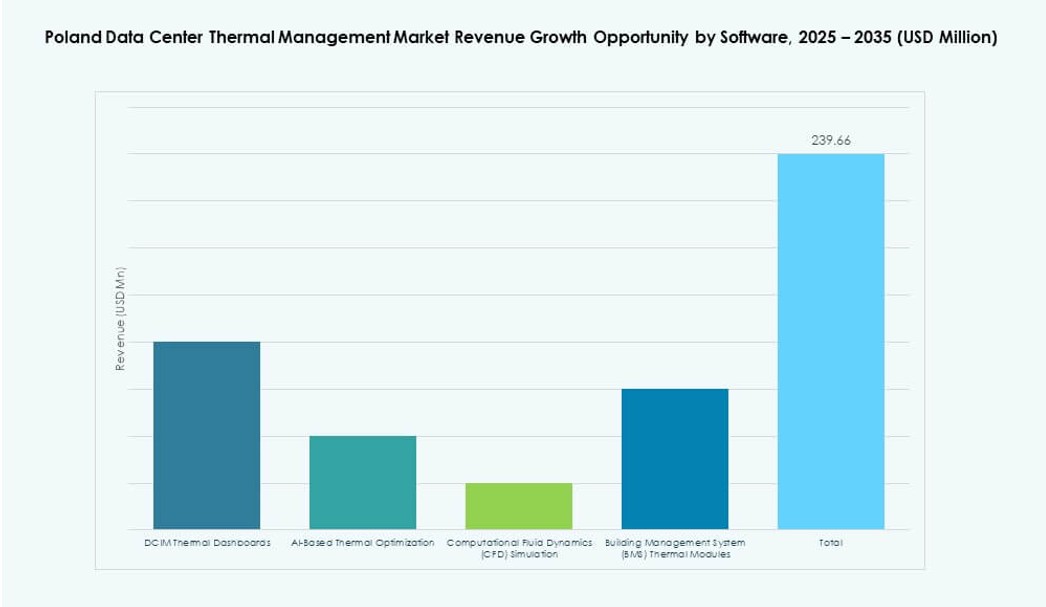

By Software

AI optimization and DCIM platforms lead software growth in thermal management. Operators rely on predictive insights to reduce thermal risk. CFD simulation helps plan airflow strategies before deployment. BMS modules connect thermal data with broader facility controls. The Poland Data Center Thermal Management Market sees rising bundling of software with hardware.

By Services

Installation and commissioning services form the base of project execution. Preventive maintenance and retrofits are key for uptime and compliance. Monitoring as a Service supports remote operation. Upgrades become frequent as workloads scale. The service segment gains traction among medium and enterprise data center operators.

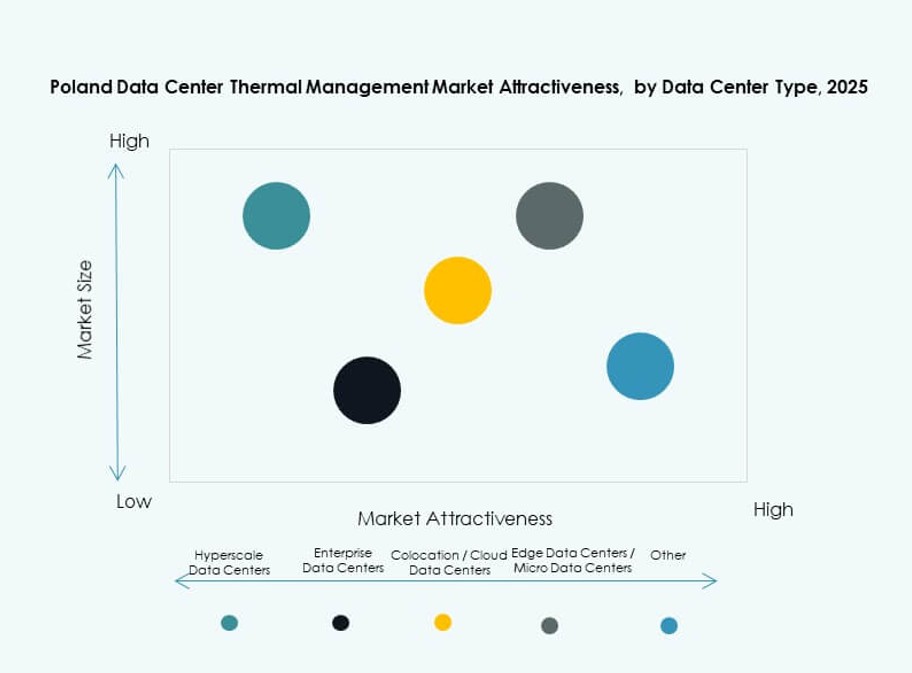

By Data Center Type

Hyperscale and colocation lead due to volume and efficiency needs. Enterprise data centers focus on customized thermal planning. Edge and micro data centers require compact, localized cooling setups. Other facilities such as government or financial institutions seek robust thermal uptime. The Poland Data Center Thermal Management Market spans all types with unique needs.

By Structure

Rack-based systems dominate in edge and AI environments. Row-based setups offer modularity and airflow control for growing sites. Room-based systems continue in legacy setups but lose share to more efficient designs. Vendors cater to structure-specific requirements with adaptable solutions. Structure-based segmentation shapes innovation directions.

Regional Insights

Western Poland Emerges as the Dominant Subregion with 42% Market Share

Western Poland leads the Poland Data Center Thermal Management Market, driven by strategic location and connectivity. Proximity to Germany, energy availability, and infrastructure readiness support growth. The region hosts key hyperscale projects and major colocation hubs. Operators benefit from cross-border digital traffic and low-latency access to Western Europe. Investments focus on liquid-based cooling and AI-ready infrastructure. It accounts for 42% of the market, supported by robust regional policy support.

- For instance, Beyond.pl’s Data Center 2 in Poznań operates with a PUE of 1.2, reflecting strong energy‑efficiency standards. The facility supports high‑density IT environments, with active halls designed for 20+ kW per rack and expansion readiness for higher densities.

Central Poland Accounts for 35% Share with Expanding Enterprise and Industrial Demand

Central Poland sees fast growth driven by enterprise demand and national infrastructure programs. Cities like Warsaw and Łódź serve as business and tech hubs. Colocation and private cloud operators scale cooling systems to match rising IT loads. The Poland Data Center Thermal Management Market benefits from grid modernization and talent availability. Investors find the central corridor attractive due to government incentives. The region holds 35% of the total market share.

- For instance, Atman’s WAW‑3 data center campus near Warsaw offers a substantial colocation footprint with over 19,000 m² of total space planned across three buildings. The first phase operates with precision cooling infrastructure designed to support high‑density workloads and advanced thermal control systems.

Northern and Eastern Poland Together Represent 23% with Edge and Telecom Expansion

Northern and Eastern Poland represent emerging demand zones, especially for edge and telecom-backed deployments. Cities near the Baltic coast and eastern border develop micro-data centers. Operators roll out modular cooling for low-density, remote sites. These subregions contribute 23% of the Poland Data Center Thermal Management Market. Infrastructure constraints exist, but targeted policies support digital penetration. New use cases in mobility and smart infrastructure spur thermal upgrades.

Competitive Insights:

- Vertiv Group Corp.

- STULZ Polska

- Schneider Electric SE

- Daikin Industries Ltd.

- Mitsubishi Electric Corporation

- Trane Technologies plc

- Airedale International Air Conditioning Ltd.

- Delta Electronics, Inc.

- Johnson Controls International plc

- Huawei Technologies Co., Ltd.

The Poland Data Center Thermal Management Market features strong competition among established global players and regional manufacturers. Vertiv, STULZ, and Schneider lead with advanced cooling systems tailored for hyperscale and AI-ready data centers. Domestic firms like STULZ Polska and APEX-ELZAR focus on localized integration and retrofit services. Most companies offer hybrid product portfolios, combining precision hardware with smart software. Innovation centers on modular designs, liquid cooling, and AI-based thermal analytics. Players differentiate on efficiency, response time, and energy savings. It continues to attract foreign investment and strategic partnerships as demand for high-density cooling infrastructure grows. Vendor strategies focus on turnkey solutions, regional alliances, and green certifications to gain a competitive edge.

Recent Developments:

- In December 2025, Trane Technologies entered a definitive agreement to acquire Stellar Energy Digital adding modular liquid-to-chip cooling solutions and two assembly facilities to strengthen its data center thermal management offerings

- In September 2025, Atman launched the first phase of its new Warsaw data center campus featuring 14.4MW of IT capacity with advanced cooling readiness for high-density workloads.